Author: Jae, PANews

The end of a cycle often begins with the most subtle indicators.

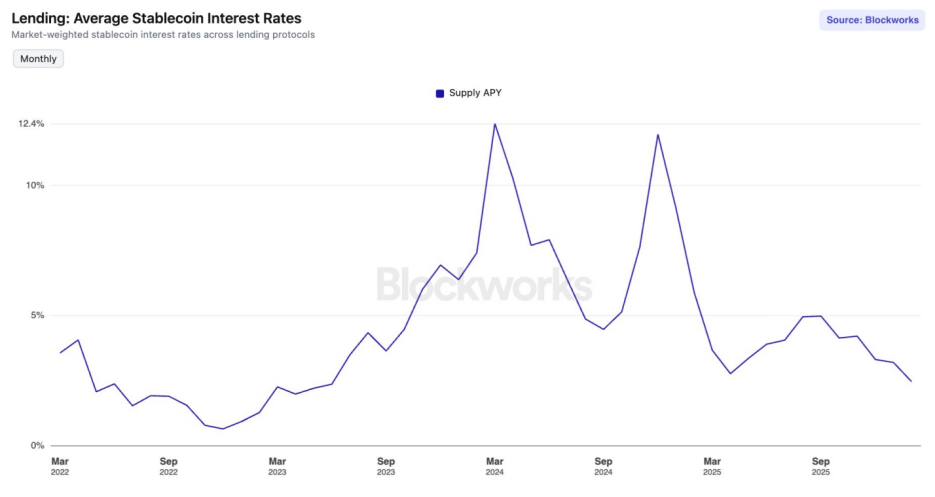

Since September 2025, the DeFi (decentralized finance) market has entered a "interest rate winter." The average annualized yield (APY) for mainstream stablecoins in leading lending protocols has touched the lowest level since June 2023.

On Aave V3 on the Ethereum mainnet, USDC and USDT deposit rates have fallen below 2%. Meanwhile, the yield on the US ten-year Treasury bond has rebounded to 4.24%. For DeFi players who have experienced DeFi Summer and are accustomed to high APYs, this is not just a decline in numbers, but rather a tolling bell for the end of a cycle.

Is this merely a cyclical fluctuation, or is the market undergoing a structural reshaping?

Supply-demand mismatch and liquidity overload trigger interest rate collapse

Over the past six months, the interest rate curves of mainstream lending protocols have shown a downward trend, as their interest rate models experience a yield collapse caused by "oversupply."

Interest rates are the price of capital. The physical basis determining the price is the amount of capital supplied.

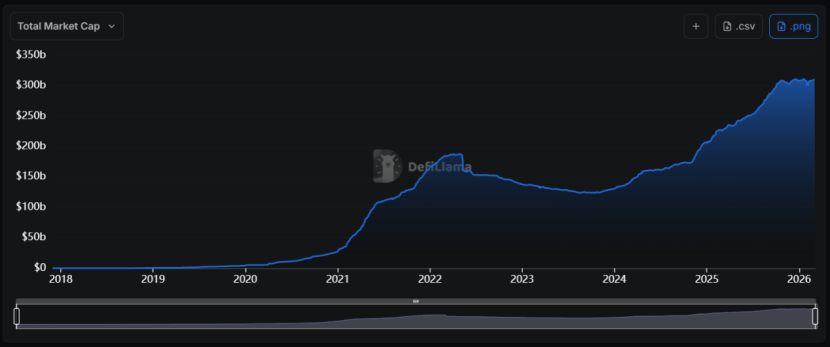

Since 2024, the stablecoin sector has undergone an unprecedented "expansion wave," with its total market capitalization skyrocketing from less than $130 billion to over $310 billion, reflecting a compound annual growth rate of about 55%.

The problem lies in the fact that the surge in supply was not accompanied by a proportional expansion in on-chain demand.

The problem lies in the fact that the surge in supply was not accompanied by a proportional expansion in on-chain demand.

When the supply of a certain commodity (stablecoin liquidity) increases significantly while demand weakens, its price (interest rate) is bound to fall. This is a fundamental principle of economics, and DeFi is no exception.

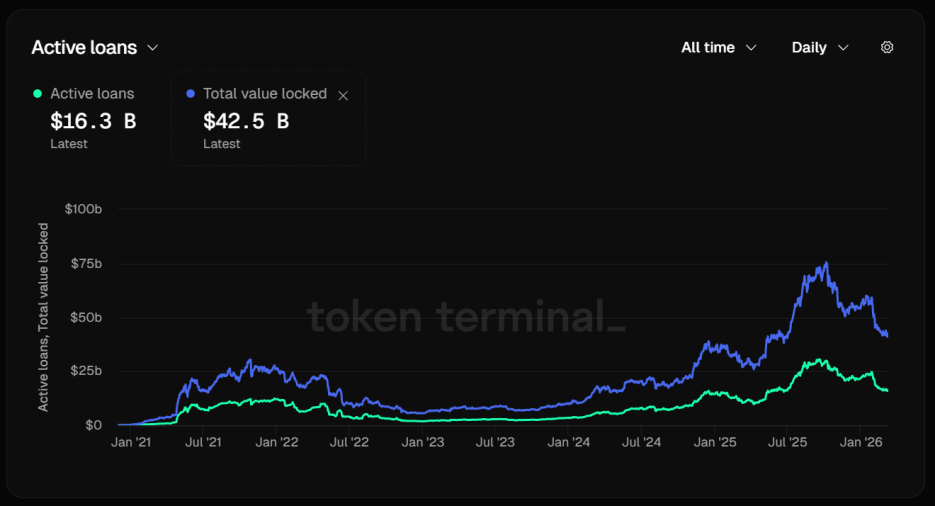

Taking the leading lending protocol Aave as an example, its stablecoin utilization rate is significantly declining. As of March 12, Aave's total locked value (TVL) reached an impressive $42.5 billion.

Upon examining the capital structure, a disturbing figure emerges: active loans are only $16.3 billion. Over 60% of the deposited assets are idle, and the mismatch between supply and demand has directly led to a rapid decline in interest rates.

This means that funds are being deposited without being lent, leading to severe liquidity congestion, forcing the protocol's algorithm to automatically lower the interest rate curve in an attempt to attract more borrowers.

However, these efforts have achieved little. The benchmark rates for USDC and USDT on Aave V3 on the Ethereum mainnet have already fallen below 2%, in stark contrast to the double-digit returns seen during the bull market.

However, these efforts have achieved little. The benchmark rates for USDC and USDT on Aave V3 on the Ethereum mainnet have already fallen below 2%, in stark contrast to the double-digit returns seen during the bull market.

The stablecoin market has fallen into a "liquidity trap." When the market is flooded with low-cost funds but lacks high-return investment opportunities, these funds accumulate in the lending protocol's pools.

Funding rate collapse and cooling of circular lending lead to leverage deceleration

The prosperity of DeFi stablecoin interest rates is essentially driven by "leverage." When arbitrage activities in the perpetual contract market cool down, the borrowing demand for stablecoins rapidly shrinks, leading to a sharp drop in interest rates.

During the bull market, bullish sentiment caused funding rates to be positive and high, and arbitrageurs would use the "borrow stablecoins to buy spot + sell perpetual contracts" delta-neutral strategy to hedge risk-free and earn funding fees. In this process, stablecoins act as fuel.

However, the derivatives market has recently shown lackluster performance. On mainstream centralized exchanges (CEX), the funding rates for BTC and ETH have often exhibited negative values or very low positive values. This reflects that bearish forces dominate the market, or bulls are overly cautious.

Regardless of the explanation, they all point to the same conclusion: a lack of motivation among arbitrageurs.

When annualized funding rates plummet, considering borrowing costs and transaction fees, the net profits for arbitrageurs will take a significant hit. Their borrowing demand for stablecoins consequently sees a cliff-like drop.

Another major source of borrowing demand for stablecoins is circular lending. The typical path of this yield-enhancing strategy is: depositing income-generating assets like sUSDe in Aave, borrowing stablecoins like USDC, and then converting the borrowed USDC into more sUSDe and depositing it.

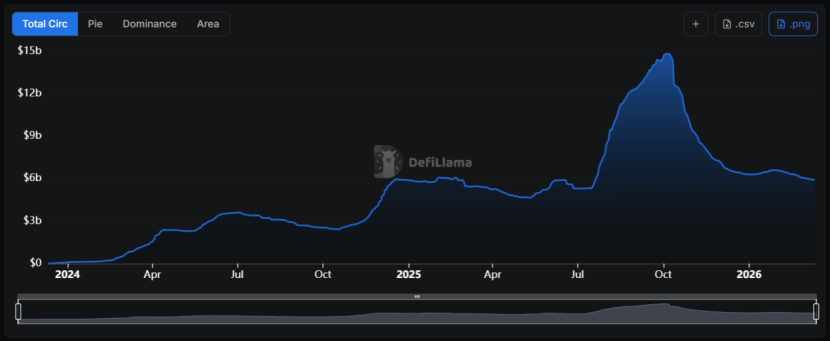

This strategy once thrived because USDe yields were as high as 30%, while borrowing costs were only around 10%, creating a 20-percentage-point arbitrage space.

However, after the "1011" incident, the yield spreads catastrophically narrowed, and USDe faced a ceiling in "scalability," with its size plummeting from nearly $15 billion to the current $6 billion.

The yield of USDe is highly dependent on the size of bearish positions in the market. Since the total Open Interest in the perpetual contract market is limited, when USDe expands to a certain extent, the short positions required to hedge will itself lower the market's funding rates, thereby suppressing the yield of sUSDe.

The yield of USDe is highly dependent on the size of bearish positions in the market. Since the total Open Interest in the perpetual contract market is limited, when USDe expands to a certain extent, the short positions required to hedge will itself lower the market's funding rates, thereby suppressing the yield of sUSDe.

For ordinary traders, a decrease in sUSDe yields will reduce their strategy's yield spread. Their reduced demand for leveraged positions will further lessen their need for stablecoin collateral.

This creates a self-reinforcing negative cycle: diminished demand → falling interest rates → further diminished demand.

Shift in risk preference in the crypto market, funding seeks more certainty

The overall decline in risk preference in the crypto market is another important factor leading to lower stablecoin interest rates.

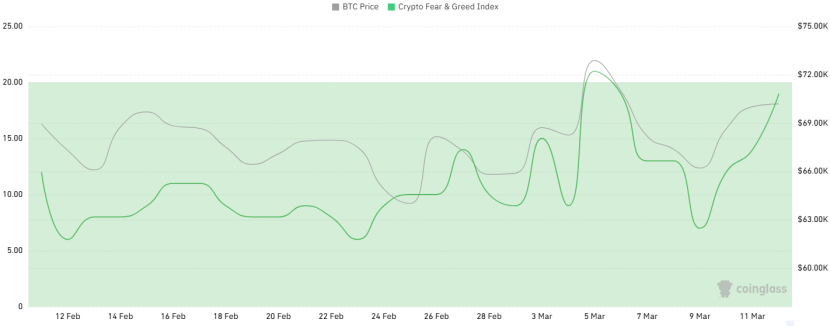

In the past month, the Crypto Fear & Greed Index has frequently dipped into the "extreme fear" zone, even when the BTC price maintained around $70,000, market sentiment did not show sustained improvement.

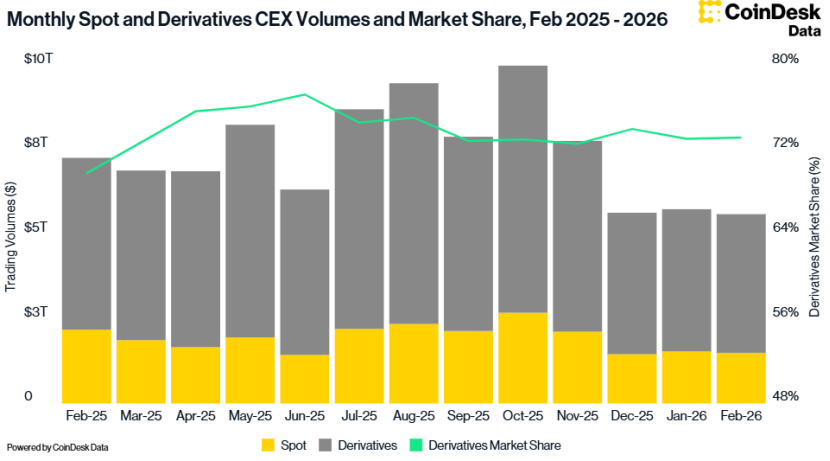

CoinDesk Data also shows that in February, the total trading volume on CEX shrank by 2.41%, falling to $5.61 trillion, the lowest trading volume since October 2024.

The decline in risk preference has prompted investors to turn to segments with higher certainty.

The decline in risk preference has prompted investors to turn to segments with higher certainty.

Since January 2024, the effective federal funds rate of the Federal Reserve has remained above 3.6%. Although the market anticipates a mild rate cut path in the future, the current actual rates remain relatively high.

This macro environment has also exerted a profound suppressive impact on DeFi stablecoin interest rates. When the risk-free yields of US Treasuries exceed DeFi deposit rates, rational investors will choose to withdraw funds from on-chain protocols or invest them in RWA (real-world asset)-backed protocols without risk premium compensation.

This macro environment has also exerted a profound suppressive impact on DeFi stablecoin interest rates. When the risk-free yields of US Treasuries exceed DeFi deposit rates, rational investors will choose to withdraw funds from on-chain protocols or invest them in RWA (real-world asset)-backed protocols without risk premium compensation.

In the interest rate winter, not all protocols are shrinking. Sky (formerly MakerDAO) has built a unique "yield moat."

Compared to Aave's reliance on on-chain lending demand, Sky's yields also stem from its $1.5 billion mature RWA assets. These assets include US Treasuries, AAA-rated corporate debts, etc., which are not affected by fluctuations in the crypto market and provide a stable underlying cash flow.

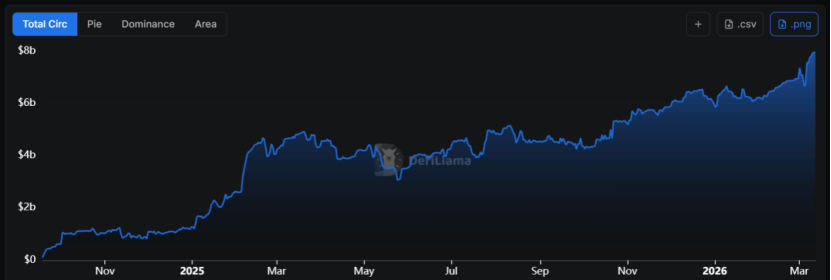

This model of converting RWA into underlying collateral has driven the supply of USDS to grow by 68% year-on-year, with a market capitalization nearing $8 billion.

As of now, the interest rate for sUSDS still hovers around 3.75%, becoming the "de facto floor" for on-chain yields. In the vaults related to USDC and USDT, deposit rates can exceed 5%.

As of now, the interest rate for sUSDS still hovers around 3.75%, becoming the "de facto floor" for on-chain yields. In the vaults related to USDC and USDT, deposit rates can exceed 5%.

This positions Sky in a role similar to that of a "benchmark rate platform." In contrast, the rates for similar assets on Aave are almost non-competitive.

Thus, Sky is transforming from a mere stablecoin protocol into a "fixed income asset management" protocol, utilizing its massive RWA portfolio to hedge against downside risks in the crypto market. When there is a lack of demand within DeFi, it can obtain yields from the outside (traditional financial market).

For investors, learning to examine the underlying logic of yields—whether they come from bond dividends or volatility premiums in the futures market—will become a necessary lesson for this cycle. Strategies also need to shift from "chasing APY" to "seeking differentiated risk exposure."

The "interest rate winter" is not only a result of cyclical fluctuations but also an inevitable growing pain of DeFi "bubble deflation."

Perhaps just as the trough in 2023 birthed the prosperity of 2024, this bottoming out of interest rates may also be DeFi accumulating energy for the next leap.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。