Written by: Prathik Desai

Translated by: Block unicorn

I love exploring how cryptocurrency is changing the way money flows. It feels great, but the reality is far more complex. Just look at how large institutions have moved money over the past decade to understand the reasons behind it.

Transatlantic bank wire transfers still take one to two days. They have to go through intermediary banks, each step generating a reconciliation record, with customers needing to pay fees of about $25 to $45. This system is nearly the same as the architecture from the 1970s, only that email has replaced telephone communication and the SWIFT system has replaced a complex maze of cables. Of course, the speed of database operations has improved as well. But that’s about it. Time has not correspondingly shortened.

You might think this is a technical issue, but I believe it is more of a coordination issue.

Blockchain and stablecoins have existed for over a decade. However, they have never solved all the problems at once. Some blockchains and stablecoins provide the speed institutions need but publish all data under the guise of "transparency." Others balance speed and privacy but create isolated systems that cannot communicate with each other.

The problem with new technology is that it can easily intimidate large institutions operating in highly regulated industries, such as banks. To get them to migrate to new technology, it is crucial to ensure that all pain points are resolved in advance. Any issue that proposes to "solve after migration" simply won’t work.

After some time, this situation has finally begun to change. Ironically, banks are now turning to blockchain technology to avoid losing ground in the face of digital assets.

Last month, five U.S. banks launched the Cari Network, with combined assets exceeding $750 billion. This system converts ordinary deposits into digital tokens that can be settled instantly, operate around the clock, and are insured by the Federal Deposit Insurance Corporation (FDIC).

In today’s in-depth analysis, I will introduce how blockchain developers have tried to build solutions for institutions in the past and what is different this time.

Missed opportunity

About a decade ago, alliances like R3 and Hyperledger built private blockchains for institutions, which had ambitious development roadmaps and included world-class financial institutions such as BNP Paribas, Citigroup, and Barclays. Although these blockchains ran smoothly and kept accurate ledgers, they were isolated and could not interact with anything outside the closed infrastructure.

These efforts gradually faded away. Others turned to different approaches.

Subsequently, banks began experimenting with public blockchains—primarily Ethereum. It immediately addressed the issue of composability. A shared, neutral ledger accessible to everyone allowed banks to interact within their respective ecosystems. However, solving one problem would trigger another. On public chains, anyone who knows how to look can see every counterparty, every transaction, and every balance using a browser.

Banks need a single system that can provide privacy, compliance, speed, and connectivity.

What has changed

By 2025, there were two breakthroughs: one technological and one demand-related.

First, let’s understand the technology. Zero-Knowledge Proofs (ZK Proofs) gained attention due to their unique advantages. A ZK proof is a cryptographic method that allows you to prove the validity of a transaction without revealing its details.

Although this technology has been around for years, it only became cheaper and quicker recently. In the past, generating these proofs was extremely costly, making deploying the entire system impractical from a commercial perspective.

The number of transactions processed per second has jumped from a low of 400 to at least 15,000. The time required to finalize transactions has been reduced to less than one second. All of this has been achieved while ensuring the privacy of transactions and their parties. In contrast, traditional financial infrastructure takes at least a day to process these transactions.

ZK Proofs also address another barrier perceived by enterprises.

In 2018, one bank had to hire engineers to build a blockchain from scratch when evaluating blockchain technology, figuring out how to generate proofs, running their own servers, and verifying whether all of this could transform into commercial benefits. It’s worth noting that they weren’t even sure if this system would be feasible at that time.

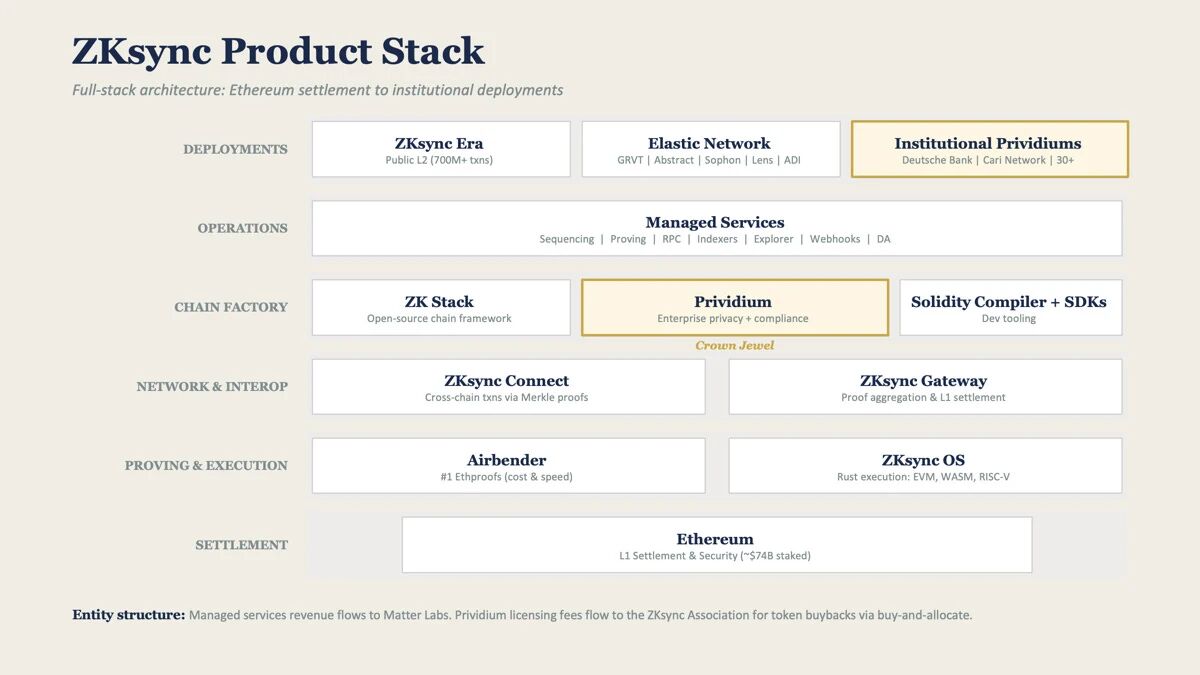

ZKsync, developed by Matter Labs, is an Ethereum scaling platform that addresses this issue by providing blockchain-as-a-service (BaaS) to enterprises. Its institutional product suite (including Prividium, Connect, Gateway, etc.) offers chain deployment, transaction processing, proof generation, compliance tools (including KYC checks, role-based access control, login control), and connections to other blockchains.

This tech stack allows enterprises to customize configurations and begin deployment. It can be understood as purchasing blockchain as a service.

ZKsync is not the only company offering such solutions. The Canton Network, backed by Goldman Sachs, DTCC, Citadel, and BlackRock, takes a different approach. It does not use zero-knowledge proofs but employs a permissioned model where authorized validators coordinate private transactions among known counterparties.

They are all building the connectivity layer required by institutions. However, there is disagreement on whether trust should be established through cryptographic proofs or through contract governance among known participants.

In my view, there is currently almost no difference between permissioned and non-permissioned approaches. Both aim to solve the same problem for institutions. In fact, Canton’s institutional partners are even more prominent than ZKsync.

However, certain features of ZKsync may encourage institutions to adopt its use. As long as interactions and flows of funds occur between known participants within familiar jurisdictions, Canton’s permissioned network can operate smoothly. Yet when enterprises wish to expand across jurisdictions and transact with parties outside of Canton’s closed jurisdiction, ZKsync can help enterprises achieve cross-jurisdictional composability.

It is this technological breakthrough that has prompted banks to adopt blockchain technology.

But why would banks abandon their long-standing, proven systems even if those systems are slow? Just because there are cheaper, faster alternatives?

Do you really think banks would suddenly shift from "blockchain is interesting but impractical" to "blockchain is commercially viable" just because a technology they knew little about suddenly became economically feasible? Interestingly, every time enterprises begin to lose money, every technology is granted "strategic importance."

Resources under siege

Over the past decade, the stablecoin market has reached $300 billion. They have done what banks have refused to do for years: transfer funds quickly. Nowadays, every circulating digital dollar has departed from the banking system.

The infrastructure I mentioned earlier, such as ZKsync's Prividium and Canton's permissioned payment system, is key to helping these banks reclaim market share in digital assets. With these blockchain-as-a-service (BaaS), banks can transfer existing deposits just like stablecoins and process and settle transactions with the same speed and finality. Additionally, there’s an added benefit: banks can provide regulatory protection and balance sheet advantages that only they can offer while achieving all these objectives.

This situation is already occurring in real life.

The Cari Network launched last month by five U.S. regional banks (Huntington Bank, First Horizon Bank, M&T Bank, KeyCorp Bank, and Old National Bank) is tokenizing bank deposits on the ZKsync Prividium platform. These deposits remain on the banks’ balance sheets, insured by the FDIC, and settle in seconds.

The Cari Network is not an isolated incident.

In February 2026, the Central Bank of the UAE approved DDSC, a stablecoin backed by dirhams, running on the ADI Chain, built using ZKsync's proof engine.

In June 2025, Deutsche Bank began building a tokenization platform on a ZKsync-supported chain, reducing the time to establish new funds from months to weeks.

The future of institutional finance

When writing finance articles, I often ponder a central question: “How will money flow in the future?” This is a question worth considering, as it reveals the financial behaviors of individuals and enterprises.

I believe that most people, regardless of their group, do not care much about the core principles represented by cryptocurrency. Banks care even less. I am sure that the leadership teams of banks are not sitting in boardrooms debating the merits of decentralization versus centralization. They certainly do not care whether their transactions are processed on Ethereum, Solana, or some private network located in Timbuktu.

What they care about most are privacy, composability, and speed. If a system can help enterprises save a few dollars while meeting these needs, it will capture their attention. If there is also a reason for adopting new technology that has "strategic significance" (like a stablecoin revolution that could disrupt their business), that would be even more helpful.

Therefore, I anticipate that the integration of Web2 and Web3 finance will revolve around technologies that can transfer money more efficiently. This could be achieved through blockchains supported by ZKsync or Canton that can transfer tokenized versions of fiat currency. Alternatively, it might also come from dedicated payment blockchains being built by payment companies like Circle’s Arc, Stripe’s Tempo, and Stable.

I believe both solutions are equally viable. For banks that do not wish to adopt stablecoins, ZKsync's blockchain-as-a-service (BaaS) is clearly a more ideal evolutionary choice. Meanwhile, banks that have already integrated stablecoins into their payment systems will opt for blockchains supporting digital dollars.

But I am confident who the biggest loser will be: those who insist on using technologies that still transfer and settle funds based on date and time.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。