Author: José Maria Macedo, Delphi Labs Cofounder

Translation: Shenchao TechFlow

Introduction: The founder of Delphi Labs spent two weeks intensively exploring the Chinese AI ecosystem, meeting numerous founders, investors, and CEOs of listed companies.

His conclusion was unexpected: he was more optimistic about hardware than anticipated, more pessimistic about software than expected, and his observations of Chinese founders overturned his previous understanding.

The article also covers hot topics such as valuation bubbles, the humanoid robot track, and information asymmetry between the East and West.

The full text is as follows:

I spent two weeks in China, meeting a large number of founders, VCs, and CEOs in the AI ecosystem. Before going, I was optimistic about this ecosystem, anticipating I would see world-class AI talent doing things at valuations far below those in the West.

By the time I left, my views had changed - they became more specific: hardware is stronger than I expected, software is weaker than I expected, and some observations about Chinese founders also surprised me.

The Issue with Founders

A common characteristic of the excellent founders I have invested in is: independent thinking, rebelliousness, extreme focus, and obsession. They are not obedient. They constantly ask "why," refusing to accept secondhand wisdom. The decisions they make often seem inexplicable to outsiders but make perfect sense to them. They possess an inherent, uncontainable intensity, often manifested as a long-term obsession and excellence. As a VC, I meet many smart people every day; this type is easily recognizable in a crowd because their life trajectories have a distinct "sharpness."

Many founders I met in China belong to another type, which took me by surprise.

They are extremely accomplished - top universities, experiences at ByteDance or DJI, papers in Nature, multiple patents. In the West, these achievements are only found among the top technical talents; in China, they are the entry ticket. They also work harder than almost anyone I have encountered. We held meetings at various times, even on weekends, and traveled between cities nonstop. One founder met us on the day his wife was giving birth.

However, independent thinking, rebellious spirit, and a vision from 0 to 1 are much harder to find. The backgrounds of the founders are very similar, and their pitches tend to be more conservative. Many ideas are upgraded versions of existing products (impressive V2), rather than truly original bets. Given the vast scale of technical talent produced in China, I expected to encounter more people presenting "ideas I have never heard of."

My interpretation is that China's education system nurtures excellence but does not allow enough space for deviation. It produces top executors skilled at solving known problems, rather than those who come with "a problem no one knows exists."

VCs Reinforcing This Model

Interestingly, local investors are exacerbating this trend.

The investment logic of most Chinese funds is based on one premise: investing in the best talent emerging from ByteDance or DJI. They focus on resumes, not brilliance; on background, not beliefs. The portrait of VCs themselves is similar - coming from large companies or consulting and investment banks, resembling European VCs from a decade ago.

Ironically, historically, the Chinese founders who truly built great companies mostly never worked in big companies at all. Jack Ma was an English teacher who took the college entrance exam twice before passing. Ren Zhengfei founded Huawei at 43 after serving in the military. Liu Qiangdong started selling goods in a traditional market. Dr. Wang Xing started his entrepreneurship before finishing his studies. The recent Liang Wenfeng, who created DeepSeek, has never worked anywhere outside of his own company. These individuals are outliers, belonging to that group without "standard resumes" - precisely the types the current investment system tends to overlook.

Finding such people has genuine alpha, but currently, it seems very few are looking there.

Shenzhen and the Hardware Ecosystem

The most shocking thing I saw in China wasn't a startup's pitch.

It was Shenzhen's hardware underground workshops - engineers systematically obtaining high-end Western products, disassembling them piece by piece, and reverse-engineering everything in an extremely rigorous way. When I left, I was genuinely uncertain whether most Western hardware founders understood what they were competing against. The network effects here are not theoretical; they are physical and dense, built up over decades.

The entrepreneurs we met demonstrated this with data: over 70% of hardware investments come from the Greater Bay Area, nearly 100% from China - this means the iteration cycles are unmatched by Western hardware companies.

Most of the founders I met are using DJI's approach: developing consumer hardware in a specific niche - electric wheelchairs, mowing robots, new generation fitness equipment - achieving revenues in the 8 to 9-digit range (USD), then leveraging customer bases or underlying technologies to expand into adjacent categories. Some companies are already much larger than you might imagine. The strongest company I saw this time was Bambu Lab, a 3D printing company that most Westerners have not heard of, reportedly making $500 million in annual profit and doubling every year.

Bearing Skepticism Towards Chinese Software

When I left, my skepticism about Chinese software opportunities was deeper than when I arrived.

At the model level, China's open source is indeed strong, but the closed-source models still have a significant gap compared to the best in the West, and this gap may be widening. The difference in capital expenditure is enormous. GPU acquisition remains restricted. Western labs are increasingly cracking down on distillation. Revenue numbers say everything: Anthropic reportedly achieved $6 billion ARR in just February. China's best model companies have ARR in the tens of millions of dollars.

In the software entrepreneurship space, the mainstream profile is PMs and researchers coming from ByteDance, creating agentic or ambient consumer software aimed at the Western market. The talent is indeed strong, but many of these products fall squarely within the functional range that large labs would organically release - a single version release could render them redundant. What surprised me further is that China lacks large, rapidly growing private software companies. In the West, aside from model companies, there is a batch of startups achieving 9-digit or even 10-digit ARR, with astonishing growth - Cursor, Loveable, ElevenLabs, Harvey, Glean. Breakthrough private software companies of this level basically do not exist in China - with a few exceptions like HeyGen, Manus, GenSpark, which also left after establishing themselves.

Valuation Bubble

Despite the disappointing software landscape, the bubble is very real - both early and late stage.

At an early stage, the top talent coming out of ByteDance, DeepSeek, and Dark Side of the Moon is indeed much cheaper than equivalent talent in the US; however, median valuations have converged. It's common for consumer startups without products to be valued at $100 to $200 million. Seed rounds exceeding $30 million are not uncommon.

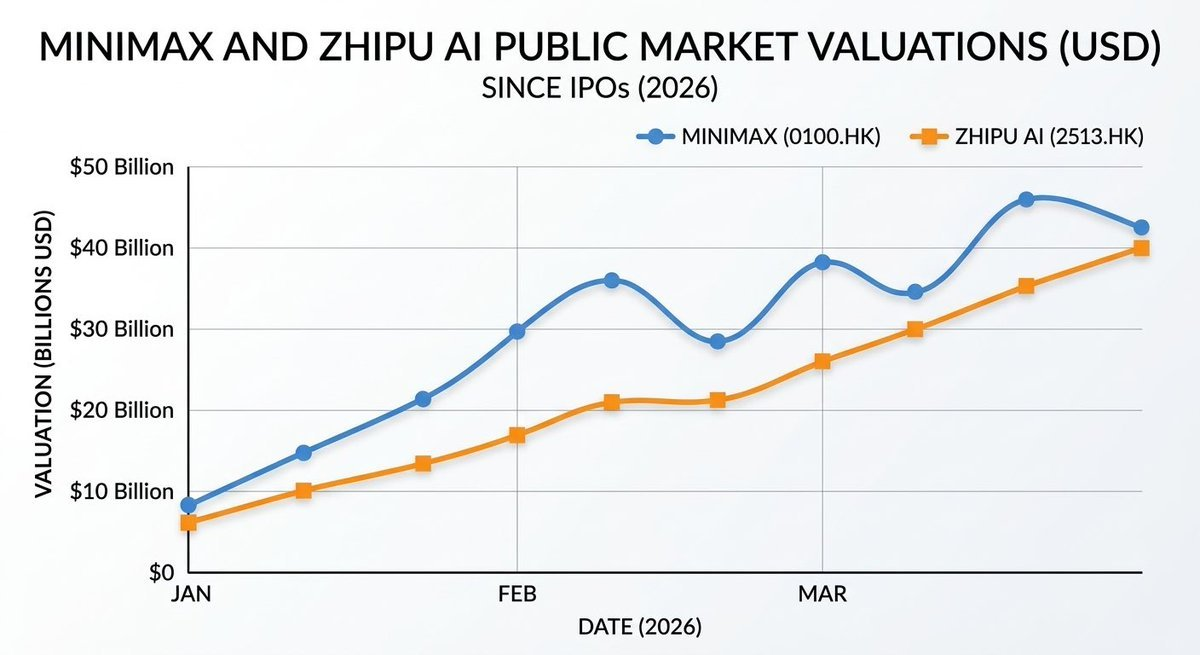

The numbers in late stage are harder to justify. MiniMax has a valuation of about $40 billion in the public market, with an ARR of less than $100 million - about 400 times revenue. Zhitu is valued at about $25 billion against $50 million in revenue. For comparison: OpenAI's highest valuation round was about 66 times ARR, while Anthropic was about 61 times.

Private model companies like Dark Side of the Moon are using these public market comparisons for financing - within months, valuations went from $6 billion to $10 billion to $18 billion. Friends in crypto are familiar with this pattern: investors compare private valuations with a "pre-unlock" public market price. Additionally, the fact that Zhitu and MiniMax can maintain this level is partly because they are currently the only means to gain exposure to the "Chinese AI narrative," which itself carries a premium. However, as more companies go public, this premium will be diluted. Finally, the IPO window has a characteristic - it can close suddenly, without warning. No one can guarantee you can exit this arbitrage before benchmark prices move.

The humanoid robot track is in a similar situation. China has around 200 humanoid robot companies, about 20 of which have raised over $100 million, with several valued at billions - almost all have no revenue, most plan to IPO on the Hong Kong Stock Exchange in 2026 or 2027. If this market is real, China's hardware advantage makes the long-term landscape relatively clear. However, commercialization may be much slower than the current financing pace suggests, and I doubt whether the Hong Kong market can sustain so many humanoid robot companies valued in the tens of billions, all currently waiting to IPO. For now, I won’t touch it.

Notable Information Asymmetry

One thing surprised me: nearly every founder I met is first targeting the global market and then the Chinese market. They use Claude Code, follow Dwarkesh's podcast, and have a deep understanding of the startup ecosystem in San Francisco - often clearer than those Western investors who haven’t been consistently paying attention.

The hostility from the West towards China is noticeably greater than China's hostility towards the West. Chinese founders feel that combining China's engineering execution capabilities and deep hardware expertise with Western go-to-market and product thinking is completely non-contradictory. When this combination takes shape within an appropriate founding team, some truly remarkable companies will emerge.

Finding these founders - those who do not fit the "standard resume template" optimized by local VC systems - is what we are working on now.

Special thanks to @woutergort for opening up his excellent network in China, @PonderingDurian for organizing this trip, and Claude for patiently editing my musings on the plane.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。