撰文: @BlazingKevin_ ,the Researcher at Movemaker

SEC 主席保罗·阿特金斯指出整个美国金融市场,包括股票、固定收益、国债和房地产等,可能在未来两年内全面迁移至支撑加密货币的区块链技术架构之上。这可以说是美国金融体系自 20 世纪 70 年代电子交易出现以来最重大的结构性变革。

1. 全面上链的跨部门协作框架与实际贡献

阿特金斯推行的“Project Crypto”倡议并非 SEC 单方面行动,它建立在跨越立法、监管和私营部门的系统性合作之上。实现价值超过 50 万亿美元的美国金融市场(包括股票、债券、国债、私人信贷、房地产等)的全面上链,需要多方机构明确角色和贡献。

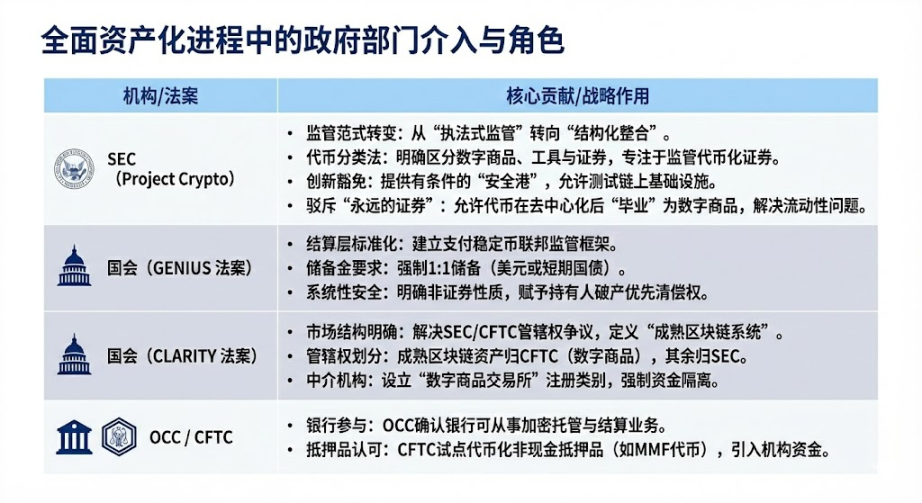

1.1 全面资产化中会介入的政府部门

需要补充说明的是,“Project Crypto”和“创新豁免”机制承认了区块链技术与现有金融法规的不兼容性,提供了一个受控的试验环境,允许传统金融机构(TradFi)在不违反核心投资者保护原则的前提下,探索和实施代币化基础设施。

GENIUS Act 通过创建合规的、有全额储备背书的稳定币,明确监管权移交给银行监管机构,解决了机构在链上进行交易和抵押所必需的 Cash Leg 问题。

CLARITY Act 通过划分 SEC 和 CFTC 的管辖权,明确针对加密原生平台并创建了“成熟”的定义,使得机构能够明确知道其持有的数字资产(如比特币)在哪个监管机构的框架下运作,同时为加密原生平台提供了注册成为联邦监管中介机构(“经纪商 / 交易商”)的途径。

OCC 成立于 1973 年,专门为期权、期货和证券借贷交易提供清算和结算服务,促进市场稳定性和完整性。CFTC 是期貨市場及期貨商的主要管理者。

这种跨部门的协同,是美国金融市场实现全面上链的先决条件,为后续 BlackRock、摩根大通等巨头大规模部署和 DTCC 等核心基础设施的整合奠定了坚实基础。

1.2 传统金融巨头的协作

在美国传统金融巨头的协作蓝图中,各机构的深化布局体现了更为具体的战略侧重与技术细节。贝莱德为首个在公链(以太坊)上发行的代币化美国国债基金,这奠定了其作为资产管理方将传统金融收益引入公链生态的基石地位。

摩根大通在将其区块链业务更名为 Kinexys 后,它允许银行在数小时内而非数天内完成代币化抵押品与现金的原子互换,显著优化了流动性管理;同时,其在 Base 链上试点 JPMD 的举措,被视为向更广阔的公共区块链生态系统延伸的战略性步骤,旨在寻求更强的互操作性。

最后,存管信托与清算公司(DTCC)的具体突破由其子公司存管信托公司(DTC)完成,作为全球最重要的交易基础设施提供商,其获得的 SEC“无异议函”使其能够将传统的 CUSIP 系统与新的代币基础设施连接起来,从而在受控环境中正式开启了包括罗素 1000 成分股在内的主流资产代币化试点。

2. 全面代币化后的金融环境与影响分析

资产代币化的核心目标是打破传统金融的“孤岛效应”和“时间限制”,打造一个全球化的、可编程的、全天候的金融系统。

2.1 金融环境的重大提升:效率与性能的飞跃

代币化将带来传统金融系统难以比拟的效率和性能优势:

2.1.1 结算速度的飞跃(T+1/T+2 到 T+0/ 秒级):

提升: 区块链能够实现近乎实时的(T+0)甚至秒级结算和交割,与传统金融市场通常需要的 T+1 或 T+2 结算周期形成鲜明对比。UBS 在 SDX 发行的数字债券展示了 T+0 结算能力,欧洲投资银行的数字债券发行也将结算时间从五天缩短到了一天。

解决的痛点: 极大地减少了结算滞后带来的交易对手信用风险和操作风险。对于像回购和衍生品保证金这类对时间敏感的交易,结算速度的提升至关重要。

2.1.2 资本效率的革命与流动性释放:

提升: 实现了“原子交割”,即资产和支付在单个、不可分割的交易中同时发生。同时,通过代币化,可以释放当前锁定在结算等待期或低效流程中的“沉睡资本”。例如,可编程抵押品管理每年可释放超过 $1000 亿的被困资本。

解决的痛点: 消除了传统“先交付后付款”操作中的本金风险。降低了对清算所高额保证金缓冲的需求。同时,代币化货币市场基金(TMMFs)可以作为抵押品直接转移,保留了收益,避免了在传统系统中需要赎回现金再重新投资带来的流动性摩擦和收益损失。

2.1.3 透明度与可审计性的增强:

提升: 分布式账本提供单一、不可篡改的权威所有权记录,所有交易历史公开、可验证。智能合约可以自动执行合规检查和公司行为(如派息)。

解决的痛点: 彻底解决了传统金融中数据孤岛、多重记账和手工对账的低效问题。为监管机构提供了前所未有的“上帝视角”,能够进行实时、穿透式监管,有效监控系统性风险。

2.1.4 24/7/365 的全球市场访问:

提升: 市场不再受限于传统银行的工作时间、时区或节假日。代币化使得跨境交易更为顺畅,资产可在全球范围内进行点对点转移。

解决的痛点: 克服了传统跨境支付和流动性管理中的时滞和地域限制,尤其利好跨国公司的现金管理。

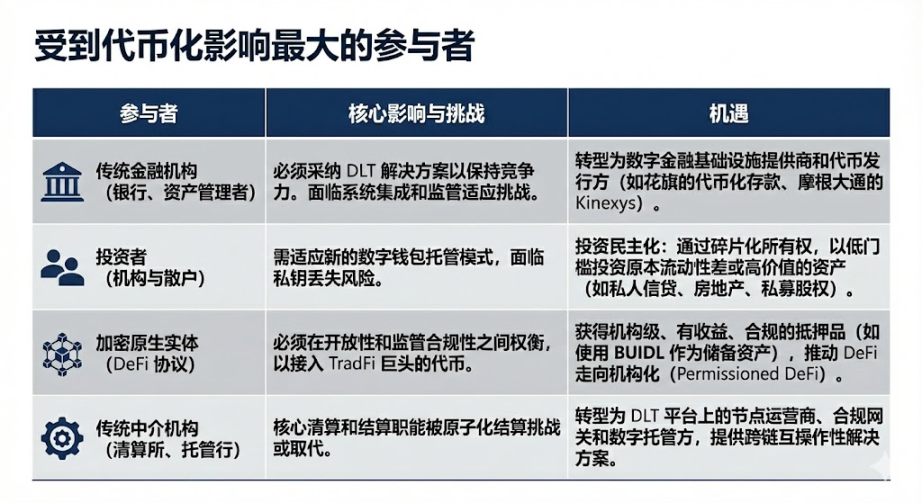

2.2 受到影响最大的参与者

代币化带来的变革是颠覆性的,对以下几类市场参与者产生了最大的影响:

主要挑战与风险:

流动性和净额结算的权衡: DTCC 当前通过对数百万笔交易进行净额结算,将实际需要转移的现金和证券量减少 98%,实现了巨大的资本效率。原子化结算(T+0)本质上是实时全额结算(RTGS),这可能导致净额结算效率的损失,需要市场在速度和资本效率之间寻找混合解决方案,例如日内回购。

隐私悖论: 机构金融依赖交易隐私,而公链(如以太坊)具有透明性。大型机构无法在公开链上执行大宗交易而不被“抢跑”。解决方案是采用零知识证明等隐私保护技术,或在许可型链上操作(如摩根大通的 Kinexys)。

系统性风险的放大: 24/7 市场消除了传统市场的“冷静期”。算法交易和自动化保证金追缴(通过智能合约)可能在市场压力下触发大规模的连锁清算,从而放大系统性风险,类似于 2022 年英国 LDI 危机中的流动性压力。

2.3 代币化基金(TMMF)的核心价值体现

货币市场基金(MMFs)的代币化是 RWA 增长中最具代表性的案例。TMMFs 作为抵押品尤其具有吸引力:

保留收益:与不生息的现金不同,TMMFs 作为抵押品可以持续赚取收益,直到被实际使用,降低了“抵押品拖累”的机会成本。

高流动性和可组合性:TMMFs 结合了传统 MMFs 的监管熟悉度和安全性,以及 DLT 带来的即时结算和可编程性。例如,贝莱德的 BUIDL 基金通过 Circle 的 USDC 即时赎回通道,解决了传统 MMF 赎回需 T+1 的痛点,实现了 24/7 的即时流动性。

3. DTCC/DTC 在代币化过程中的角色

DTCC 和 DTC 是美国金融基础设施中不可或缺的核心系统性机构。DTC 托管的资产规模巨大,覆盖了美国资本市场绝大部分的股票登记、转移和托管。DTCC 和 DTC 被视为美股市场的“总仓库”和“总账房”。DTCC 的介入,是从根本上确保代币化进程的合规性、安全性和法律有效性的关键。

3.1 DTC 的核心角色与责任

身份和规模: DTC 负责中央证券托管、清算和资产服务。截至 2025 年,DTC 托管资产规模达 $100.3 万亿,涵盖 144 万种证券发行,主导着美国资本市场绝大部分股票的登记、转移和确权。

代币化桥梁与合规保证: DTCC 的介入代表了传统金融基础设施对数字资产的官方认可。它的核心责任是充当传统 CUSIP 系统与新兴代币化基础设施之间的信任桥梁。DTCC 承诺代币化后的资产将维持与传统形式相同的高度安全、稳健性、法律权利和投资者保护。

流动性整合:DTCC 的战略目标是通过其 ComposerX 平台套件,实现 TradFi(传统金融)与 DeFi(去中心化金融)生态系统之间的单一流动性池。

3.2 DTC 代币化流程与 SEC 无异议函

2025 年 12 月,DTCC 的子公司 DTC 取得了美国 SEC 具有里程碑意义的无异议函,这是其大规模推进代币化业务的法律基础。

3.3 DTC 代币化带来的影响

DTC NAL 的批准被认为是代币化的里程碑,其影响主要体现在:

官方代币的确定性: DTC 的代币化意味着美国官方背书的代币化股票即将来临。未来进行美股代币化的项目方将可能直接接入 DTC 的官方资产代币,而非自行构建资产上链基础设施。

市场结构整合: 代币化将推动美股市场向 CEX+ DTC 托管信托公司”的模式发展。纳斯达克等交易所可能直接下场扮演 CEX 的角色,而 DTC 管理代币合约,并允许提币,实现流动性的完全打通。

增强抵押品流动性: DTC 的代币化服务将支持增强的抵押品流动性,实现 24/7 访问和资产可编程性。DTCC 已经探索利用 DLT 技术优化抵押品管理近十年。

消除市场割裂: 股票代币不再是与传统资产割裂的数字类型,而是完全融合到传统资本市场的总账本中。

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。