Author: Hazel, Zhi Wu Bu Yan

This giant that once rewrote global payments and created a generation of entrepreneurial gangs is no longer glorious. Just as it hits rock bottom, the hunters have already sensed the smell of blood.

Around 2006, a group of small foreign trade bosses in Guangdong and Fujian began exploring how to open stores on eBay. They sat in small offices next to factories, doing business with strangers on the other side of the earth with broken English.

The hardest part was not the language, not the logistics, but the money—how to ensure that an American buyer could safely send money to a Chinese seller?

What made this possible was a blue button. That button was called PayPal.

At that time, PayPal represented the forefront of financial democratization and cutting-edge productivity. Following the "Website Payments Standard Integration Guide", small and medium-sized businesses around the world only needed to input a piece of HTML code and paste it on their webpage to collect payments globally.

This technological equality, combined with the foundation laid by eBay's only officially recommended payment method, made PayPal undoubtedly the global payment hegemon. To this day, if you open any overseas checkout page, you will surely find a place for PayPal.

Twenty years have passed. Many of those small foreign trade bosses have transformed from eBay shop owners into cross-border merchants flourishing across independent sites, Amazon stores, TikTok, and Temu. China's cross-border e-commerce export scale has surpassed 2 trillion RMB, and payment tools have evolved from a blue button to a blooming array of options including Stripe, Wise, LianLian, and WanLiHui.

The industry has grown, but PayPal has somewhat fallen behind.

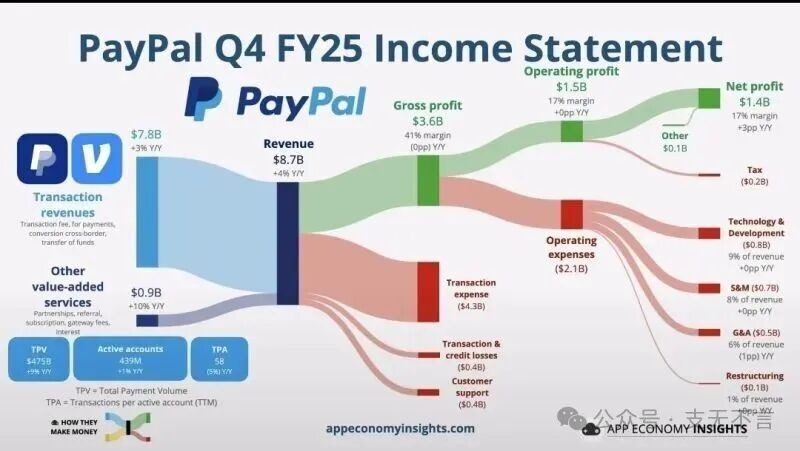

Three weeks ago, on February 3, PayPal announced its financial report, and its stock price plummeted by 20% in a single day, with the CEO leaving quietly. The main source of profit, branded checkout, has seen its active user growth rate drop from a previous high-speed track to just 1%, and the transaction volume of active accounts has decreased by 5% in the past 12 months.

Whether it's Stripe's one-click link payment, biometric verification Apple Pay, or simply using Google to fill in credit card information, all seem to be much more convenient than the slightly outdated blue icon interface, which one might struggle to remember the login password for.

It was once a legend created by figures like Musk, Peter Thiel, and Hoffman. Pelosi once held a significant stake, and Ark Invest's Cathie Wood was among its most loyal supporters, but they have both opted to cash out.

PayPal's market value has dropped from a peak of $363 billion during the pandemic to a recent low of $38 billion—90% evaporated over five years, with the P/E ratio touching a low of 7.4. It wasn't until Bloomberg reported today that at least one large competitor is evaluating an overall acquisition and that multiple parties have expressed interest in part of its assets that the stock price rose nearly 10% in response.

The news itself is the most precise note on PayPal's situation. When a company starts to be seen as prey rather than a hunter, and its market value rises as a result, it indicates that the market's confidence in its independent operation is now lower than the expectation that it will be acquired.

The once payment empire, like the aging British Empire, still has its flags planted around the world, the sun hasn’t set yet, but those who see it no longer harbor the awe of years past. Everyone knows in their hearts that the times have changed. But how did it fall so low?

"It is truly painful to see a company I love so much reach this point."

On February 3, former PayPal president David Marcus published a long post on X, unusually criticizing the company he once poured his efforts into.

David Marcus's career has always been intertwined with radical financial innovation. He is currently the CEO of LightSpark, a Bitcoin Lightning Network payment company. During his time at PayPal, he recruited top engineering talent and led the acquisition of Braintree and Venmo; during his time at Facebook, he was one of the leaders of the sensational stablecoin project Libra. Although Libra stumbled due to regulatory issues, today’s stablecoin craze is proof of David's foresight and boldness.

In addition to the plummeting stock price, another reason stimulating David to issue this long post was the departure of former CEO Alex Chriss after less than three years in office, with former HP CEO Enrique Lores taking over.

Enrique Lores served as CEO at HP for seven years, introducing the profitable model of printing-as-a-service and initiating large-scale layoffs; there is no doubt that he is an expert in cost reduction and efficiency improvement. If the PayPal board had long considered an overall or partial sale of PayPal, this choice of candidate would make even more sense.

David subtly expressed his discontent: "I do not know Enrique. He might be a great leader, but at least from the information on paper, he is an executive from the hardware industry now parachuted into a payment company."

This echoes David's core criticism. Unlike the market voting with its feet due to poor financial performance, David believes PayPal's lifeblood is that—"The leadership style of the company has completely shifted from 'product-driven' to 'financial-driven.' Over time, belief in the product has given way to financial optimization."

Paraphrasing a famous saying by Benjamin Franklin: Any company that sacrifices products for temporary stock price performance will ultimately fail to keep up with the trends of the product era and will also lose stock prices.

David believes PayPal has lost its "mojo." This was a spirit during PayPal's gang era, a wild force that dared to tear the office roof off to solve an impossible problem. But today, that force has been replaced by compliance checks and financial optimization.

Stripe, which conquers developers with its simple API, has this mojo. Opening Stripe, the constantly pulsating "Global GDP running on Stripe" in the upper left corner exudes a conqueror's aura.

In recent years, Apple's strong promotion of Passkey has this mojo. Relying on underlying security chips and Face ID, it has taken the payment experience to an extremely comfortable extreme—just raise your wrist, scan your face, and done, without even opening an app. This is something PayPal cannot match, which still relies on the three-step experience of redirecting pages, re-authorizing, and waiting for confirmation.

Revolut, representing neobanks, has this mojo. With strong execution power, this emerging enterprise has quickly built a full-stack financial platform covering stocks, currency exchange, and cryptocurrency across dozens of countries, constantly conquering new territories.

These three companies share a common point: their mojo does not come from scale, not from user numbers, and not even from money. It comes from a belief in the product: believing that what they are doing will make a difference in some corner of the world.

And this is just the tip of the iceberg. Shop Pay, Klarna, Affirm, Afterpay, Wise, Cash App, Adyen—every niche in the payment track is crowded.

PayPal once had such a thing. That piece of HTML code, the button that allowed an American uncle selling second-hand goods from his garage and a small factory boss in Guangzhou to complete cross-border settlements, was itself a declaration of changing the world. But the process of losing it was quiet, almost silent.

When talking about PayPal's development in recent years, one cannot overlook Venmo.

Venmo did one thing right: it turned transferring money into a social experience—splitting the bill for meals, sharing rent, sending an emoji to friends is much more fun than a bank transfer. Its spread among young people in the US is more like a social app rather than a payment tool. “Venmo me” has even become a verb, synonymous with transferring money among young Americans.

PayPal's acquisition of Venmo was actually a byproduct of acquiring the payment service provider Braintree. This product, which was not so remarkable at the time, is now a bright spot in PayPal's dim financial report: $1.7 billion in revenue by 2025, over 100 million monthly active accounts, a 50% year-on-year increase in Pay with Venmo transaction volume, and a 40% growth in debit card users.

But behind these numbers, several deep-seated problems are fermenting: those optimistic about it are obsessed with the doubling of debit card transaction volume, believing that this cash cow is entering a period of monetization; while those concerned about it would question if such prosperity is merely relying on exploiting the remaining social circles, how long can this afterglow last?

This division essentially shows that Venmo is caught in a pincer attack in its ecological niche: upward, it cannot breach the hard wall built by Apple Pay and Google Pay; downward, it cannot penetrate the underlying networks buried by Stripe and Adyen. Venmo's growth is strong, but the ceiling is quite apparent.

First is the internal friction of the growth model. A 20% revenue growth rate comes with only a 7% increase in active users—Venmo is no longer expanding but taxing its own users, squeezing more out of the same batch of users without attracting a new generation.

Second is the dual predicament of geography and product soul. Venmo has always been locked in the domestic US market, capturing the American dining table, but has not yet entered the world's cash registers.

Finally, there is the temporary abandonment of the all-scenario financial imagination. PayPal designed a business loop for Venmo that included a shopping plugin called Honey, meant to connect the "discovery-settlement" chain. However, in 2024, Honey nearly collapsed due to a scandal involving the alteration of affiliate links, causing the flow of customers to be cut off, and also diminishing Venmo’s transformation journey.

How does an independent consumer payment application prove itself worthy for users to actively open it? This question is what Venmo is working hard to answer, but the answer remains to be revealed.

Venmo reflects PayPal’s anxieties on the consumer side. At even farther frontiers, PayPal has also bet on two other cards—one called PYUSD, and the other called agent payments. The commonality of these two cards is: the track is broad enough, but the odds are not yet secured.

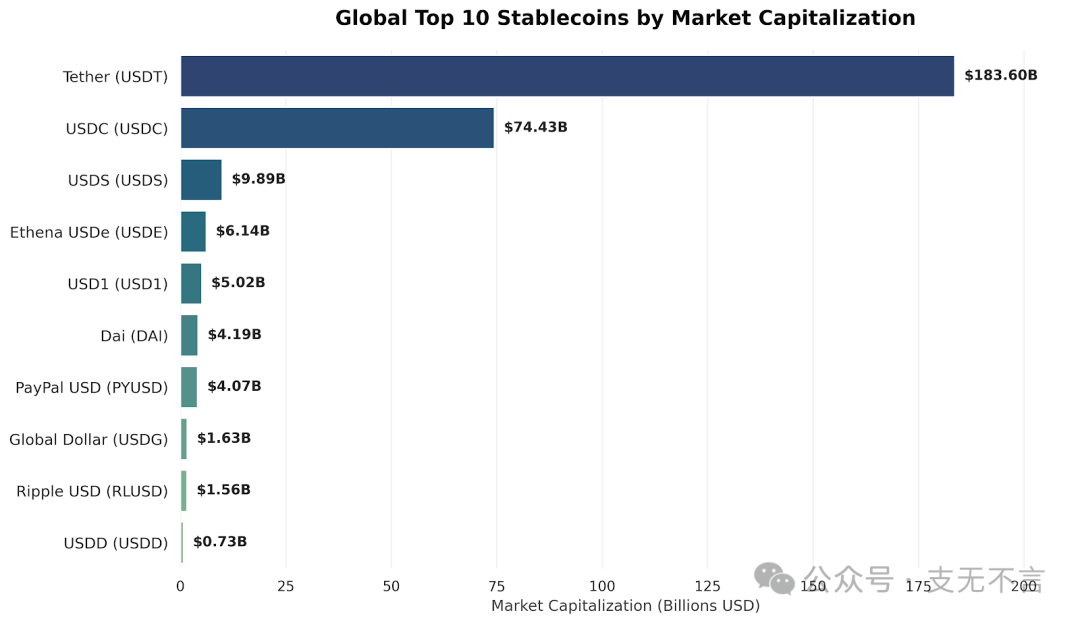

Objectively speaking, PYUSD is doing decently. Since its launch in 2023, it has reached a market scale of $4 billion, ranking among the top ten in global stablecoin market values. However, compared to Tether’s roughly $180 billion USDT and Circle’s approximately $70 billion USDC, the scale of PYUSD can only be considered a mere fraction.

It instead proves one thing: even if everyone can issue stablecoins, the thresholds for channel distribution and user mindset remain very high, and a giant like PayPal cannot hope for a dimension-reducing strike.

When PayPal announced a 4% annual interest rate for PYUSD holders in April 2025, the industry was astonished that a giant was about to kill the competition, but the development of matters is gradual. The trillion-level usage of stablecoins relies primarily on crypto trading for arbitrage, market making, cross-border arbitrage, and gray market fund transfers, DeFi lending, LP, and yield farming's underlying assets, none of which are PYUSD's strengths.

In the future, the usage scenarios for stablecoins will undoubtedly become more commonplace and daily, including cross-border B2B payments, on-chain settlements, and everyday retail. However, competition will also be extremely fierce. Not to mention the two towering mountains of USDT and USDC, innovation-oriented USDe and USD1 backed by the Trump family are also strong competitors, and PYUSD does not have absolute winning odds.

Beyond stablecoins, PayPal is also focused on agentic payments. They have abandoned error-prone web crawlers and instead opted to integrate with merchant order management systems via API. Merchants only need to sign agreements, and PayPal can distribute their real-time data on inventory, colors, prices, etc., to mainstream AI platforms like Google Gemini and PayPal’s own app.

The idea is clear, but this is a market yet to be validated. Recently, Qianwen distributed red envelopes to invite everyone to drink milk tea, serving as market education for domestic consumers about AI shopping. However, changing consumer habits is not a one-time task. Whether chatting with AI to shop will become mainstream or if the primary shopping experience really lies in a person carefully comparing prices remains an unknown.

Even if in the future people truly get used to saying to ChatGPT: "Help me buy a cup of lightly sweetened Oolong tea," the entity controlling transaction retention data will still be the AI platform with a vast user base, which is highly likely to have its own proprietary payment methods or benefit everyone equally. In this entirely new chain, PayPal's position still remains in question.

After discussing so much about loss and uncertainty, you might think that PayPal's story has reached a conclusion.

But things never have just one side. Braintree remains the underlying payment engine for many global platforms. Pay Later processed over $40 billion in transactions in 2025, leading the BNPL market in the US. Launched in August 2024, Fastlane's one-click checkout is one of its rare proactive moves, directly challenging Apple Pay and Shop Pay. Together with 400 million active accounts and over $6 billion in free cash flow throughout the year—these assets are a strategic entry ticket that any company looking to position itself in the AI agency economy era would find hard to replicate from scratch.

Close to thirty years of accumulation has not gone to waste and will not disappear into thin air. It’s just a pity that the great river flows eastward, washing away all things.

The one who understands how to use this ticket the best may no longer be PayPal itself.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。