🤔Increasing $6,800 to $1.5 million in two weeks.

Written by: The Smart Ape

Translated by: Saoirse, Foresight News

This is a perfect case to illustrate the importance of "learning to program" — with programming, you can increase $6,800 to $1.5 million in just two weeks on the cryptocurrency exchange Hyperliquid.

Not long ago, a Hyperliquid trader achieved this.

Even more astonishing is that the trader took almost no risks. He neither bet on market direction nor followed the hype of popular assets, relying solely on a sophisticated market-making strategy — the core logic revolves around "market maker rebates," combined with automated operations and strict risk management.

Market Making Mechanism on Hyperliquid

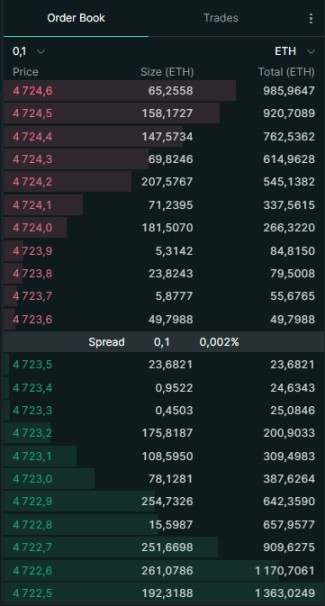

Before delving into the strategy, we need to understand the market-making logic of the Hyperliquid platform. Hyperliquid is an order book model exchange where users can place two types of orders:

Buy Orders: "Buy orders" (for example, "I want to buy SOL tokens at $100")

Sell Orders: "Sell orders" (for example, "I want to sell SOL tokens at $101")

These pending orders together form the "order book." Traders who place buy or sell orders are referred to as "makers."

The core role of makers is to "provide liquidity": by placing limit orders in advance, they supplement the market with tradable order volume.

In contrast, there are "takers": these traders directly execute existing orders in the order book (for example, "market buy" a token at the current best selling price).

Market makers are crucial to the market: it is because of them providing liquidity that the market bid-ask spread can be maintained at a low level; without market makers, traders may face issues like "unreasonable pricing" and "significant slippage."

Key Point: Market Maker Rebates

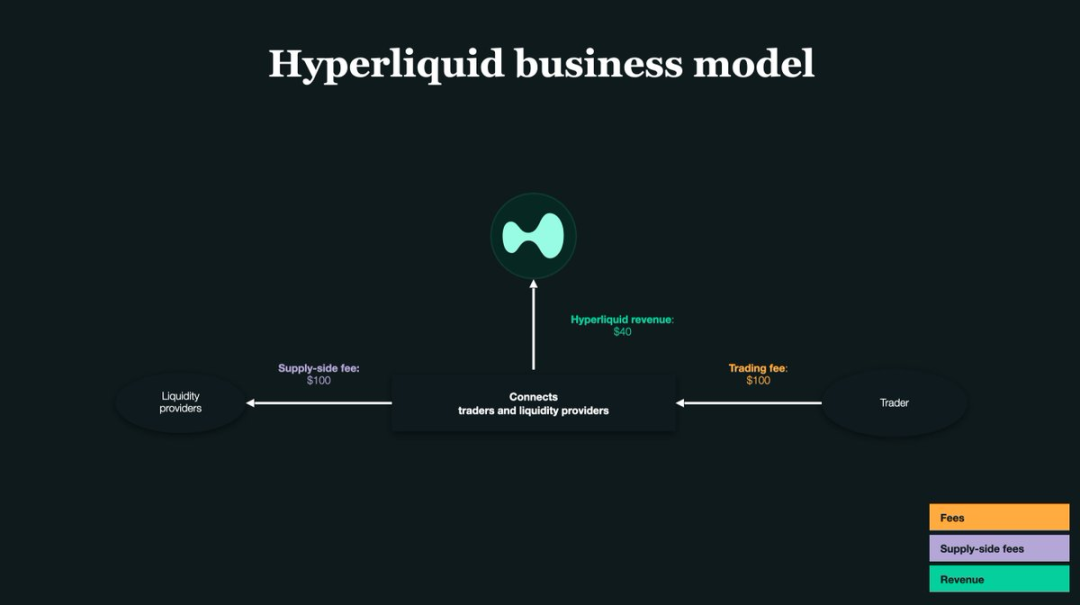

The core of the exchange is "liquidity" — to encourage users to become market makers and supplement market liquidity, Hyperliquid offers "transaction rebates": every time a maker's order is executed, the platform returns a small rebate.

On the Hyperliquid platform, the rebate rate for each transaction is approximately 0.0030% — meaning that for every $1,000 traded, a rebate of $0.03 is earned.

It is this seemingly meager rebate that allowed the trader to achieve the leap from "6,800 dollars to 1.5 million dollars." The core of his strategy is "one-sided quoting": placing limit orders only on one side of the order book (either only buy orders or only sell orders); once the market price changes, he quickly cancels the original order or switches to quoting on the other side.

In simple terms, his operational logic is: provide liquidity only on one side to earn rebates while using a bot to adjust order direction in real-time, avoiding risks from holding positions. Ultimately, relying on the massive trading volume brought by "automated high-frequency trading," the small rebates accumulate into substantial profits.

Core Pain Points of Traditional Market Makers

Most market makers place orders on both the "buy side" and "sell side" of the order book simultaneously.

For example: you place two orders — a buy order to buy 1 SOL at $100 and a sell order to sell 1 SOL at $101.

If both orders are executed, you earn a profit of $1 from "buying low and selling high."

However, this model has a critical issue: position risk.

If the buy order is executed and the sell order is not: you will passively hold SOL tokens;

If the sell order is executed and the buy order is not: you will passively hold stablecoins (like USDT).

Once the market price fluctuates unfavorably, these passively held assets may face significant losses.

This is also why the Hyperliquid trader chose "one-sided quoting": by placing orders on one side, he can more strictly control his positions and avoid passively holding unnecessary assets. However, this model comes with the cost of a higher "arbitrage risk."

What Does "Being Arbitraged" Mean?

For a specific scenario: you place a buy order on the order book to "buy SOL at $100." At this moment, unexpected bad news causes the price of SOL to drop to $90.

Your "buy at $100" order remains on the order book and has not been canceled;

Faster traders will immediately sell you SOL at "$100" (i.e., your buy order is executed);

The final result: you end up paying 10% more to buy SOL, and even if you receive platform rebates, you will still incur significant losses.

This situation is referred to as "adverse selection," commonly known as "being arbitraged."

Therefore, when adopting the "one-sided quoting" strategy, "accuracy" and "speed" are key to success — the effectiveness of the entire strategy entirely depends on the bot's response efficiency and operational accuracy.

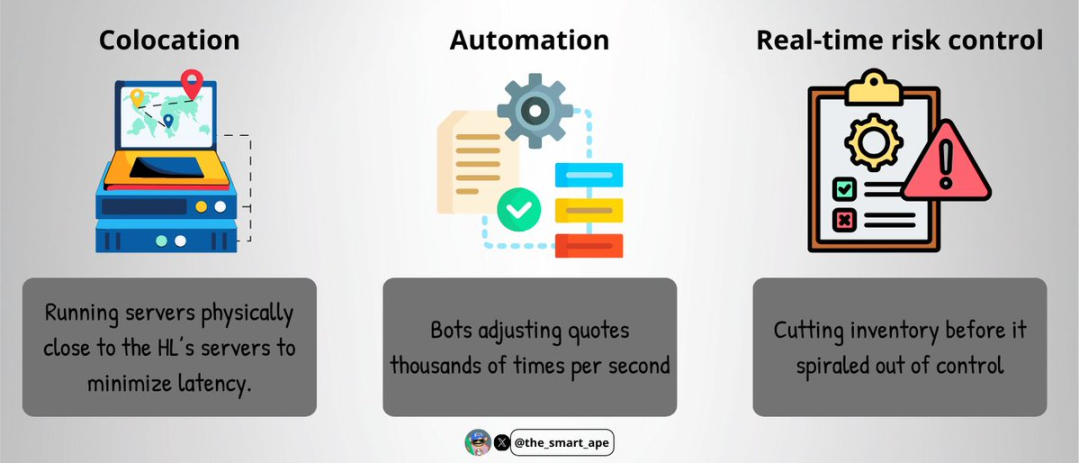

High-Frequency Trading Infrastructure

To avoid "being arbitraged," the trader built a "high-speed execution system," which includes:

Custodial services: physically deploying trading servers close to Hyperliquid's platform servers to minimize network latency;

Automated operations: the bot can adjust thousands of quotes per second, achieving "real-time price tracking";

Real-time risk control: automatically closing positions or adjusting positions before holding risks spiral out of control.

Building such infrastructure requires high costs and is technically complex — which is why only a few professional market makers can deploy such systems.

From a technical perspective, his trading bot is likely written in C++ or Rust (both known for "fast execution" and "low latency"); the servers are hosted close to Hyperliquid's "order matching engine" to ensure his orders are prioritized for matching.

The bot obtains real-time order book data through WebSocket or gRPC protocols, completing the "order placement - cancellation - switching quote direction" operations within milliseconds — ensuring continuous rebate earnings while avoiding order "expiration" due to price changes.

How to Maintain "Delta Neutral"?

Most impressively, the trader always maintained a "Delta neutral" state: despite his total trading volume reaching billions of dollars, his net position risk was always controlled within $100,000.

How did he achieve this?

The bot tracks the changes in SOL token holdings in real-time;

Sets strict risk limits (net position risk never exceeds $100,000);

Once the position risk approaches the limit, the bot immediately stops trading on the current side and switches to quoting on the opposite side, achieving position rebalancing through reverse trading.

He did not adopt an "arbitrage between spot and futures" model but operated entirely in the "perpetual contract" market — since all trades are completed in the same market, position hedging and risk control are simpler.

However, this strategy requires extremely high "discipline" and "accuracy": even the smallest operational error can lead to significant losses.

The Mathematical Logic Behind It

The profit calculation logic of the entire strategy is actually quite clear:

Within two weeks, the trader's total trading volume reached $1.4 billion;

The market maker rebate rate is 0.003% per transaction;

Profit obtained solely from rebates = $1.4 billion × 0.003% ≈ $420,000.

On this basis, he also adopted a "profit reinvestment" strategy — immediately reinvesting each rebate into trading, amplifying profits through the "compound effect." Ultimately, the total profit reached $1.5 million.

And all of this started with just $6,800 in initial trading capital.

Why Can't You Directly Copy This Strategy?

You might think: "If that's the case, can't I just copy his trades to earn the same amount of money?" But the reality is that this strategy is almost impossible to replicate, primarily due to:

You don't have his "execution speed": the combination of professional hosting servers + low-latency code is something ordinary traders find hard to achieve;

You don't have his "capital scale": although the initial capital was only $6,800, the trading scale later reached a professional level due to profit compounding;

You don't have "precise code and bots": his bot has been repeatedly debugged to adapt to every tiny fluctuation in the order book, which ordinary developers find hard to replicate;

You don't have "24/7 uninterrupted infrastructure and monitoring": the cryptocurrency market trades 24/7, requiring real-time monitoring systems to respond to sudden risks.

In short, this is a "professional-level high-frequency trading system," not something ordinary retail investors can easily replicate.

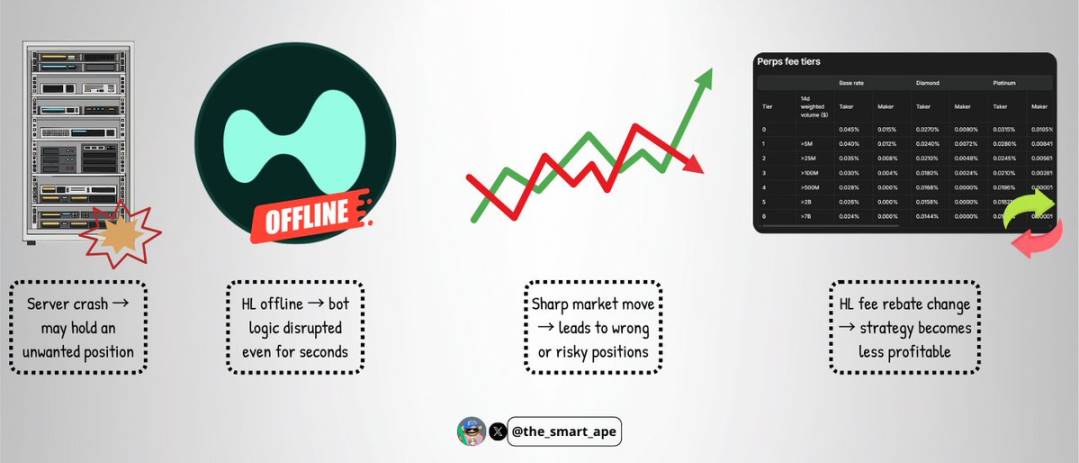

Potential Risks of the Strategy

Even for such a highly sophisticated bot, there are still significant risks to consider:

Server failures: If the server crashes, it may cause the bot to be unable to cancel orders in time, resulting in passive holding of a large risk position;

Exchange failures: Although rare, if the Hyperliquid platform experiences downtime or malfunctions, it may disrupt the bot's trading logic within seconds;

Extreme market volatility: Severe market movements may break the balance of "one-sided quoting," leading to strategy failure and losses;

Changes in fee structure: If Hyperliquid adjusts the market maker rebate rate or trading fees, it could immediately significantly reduce the profitability of the strategy.

This strategy, while sophisticated, is not "flawless."

Conclusion

Increasing $6,800 to $1.5 million in two weeks may sound like "getting lucky with meme coins," but in reality, it is backed by solid technical capabilities, strict discipline, and precise system design.

This is an excellent case study that demonstrates how to "scale the use of market maker rebates," "maintain delta neutrality," and minimize "directional risk."

The core insight from this case is: trading is not just about "predicting prices." Sometimes, the most profitable strategy is to thoroughly understand market structure rules and build a system that creates value in "corners that others overlook."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。