IEEPA tariffs have been ruled illegal, which essentially means that the core tariff weaponization strategy of Trump's second term has been significantly weakened. Although Section 122 is currently being used as a transition, the 15% alternative tariff is already noticeably lower compared to IEEPA, especially with a more obvious decline in the actual tax burden in regions such as China, Japan, South Korea, and Taiwan. Additionally, Section 122 only has a 150-day validity, and it requires Congress approval upon expiration. Given the clear opposition from the Democrats, the probability of maintaining tariffs in mid to late July is not low.

This is favorable for the risk market. The market fears uncertainty the most, and Trump himself is the biggest source of policy uncertainty. After the Supreme Court rejected the IEEPA path, even if the White House continues to seek alternative tariff tools, the impact will likely be weaker than IEEPA. The market's pricing logic regarding tariffs will gradually shift from Trump's statements back to a framework of legal constraints and bipartisan negotiations.

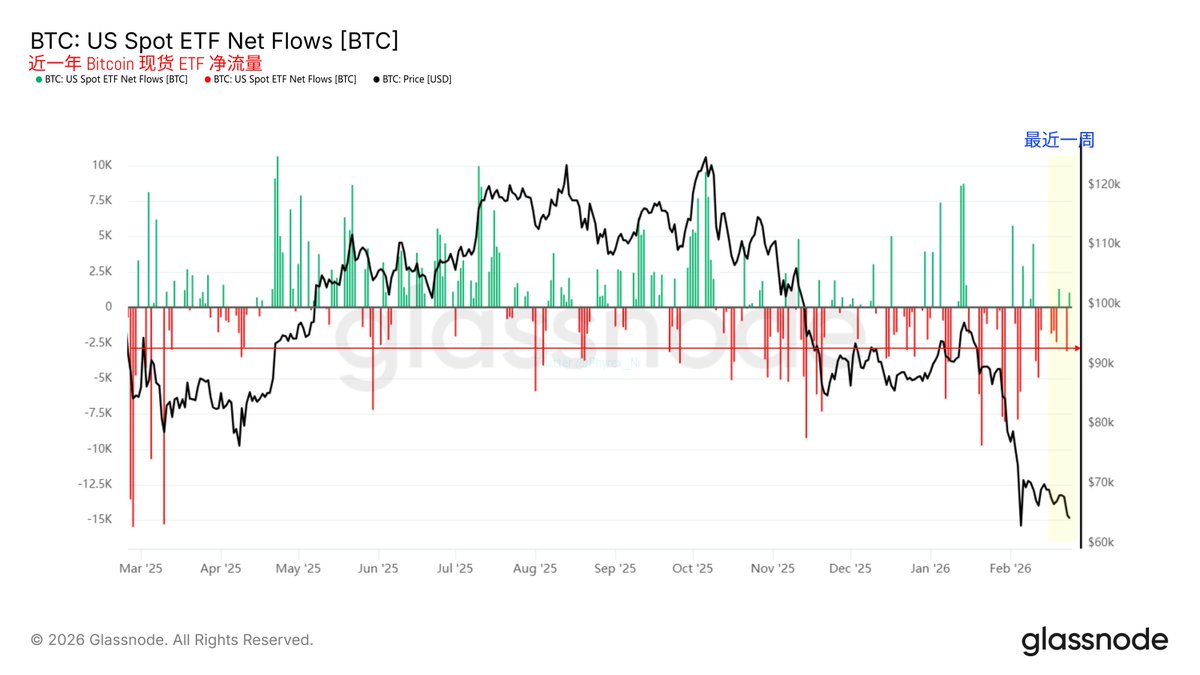

Regarding Bitcoin, short-term fluctuations remain, but there are signs of marginal easing in panic selling. Spot ETFs are still seeing outflows, but the scale of outflows has significantly decreased in the last month, indicating that the panic funds may be nearing the end of their exit. Meanwhile, BTC has approached the shutdown price range for miners, making buying coins relatively more cost-effective compared to mining.

It was originally expected that miners would continue to exit near the shutdown price and that difficulty would decrease, but this week the mining difficulty has instead rebounded significantly, indicating that miners still have a strong willingness to participate at current prices. Reasons may include a drop in miner prices and the latest models having lower pure electric shutdown prices, but regardless of the reasons, the difficulty rebound itself indicates that miners have not clearly surrendered.

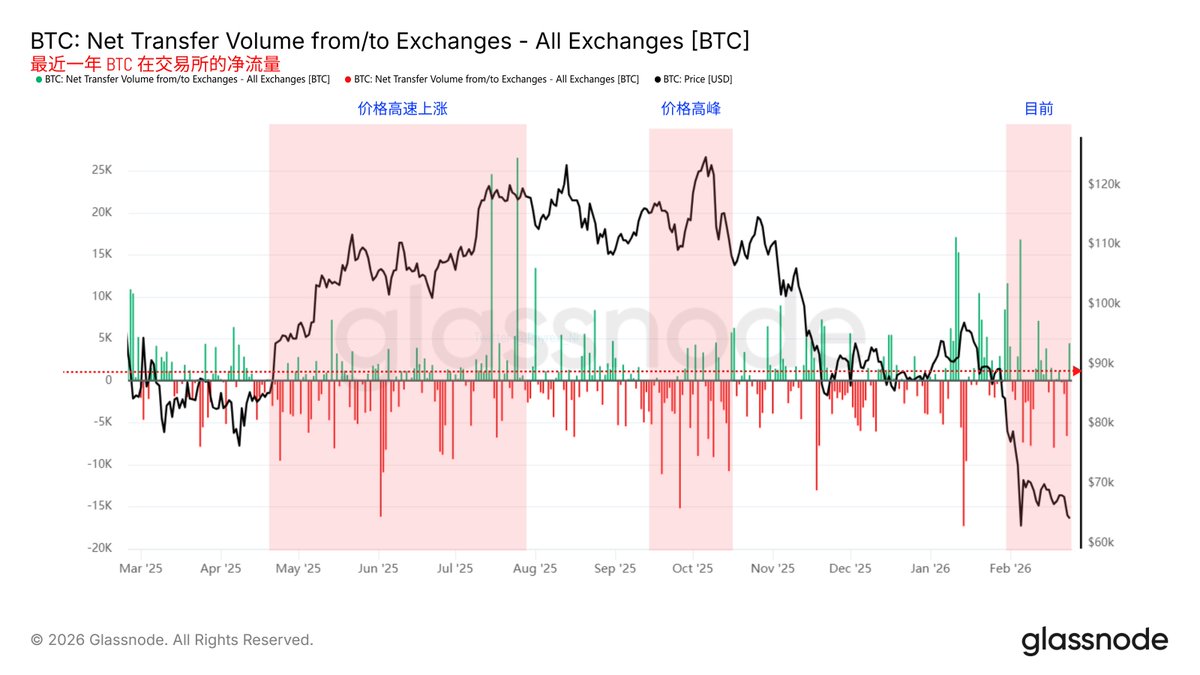

In terms of on-chain data, the long-term holder NUPL remains in the anxiety zone, suggesting that market sentiment is indeed cautious and investors are worried about further declines. However, combining the net positions of BTC on exchanges and the inflow data, the selling pressure is continually decreasing; whether traditional investors or native players, the willingness to sell at this position is diminishing.

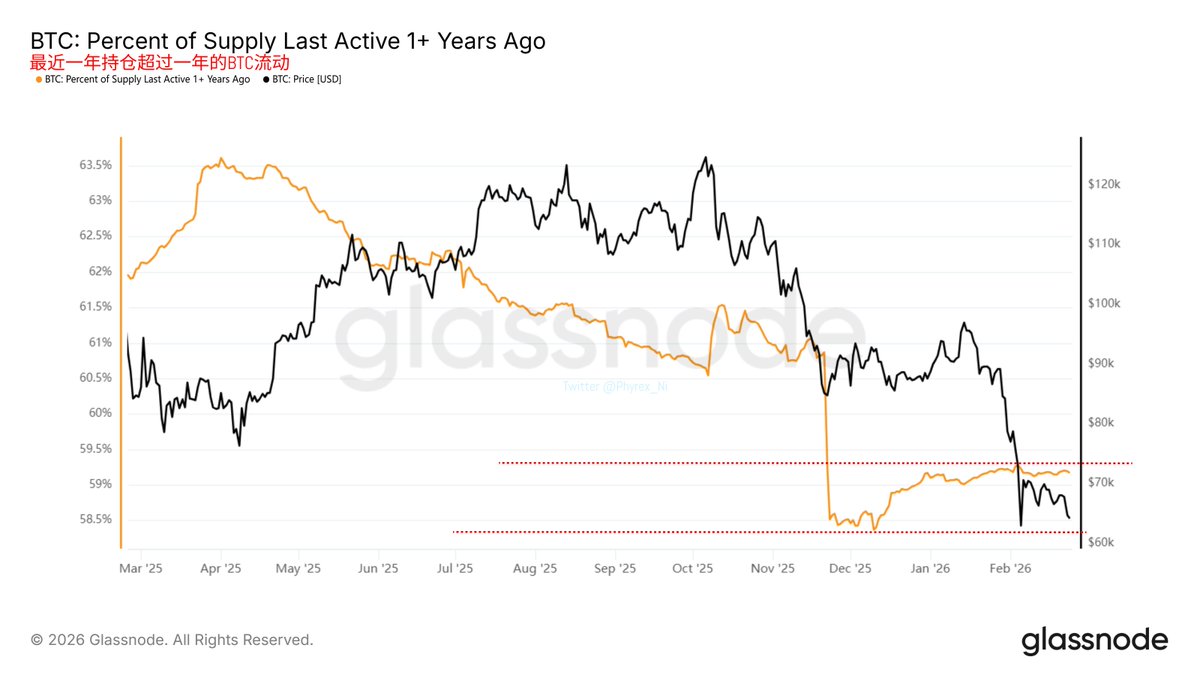

More critically, while BTC dropped from $90,000 to $65,000 within a month, the price distribution data indicates that multiple key support zones did not show significant collapse, and high-cost holders have not experienced large-scale panic selling. This is uncommon in historical bear markets, indicating that more and more chips are shifting towards long-term holders, and low prices do not necessarily force out their holdings.

Additionally, data on BTC flows for holdings exceeding one year shows that after hitting the bottom in December 2025, long-term holders’ positions have not decreased but instead increased, further showing that price declines have actually enhanced the holding willingness of some investors. The issue is that while selling pressure has decreased, purchasing power has not recovered in parallel. Net flow data from exchanges shows that as selling pressure weakens, buying pressure is also weakening, implying that funds have not notably flowed back into the crypto market, and most funds are not in a hurry to bottom fish. Thus, at this stage, BTC seems more likely to be "not falling" rather than "immediately rebounding strongly."

Overall, the biggest uncertainty factor in the market has clearly weakened. Subsequent fluctuations and inflation pressures arising from tariffs may decline, and the Federal Reserve's policy constraints will also be relatively eased. The market in the second half of the year remains promising, focusing on three variables: the Federal Reserve's path, the subsequent implementation pace of tariffs, and changes in expectations for the mid-term elections. If these three lines align properly, both risk assets and Bitcoin are expected to experience a more decent rebound.

In my personal opinion, the $BTC $60,000 range is a strong support area, and unless more "stimulating" negative news appears, it is unlikely to be easily broken. The key in this range is a substantial reduction in selling, but the lack of upward momentum is still due to insufficient liquidity and a lack of purchasing power, so the short-term is expected to remain primarily stable.

@bitget VIP, lower fees, better benefits

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。