This article is from:@peruvian_bull

Translated|Odaily Planet Daily(@OdailyChina);Translator| Ethan(@ethanzhang_web3)

Editor's Note: In the past four months, Bitcoin has formed a near-fixed rhythm - every time the US stock market opens, it is met with a noticeable wave of selling pressure. It rises during the Asian session, continues to rise during Europe, but quickly falls when New York opens. Traders call it the "10 o'clock strike." This force is like an invisible structural headwind, repeatedly liquidating leveraged positions, depressing market sentiment, and gradually consuming investors' patience.

However, when the lawsuit documents against Jane Street were officially made public, this rhythm that had lasted for months was suddenly interrupted. Was this merely a coincidence, or a signal of a deeper structural change? How did the whole process unfold? Below is the complete translation by Odaily Planet Daily.

——————Divider——————

The most powerful trading firm you've never heard of has just been caught in the act. Twice, in two different continents. And Bitcoin seems to have finally exhaled as a result.

Jane Street Group is a quantitative trading firm headquartered in New York. They do not have a CEO.

According to their own words, they operate like an "anarchist commune." In the first nine months of 2025, they achieved a net trading income of 24 billion dollars, surpassing the 20.5 billion dollars of the entire year of 2024. In the second quarter of 2025 alone, it reached 10.1 billion dollars, the highest quarterly trading income in Wall Street history.

By any standard, they are the most profitable trading institution in the world.

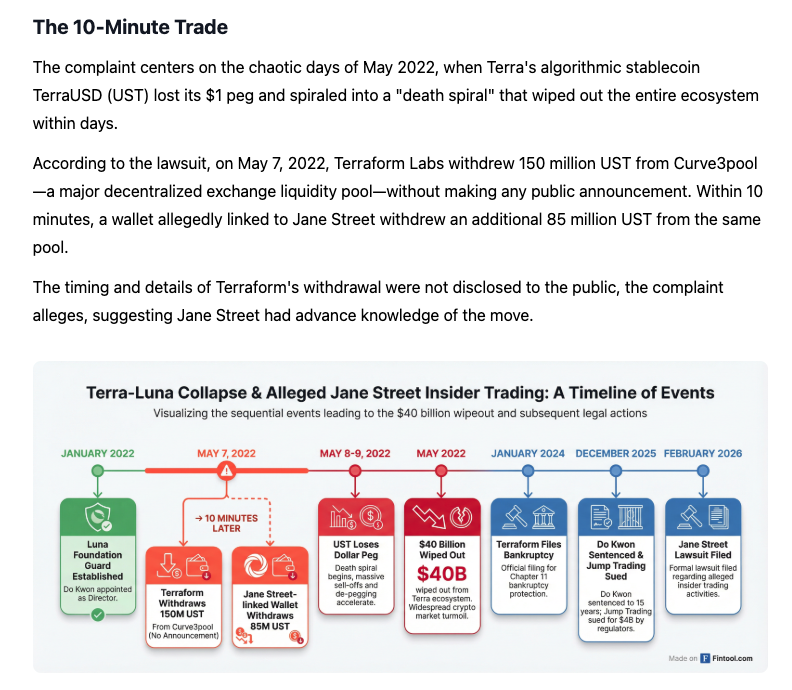

And just this week, the bankruptcy administrator of Terraform Labs filed a lawsuit in Manhattan Federal Court, accusing Jane Street of using insider information to front-run the collapse of Terra Luna in May 2022. This collapse evaporated 40 billion dollars in market value and triggered a chain reaction that ultimately led to the downfall of Celsius, Three Arrows Capital, and FTX.

The accusation is shockingly simple. On May 7, 2022, Terraform Labs quietly withdrew 150 million dollars in UST from the major decentralized liquidity pool Curve3pool. There was no public announcement, just a silent withdrawal of liquidity.

Ten minutes later, a wallet linked to Jane Street withdrew 85 million dollars from the same pool. Just ten minutes...

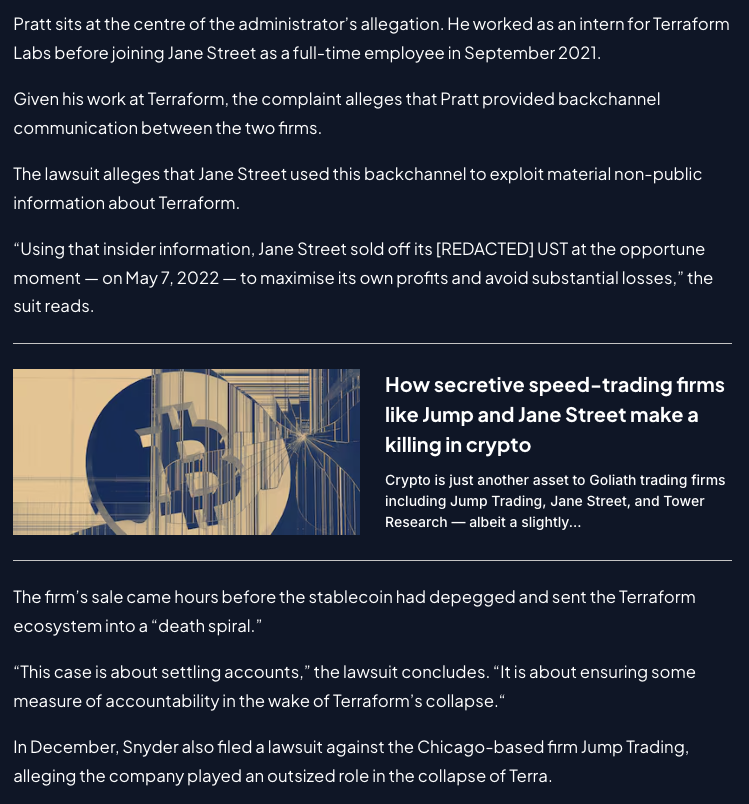

The lawsuit claims that a former Terraform intern, Bryce Pratt, who became a full-time employee at Jane Street in September 2021, established private communication channels with former colleagues and allegedly transmitted significant non-public information regarding Terraform’s liquidity changes directly to Jane Street's trading team.

The lawsuit lists four defendants: Jane Street Group LLC, co-founder Robert Granieri, and employees Bryce Pratt and Michael Huang.

The administrator's statement strikes directly at the heart: The trades conducted by Jane Street could not have been completed without the exclusive insider information they possessed.

What’s worse, the lawsuit claims that Jane Street's withdrawal helped trigger the de-pegging of UST, plunging the entire Terraform ecosystem into a death spiral. LUNA plummeted from over 80 dollars to nearly zero. 40 billion dollars evaporated. Ordinary investors lost everything. Pensions, education funds, lifelong savings vanished in days.

Jane Street's response? They described the accusations as “desperate and baseless.”

But the problem is, this is not the first time.

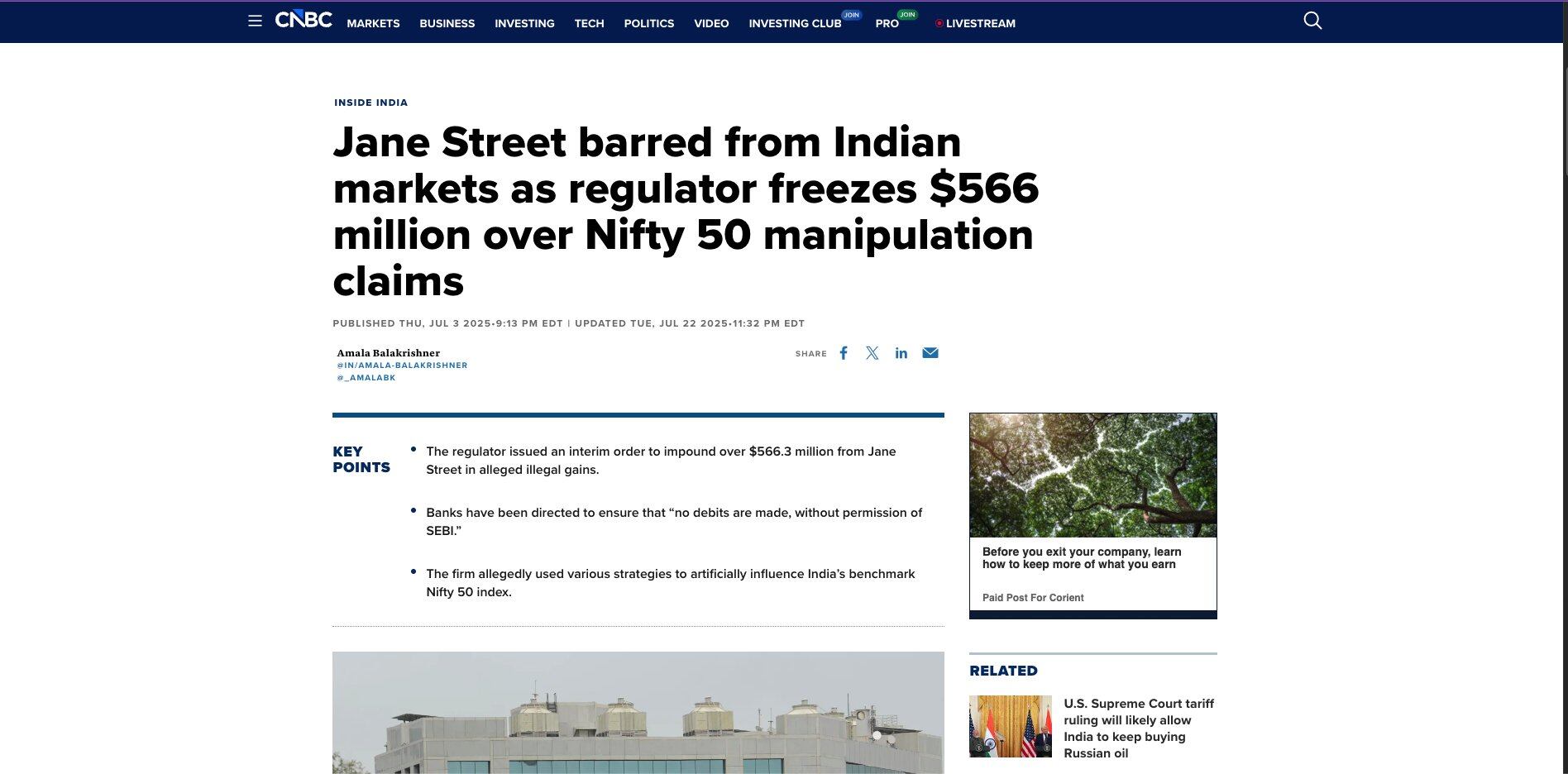

In July 2025, the Indian Securities and Exchange Board (SEBI) alleged one of the largest market manipulation cases in the country's history against Jane Street. The investigation found that between January 2023 and March 2025, on 18 derivative expiration dates, Jane Street conducted textbook-style pump-and-dump operations on the Bank Nifty index.

The methodology is extremely mechanical:

Morning: Jane Street's algorithms massively buy constituent stocks and futures, pushing the index up by 1% to 1.3%. On certain trading days, SEBI determined that all positive index gains were entirely from Jane Street.

At the same time, they established large short option positions, mainly selling call options and buying put options, with a ratio far exceeding stock positions. SEBI determined that, based on delta equivalent calculation, the option position size was 7.3 times the spot and futures positions. This is neither hedging nor arbitrage, but packaged directional manipulation.

Afternoon: They reverse their operations, selling the stocks bought in the morning. The index falls, and the short options profit. This cycle repeats on each expiration date.

SEBI assessed illegal profits of 484.3 billion rupees, approximately 580 million dollars, and described their actions as “deliberately designed to manipulate settlement prices.” The regulatory agency also noted that even after a clear warning from the National Stock Exchange in February 2025, Jane Street continued to execute this strategy.

SEBI’s language is unusually severe: “Market integrity and the trust of millions of retail investors and traders cannot be hijacked by such untrustworthy actors.”

Jane Street has been banned from entering the Indian securities market, has deposited over 560 million dollars into escrow accounts, and filed an appeal. As of now, the case is still under adjudication in the Indian Securities Appellate Tribunal.

Now, back to Bitcoin.

Since November 2025, Bitcoin traders have noticed an abnormal phenomenon. Around 10 a.m. Eastern Time every day, coinciding with the opening of the US stock market, a large number of sell orders flood into BTC and related ETF shares. The pattern is remarkably consistent: rising during the Asian and European sessions, then facing selling pressure when New York opens. (Refer to the article: "Is Jane Street Manipulating Bitcoin? The Viral Theory Explained")

This data cannot be ignored. Charts from December 2025 show that on certain trading days BTC could drop from 89,700 dollars to 87,700 dollars in just a few minutes, first blowing up 171 million dollars in leveraged long positions, and then quickly rebounding. This trend appeared on December 1, December 5, December 8, December 10, December 12, and December 15, and repeated itself in January and February 2026.

The crypto community on Twitter nicknamed it: “10 o'clock strike.”

Soon, the finger pointed to Jane Street, and not without reason. Jane Street is one of the four authorized participants of BlackRock's IBIT. IBIT is the largest spot Bitcoin ETF in the world. The other three are Virtu Americas, JPMorgan Securities, and Marex. As an AP, Jane Street has the special authority to create and redeem ETF shares, which means they have direct access to that core pipeline that "puts Bitcoin into institutional wrappers and takes it out again."

Their 13F disclosures also confirm their massive size. According to their Q3 2025 filing, Jane Street held 5.7 billion dollars' worth of IBIT shares. In Q4 2025, they increased their holdings by 276 million dollars, bringing their total holding to over 20 million shares, valued at approximately 790 million dollars at year-end prices. Their peak exposure once approached 2.5 billion dollars' worth of IBIT.

But what is truly suspicious is: reportedly, while they were smashing BTC on the spot in the mornings, they simultaneously increased their MSTR (Strategy, formerly MicroStrategy) holdings by 473% in Q4 2025, accumulating 951,187 shares valued at approximately 121 million dollars. Meanwhile, during the same period, large institutions like BlackRock and Vanguard were significantly reducing their MSTR holdings, at scales measured in the billions of dollars.

You can reflect on this logic once more: Opening sell BTC - driving down the price - blowing up leveraged long positions - buying back at low levels; at the same time, capitalizing on the expectation of a rise to reverse positions and add holdings in the market's "most leveraged" Bitcoin proxy assets.

Glassnode co-founders Jan Happel and Yann Allemann reignited this speculation through their X account Negentropic, linking the rhythm of algorithmic trading with the Terraform lawsuit documents. The Milk Road account further amplified the discussion, stating that the market has had "continuous whispers" pointing towards certain institutional trading desks executing "a very specific and somewhat shadowy script."

Then, the lawsuit landed. An extraordinary thing happened.

After Terraform submitted the lawsuit against Jane Street, the "10 o'clock strike"... did not occur. For the first time in months, Bitcoin did not drop at the opening of the US stock market; instead, it rose.

Today Bitcoin rose over 3%, breaking through multiple resistance levels, returning to above 68,000 dollars - just days ago, it had nearly dipped below 60,000 dollars. Over 323 million dollars in short positions were liquidated. The Stochastic RSI touched 100. ETF net inflows reached 257.7 million dollars, the highest since early February.

This pattern has been broken.

Of course, I have to be cautious. Correlation does not equal causation. There may be many variables involved: Trump's State of the Union address, technical overselling, and short covering. The Fear and Greed Index fell to 11, indicating "extreme fear," which often signals a reverse turning point. The RSI also dropped to 15.80, a reading not seen since the pandemic crash in 2020 - and after which there was a 1400% surge. Yet, at this point in time, it is still hard to consider it a coincidence.

A saying circulating on X is that after the lawsuit, Jane Street was “forced to shut down trading algorithms.” Jane Street told Cointelegraph that these are “baseless claims that take things out of context.” Regardless of whether they were forced to halt trading or voluntarily pressed the pause button out of legal risk, the outcome is the same: that persistent selling pressure has disappeared.

What does this really mean for Bitcoin?

Spot Bitcoin ETFs were originally seen as the "ultimate equalizer": institutional gateway, compliant product, BlackRock endorsement. And they have indeed been remarkably successful—IBIT has absorbed over 20 billion dollars since its inception.

But the ETF structure also brought back something that Bitcoin once sought to escape: trusted intermediaries with privileged access.

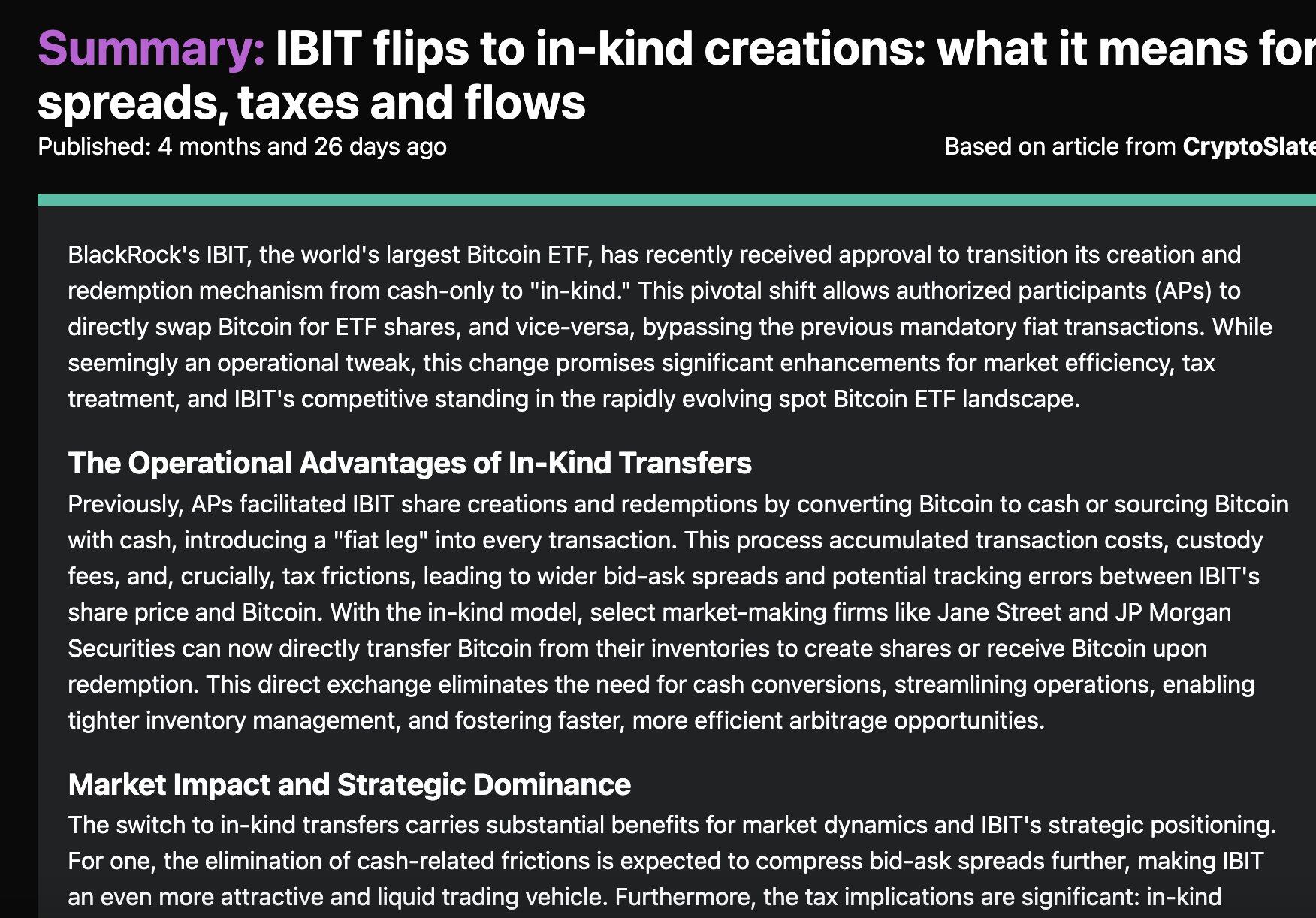

When the SEC approved spot Bitcoin ETFs in January 2024, it required a "cash-only" creation and redemption mechanism. Whenever shares need to be created or redeemed, someone must buy and sell real Bitcoin. And the institution accessing this process—the AP—naturally has a structural advantage over other market participants.

By September 2025, the SEC also approved IBIT to adopt "in-kind" creation and redemption, meaning APs can directly exchange Bitcoin for ETF shares without going through fiat currency. This gave Jane Street, Virtu, JPMorgan, and Marex more direct control over the flow of "Bitcoin moving in and out of the largest institutional shell."

The "10 o'clock strike" is essentially a new symptom of an old ailment—a disease that has plagued the gold market for decades.

I wrote in "The Gold Endgame Begins": In the paper-for-paper trading game, whoever is closer to the privileged interface can push prices before the rest of the market reacts.

JPMorgan traders Gregg Smith and Michael Nowak were found guilty of engaging in "spoofing" in the precious metals futures market. The scheme lasted 8 years and involved thousands of illegal trades. JPMorgan paid 920 million dollars in settlements for this. Deutsche Bank also paid 30 million dollars for similar issues. UBS, HSBC, and six individual traders have also been subjected to CFTC spoofing charges.

The same script. Just changed the asset.

And every time, these institutions wrap it up as “market making,” “providing liquidity,” or “hedging,” and the euphemisms could go on endlessly. The result is always the same: ordinary people get torn apart, insiders profit from price differences.

So, what’s next?

The larger structural picture has not changed. In the first eight weeks of 2026, ETFs saw a net outflow of 4.5 billion dollars, which looks frightening. But Strategy (Saylor’s company) just bought 39 million dollars' worth of BTC, accounting for 99% of all purchases by listed companies during that period. The real big players are not selling; they seem to be waiting for the algorithms to finish their job.

Perhaps—just perhaps—the algorithms have stepped back.

If Jane Street, due to legal risks, cross-continental regulatory scrutiny, or self-preservation, has been forced to withdraw from that "daily selling plan" (as stated in the accusations), then a structural headwind that has pressed down on Bitcoin for four months would have had a piece removed.

Bitcoin was born for moments like this: a currency system that does not rely on trusted intermediaries; a system that does not need authorized participants; a system that should not be jumped by “the former intern's private channel.”

But do not forget how we got here. Those institutions, referred to as “market makers” and “liquidity providers,” are exactly those accused of front-running the collapse, manipulating national-level indices, and executing daily algorithmic sell-offs against the underlying assets tracked by their ETFs.

This is the system Bitcoin was designed to replace.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。