There are many important things to manage, but nothing is more important than risk.

Written by: Spicy

Translated by: Luffy, Foresight News

There are many important matters in trading, but nothing is more important than risk management.

I was a professional trader and have been involved in cryptocurrency trading for 8 years. Thank you for taking the time to read this article; in return, I will share my knowledge of risk management with you without reservation.

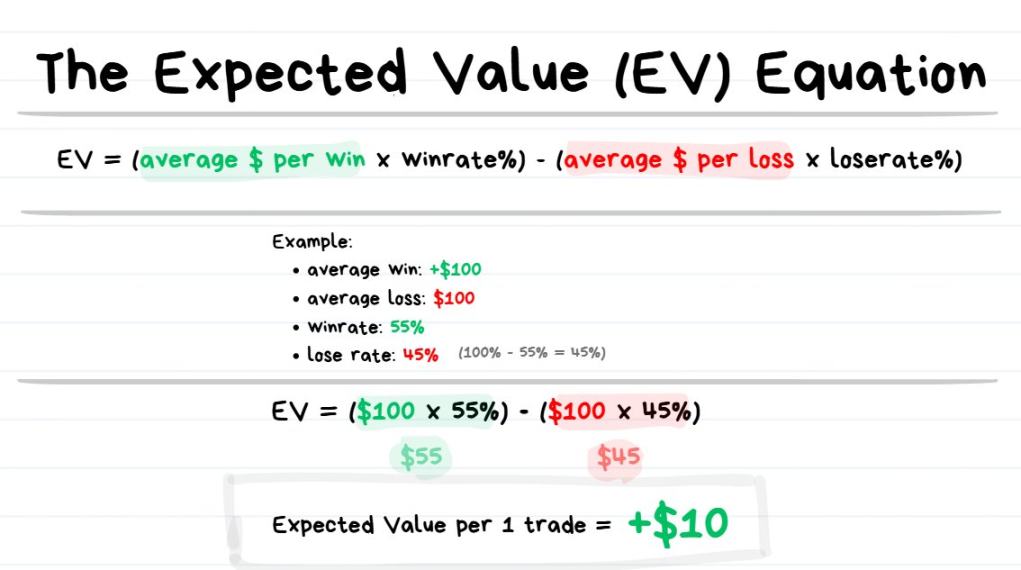

Expected Value (EV) Formula

Expected Value Formula: EV = (Average Profit × Win Rate) - (Average Loss × Loss Rate)

Tip: Expected value refers to "the average result you can expect when making the same decision repeatedly."

Every trader must understand the concept and calculation of expected value. Why is expected value so important? The expected value of trading helps us estimate "the expected profit after making N trades in the future."

For example, if the expected value of each trade is +$10, then after making 1000 identical trades, your expected profit would be approximately $10 × 1000 = $10,000.

If you have a positive expected value (+EV), trading will be profitable in the long run;

If you have a negative expected value (-EV), trading will ultimately incur losses in the long run.

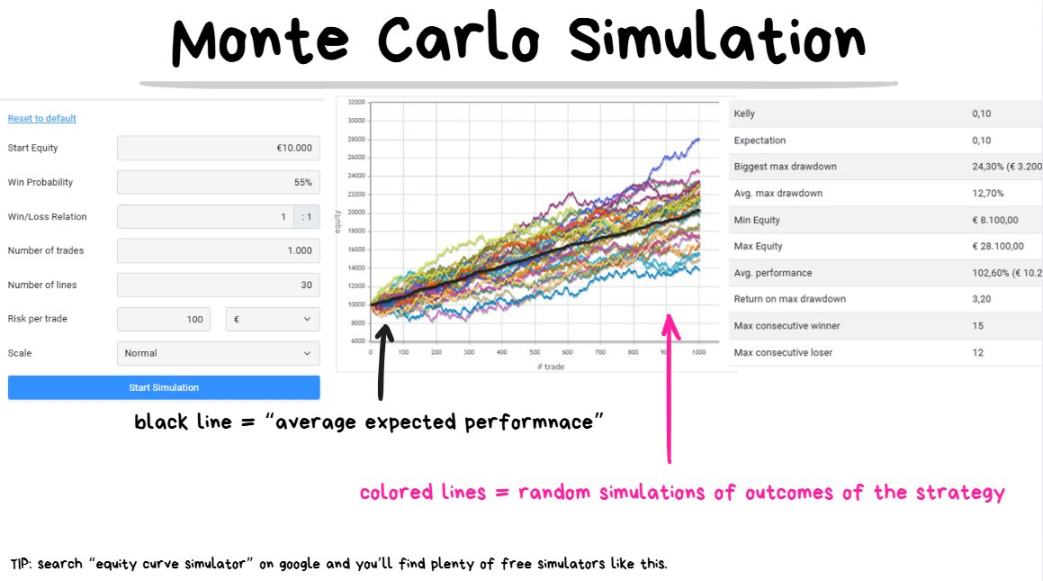

Next, I will introduce "Monte Carlo Simulation," which can visually present the actual effects of expected value.

Monte Carlo Simulation

First, a quick understanding of Monte Carlo Simulation

Assuming a trading strategy has a win rate of 55% and a risk-reward ratio of 1:1, we will conduct 30 simulations of its performance over the next 1000 trades. This is a profitable strategy with a positive expected value (+EV).

Tip: Monte Carlo simulation refers to predicting all possible outcomes after making N trades by running a large number of random hypothetical scenarios.

Monte Carlo simulation helps us manage expectations and roughly assess the profit potential of a strategy.

Simply input the initial capital, win rate, average profit-loss ratio, and number of trades, and the simulation program will generate random combinations of possible trading performance.

The thick black line in the chart represents the average expected result: if the expected value of each trade is +$10, the total profit after 100 trades would be approximately +$1000; after 1000 trades, the total profit would be approximately +$10,000.

Please note the word "approximately," as results cannot be guaranteed and may have some variance.

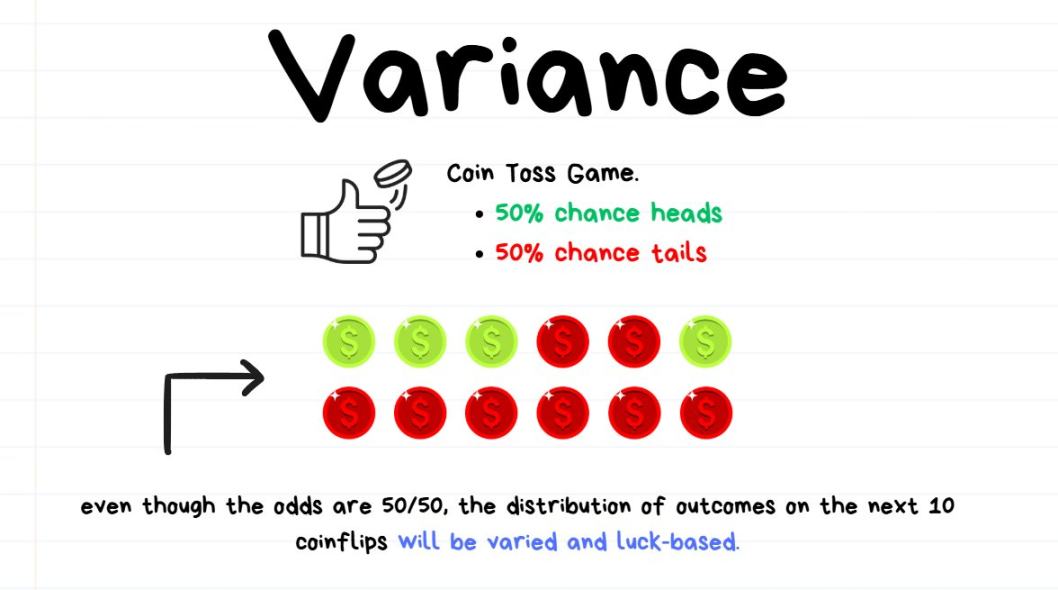

Next, a quick understanding of variance

Whether you like it or not, randomness affects trading performance.

Using a coin toss analogy: suppose you play a coin toss game, where the probability of heads and tails is each 50%.

If you toss the coin 10 times, you might get 8 heads and 2 tails; although the probability of heads should be 50%, the actual occurrence rate is 80%.

This does not mean the coin is rigged, and the probability of heads is 80%; it is simply because the number of tosses is insufficient, and the probability has not fully revealed its true distribution.

The difference between the actual result (80%) and the theoretical probability (50%) is the variance (80% - 50% = 30%).

If you toss the coin 10,000 times, the result might be 5050 heads and 4950 tails; although the number of heads is 50 more than expected, the variance in percentage is only 0.5% (50 ÷ 10000).

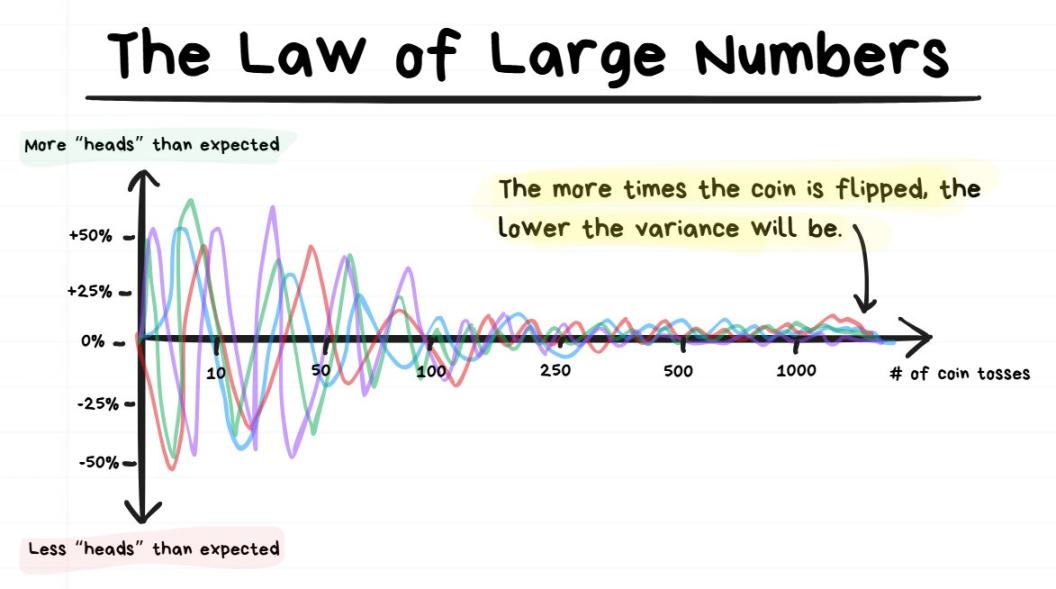

Finally, a quick understanding of the Law of Large Numbers

The more times you toss the coin, the closer the variance gets to 0.

Tip: The Law of Large Numbers states that the more times a random event is repeated, the closer the result gets to its true average value.

If you only toss the coin 10 times, the variance in the probability of heads may be large; if you toss it more than 10,000 times, the variance in the probability of heads will be very small.

In simple terms, the more times an event occurs, the closer the result gets to the true probability.

How do Monte Carlo simulation, variance, and the Law of Large Numbers relate to trading?

Monte Carlo simulation helps us manage expectations based on variance and assess the potential performance of future N trades; the more trades made, the smaller the expected variance.

It can also answer these key questions:

What should the expected profit be after making N trades?

What is the maximum number of consecutive wins that may occur?

What is the maximum number of consecutive losses that may occur?

With the current win rate and risk-reward ratio, what percentage of account loss after making N trades is considered normal?

At the same time, it also brings reminders to face reality:

Even a high-profit strategy may experience long-term drawdowns (drawdown refers to the percentage of account loss);

Even a high-win-rate strategy may experience significant consecutive losses;

Even a low-win-rate strategy may experience significant consecutive profits;

The result of the next trade is not important; what matters is the overall result of the future 100+ trades.

Core points of this section:

Sometimes you make a good trade but still incur a loss;

Sometimes you make a bad trade but unexpectedly profit.

The occurrence of these situations stems from variance (or luck). Judging whether a trade is correct based solely on a single trade result is not advisable.

Two extreme examples:

You place an order based on a trading strategy with a win rate of 90% and a risk-reward ratio of 1:1; even if this trade incurs a loss, it is still the correct decision. Because if you repeat the same trade 1000+ times and let the Law of Large Numbers take effect, you will ultimately profit.

You play a slot machine at a casino; even if you win once, it does not mean this is a wise bet; it is just luck brought by variance. If you continue to bet 1000+ times and let the Law of Large Numbers take effect, you will ultimately lose all your funds.

Key conclusion:

Do not judge the quality of a trade based on the profit or loss of the next trade; instead, base it on the expected value of the trade. You need to be patient and endure some variance for profits to gradually appear.

Leverage and Liquidation

Leverage may be one of the most misunderstood concepts by traders.

Before reading the following, please remember that you do not need to remember all the details; there is no pressure. Just grasping the basic concept of leverage is enough to handle trading.

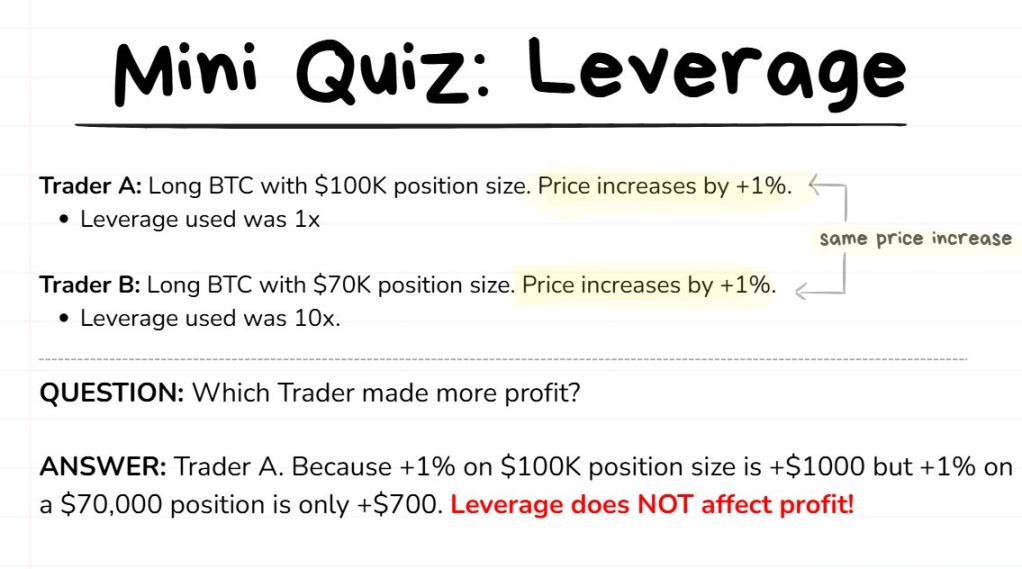

Let's do a little test to see if you understand the basics of leverage (assuming two traders have the same entry price).

Most people have a misunderstanding of leverage (absolutely incorrect): leverage is a profit multiplier; increasing leverage will magically increase trading profits.

I can say with certainty that leverage is not like that.

The true role of leverage (correct): Leverage is a tool to reduce counterparty risk and improve capital efficiency.

Counterparty risk: Refers to the risk your funds face while held on an exchange; there is a possibility of the exchange running away or committing fraud (e.g., the FTX incident), so funds are not absolutely safe.

Capital efficiency: Refers to the efficiency of using funds to earn more profit. For example: earning $1000 per month with a $1000 principal is 100 times more efficient than earning $1000 per month with a $100,000 principal.

Before delving deeper, let's clarify the definitions of several terms and then return to the study of leverage.

Trading account balance: The total funds you are willing to use for trading;

Exchange account balance: The funds you deposit on the exchange, usually only a small part of the trading account balance; it is not recommended to deposit all trading funds on the exchange;

Margin: The deposit required to open a trade;

Leverage: The multiple of funds you borrow from the exchange;

Position size: The total amount of tokens you actually buy/sell in a trade (or its dollar value).

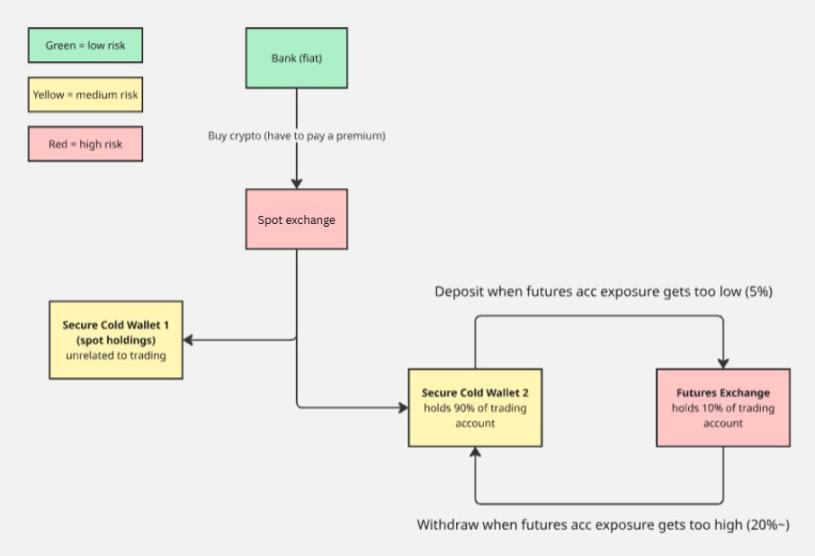

Supplementary note: The following diagram is a flowchart of how I manage deposits and withdrawals on exchanges, with the core principle being "do not concentrate all funds in a single exchange to avoid excessive exposure to risk."

Understanding the above concepts through an example

Suppose you have $10,000 available for trading; this is your trading account balance.

You do not want to deposit all $10,000 into the exchange (worried about the exchange freezing funds, fraud, or being hacked), so you only deposit 10%, which is $1000; at this point, your exchange account balance is $1000.

You find a good trading opportunity in Bitcoin and want to go long on $10,000 worth of BTC. When you click buy, the system will prompt that you have insufficient funds because your exchange account balance is only $1000, and you need to borrow the required funds through leverage to open the position.

After adjusting the leverage to 10 times, you can successfully open the position by clicking buy again:

The position size of this trade (the actual value of BTC bought) is $10,000;

The margin (the deposit you paid) is $1000;

The leverage multiple is 10 times.

Tip: Whether using 1x or 100x leverage, the profit of a $10,000 position will always be the same; the essence of a $10,000 position does not change with leverage. Even if you adjust the leverage during the trade, it will not affect the final profit.

Purpose of Liquidation

When you open a position using leverage, you are essentially borrowing money from the exchange, and this money does not come from thin air.

If you open a $10,000 position with 10x leverage and your exchange account balance is only $1000, then $9000 of that is borrowed from the exchange, and this borrowed money can only be used to open the position.

To ensure that the exchange can recover the borrowed funds, there is a liquidation mechanism.

Liquidation: If the price reaches a specific point (liquidation price), the exchange will forcibly close your position and confiscate the margin you paid. After that, the position will be taken over by the exchange, and any subsequent profits or losses will no longer concern you.

Simplified Understanding Through Analogy

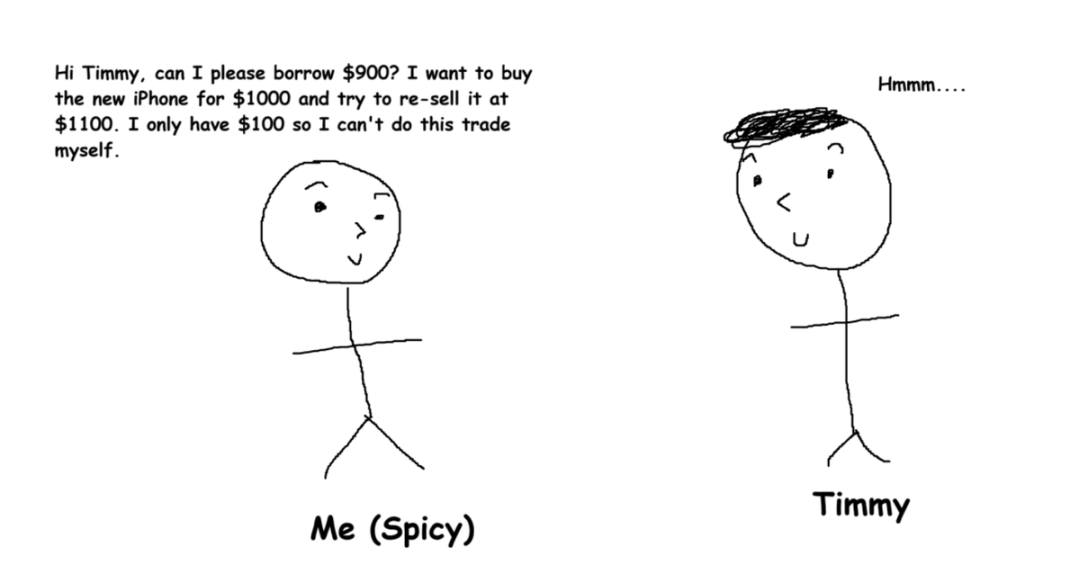

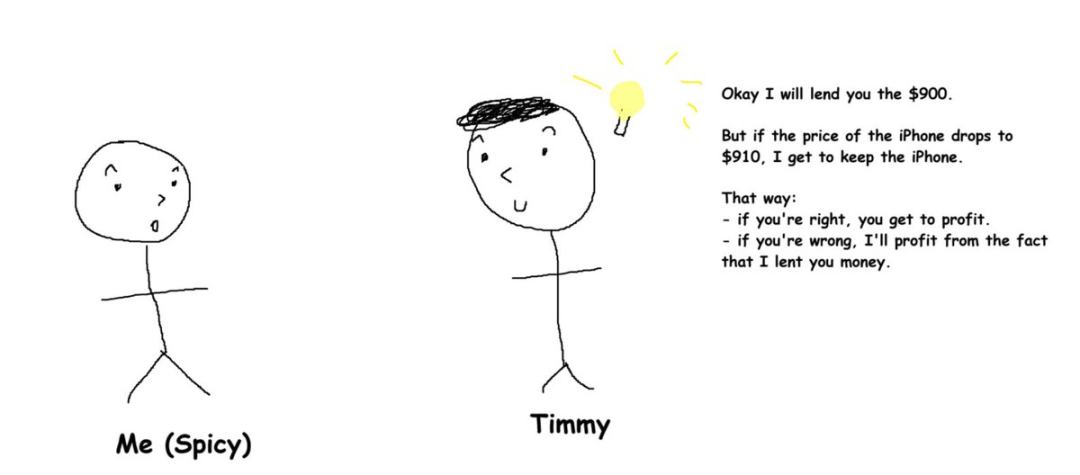

Suppose you are optimistic about a new iPhone, currently priced at $1000, and you expect it to rise to $1100 (a 10% increase). You plan to buy at $1000 and sell at $1100, making a profit of $100.

But the problem is, you only have $100 in your bank account.

So you approach the wealthy Timmy and borrow $900 from him to make this iPhone trade.

Potential Risk

If Timmy lends you $900 and the iPhone price drops below $900, even if you sell the iPhone, you won't be able to repay Timmy in full, resulting in an unwarranted loss for him, which he is unwilling to bear.

Solution

Both parties sign a mutually beneficial agreement (the essence of a perpetual contract is an agreement between the trader and the exchange):

You and Timmy agree that if the iPhone price falls below $910, you must hand over the purchased iPhone to Timmy, which is equivalent to your position being liquidated.

At this point, you will lose the initial $100 you paid (the margin); Timmy will then attempt to sell the iPhone himself; if the price does not fluctuate much and he can sell it for more than $900, he will make a profit.

Timmy requires "taking over the iPhone if the price falls below $910 rather than $900" because he should receive a reasonable return for "lending you money," allowing him enough room to "sell the iPhone and recover his principal."

Core Points of This Section

There is no need to remember all the definitions of terms; the most critical understanding is that leverage is merely a tool to help you achieve the desired position size.

Additionally, never put yourself at risk of liquidation; the costs and fees associated with liquidation are extremely high.

Tip: Every trade must have a stop-loss set. Trades without stop-losses are highly risky.

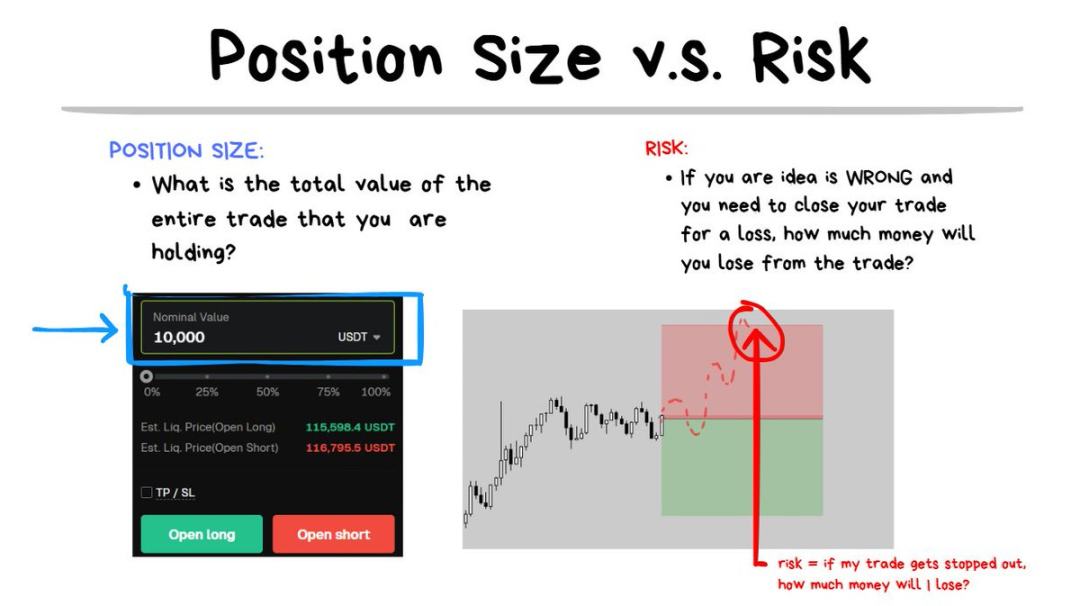

Difference Between Position Size and Risk

Another concept often misunderstood by traders is the difference between position size and risk.

Position size refers to the total amount of tokens (or dollar value) involved in the trade. For example: I bought $10,000 worth of BTC, so the position size is $10,000.

Risk refers to the amount of money you will lose if your trading judgment is incorrect and you need to stop-loss. For example: if the price hits the stop-loss level, I will lose $100, so the risk is $100.

Before making any trade, I first ask myself: "If my judgment is wrong and I must stop-loss, how much loss can I accept?"

This is a crucial question, but many traders completely overlook it. They firmly believe that their trading ideas are absolutely correct and cannot go wrong, and combined with the influence of FOMO, they often end up in trouble.

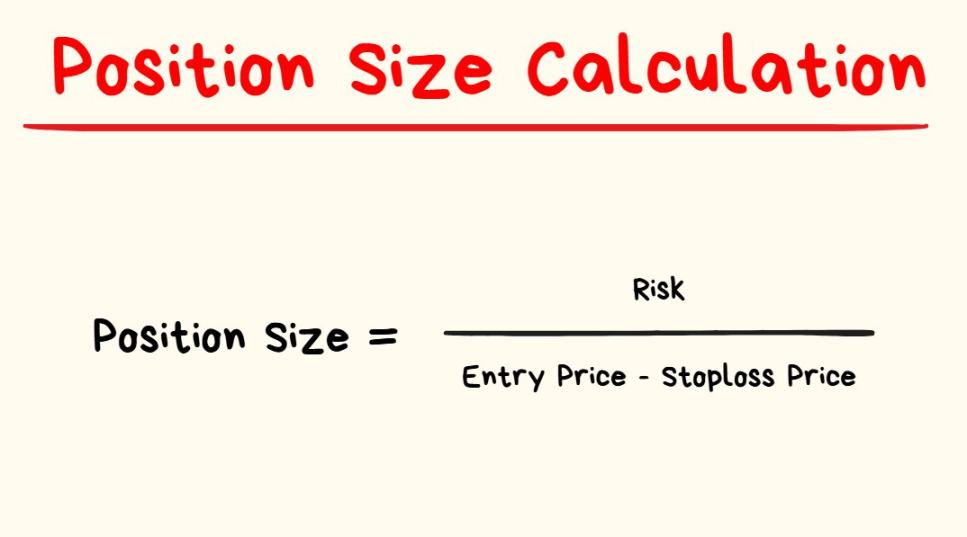

Once you determine the acceptable loss amount for the next trade, the next step is to calculate the required position size.

You don't need to worry about doing math calculations before every trade; there are simpler methods.

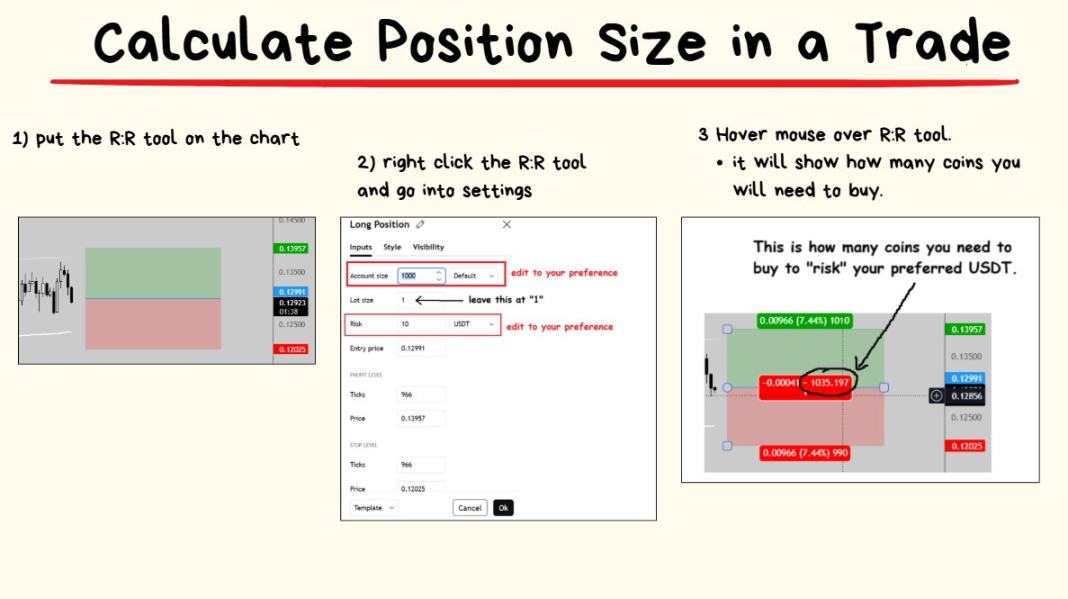

TradingView's risk-reward tool has built-in calculation functions:

The operation is straightforward; let's move on to the last knowledge point 🤓

Bankruptcy Risk and Reasonable Bet Size

All traders eventually ask a common question: how much risk is appropriate for each trade?

Answer: It depends.

Common answer: A widely circulated suggestion is to risk no more than 1% of the trading capital on each trade. For example, if you have $10,000 in capital, the expected loss amount for the next trade would be $100.

My personal answer: The higher the quality of the trade, the more you bet; the lower the quality of the trade, the less you bet.

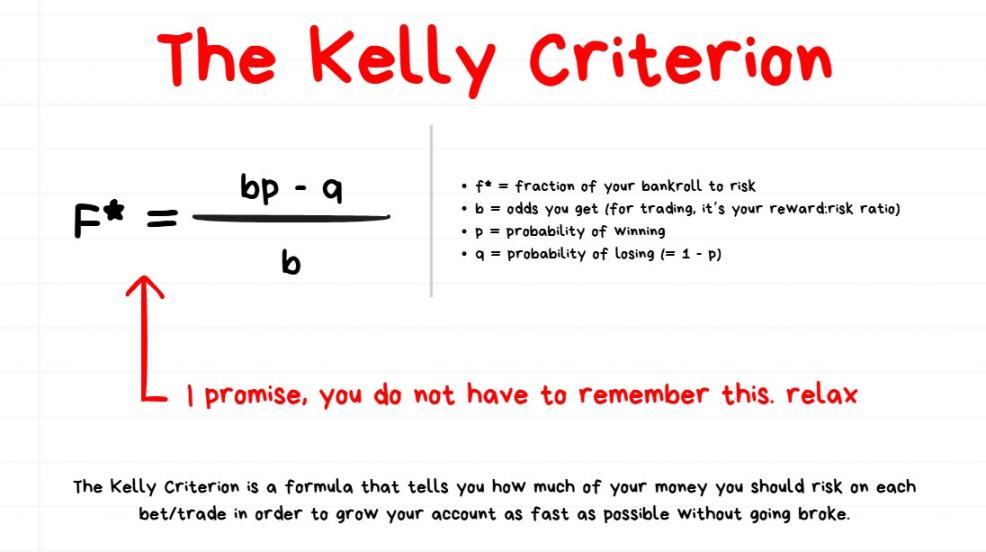

This section will discuss bankruptcy risk and the Kelly Criterion.

First, Understand Bankruptcy Risk

Even if you have a trading advantage (a profitable strategy with a positive expected value), it does not mean you won't face liquidation.

Tip: The first rule of trading is to never face liquidation. Once you are liquidated, you can no longer participate in trading; the core of trading is to stay in the market for the long term.

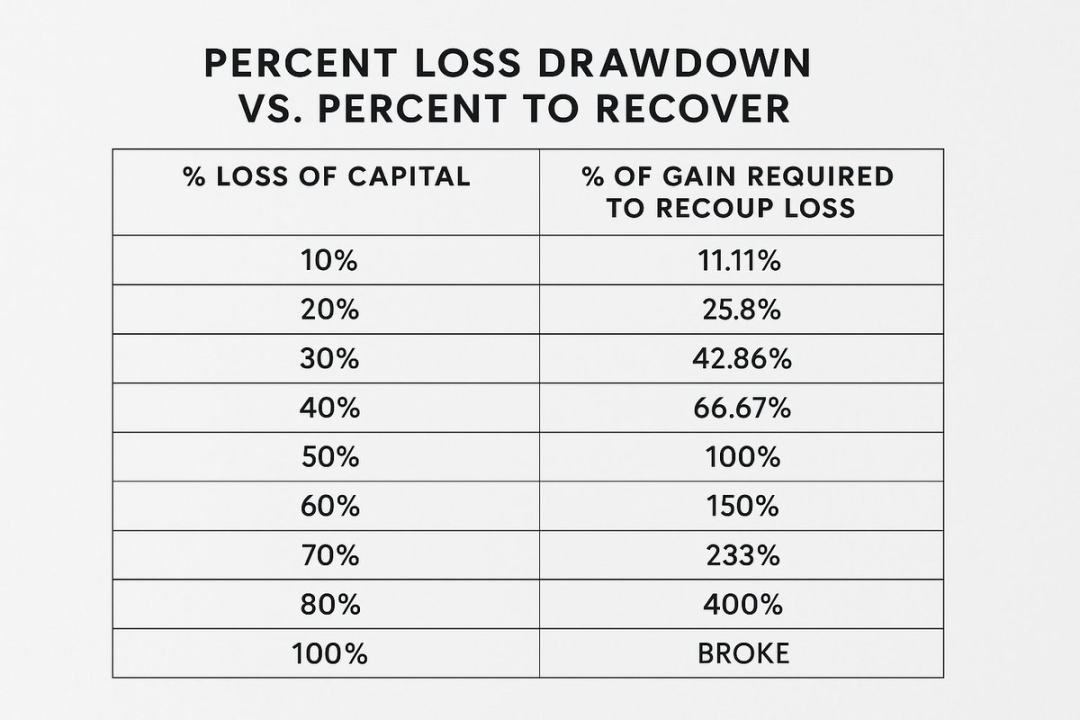

In fact, if you take on too much risk in each trade, even if the strategy is profitable, you will ultimately lose everything.

Extreme example:

Suppose you invest 100% of your capital in each trade, and your strategy has a win rate of 90% and a risk-reward ratio of 10:1; this is an extremely excellent strategy, but the problem is that trading with full margin will inevitably lead to liquidation.

Once liquidation occurs, the game is over; even if you are just on the verge of liquidation, recovery will be exceptionally difficult.

This is why it feels difficult to grow your account while liquidation happens easily.

Clearly, there is a definite upper limit to excessive risk; even with an excellent strategy, if you bet too much, you will eventually face liquidation.

Conversely, if the risk is too low (for example, risking only 0.0000001% of your capital on each trade), the account will never achieve effective growth.

So, where is the balance point for reasonable risk?

Next, Understand the Kelly Criterion, which attempts to address the "balance point" issue

There is no need to remember the specific formula of the Kelly Criterion; I list it only to satisfy curious readers.

Some traders believe that the Kelly Criterion is the best method for calculating optimal bet size; others think it is too conservative and grows slowly, choosing to multiply the Kelly result (for example: bet size = Kelly result × 2); while some traders believe it is still too aggressive and does not account for unexpected errors, opting to divide the Kelly result (for example: bet size = Kelly result ÷ 2).

My Core View on the Kelly Criterion and Optimal Bet Formula

I believe there is no perfect method for calculating bet size.

Even if you use the Kelly Criterion or other complex formulas to calculate bet size, there are no absolutely perfect solutions in the trading field.

As I mentioned earlier, I prefer to dynamically adjust bet sizes:

Low-quality trades: simply abandon and do not participate;

Standard-quality trades: risk 1% of capital;

High-quality trades: risk 2% of capital;

Super high-quality trades: risk up to 4% of capital.

Supplementary note: Is this the optimal betting method? I'm not sure! But I like simple methods, and this approach works well for me.

I assess the quality of a trade based on the strategy used to execute the trade and the variables presented in the market before opening a position.

Summary

Understanding the numbers behind trading advantages is crucial. In trading, which is a probability-based activity, expected value is the core concept;

Focus on the overall results of the next 100 trades rather than the profit or loss of the next trade, allowing the Law of Large Numbers to take effect;

Leverage is not a profit multiplier; it is merely a tool to improve capital efficiency. Remember, never put yourself at risk of liquidation;

Position size is the value of the tokens you buy/sell, while risk is the amount of money you will lose if your judgment is incorrect;

Account drawdowns are easy to fall into and difficult to recover from, so it is essential to control bet sizes reasonably. If you are a beginner, it is advisable to simplify operations: keep the risk of each trade within 1%, and adjust after becoming familiar with high-quality A+ trading patterns.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。