Original Title: "Hyperliquid's Ultimate Ambition: Creating Its Own 'Ecological Dollar' USDH"

Original Source: BitpushNews

Editor's Note: Last Friday, Hyperliquid announced the launch of a "USD stablecoin that prioritizes Hyperliquid, aligns with Hyperliquid's philosophy, and is compliant," reserving the token code USDH for this purpose. Subsequently, several stablecoin issuers, including Paxos, Frax Finance, Ethena Labs, and Agora, quickly entered the competition for the issuance rights of the USDH stablecoin. This article interprets the details of Hyperliquid's issuance of USDH and its ecological significance. Below is the original content:

As competition among decentralized exchanges (DEX) reaches a fever pitch, Hyperliquid has become one of the most watched platforms this year, thanks to its astonishing growth rate and continuously expanding product landscape.

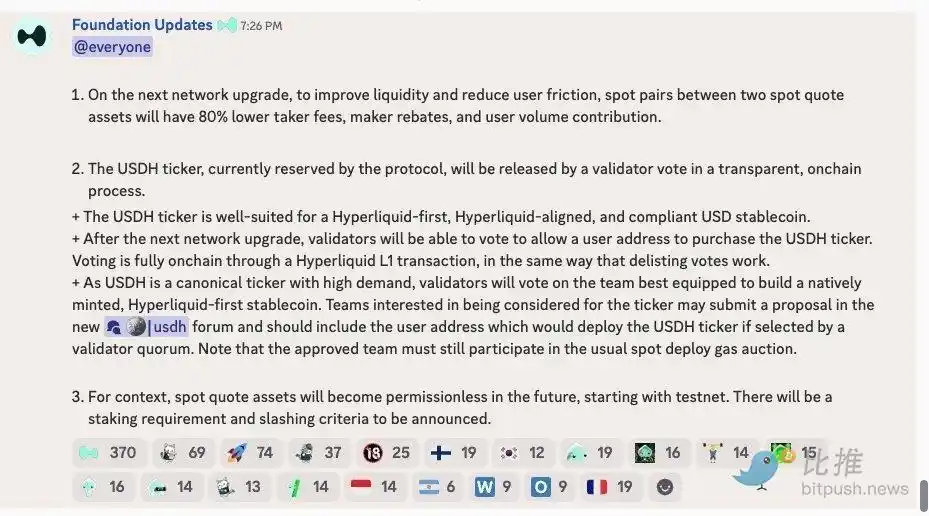

Yesterday, the foundation announced that it would launch its own USD stablecoin, USDH, through on-chain governance. This move not only signifies Hyperliquid's desire to gradually reduce its reliance on Circle's USDC but is also interpreted by outsiders as a key step in building a "self-sustaining" mechanism and perfecting its ecological closed loop.

Following the announcement, Hyperliquid's native token HYPE surged to $47.63. Although it slightly retreated afterward, according to CoinGecko data, its price still maintained a 4% increase over the past 24 hours.

From "Rookie" to "Dark Horse": The Strong Rise of Hyperliquid

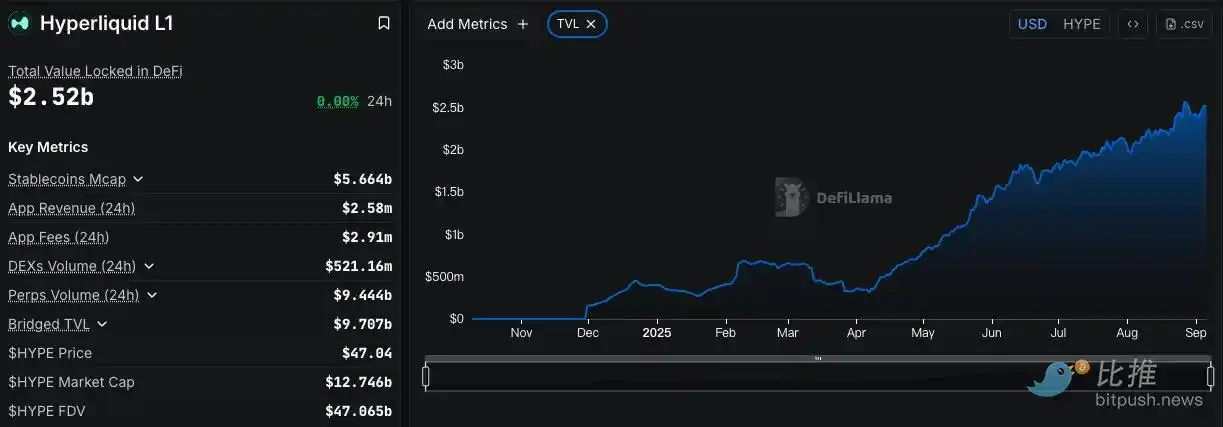

By 2025, Hyperliquid, with its exceptional trading activity, rapidly ascended from a second-tier platform to the top tier of DEX. According to DeFiLlama data, the platform's contract trading volume reached a staggering $398 billion in August, with spot trading volume also hitting $20 billion.

On August 25, its Bitcoin spot trading volume briefly surpassed that of centralized exchanges Coinbase and Bybit.

Its capital accumulation is equally impressive: at the beginning of this year, Hyperliquid's total value locked (TVL) was only $317 million, but by September, it had skyrocketed to $2.5 billion, achieving nearly eightfold growth. All of this indicates that Hyperliquid is rapidly gaining user favor, becoming an important hub for capital and trading liquidity.

In this context, the launch of its own stablecoin USDH by Hyperliquid is clearly a timely move.

For an exchange, mastering a stablecoin not only reduces external dependencies but also transforms the interest income generated from stablecoin reserves into a driving force for its own development, truly achieving "self-sustaining."

USDH's Issuance Mechanism: Decentralized Governance Dominates

Unlike mainstream stablecoins, the issuance of USDH is not directly decided by a single company but is determined through Hyperliquid's on-chain governance system.

First, Hyperliquid has reserved a code for USDH. Next, it will open up for teams to submit proposals explaining how to issue and operate the stablecoin. Subsequently, validators will decide which team wins in a five-day voting period.

Even if authorized, the team still needs to participate in Hyperliquid Layer1's "spot deployment gas auction" to complete the launch. This means that the issuer of USDH is not predetermined by the foundation but is generated through community competition.

The design of this mechanism reflects the spirit of decentralization and allows Hyperliquid to enhance community participation and cohesion through the governance process. At the same time, the foundation clearly states that USDH must be "compliant," laying a compliance foundation for its stable operation in the context of new regulations like the GENIUS Act.

Differences from USDT and USDC

The stablecoin market is currently dominated by USDT and USDC, which together account for over 80% of the market share. In contrast, USDH's positioning is more "ecologically native."

First, the issuing entities are different. USDT and USDC are issued by centralized companies like Tether and Circle, with reserve funds managed by the companies; USDH, on the other hand, is managed by a team elected through governance voting, aligning more with the positioning of "protocol-native assets."

Second, the use cases differ. USDT and USDC almost cover the entire crypto ecosystem and serve as universal settlement tools. USDH primarily serves internal trading within Hyperliquid, becoming a dedicated stable asset for derivatives, clearing, and liquidity pools.

More importantly, the revenue models differ. The reserve interest of USDT and USDC is exclusively enjoyed by the issuing companies, while once USDH is operational, its reserve income may be redistributed through governance, flowing back to validators or the community. This makes Hyperliquid's stablecoin not just a payment tool but also a "blood circulation system" driving ecological growth.

In terms of transparency and compliance, USDT has long faced scrutiny, while USDC has gained some trust due to Circle's background. Hyperliquid explicitly emphasizes the compliance attributes of USDH and combines its operation with on-chain governance, theoretically increasing transparency.

Community Controversy

It is worth noting that the announcement of USDH's plan has sparked intense debate within the community.

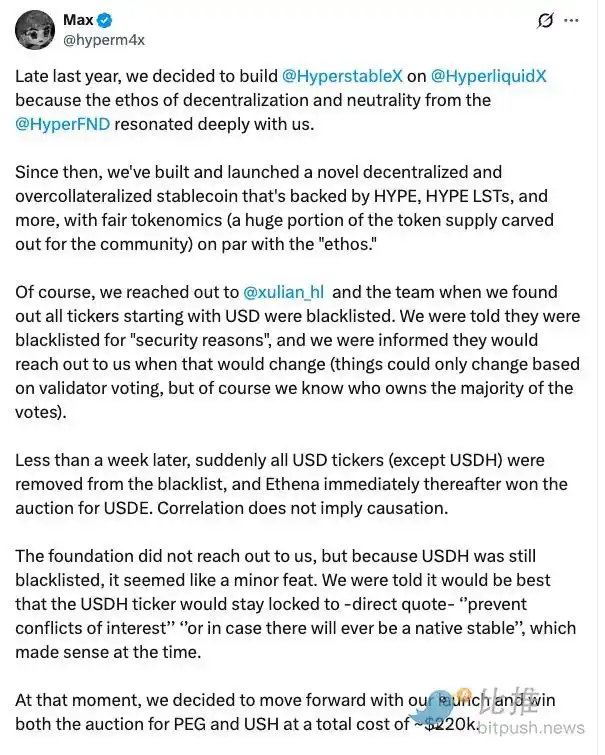

Max, a developer from the established stablecoin protocol Hyperstable, was the first to speak out. He pointed out that the USDH code had previously been blacklisted, forcing them to use "USH" as the stablecoin symbol. Now, with the foundation suddenly unblocking USDH, Hyperstable feels that the rules have been changed arbitrarily, which is "extremely unfair to teams that have already invested significant resources."

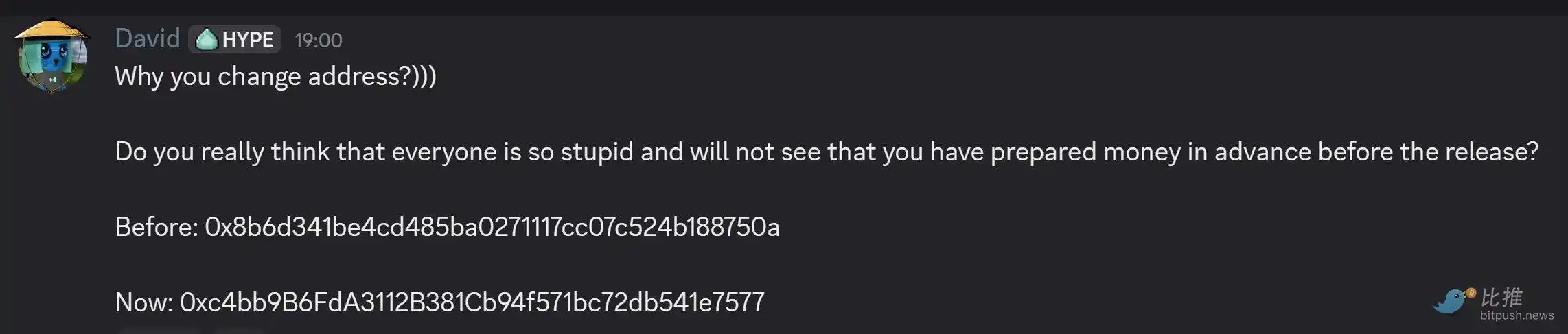

Meanwhile, another candidate team, Native Markets, has also sparked controversy with its proposal. Community members discovered that the team's wallet received funding from Hyperliquid only hours before the announcement, while their submitted plan was detailed and seemed well-prepared. This raised suspicions about whether they had prior knowledge of the news or if there was some undisclosed relationship with the foundation.

Supporters argue that unblocking USDH is not "backdoor manipulation" but a response to the changing compliance environment following the enactment of the GENIUS Act. Since the external environment has changed, the rules naturally need to be adjusted. Behind the debate lies skepticism about whether Hyperliquid can maintain governance neutrality and treat developers fairly.

A New Phase in the Stablecoin Race

The larger context is that the stablecoin market itself is entering a new round of expansion. According to DeFiLlama data, the total market value of stablecoins worldwide has exceeded $285 billion, growing over 5% in the past week. Among them, Tether's USDT holds a 58% share, followed closely by USDC.

At the same time, industry giants and emerging players are entering the fray: MetaMask is collaborating with infrastructure provider M0 to launch mmUSD; payment giant Stripe is also partnering with Bridge to issue an internal stablecoin. In this trend, Hyperliquid's USDH is not an isolated attempt but part of a larger wave, as exchanges, public chains, wallets, and payment companies all seek to control their own currency systems to reduce external dependencies and capture long-term benefits from reserve assets.

If USDH can be successfully launched, it will be an important step for Hyperliquid to achieve "self-sustaining" and signifies that it is no longer content with merely being a trading platform but is making substantial strides toward building a complete financial ecosystem. Next, it will depend on how the community reaches a consensus and takes action; the story is just beginning.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。