Author: Xiao Xiaopao

01

Macro analysis has two schools of thought, one is the "storytelling school" — focusing on the overall picture, historical rhythms, and cycles of civilization. After listening, you feel enlightened, but upon careful reflection, it cannot be proven or disproven. Its main function is to stimulate your hormones and make you feel like you are at the forefront of history.

The other is the "money-making school" — only concerned with one question: what do these stories mean for my position? This is the pragmatic approach. After all, at crucial moments, listening to stories does not help at all and often leads one astray.

If we apply this to the field of narrative analysis, then the first school manufactures narratives, while the second deconstructs them.

I have devised an indicator called the "Narrative to Reality Ratio"; or in simpler terms, the ratio between "at first glance" and "upon further reflection." Using Daniel Kahneman's framework in "Thinking, Fast and Slow," this represents the deviation between your "System 1" (fast intuitive response) and "System 2" (slow rational analysis).

This deviation will eventually be corrected. And the time lag that arises during the correction process may be our profit window.

To operate within this framework, we can break down information into "numerator" and "denominator."

Numerator: is the stuff that can overwhelm your senses in a short period: mainstream narratives, clickbait, media signals, various trending topics. They hit your emotions directly, triggering a stress response from System 1. After reading, your heart races, and your hands itch to place an order.

Such narratives often come from analysts, podcasters, and influencers who cater to the audience. They respect algorithms and traffic, not facts, nor you.

Denominator: is the foundational judgment. It requires you to calm down from the 90 seconds of hormonal shock (which is theoretically based: "the 90-second emotion rule"), to engage in severe thinking that is counterintuitive, uncomfortable, and even against human nature. This kind of analysis often comes from those who may be quite annoying, tend to ramble, but do not tell you which stock to buy; or who frequently challenge your comfort zone.

The work of the numerator can be delegated to AI, but the judgments of the denominator must be made by humans. So far, I have not seen any shortcuts.

For example, let's make a judgment on:

"Iran announces the reopening of the Strait of Hormuz"

"The Strait of Hormuz has been closed again"

"Trump prepares to launch airstrikes against Iran, destroying roads and bridges"

"Trump says he won't strike because victory has already been declared"

"The Strait of Hormuz is both open and closed, depending on whose ship and how much is paid"

Are these numerator or denominator?

These are clickbait, not numerator or denominator. Both the numerator and denominator are narratives; narratives should be a story, one that sounds reasonable and can drive people to action. But it does not necessarily reflect reality.

Let me give you another example, this time not clickbait:

02

Historically, there is a repeatedly occurring pattern: empires with excessive debt tend to shift their pressure outward when encountering internal problems. Small countries with too much debt only have difficult times. But great powers — such as the United States, historical Britain, and any previous empire — will adopt a more aggressive outward posture when internal contradictions accumulate to a certain extent.

This is not conspiracy theory; it is merely a historical pattern. Excessive debt makes politics more polarized and populist, leading to more radical decision-making.

So what is the way out of a debt crisis? Theoretically, there are three options: default, inflation dilution, and economic growth.

In reality, all three solutions exist, but mainly rely on the latter two: inflation dilution and growth.

The reason is quite simple: sovereign countries that can print their own currency will almost never default in name. The United States will not say, "I am defaulting on this national debt." Instead, it does something more elegant — achieving a de facto default through a gradual decrease in purchasing power.

Hence, inflation is not always a bad thing — it depends on how it comes about. If inflation is accompanied by increased productivity, it is less painful.

The 1990s to 2000s were a sweet time. Globalization, offshore outsourcing, and automation worked together to significantly lower manufacturing costs. Even though money supply grew continuously, ordinary consumers did not feel much price increase. Inflation mainly concentrated in areas not covered by this wave of efficiency revolution — medical services, education, and various industries requiring local labor.

When the benefits of globalization and manufacturing automation had mostly been consumed, AI arrived. AI began to lower costs in the white-collar service sector. Ideally, if the money supply grows by 8% each year, but AI-driven technological advances make things cheaper by 4%, consumers will ultimately experience inflation of only 4% — uncomfortable, but not revolutionary.

However, when debt continues to expand to a higher level, AI will no longer be effective. A different script must be adopted — war.

Once war becomes the main means, "inflation without productivity" will emerge. We will soon witness: countries spending massively on weapon production, but weapons will not produce anything; their sole function will be to destroy others' productive assets. Coupled with energy facilities being damaged and key shipping routes being threatened — this is a negative productivity shock. Things that were previously abundant suddenly become scarce and expensive. The outcome is global inflation.

At this point, do you feel this story makes sense? Is it on point? Is it numerator or denominator?

The logic appears coherent and reasoned, backed by historical facts and underlying financial system analysis, and seems like a relatively reliable narrative analysis.

However, it remains within our "comfort zone" understanding, as this is an overly simplified historical pattern, not the dynamically changing "reality."

So in my view, it is still the numerator.

03

So what should the denominator be?

When discussing the impact of "war" on the economy, it is easy to oversimplify.

Firstly, the modifiers before "war" are crucial. What we have observed from a distance in recent years (without personal experience) are "localized" wars, and localized wars affect each country differently; summed up, it might even round off to a positive outcome.

For the warring sides, or even multiple parties, the destruction is undoubtedly significant. Not only economically, but the populace also suffers. However, for regions that are not involved in fighting, theoretically it can instead stimulate demand and growth. The most obvious example is the economic growth of the United States during World War II, which can even be described as "rapid."

For instance, during the Russo-Ukrainian War, Japan presents an even more interesting case:

Japan has long been trapped in a deflationary trap — companies hesitate to raise prices, salaries do not increase, and consumption lacks motivation; weak consumption leads firms to further hesitate about raising prices. Nothing moves, and the economy remains stuck. Japan has been in this state for 30 years. Until the Russo-Ukrainian War broke out.

The Russo-Ukrainian conflict brought about global inflation, and the external price pressure actually pushed Japan out of that "no price increases" deadlock. The consumer price index reached a year-on-year growth rate of 4.3% in January 2023, and in the 2025 "spring battle," wages were negotiated to have an average increase of 5.3%, the highest in over 30 years. The same goes for Europe. The deflationary poison that had been lurking in these two economies for so many years was thus forcibly pushed out by war. (This inevitably makes one think of one's own country, as China is currently in a phase of low inflation bottoming out.)

Of course, the premise is that the impact of war is controllable and the duration is limited. Now the U.S.-Israel-Iran conflict has entered a new round, with energy tightening, and everything has become complicated. Europe, which had just started to show signs of improvement, is suddenly facing stagflation pressure — economic growth is slowing while inflation is rising simultaneously.

The European Central Bank (along with the Bank of England) has only one main task: to curb inflation. Their policy space is much smaller than that of the Federal Reserve; a slight misstep can lead to market punishment. Meanwhile, Japan, which had just been shaken out of deflation and was getting back on track, is now facing another type of pressure: the citizens are not pleased. The public's tolerance for rising prices is rapidly diminishing. Therefore, Japan has taken a very "Japanese" path: opting not to raise interest rates, but to distribute money and reduce consumption tax — absorbing monetary pressure through fiscal means.

04

Another narrative that is easily oversimplified is the story from the beginning. This is currently the most popular "numerator narrative": U.S. inflation is bound to explode, and the Federal Reserve will be forced to raise interest rates significantly, which will cause global markets to collapse.

It sounds logical and causally complete: after all, the Federal Reserve cannot print oil. But upon closer examination, it is based on an implicit assumption — that the energy crisis will inevitably become a U.S. inflation problem.

Many people overlook the fact that the U.S. is a net exporter of oil and oil products, with crude oil production reaching a record 13.6 million barrels per day last year. While rising oil prices may lead the public to complain at gas stations, from a macro perspective, the U.S. is actually one of the parties impacted the least.

Even more counterintuitively, with natural gas, the U.S. production is extraordinarily high — by 2025, daily production will be nearly 109 billion cubic feet, another historical high; thus, when export channels are restricted (for example, when LNG shipping encounters obstacles), domestic gas prices actually tend to decrease.

Additionally, the direct effects of the "Great Beauty" tax reduction policy — the after-tax wages of the base-level residents have actually increased. Some analyses estimate that just the tax reduction alone is enough to offset the impact of ongoing oil prices at the current levels for six months.

Thus, the actual impact on the U.S. economy is not significant; it may even be a beneficiary. Although rate cuts might be delayed, the urgency is not as great.

Further, while war may disrupt transportation and logistics physically, today’s supply chains are no longer a single massive chain — if any one link in the middle breaks, the whole chain is affected; it has become a vast, complex spider web. It is even distributed; if one node breaks, many other nodes can still connect. As for oil-producing countries, the divide is even larger: some have completely disrupted shipping, making it impossible to profit from high oil prices (for example, Kuwait or the UAE); while others are completely unaffected and are pure beneficiaries (such as Angola or even Venezuela).

Thus, the term "cocoon" is very fitting for the current global economy. Economies live in their own cocoons, possessing their own cyclic logic and methods for withstanding shocks.

The current global economy cannot simply and brutally be attributed to a single cause anymore. And the era where one could become a prophetic future-teller by narrating a grand story — if it ever existed — has indeed passed.

05

Returning to the denominator. In fact, war is just a sudden significant branch line, while your main line setting remains unchanged. The window for trading shocks will close, the half-life of emotions will expire, the shelf life of narratives will pass, and ultimately everyone's attention must return to the economy itself.

So what are the truly noteworthy "denominator-level" events at the moment?

I can think of, nearer in time:

Will there be a significant change in the direction of Federal Reserve policy, and will the new Federal Reserve Chair be smoothly appointed: the timing, rhythm, and extent of interest rate cuts, and who makes this decision, remains the most important single variable in global asset pricing.

Are there any significant changes in the fiscal and monetary policy statements of several major countries: how does the European Central Bank articulate under stagflation pressure, and the marginal changes in the Bank of Japan's tolerance for inflation; and in the second and third quarters, China's economic window, the strength and rhythm of growth stabilization will directly determine market direction.

Further out:

Are countries continuing their various de-dollarization arrangements? Quietly arranging, no shooting? For example, diversifying reserve assets? Promoting settlement in other currencies?

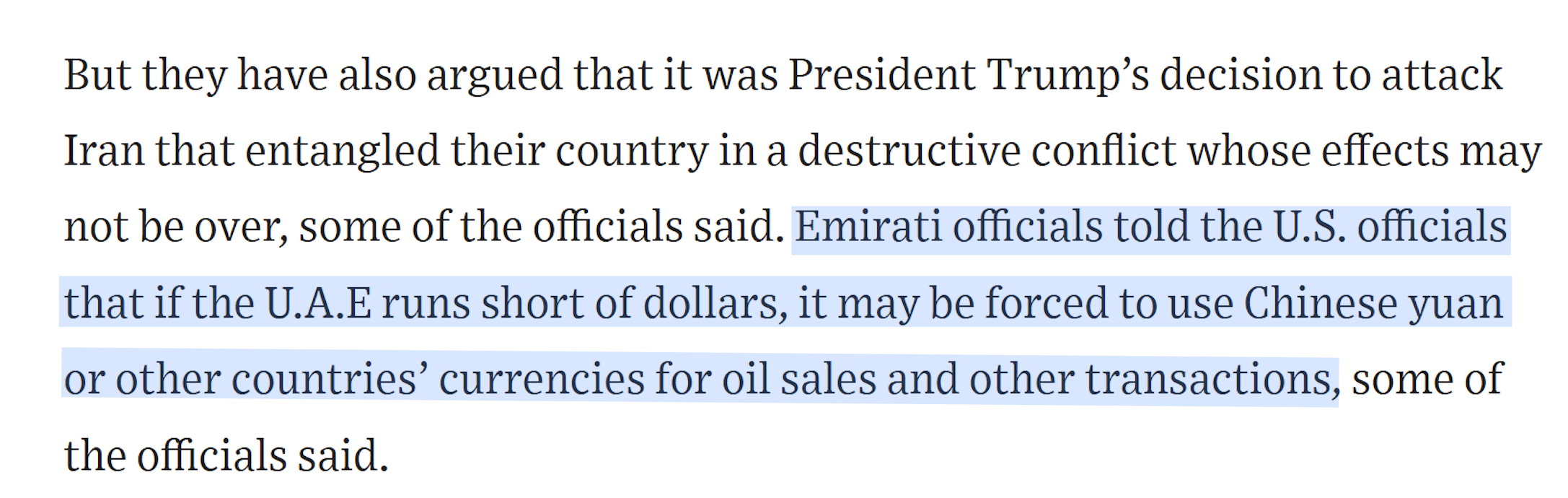

Do Middle Eastern princes still have enough dollars? Will they continue to swap with the U.S. or change it for renminbi?

(This is from today's Wall Street Journal report, it seems that it really is no longer enough. Moreover, it directly states that if there is truly no way, we will really have to switch to renminbi settlement.)

Has Europe awakened to strategic autonomy? If one day Europe truly achieves security and economic strategic autonomy, will it still need the U.S. and the dollar?

And: will renminbi assets increasingly resemble safe-haven assets? How strong is the resilience of the stock market? How long will bond prices rise and capital inflows continue? Will the renminbi still appreciate in the context of a strengthening dollar?

These denominators, while also a narrative, come from the experiences and work done by human analysts; they will not appear in daily news pushes, nor will they create jittery emotional fluctuations. But they will gradually correct the numerator.

In an age where narratives abound, the most scarce ability is not acquiring information — AI can already help you with that — but determining what is truly important amidst the noise of information. After all, the numerator will stimulate your hormones, while the denominator will protect your wallet.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。