作者:Zhou, ChainCatcher

数字资产财库(DAT)模式一度被视为加密投资的创新路径,公司通过持有加密资产作为储备,推动股价上涨,形成“买币-融资-再买币”的飞轮。

但如今市场观点似乎开始转向:一方面,DAT 公司今年累计融资已超 200 亿美元,部分机构投资者认为高峰已过。另一方面,做空声音渐起,投资者开始质疑是否会出现集体抢跑,财库模式究竟是长期护城河还是短期投机工具。

本文围绕投资者关注度较高的话题展开讨论,并采访和总结了一些机构对于当前DAT趋势的看法。

DAT 股票值得投资吗?为什么不直接选择买币或买 ETF?

普通投资者在评估 DAT 股票时,常纠结于其是否优于直接持有加密货币或通过 ETF 间接曝光。

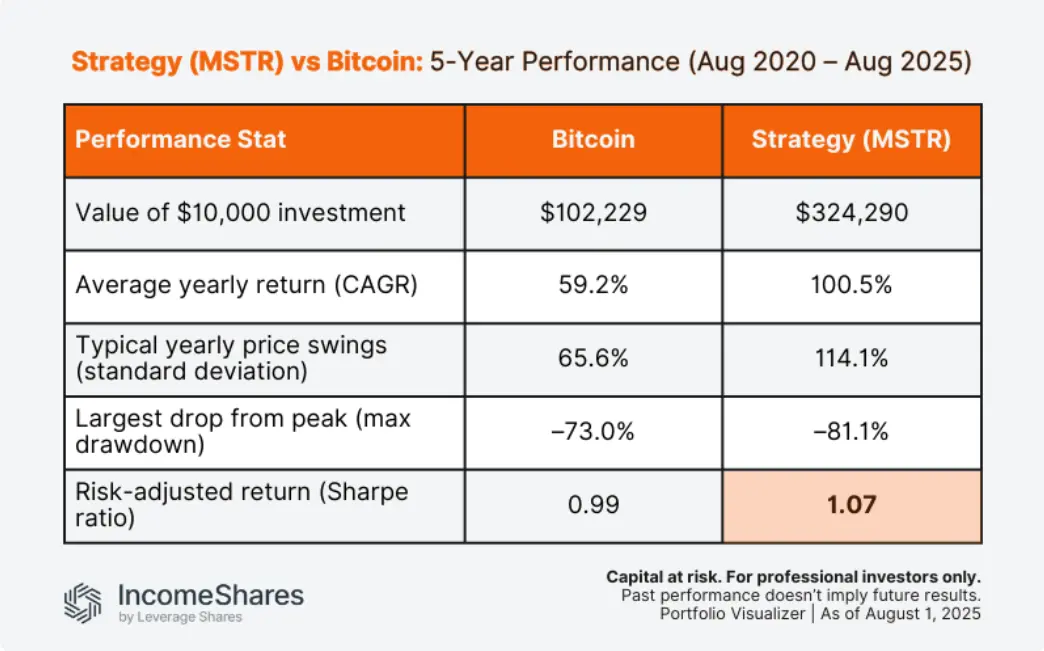

DAT 公司股票提供杠杆效应,以 MicroStrategy 为例,Portfolio Visualizer 的数据,以10,000 美元为投资起点,2020 年 8 月至 2025 年 8 月期间,比特币上涨至 102,229 美元,而 MSTR 则飙升至324,290美元。MSTR 的波动性更高(114% vs 65.6%),年化回报率也更高(100.5% vs 59.2%),这使得其夏普比率高于比特币。当然,这得益于公司通过债务融资放大比特币持有量。

孙宇晨曾公开表示,传统的ETF可以让你接触加密货币价格,但仅此而已。DAT则更进一步,它们让资产发挥作用。这些DAT并非闲置,而是在DeFi和收益协议中质押、借贷和部署资本,赚取实际回报,同时保持链上完全透明。这种模式将数字资产从投机性持有转变为高效的金融引擎,其表现远超ETF。

然而,Forbes 分析师 Alexander Blume 表示,DAT公司使用非常复杂的金融产品利用了散户投机、债务工具、市场营销以及法律和司法套利等因素,希望能跑赢比特币。其中一些策略面临着黑天鹅式的风险,它们看起来表现良好,直到突然失败。

CoinShares 表示,DAT 股票的风险高于 ETF,因为它们不仅受加密价格影响,还涉及公司运营和债务负担。这种新兴模式存在一些风险,可能被当前的牛市所掩盖。而那些追求山寨币或模因币但缺乏可持续核心业务的公司,会让投资者面临更高的波动性和不确定性。如果币价停滞或下跌,这些公司很快就会过度杠杆化,并容易受到剧烈回调的影响。

相比之下,直接买币提供完全所有权,但也需应对保管和税务复杂性;ETF 降低了加密货币的门槛,需要支付一定的年费(一般是0.25%),交易便捷但缺少杠杆。Halborn 顾问团队指出,DAT 适合寻求高回报的投资者,但 ETF 更适合风险厌恶者,因为后者分散化更好,避免单一公司破产风险。

据粗略统计,2025年9月,DAT股票宣布储备后24小时平均上涨150%,吸引短期资金。然而风险与之并存,2025年下半年以来,Metaplanet 股价已跌去超七成,市值已跌破其比特币储备价值,mNAV 比率降至 0.99,市场信心明显不足。

财库趋势能持续多久?财库币本身的价值几何?

财库趋势自 MicroStrategy 开启以来,已吸引多家公司效仿。2025 年,全球已有超过 160 家上市公司将比特币、以太坊等加密货币纳入企业资产负债表,总持仓价值已突破 2,400 亿美元。

其中,截至10月6日,统计中的全球上市公司(不含挖矿公司)合计持有比特币总量为 864,210 枚,当前市场价值约为 1,074.3 亿美元,占比特币流通市值的 4.34%。

传统资金进来推高了估值,也引发了人们对泡沫的担忧。Presto研究主管Peter Chung表示,尽管财库公司崩盘的风险确实存在,但与加密货币上一次兴衰周期中出现的崩盘情景相比,它们更为微妙。

随着溢价收窄、主流标的已被覆盖,资金关注点正转向执行、规模化与并购整合,且对传统加密初创融资形成挤出效应,市场对DAT趋势的持续性产生质疑。业内专家预测,包括知名科技巨头在内的大型公司将在 2025 年底开始建立比特币头寸。对于中小型企业和大型企业来说,问题已经从“是否”转变为“何时”。

华兴资本Web3业务部负责人 Patrick PAN 对 ChainCatcher 表示,任何新兴市场在早期都会经历“专业机构引领—中小玩家涌入—优胜劣汰再集中”的周期。目前的中小型 DAT 更多还处在“实验阶段”,对市场教育是有积极意义的。但最终能长期存续的一定是合规透明、资本结构清晰、具备稳定收益模型的头部财库。

今年以来的趋势是,DAT的币种选择从比特币扩展至ETH、Solana、BNB,甚至是XRP、AVAX、ENA、IP、狗狗币等山寨币,呈现出多元化趋势。Patrick PAN 表示,这其实是市场自然选择的过程。短期内,一些小币种被纳入是为了提升收益或试水机制,但长期来看,优质资产仍会占据主导。

不过,Elementus 分析师曾提到,投资山寨币储备的企业面临着额外的风险,这是一种分散性较差的押注。在市场崩盘时,山寨币通常与比特币具有更高的相关性,但在某些情况下,它们可能无法平等地分享比特币的“优质资产迁移”地位。

财库究竟是护城河还是收割器?怎么看待投机化风险?

目前来看,DAT浮盈规模庞大,如Strategy比特币持仓仍浮盈超 245 亿美元,迄今收益率为 51.91%,这些财库公司是否存在提前兑现利润的可能?

做空机构 Kerrisdale Capital 在 X 平台发文宣布已做空以太坊财库储备公司 Bitmine 的股票,其认为所谓 DAT 模式已经变得平庸且毫无新意。该机构表示,稀缺性和类似meme的热情曾经让溢价在不断稀释的情况下保持高位,但这些条件已经消失了。

据悉,自1011崩盘事件以来,BitMine 仍在持续买入以太坊,目前已增持近 38 万枚,价值约合 15 亿美元,总持有量已超 300 万枚。

目前来看,财库公司仍然承担着加密市场的主要买方角色,但在净资产随价格回落而缩水的阶段,其追加资金的能力受限,边际买盘的强度下降。

机构预测到明年年初仍会有新项目推出,但融资额度会更小。至于规模高达 5 亿至 10 亿美元以上的 DAT 巨额融资,只有少数市值高且波动性足以支持可转换债券的参与者能够真正筹集到这些资金。

Bit Digital 首席执行官 Sam Tabar 在新加坡 Token 2049 峰会期间表示,数字资产国库(DAT)公司应考虑采用无担保债务融资替代有担保债务,以更好地应对潜在熊市。提升每股加密资产持仓最高效的方式是债务融资,在股本不变的前提下增加加密资产持仓虽好,但融资类型选择至关重要——错误的杠杆足以摧毁企业。

Presto 的数据显示,DAT公司融资中只有三分之一是通过债务融资的,而且其中 87% 的债务是无担保的。Chung 认为,即使在最坏的情况下,潜在抵押品的比例也远低于 2021 年周期的杠杆水平,因此只要坚持这一原则,追加保证金就不太可能出现系统性清算风险。他指出,这并不意味着加密货币资金管理公司永远不会出售其持有的加密货币。在不可预见的情况下,如果急需现金,且没有其他资金来源,加密货币资金管理公司可能会清算这些资产。

在加密行情下跌时,财库公司如何缓冲风险?数字资产财富管理平台 Amber Premium (纳斯达克代码:AMBR)总裁 Vicky Wang 在接受 ChainCatcher 采访中表示,下行周期的关键不在“赌方向”,而在于系统化的“防御-调节-保障”:从资产与流动性的降波管理、到以纪律化再平衡与估值偏离管理稳定 mNAV 锚、再到托管分层与透明披露,把操作风险与信息不对称降到最低。

同时,DAT 的策略谱系也在快速分化:单一币种暴露更依赖长期叙事与承压能力,多币种组合考验相关性与再平衡机制,面向更复杂结构的策略则需要衍生品、流动性、会计与合规交叉的专业 skill set。

对于短期的投机化风险,Vicky Wang 表示,这不是一条可持续的路。一个DAT的成功依赖于基础资产的长期投资价值。加密市场强周期性意味着大多数 DAT 都会共同经历起伏,穿越周期靠的是“认知与机制”的双轨治理。

结语

总体看,DAT股票本身适合寻求高回报的投资者,而财库融资买币的趋势取决于各个公司的融资能力(成本和方式),它们若是注重长期治理,DAT便是护城河,否则便成了投机陷阱。优秀的财库公司绝不是简单的追逐币价Beta,而是通过经营与治理维持mNAV 长期正溢价。加密投资者更应聚焦基本面稳健的公司,谨慎评估回撤与套现策略。

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。