Author: Pharos Research

This article systematically explains from the dual perspective of resource structure and political risk pricing why real-world assets (RWA) in the Middle East have long exhibited a structure characterized by a high concentration of real estate. The study shows that this phenomenon is not a result of short-term market choice, but rather a structural equilibrium shaped by the capital sedimentation path driven by the circulation of oil dollars, the long-term allocation preferences of sovereign capital, and the implicit screening mechanism of regulatory and political risks. On the resource level, the large-scale dollar liquidity released cyclically from oil revenues needs to find asset carriers with high capacity, stable cash flow, and value anchoring ability, making real estate the core capital reservoir. In terms of institutional and financial systems, real estate has advantages such as clear property rights, mature valuation systems, and a high degree of structuring and securitization, making it the asset type that can most easily complete the mapping from off-chain to on-chain. In the dimension of political risk, the Middle Eastern regulatory system forms an implicit prioritization mechanism for asset categories through compliance costs, approval paths, and information disclosure requirements. Due to its strong asset visibility, clear execution paths, and high binding with sovereign credit, real estate has become a politically acceptable asset recognized by regulators and investors. Meanwhile, the market preference shaped by sovereign capital over the long term further reinforces the dominant position of real estate in RWA through two-way transmission on both the supply and investment sides. Therefore, the essence of RWA in the Middle East has not reconstructed the asset system but is a technical extension of re-liquefying and repricing existing real estate assets. Its asset structure follows a three-layer mechanism of supply-side institutional screening + regulatory risk constraints + investment-side preference reinforcement. In the short term, the concentration of real estate will continue; whether it will move towards diversification in the medium to long term depends on the evolution path of economic structural transformation, financial system deepening, and regulatory risk preferences.

Keywords: RWA, real estate concentration, oil dollar circulation, sovereign capital allocation, political risk pricing

Phenomenon Definition: Why is the Asset Structure of Middle Eastern RWA Highly Concentrated in Real Estate?

1.1 Research Background and Problem Statement

From 2024 to 2026, RWA achieved a critical transition from concept-driven to scale implementation. According to data from RWA.xyz, as of March 30, 2026, the global on-chain RWA scale had exceeded $26.74 billion, with significant regional differences in development paths:

North America: Rapid expansion of interest rate assets represented by U.S. Treasury bonds

Europe: Fund shares and bill-type assets prioritized for compliant tokenization

Asia: Supply chain finance and small to medium-sized enterprise financing as main landing scenarios

In contrast, the Middle Eastern market exhibits markedly different structural characteristics, with real estate maintaining a long-term share of over 60% in RWA, significantly higher than the global average.

This concentration is not only reflected in asset distribution but is also evident across multiple key dimensions:

Priority directions of regulatory piloting

Issuance structure of sovereign or semi-official platforms

Investment-side capital allocation preferences

Actual survival scale of on-chain assets

Given the high policy openness and ample capital supply, the Middle East should have formed a diversified RWA asset system, yet the reality has shown significant convergence, with real estate becoming almost the only core asset class to achieve large-scale implementation. This structural contrast raises a critical question: why is RWA in the Middle East still locked into a single asset track under the dual advantages of institutions and capital?

For Pharos, this is not only a regional market issue but also a foundational infrastructure design issue. As a high-performance Layer 1 public chain, Pharos's core objective is to support large-scale on-chain and circulation of real-world assets, while the Middle Eastern market precisely provides the closest existing RWA sample for practical implementation. The phenomenon of asset concentration essentially reveals a key fact: on-chain asset structure is not determined by technology but is jointly shaped by institutional feasibility, risk pricing, and capital acceptability.

Therefore, the significance of studying RWA in the Middle East lies in:

(1) Clarifying which assets can truly enter the on-chain system (asset screening boundaries)

(2) Understanding how regulation and risks influence asset standards (compliance and structural design)

(3) Judging future asset diversification requirements for on-chain performance, contract structure, and liquidity mechanisms (infrastructure evolution direction)

Based on this, this article will analyze from four dimensions: asset distribution, project structure, capital allocation, and risk pricing, systematically dissecting the institutional screening and risk constraint mechanisms behind real estate concentration, and providing a reference framework for the next phase of RWA infrastructure adaptation.

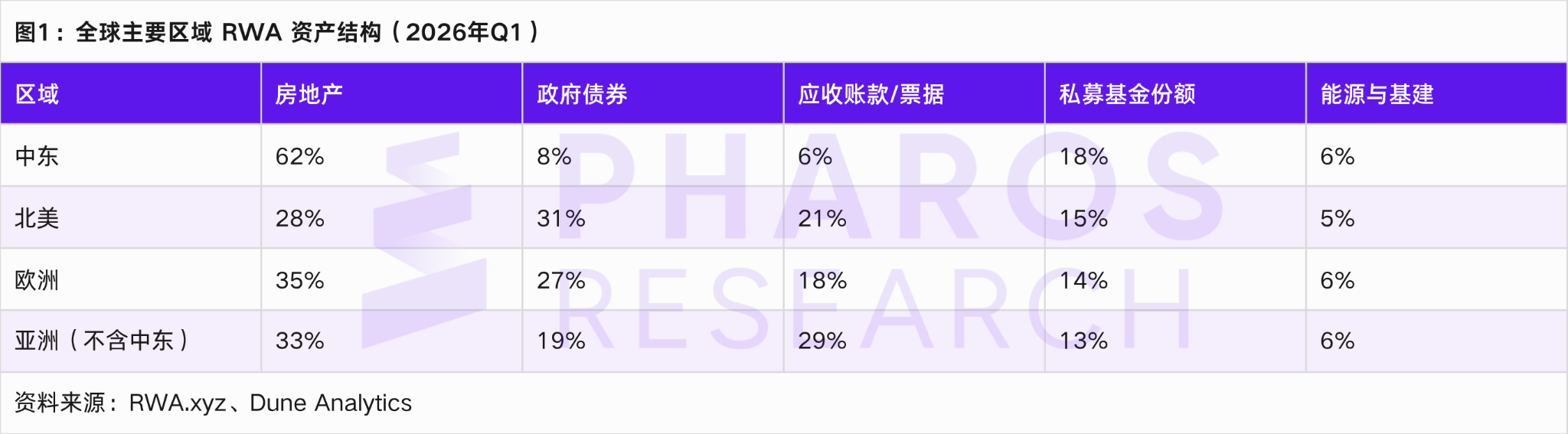

1.2 Regional Differentiation of Global RWA Asset Structure

According to statistics from RWA.xyz Q1 2026 data, global RWA asset distribution shows clear regional differentiation.

It can be seen that the asset structure in the Middle East exhibits three significant characteristics:

The proportion of real estate is significantly high (>60%)

Government bond assets account for significantly less than in North America

Accounts receivable and supply chain finance asset development is lagging

If explained solely from the perspective of technological maturity or regulatory openness, the aforementioned differences are difficult to substantiate. For example, the tokenization of North American Treasury bonds is based on institutional credit advantages, while Asian supply chain finance stems from financing demand drivers.

However, the Middle East does not lack capital or policy support, and the differences in asset structure are likely sourced from deeper economic structural and risk pricing logic. From global practice, the prioritized development path of different RWA asset types in various regions is closely related to their financial system characteristics: Western markets focus on government bonds and quasi-fixed income assets, relying on a mature interest rate system and institutional investor base; some Asian markets lean more toward consumer finance and supply chain financial assets, backed by the financing needs of small to medium-sized enterprises and platform-based risk control capabilities.

Therefore, rather than merely questioning why bond and bill-type assets have not prioritized development, it is more critical to examine the adaptability of different asset types within a unified comparative framework, including: clarity of property rights, stability of cash flows, execution difficulty, information transparency, regulatory sensitivity, and investor understanding costs.

Within this framework, the deployment sequence of different asset types is not accidental but is determined by their comprehensive performance across the aforementioned dimensions. It is under this multi-dimensional comparison that physical assets such as real estate often perform more harmoniously across multiple key dimensions, making it easier to achieve large-scale implementation in the early stages.

1.3 Verification of Concentration at the Project Level

From actual implementation projects, the phenomenon of asset concentration is further verified. A statistical analysis of disclosed RWA projects in the Middle East from 2024 to 2026 shows:

Real estate projects account for about 66%, primarily concentrated in Dubai, Abu Dhabi, and Riyadh.

Its typical structure is:

Setting up SPV in ADGM or DIFC

SPV holds property rights or long-term leases

Issuing income rights Token

Investors gain rental income and asset appreciation returns

In contrast, on-chain accounts receivable or corporate credit asset packaging are relatively rare in the Middle Eastern market.

This difference may not solely stem from investment-side demand structure but rather may be the result of a confluence of supply-side institutional convenience, regulatory acceptability, and investment-side preferences. For instance, compared to accounts receivable or corporate credit assets, physical assets like real estate have a more mature system of property rights and valuation, making it easier to gain regulatory approval and structural design support, thereby facilitating large-scale implementation on the supply side. Simultaneously, the investment side shows a stronger inclination to allocate to assets with collateral attributes, stable cash flow, and alignment with national strategies, while the acceptance of purely credit-based, non-physical assets is relatively limited. From a funding structure perspective, sovereign funds and high-net-worth investments long prefer large-scale, low-volatility assets, and this allocation logic also influences the choice of RWA asset types to some extent.

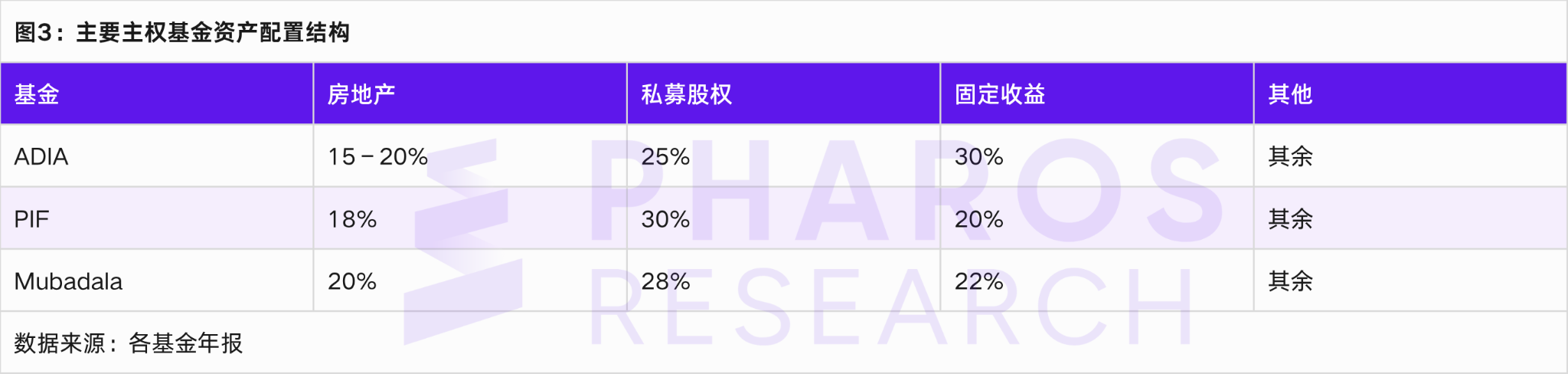

1.4 The Impact of Sovereign Capital Allocation on Asset Selection

The asset structure of Middle Eastern RWA is highly consistent with the long-term allocation preferences of sovereign capital, but this consistency is not coincidental; it is the result of sovereign capital long shaping local asset allocation preferences and market structures, indirectly translating into the choice of tokenizable assets. According to Global SWF data, as of March 2026, the major sovereign wealth funds were as follows: Abu Dhabi Investment Authority (ADIA) approximately $1.187 trillion, Public Investment Fund (PIF) approximately $1.151 trillion, and Mubadala Investment Company around $358 billion. Their asset allocation structure shows:

This allocation not only reflects the investment choices of sovereign funds but over the long term shapes the supply structure and pricing logic of the local asset market through capital flows and project preferences.

It can be observed that real estate, long considered a core allocation asset, possesses characteristics such as capability to accommodate large amounts of capital, stable cash flows, and high alignment with national development strategies. These characteristics not only meet the needs for sovereign capital allocation but also, over time, influence the asset supply direction of developers, the collateral and financing preferences of financial institutions, and the selection criteria for standardized assets by platforms. More importantly, sovereign funds do not directly participate in RWA issuance, but their long-term allocation behavior has established an implicit asset screening mechanism in the local market: a preference for large-scale, stable-return, collateralizable, and nationally strategic assets. This preference is progressively transmitted to the underlying asset choices of RWA projects through capital supply, financing structure, and asset development logic. In this transmission mechanism, developers, platforms, and funders, when selecting tokenizable assets, are more inclined to choose mature asset classes that have already been validated by sovereign capital, rather than attempting to introduce new assets that lack a historical allocation foundation. Thus, a key judgment can be made: RWA in the Middle East has not altered the existing asset allocation logic but is a technical extension and re-liquefying of existing real estate assets based on the asset structure shaped long-term by sovereign capital.

1.5 Political Risk Pricing and Real Estate Advantages

From a risk pricing perspective, real estate possesses significant institutional advantages.

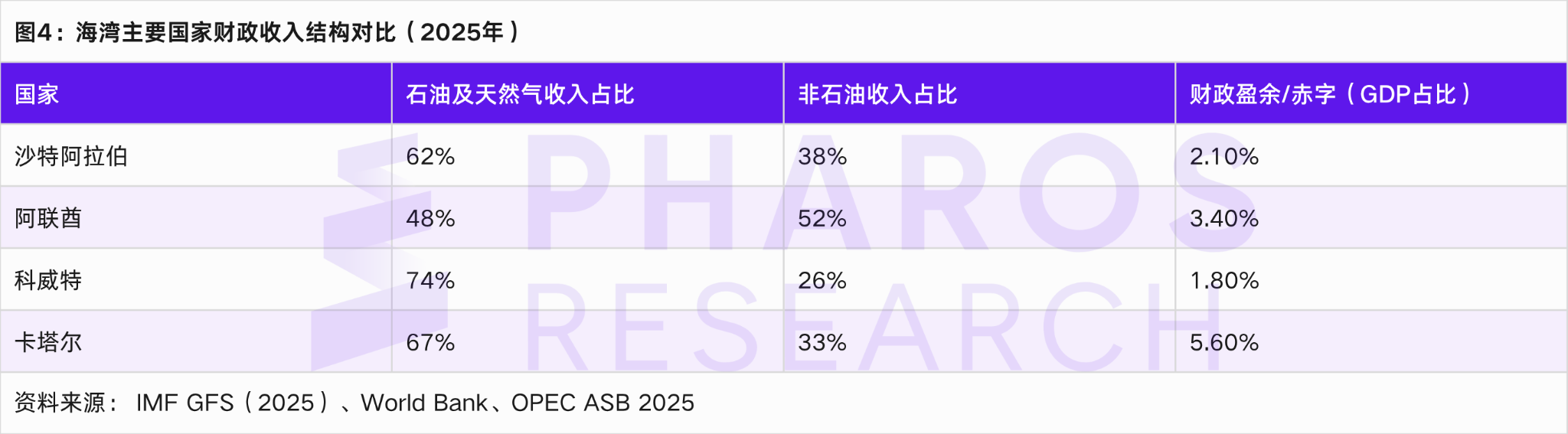

Middle Eastern countries generally rely on resource-based economic structures. According to the IMF's October 2025 updated "Economic Outlook for the Middle East and Central Asia" and related member countries' Article IV consultation reports, oil and gas revenues account for 40%-70% of fiscal revenues in Gulf countries. This structure generates: high volatility in fiscal revenues and a need for stable sedimentation carriers for capital. Within this background, real estate has threefold advantages:

Strong asset visibility and security: actual assets provide more certainty amid political and market fluctuations

High binding with national strategies: real estate is often directly linked to urban development and sovereign brand building

Significant policy attributes: visa, residency, and investment incentive policies (such as the golden visa mechanism) are all tied to real estate investments

In contrast, accounts receivable rely on corporate credit, bonds involve sensitivity to sovereign credit, and supply chain finance involves cross-border execution risks. High oil prices lead to liquidity expansion but do not automatically direct towards real estate; what truly makes it the preferred RWA target is that real estate simultaneously meets high capacity, visibility, standardized valuation, and policy alignment, while other assets often can only meet part of these criteria. In the comprehensive risk-return trade-off, real estate becomes the most acceptable tokenized asset class.

02 / Resource Structure Perspective: Oil Economy, Fiscal Structure, and Capital Outflow

The previous chapter explained the phenomenon of asset structure concentration towards real estate in Middle Eastern RWA from the results perspective; it further needs to answer: why can this structure continue to strengthen and exist stably over the long term? Mechanistically, this structure is not merely the result of a single market choice but is formed jointly by sovereign capital allocation logic, financial system behavioral preferences, and risk constraints. Therefore, this article analyzes the driving mechanism behind the concentration of RWA real estate in the Middle East from three dimensions: sources of capital, behaviors of financial intermediaries, and risk pricing mechanisms.

2.1 Oil Dollar Circulation and Real Estate Asset Sedimentation Mechanism

From the perspective of asset supply structure, the concentration of Middle Eastern RWA towards real estate is not due to a technical path choice but is determined by the long-term capital sedimentation result instigated by the oil dollar circulation mechanism. In other words, RWA is essentially the re-liquefying of an existing asset structure, rather than a reconstruction of asset sources.

Firstly, from the perspective of fiscal revenue structure, Gulf countries remain in a typical resource-based economic paradigm. According to the OPEC Annual Statistical Bulletin 2025, IMF Government Finance Statistics (2024–2025), and World Bank Data 2025, major oil-producing countries continue to exhibit a high degree of dependency of fiscal revenue on oil and gas resources, indicating significant cyclicality and external dependency in their fiscal revenue.

Even if countries like the UAE have increased their share of non-oil revenues, their fiscal surpluses remain highly correlated with oil price cycles. This structure leads to two macro outcomes: one is that national income exhibits significant cyclical volatility; the second is the formation of large amounts of dollar-denominated capital sedimentation during high oil price periods, which needs to be exported through long-term allocations.

From the capital flow perspective, the dollar income generated from oil exports does not fully enter current fiscal expenditures but is reallocated through sovereign wealth funds (SWF). According to real-time monitoring by SWFI and Global SWF, the total asset scale of the seven Gulf giants (ADIA, PIF, KIA, QIA, Mubadala, ADQ, ICD) had reached approximately $6 trillion by the beginning of 2026, with a significant portion long allocated to real estate and infrastructure assets.

In this context, real estate has gradually evolved into the core buffer for absorbing the fluctuations of the oil cycle. However, it should be further explained that the liquidity released during rising oil prices does not distribute evenly across all asset classes but exhibits a clear structural preference—private equity, infrastructure, and real estate together form the primary receiving directions. The reason why real estate ultimately occupies a dominant position within the RWA system is fundamentally due to its comprehensive advantages under securitization conditions being markedly higher than other asset classes.

From the capital flow path perspective, rising oil prices typically first drive sovereign wealth funds and high-net-worth capital to expand asset allocations; their funds undergo three layers of screening when entering risk assets: the first layer is asset return expectations (PE/VC have high elasticity but are longer in cycle); the second layer is liquidity requirements (bonds are highly liquid but have rigid returns); the third layer is structured securitization capability. Under this screening mechanism, although real estate's yield may not surpass that of PE, it possesses clear advantages in terms of property rights clarity, stable cash flows, and the potential for standardization, making it the most suitable type of asset to enter the RWA structure.

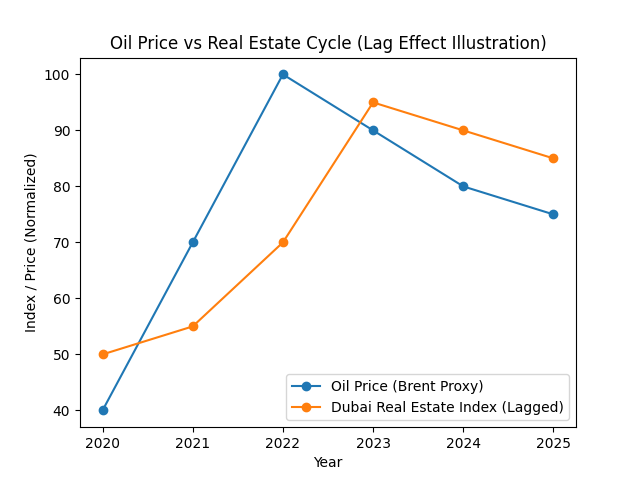

By comparing data from the U.S. Energy Information Administration (EIA) regarding Brent crude oil prices (2020–2025) and the Dubai Land Department's real estate index (2025 report), the following structural rules can be observed:

Oil price upcycle (e.g., 2006–2008, 2021–2023) → Real estate transaction volume and prices expand simultaneously

Oil price downcycle (e.g., 2014–2016) → Real estate prices enter an adjustment period

Real estate pricing typically exhibits a lag effect of 6–18 months to oil price changes

Figure 5: The cyclic relationship between oil prices and real estate prices

Source: Pharos Research

As shown in the figure, real estate prices do not change synchronously with oil prices but exhibit a significant lagged relationship. During the oil price up phase (e.g., 2021–2023), real estate prices usually enter an accelerated upward phase 6–18 months later; meanwhile, after a decline in oil prices, the real estate market does not immediately adjust but demonstrates certain price stickiness. This lagging + stickiness characteristic allows real estate to assume a liquidity buffering function in the oil cycle.

According to Dubai Land Department data, in 2025, trade volume in Dubai’s real estate increased by 30.64% year-on-year, reaching a nearly ten-year high; this growth cycle is highly consistent with oil price recovery since 2021. This leads to a crucial conclusion: real estate is not an ordinary asset class, but a storage device for oil income in the local economy.

On this structure, examining the asset selection logic of RWA becomes very clear—when on-chain assets require characteristics of stable cash flow + collateralizability + valuation anchoring, real estate naturally becomes the optimal underlying asset, rather than corporate receivables or SME financing assets.

Furthermore, from the perspective of cross-border capital flows, oil dollars do not remain entirely in the domestic market but are allocated overseas to core assets through sovereign funds. According to SWFI (2025) statistics, Middle Eastern sovereign capital has long-held positions in global core city (London, New York, Singapore) commercial real estate totaling over $200 billion and continues to increase. This dual-cycle allocation strategy reinforces the position of real estate within domestic asset systems—specifically, real estate is viewed as a cross-cycle, low sovereign risk asset with global pricing power.

Within this framework, the true function of RWA needs to be reinterpreted: it has not changed asset generation logic but provided a new liquidity outlet for already sedimented real estate assets, allowing assets that originally relied on bank credit or overall transaction exits to achieve finer-grained circulation through on-chain fractionalization. Therefore, the current real estate model of RWA in the Middle East can essentially be defined as: oil dollars → sovereign capital sedimentation → real estate value storage → RWA re-liquefaction four-layer structural model.

This structure also implies an important constraint: as long as the oil price cycle continues to dominate fiscal revenues, real estate's role as a capital reservoir will not change, and the development boundary of RWA will, to a significant extent, be subject to this macro mechanism rather than being driven purely by regulatory or technical factors.

2.2 Financial System Preferences and Asset Availability: Why Real Estate Has Preferred Securitization Conditions

In the RWA system, asset availability primarily depends on whether the asset possesses a legally recognizable and controllable property structure; thus, the property rights system itself is a prerequisite for asset availability. The macro resource structure determines capital flow, but what truly determines whether RWA can land is the underlying property rights system and legal execution structure. From global RWA practice, whether an asset has clear, executable, and transferable property rights is the primary prerequisite for completing the mapping from off-chain assets to on-chain certificates. The concentration of RWA in real estate in the Middle East is not coincidental; it stems from property rights systems represented by Dubai that have relatively high adaptability for securitization globally.

From the perspective of asset availability, the property rights system is the core prerequisite determining whether assets can enter the financial system and be structured into financial products, and the reason real estate has become the earliest matured asset class for RWA is fundamentally because its property rights system first satisfied the basic conditions for securitization. Foreign investors are allowed to hold permanent property rights in designated areas, and property rights are uniformly registered and confirmed by the Dubai Land Department. This institutional arrangement gives real estate assets legal attributes similar to traditional financial assets: ownership can be registered, rights can be divided, assets can be transferred, and interests can be inherited, while also being used as collateral within the financial system. For RWA, this means that SPVs (Special Purpose Vehicles) can legally hold the underlying assets and split and map their income rights through contracts, thus forming a standardized Token structure.

Looking further, the true value of the Freehold system lies not in the ability to buy houses but in that it meets the four core conditions of RWA’s underlying structure: first, ownership is unique and verifiable; second, transfer paths are clear; third, they can be enforced by the judicial system; and fourth, they can be embedded in financial structures. In contrast, in markets where property rights are unclear or where leasing rights replace ownership (such as long-term Leasehold structures), uncertainty surrounding asset duration, yield attribution, and re-transfer leads directly to tokens being difficult to price, which in turn affects investor trust structures.

Besides the property rights system, another key advantage in the Middle East lies in the layered design of the legal system, with financial free zones like Abu Dhabi Global Market (ADGM) and Dubai International Financial Centre (DIFC) adopting a dual-track structure integrating common law systems with the local civil law framework of the UAE. This institutional design is crucial in RWA practice: firstly, SPVs can be set up under common law frameworks, offering legal structures familiar to international investors; secondly, investment agreements can incorporate British and American legal terms (such as trust structures, beneficial arrangements, etc.), reducing cross-border comprehension costs; thirdly, the dispute resolution mechanism is more mature, with arbitration and execution efficiency substantially exceeding traditional local judicial systems.

This combination of property rights system + legal framework endows Middle Eastern real estate with a natural securitization advantage: clarity of ownership in off-chain assets, standardized expression of on-chain rights structures, and a judicial system that guarantees execution form a systemic moat for RWA.

To further compare the differences in RWA adaptability among major financial free zones in the Middle East, the following is organized:

From a practical perspective, the majority of current Middle Eastern real estate RWA projects typically adopt a three-tier structure of DLD registering property rights + establishing SPVs in DIFC/ADGM + issuing Tokens on-chain; this essentially modularizes the confirmation of asset rights, legal structure, and funding structure, placing each within the most optimal institutional context. This structural design not only enhances compliance certainty but also significantly lowers the understanding and participation threshold for cross-border investors.

Therefore, a more explanatory conclusion can be drawn: the reason real estate has become the dominant asset in Middle Eastern RWA is not only due to its stable returns or large scale, but because within the existing institutional framework, it was the first to meet the simultaneous criteria of property rights clarity, legal enforceability, and financial structure adaptability. This determination influences its path dependence in the early stages of RWA.

Overall, land systems and clarity of property rights essentially constitute the underlying trust anchors of RWA. The Middle East, through the synergy of the Freehold system and common law financial free zones, has created an institutional environment that combines efficiency in property rights confirmation with execution capability, making real estate the asset type that can most easily complete the mapping from off-chain to on-chain. Under this institutional constraint, the concentration of asset classes is not a market choice but a result of institutional screening.

Compared to real estate, although bonds and accounts receivable possess relatively high liquidity within traditional financial systems, their asset availability within the RWA structure is restricted. Bonds depend on the issuing entity's credit system; while their ownership is clear, it relies heavily on centralized credit endorsements; accounts receivable harbor risks regarding enforceability and authenticity verification, particularly in cross-border scenarios, where their legal execution chains are lengthy and uncertain.

2.3 Political Function of Real Estate as a Quasi-Sovereign Asset

In the structure of Middle Eastern RWA, real estate is not merely understood as a revenue-generating asset; it plays a more complex role as a quasi-sovereign asset within institutional design and national governance frameworks, serving both as a capital absorption tool and a significant vehicle for extending national credit. The term quasi-sovereign asset here does not indicate that its legal nature is equivalent to sovereign debt or public assets; rather, it refers to assets whose returns, pricing, and liquidity expectations are significantly influenced by national strategies, policy support, and urban cred.<|vq_8849|>

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。