Original Title: The Hitchhiker's Guide to Agentic Payments

Original Author: @13yearoldvc

Translated by: Peggy, BlockBeats

Editor's Note: We are standing at a new critical point. Agentic Payments are reshaping the fundamental logic of transactions. From internal checkouts in ChatGPT to micropayments between agents, and a new order of machines paying for content—the picture of the "agent economy" is gradually taking shape.

If you are interested in the integration of AI and blockchain, the implementation path of next-generation payment protocols, or are contemplating the automation trends of future business, this article is worth your time to read carefully.

Below is the original text.

Preface

This is a lengthy article, but it is absolutely worth reading. It gathers insights from several leading builders who are shaping the future of Agentic Payments. We will explore the real problems they are trying to solve, the possible implementations of these technologies in practice, and the true bottlenecks behind them.

You can think of it as a guided journey into the frontier. Ten pages of content cover creativity, experimentation, and experiences from those building the infrastructure for the machine economy. Get ready to embark.

As the coordinator of ERC-8004 and an AI advisor for the Ethereum Foundation's decentralized AI (dAI) team, I have closely collaborated with builders, researchers, and protocol teams over the past few months, focusing on the intersection of stablecoins, decentralized infrastructure, and AI. This has allowed me to observe the real-time evolution of these technologies up close. This article is not only a presentation of research findings but also a genuine context from the builders of the intelligent economy.

Special thanks to the following individuals for their reviews and discussions (listed in alphabetical order by surname):

@louisamira (ATXP), @RkBench (Radius), @DavideCrapis (Ethereum Foundation), @nemild (Coinbase/x402), @CameronDennis (Near Foundation), @marco_derossi (Metamask), @dongossen (Nevermined), @jayhinz (Stripe/Privy), @sreeramkannan (EigenCloud), @kevintheli (Goldsky), @MurrLincoln (Coinbase/x402), @benhoneill (Stripe/Bridge), @programmer (Coinbase/x402), @FurqanR (Thirdweb), @0xfishylosopher (Pantera Capital).

The Shift to Agentic Payments

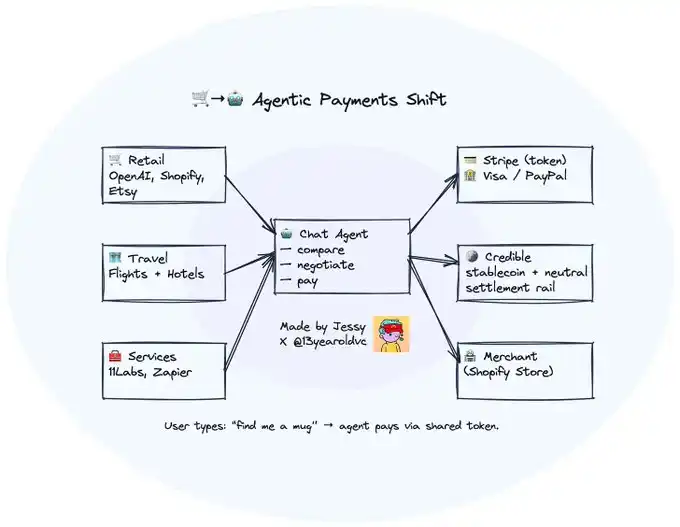

A month ago, Stripe and OpenAI launched a new feature that could change the way we shop online: you can now buy things directly within ChatGPT. No forms, no redirects, no checkout pages. Just a simple sentence: "Help me find a handmade ceramic mug," and the system will automatically complete the payment through Stripe's "shared payment token."

This process seems very smooth, even a bit magical, but it is built on a highly centralized architecture that may limit the space for true innovation in the future. Payment tokens, settlement channels, and even user identities are controlled by these two platforms, OpenAI and Stripe. In this model, while agentic payments are convenient, they cannot be freely combined and can only operate within specific ecosystems. This not only showcases future possibilities but also reminds us: without open standards and a neutral settlement layer, agentic payments will be locked into platforms, making it difficult to truly unleash their potential.

At the same time, this new payment process marks a larger shift: the real transactions are no longer conducted by the users themselves, but by "agents." The interfaces we input are beginning to replace us in price comparisons, negotiations, and even payments. Business is gradually being consumed by "agentic commerce."

Currently, it seems that three things are happening simultaneously: agents are beginning to replace humans in transactions; these transactions are likely to settle on crypto networks rather than traditional financial systems; and this may become a breakthrough application scenario for the true integration of blockchain and artificial intelligence.

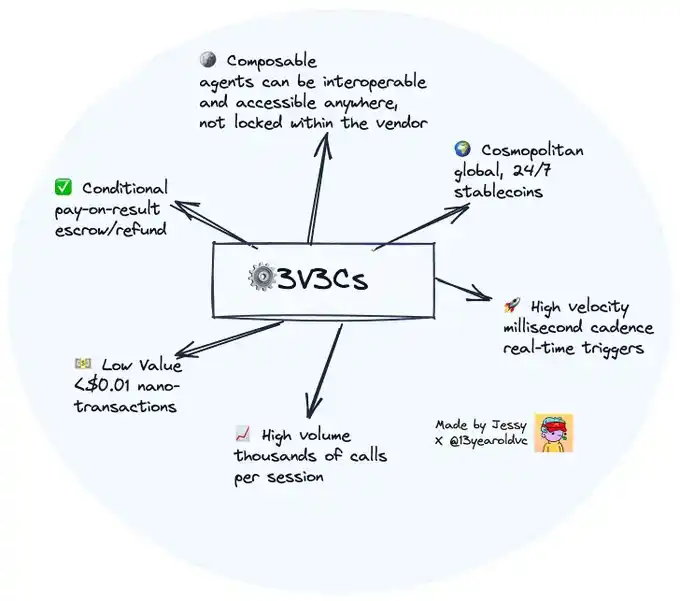

Why stablecoins and blockchain? Because the forms of these transactions are completely different from those designed for Visa or PayPal. The agentic economy is filled with small, condition-triggered, composable, high-frequency payments—fast, granular, and wide-ranging.

After discussing with Robert Bench from Radius, we found that "3V3C" is a very fitting descriptive model: high velocity (Velocity), high volume (Volume), low value (Value), conditional (Conditional), composable (Composable), and cosmopolitan (Cosmopolitan).

We observe three emerging behavioral patterns:

Humans pay agents (2C, 2B, complex optimization scenarios);

Agents pay other agents or humans;

Agents pay the entire network.

These three behaviors break the fundamental assumptions of traditional payment systems.

1. Human → Agent

The chat interface is quietly becoming the new consumer entry point. Transactions that were previously initiated in a browser are now being completed in conversations.

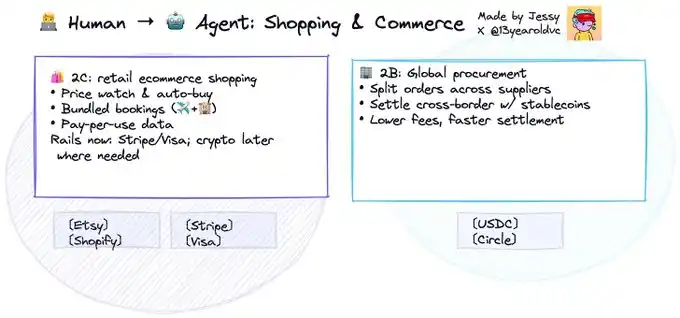

You can now directly purchase Etsy products through ChatGPT's "instant checkout" feature, and in the future, Shopify will also integrate this process, supported by Stripe. Google, Amazon, and Perplexity are also testing similar shopping models, allowing AI assistants to help users discover and purchase products within chat windows.

These AI frontends are turning into digital stores, especially in retail e-commerce (2C) scenarios—product discovery, price comparison, and purchasing are all completed in one process. Over time, people will increasingly rely on their AI agents as personal shoppers, travel planners, or booking assistants.

Interestingly, the behavior of these agents differs from that of humans: they can monitor prices in real-time and automatically place orders when discounts appear; coordinate multi-party transactions (such as booking flights and hotels simultaneously); and pay for data or service fees on demand, rather than relying on subscriptions (which we will discuss in detail in the "Agent → Network" section).

In the short term, most of these payment processes will still be completed through traditional channels like Stripe or Visa—this is fine. For retail e-commerce (2C), the existing infrastructure is already sufficient to support the "Human → Agent" interface, at least for now.

The real power of crypto payments comes into play in the global procurement (2B) segment.

Many overseas merchants and manufacturers still face issues of settlement delays and high costs because they struggle to access SWIFT or traditional agency banking systems. For example, in Yiwu, China, the world's largest wholesale market for small commodities, most small merchants have yet to hear of stablecoins. However, once the regulatory environment matures, this will become a natural application scenario.

Stablecoins can enable instant, low-cost, and transparent cross-border value circulation—just as crypto remittances have already surpassed Western Union in certain regions.

Whether on the consumer side or the enterprise side, we will see some new user behaviors that were previously unattainable: complex, condition-triggered transactions that conform to the "3V3C" model, automatically completed by agents in the background. Especially as large language models (LLMs) become smarter and operational costs decrease further, the cost savings from these transactions will far exceed the required token fees.

For example:

A procurement agent can monitor multiple multinational suppliers simultaneously, automatically splitting orders to the cheapest manufacturers and negotiating shipping costs within budget;

A creative agent can bundle subscriptions for multiple SaaS tools, dynamically renewing or canceling services based on usage.

This also means that agents must possess "composability": the output of one agent can become the input of another, forming complex multi-step workflows (such as agent clusters or cross-model thinking chains). In the past, we talked about "funding Legos," and now we also need "agent Legos."

In practical terms, "composability" means the need for standardized APIs, message formats, and permission management. Without these, agents are like applications without APIs, isolated from each other and unable to collaborate.

Therefore, these transactions are too complex, too high-frequency, and too reliant on combinations and collaborations to be coordinated by humans or traditional payment systems—but for agents running on programmable payment systems, it is a piece of cake.

2. Agent → Agent

In the future, agents will need to "hire" other agents—even humans—to complete tasks.

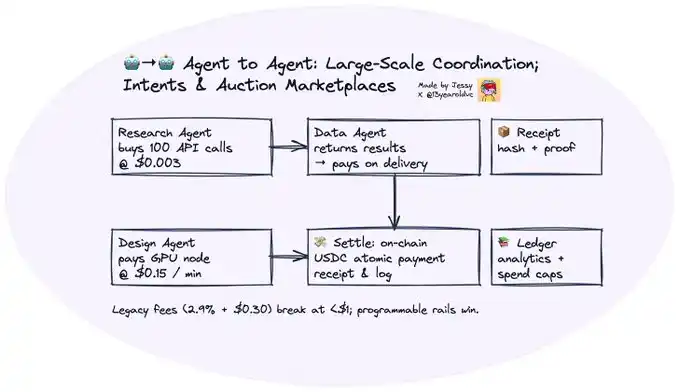

Existing business models (subscriptions, licenses, paywalls) do not apply to interactions between autonomous software. Payments between agents are often billed by the number of calls, the amount of tokens, or the number of inferences, with amounts potentially as low as a few cents or even less.

Imagine a research agent purchasing 100 API calls from a data agent; a design agent paying for GPU usage time from a compute node. These are transactions between machines, high frequency, and low amounts.

For instance, an agent may need to pay another agent $0.003 for 100 API calls, or $0.15 for GPU computation, or even just $0.0001 per inference.

Traditional payment systems cannot handle transactions of this scale—credit cards charge a fixed fee for each transaction (e.g., 2.9% + $0.30), making it impossible to operate in this scenario.

However, from a user experience perspective, these transactions may not necessarily settle in a "high-frequency, low-amount" manner. For example, on platforms like OpenRouter, businesses send millions of API calls each month, and the settlement method is through stablecoin top-ups, which is more efficient than going through the payment process for each transaction.

A more futuristic scenario is: if each robot is equipped with an agent responsible for tasks, data, and operations (possibly also through prepaid credits). For example, a drone may need to pay for weather data, navigation updates, or temporary use of a private delivery route.

This is why we need a new programmable payment structure. Agents should be able to: set budgets and rules; prepay fees; settle instantly upon task completion, accompanied by proof of work.

In other words, crypto payments make "atomic payments" between autonomous entities possible.

As time goes on, the payment behaviors of agents will no longer be limited to interactions between AI services. They may directly "hire" global human contributors, especially in international markets where stablecoins already have practical payment capabilities. This trend is not far off—we have already seen related experiments in our discussions with builders, and large-scale applications could emerge within the next one to two years.

This model is very similar to the logic of remittances. Imagine a freelance platform aimed at agents, similar to Fiverr:

A marketing agent can automatically commission dozens of micro-influencers in Southeast Asia, making automatic payments once their interaction data reaches a preset threshold;

A data labeling agent can recruit labelers from Kenya or Bangladesh, paying them small amounts in real-time per task, rather than relying on bulk invoice settlements.

Once agents can transfer funds instantly and globally, labor itself begins to resemble an API call.

From a market design perspective (which is a unique advantage of crypto systems), when there are hundreds of thousands of autonomous entities composed of humans and agents globally, another trend will emerge: intent and bidding markets. Agents will compete around task requests.

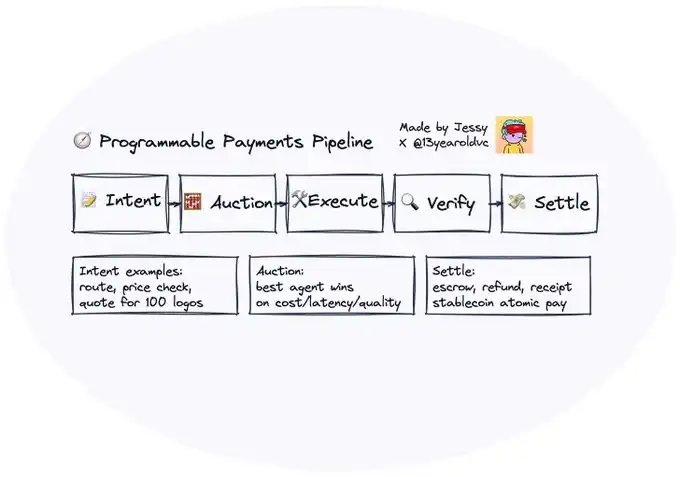

The best-performing agents will be rewarded (with stablecoins, reputation scores, or on-chain credit limits); poorly performing agents may lose their deposits or reputation. This is precisely the vision we envision and hope to build in ERC-8004.

A preliminary model might include:

Intent Layer: A shared agent registration system (like ERC-8004) for publishing structured requests and verifying agent identities;

Bidding Layer: Task allocation completed through mechanisms like Dutch or English auctions;

Evaluation Layer: Tasks completed verified by crowds, other AI agents, or oracles, with rewards automatically distributed;

Settlement Layer: Payments made via stablecoins, with updates to reputation and staking status on ERC-8004.

In the past, decentralization was often seen as inefficient—partly because human actions are slow and coordination costs are high. But now, agents are eliminating these bottlenecks: they can continuously assess who is best suited to perform tasks, what prices are reasonable, and which data is trustworthy.

Blockchain plays the role of a "state coordination layer" here—an immutable shared memory system for recording results, deposits, and points; while stablecoins serve as micropayment channels for real-time value exchange (pay-per-response, pay-per-action).

This complex "Agent ↔ Human" collaboration scenario is precisely the problem that blockchain and stablecoins are best suited to solve. Interoperability allows agents to communicate, and composability enables them to collaborate.

3. Agent → Network

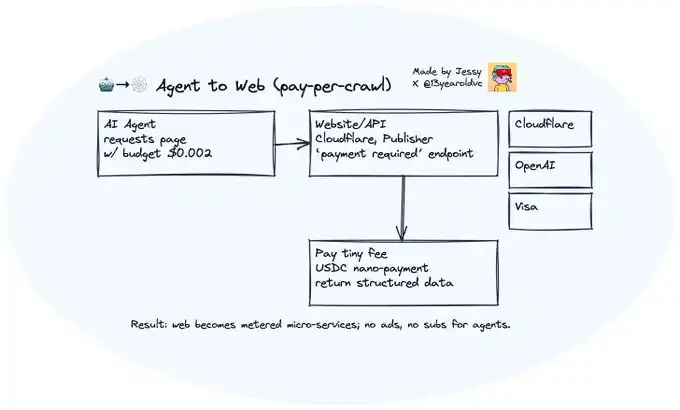

Another trend worth noting is that the users of networks are no longer just humans; an increasing amount of content is being crawled, read, and interacted with by AI agents, and in the future, it may even be dominated by agents. This means that websites will no longer charge only humans but will begin to charge machines as well—we call this "pay-per-crawl."

For example, publishers are pushing back against unrestricted content scraping. Anthropic recently paid $1.5 billion to resolve copyright lawsuits with authors—one of several cases testing whether AI companies can freely use copyrighted content. OpenAI, Microsoft, Meta, and others are also embroiled in similar disputes. The reasonable outcome may ultimately be that training data and content usage will adopt a "pay-per-access" model.

Meanwhile, Cloudflare (reportedly handling about 20% of web requests through its network) is experimenting with a new model: websites can charge agents nano-level fees (even below micropayments) to allow access to their data. They have also recently launched their own stablecoin—NET Dollar.

This is where crypto payments come into play again.

Websites and APIs can open a "payment required" interface, allowing agents to pay just a few cents or even less to read, query, or consume content without needing subscriptions or ads. This will transform the web into a system composed of microservices, where value flows no longer depend on monthly billing cycles but occur in real-time.

If you're interested in the early "402 status code" of the internet and related discussions by Andreesen and others, Jay Yu from Pantera Capital has written a great article that delves into this evolution.

Imagine a mailroom in the 1950s, where people are stuffing bills and invoices into envelopes. This inefficient process is one of the reasons we eventually adopted "Net 30" payment terms.

In reality, the "pay-per-crawl" economic model will exhibit a power-law distribution. Only a few high-traffic or high-value websites—those with data that agents truly need—will actively integrate this monetization logic. For most websites, the costs of measuring, charging, and settling agent traffic will far exceed the benefits. In other words, we believe that ultimately only a few large publishers will capture most of the revenue, while long-tail websites will remain open access or unable to monetize.

This is where intermediary platforms like Cloudflare could change the curve. If Cloudflare can enable websites to "turn on agent payments" with a switch—and handle authentication, measurement, and settlement through protocols like x402 or Web Bot Auth—then the barriers to entry will be significantly lowered.

Cloudflare can automatically recognize authorized agent requests, charge nano-level fees on behalf of the website, and automatically distribute revenue.

In this model, the open web itself will gain a native machine commerce layer: any webpage can become a billable API, and any agent can seamlessly pay while browsing, crawling, or learning.

This trend is not limited to data access. Almost all online services that can be used on a per-instance basis may shift to a "pay-per-use" model in the future. In discussions with Louis Amira, co-founder of ATXP, we explored how businesses could open new revenue streams through agent payments, citing a few examples: LegalZoom could charge $2 for an NDA; if the payment experience is smooth enough, Netflix could charge $0.50 per episode; Replit could charge based on the number of tokens, allowing unlimited "vibe-coding," charging $1.23 per million tokens; PitchBook or Bloomberg could allow agents to pull valuation models for a one-time fee of $0.25; hospitals could charge per record, providing anonymized cancer scan data for model training.

Louis began taking screenshots of the "forced upgrades" or "unnecessary paywall" scenarios he encountered—these companies could have adopted per-instance billing, turning him into a customer.

Ideally, enterprise developers could quickly launch temporary API interfaces, billing per instance rather than through monthly subscriptions; writers or researchers could sell single segments of text, charts, or datasets per query.

Conversely, agents could also access non-public data APIs on request, querying supplier data that cannot be crawled by web pages, using prepaid micro-requests. This model is particularly suitable for long-tail APIs and enterprise datasets.

Coinbase's CDP team has already made early attempts on Payments MCP, allowing LLMs to use on-chain tools like wallets and payment functions without API keys.

The internet is beginning to resemble less a collection of subscription bundles and more a "real-time billing system"—where every interaction has pricing, payment, and settlement, and value flows continuously.

We are still in the early stages, but integration is happening.

After completing a round of comprehensive research, our conclusion is that while the imaginative space for intelligent agent payments is vast, it is still in its early stages. One of the biggest challenges is that payments themselves are one of the most heavily regulated and complex areas of the internet. Their implementation often depends not on technical feasibility but on whether integration and interoperability with large enterprises and financial networks can be achieved. This makes progress inherently slow.

For startups, even if the underlying technology exists, without access to banks, card organizations, or mainstream payment processors, it is nearly impossible to conduct meaningful experiments.

In the future, enterprise-grade, compliance-grade solutions are likely to emerge. Therefore, teams like Catena Labs are building the Agent Commerce Kit, focusing on agent authentication, payment interactions between humans and agents, and targeting licensed financial institutions, regulatory compliance, and enterprise-level application scenarios. PayPal is also likely to explore similar directions.

How far are we from true intelligent payments?

Currently, most so-called "agents" are still just semi-autonomous systems. Technically, they resemble complex workflow automation tools rather than intelligent entities capable of autonomous shopping or negotiation. As Kevin Li from Goldsky said, "You can't really sell 'fully automated commerce' right now; most AI companies are still doing workflow automation."

The short-term opportunity lies in the "semi-autonomous middle ground": human-initiated actions triggering API-level per-instance settlements, completed through stablecoin channels. While these processes are not yet fully agentic behaviors, they are already using the same infrastructure—low-latency programmable wallets, per-call measurement, instant settlement—these are the core components that true "Agent ↔ Agent" commerce will rely on in the future.

Meanwhile, the underlying blockchain also needs to evolve. Intelligent payments require stablecoin channels to have high throughput, low latency, and privacy protection. Next-generation payment-oriented public chains are being explored by major players, such as Stripe's new chain Tempo and Circle's native chain, and we also look forward to more teams focused on agents and stablecoins emerging in the Ethereum L2 ecosystem (like Thirdweb). All of this indicates that the infrastructure for programmable currency is being rebuilt from the ground up to support millions of micropayments and nano-payments per second.

In addition, programmable wallets and server-side architectures must also be upgraded in sync. If wallets still assume that humans manage the mnemonic phrases, none of this can be realized. Intelligent commerce requires strategy-based server-side hosting—capable of programmable budgets, rate limiting, spending scopes, multi-signature/TEE control, and auditable authorization mechanisms.

This is precisely the significance of programmable wallets: they provide agents with callable key management and policy execution capabilities without the need to "hold mnemonic phrases." As Jamie Hinz from Privy pointed out, four years ago we might have been trying to transform Fireblocks or MetaMask into this form; today, the entire tech stack is being tailored for agents, enabling them to complete transactions within a policy framework rather than relying on passwords—security and automation are beginning to merge rather than oppose each other. (If you want to delve deeper, I recommend reading Privy's article on natural language control and policy execution.)

More importantly, this trend has already begun to manifest. Even Visa and Mastercard are adjusting their networks to accommodate intelligent agent commerce, launching Trusted Agent and Agent Pay protocols based on Web Bot Auth—indicating that authentication, authorization, and settlement are rapidly converging, whether in blockchain or traditional payment channels.

We may be just one or two key breakthroughs away from truly realizing this vision.

Once payments become programmable, the way the internet behaves will also change. Every action can be priced, paid for, and settled in real-time. Every agent, whether a model or a human, can receive instant rewards for their contributions.

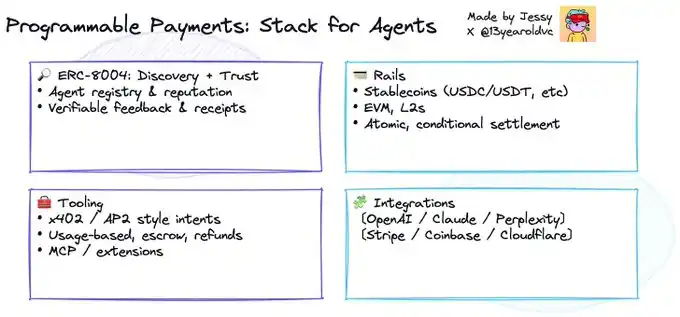

As the infrastructure gradually improves, two key standards are emerging: ERC-8004 provides a trust layer that allows agents to discover and collaborate without centralized intermediaries; x402 enables instant, frictionless payments between agents.

Together, they form the underlying pipeline of the intelligent agent economy.

We envision a future where Agent A finds Agent B through the ERC-8004 registry, negotiates service content, and then completes payment instantly through a smart payment protocol like x402, with settlement occurring on Ethereum's neutral financial layer.

To achieve true agent collaboration, they must have interoperability—capable of discovering, communicating, and exchanging data through shared protocols; they must also have composability—where capabilities can build upon one another.

As Lincoln Murr from Coinbase said, "If payments between machines are dominated by stablecoin channels, it could drive widespread acceptance of stablecoins across the internet. While Visa and Mastercard still dominate human-facing payments, agents will become the 'Trojan horse' for the proliferation of crypto payments."

The internet took 20 years to evolve from web pages to applications, and another 15 years from applications to platforms. Agents will compress this cycle. Commerce will no longer be something you "actively do," but will transform into a process that "automatically happens"—quietly, continuously, and everywhere.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。