Author: Zz, ChainCatcher

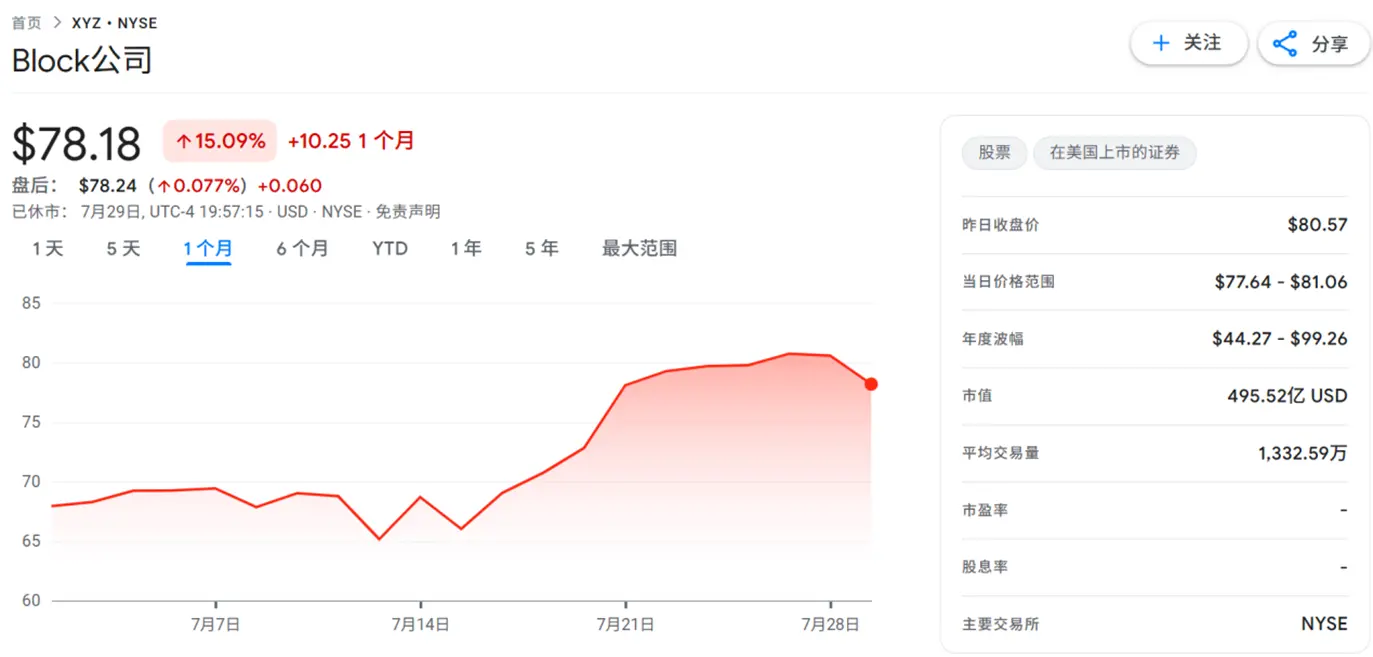

In July 2025, Block, led by Jack Dorsey, was officially included in the S&P 500 index. This fintech company, which owns the payment giant Square and the mobile financial app Cash App, has successfully positioned itself among the 500 most representative publicly traded companies in the United States. The stock price subsequently rose by 14% within a few days.

Being included in the S&P 500 means that Block will become a standard component of mainstream global investment portfolios. According to incomplete statistics, passive funds tracking the S&P 500 exceed $5 trillion in size. Based on Block's weight in the index, it is estimated that over $10 billion of traditional capital will be indirectly allocated to Bitcoin through holding Block shares.

A Trillion-Dollar Market is Being Leveraged by Block

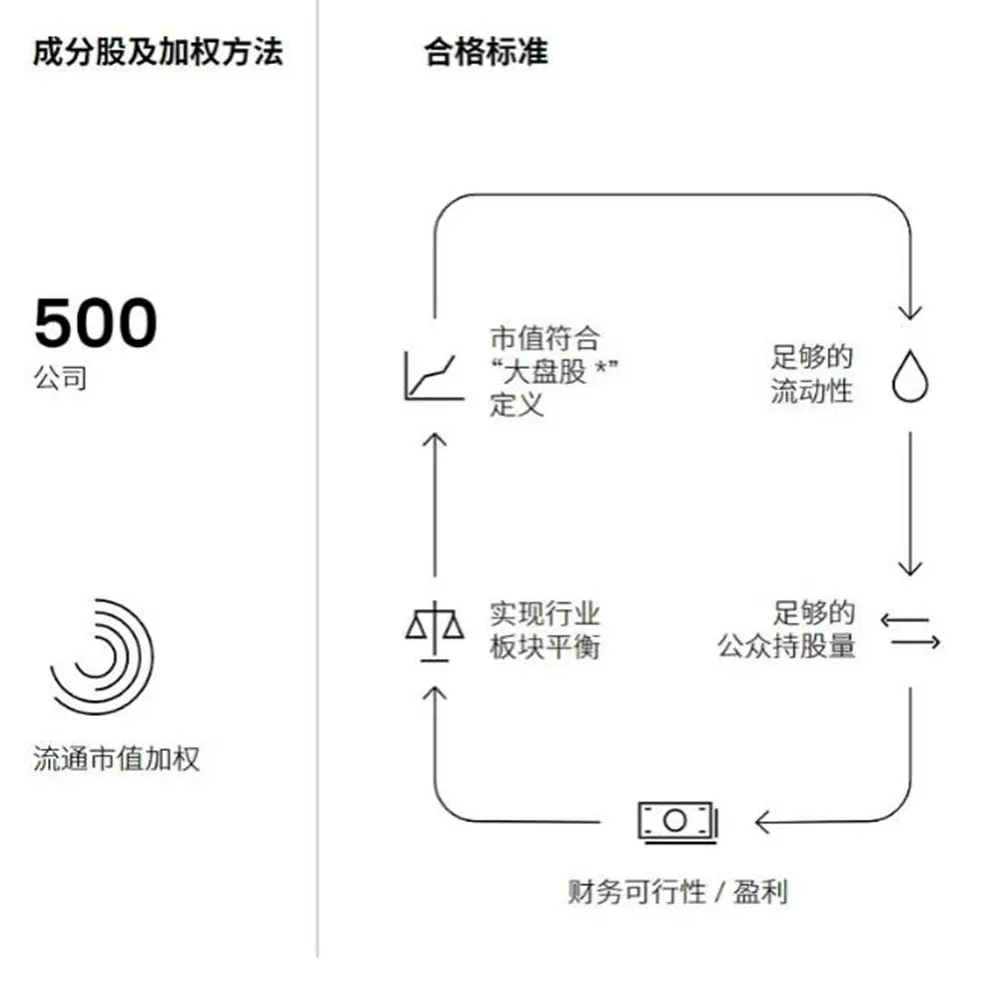

To understand the leverage that Block has leveraged, one must first understand the S&P 500 as a "protocol" for capital allocation, rather than just a simple list of stocks.

The rules of this "protocol" are extremely simple, even "clumsy": all index funds tracking it have the sole mission of precisely replicating the components and weights of the index. They have no room for subjective judgment, as any deviation means a failure to track.

Block obtained this "protocol" entry ticket precisely by passing the most stringent profitability review— the company must have achieved profitability in both the most recent quarter and the entire past year. This ticket represents the highest endorsement from the traditional financial system regarding the feasibility of a "Bitcoin-friendly" business strategy.

Thus, Block's inclusion is far more than just another tech newcomer joining the elite club.

Looking back at the history of the S&P 500, it is essentially a history of being forced to absorb emerging industries and acknowledge new business models. Based on its iconic inclusion events, a clear trajectory emerges:

In 2006, Google (Alphabet) knocked on the door, forcing funds to buy into a company whose core assets were intangible algorithms and user data.

The inclusion of Meta (formerly Facebook) in 2013 marked the formal digestion of the nebulous Web2 concept of "social graphs" by Wall Street's capital machine.

As for Tesla's inclusion in 2020, it showcased the mechanical power of this mechanism to the fullest. It is estimated that it triggered over $80 billion in passive buying.

However, when these companies were included, the funds were ultimately buying equity in a company, the value of which was closely tied to specific business models and operational performance.

In contrast, when they are now forced to buy into Block, they are not just acquiring equity in a payment company; they are also gaining direct risk exposure to the 8,363 Bitcoins on its balance sheet.

This change immediately triggered a mechanical and irreversible flow of capital. Given the core mission of S&P 500 index funds, with Block's market capitalization of about $50 billion and an estimated weight of about 0.1% in the index, this inclusion is expected to trigger over $10 billion in "passive buying" in the short term.

More cleverly, most of this capital comes from pension and sovereign wealth funds that previously would not actively touch crypto assets. This mechanical capital inflow bypasses the psychological barriers traditional investors have towards crypto assets.

If the inclusion of Google and Meta marked Wall Street's forced acceptance of new business models, and Tesla's inclusion demonstrated the enormous power of capital mobilization, then Block's inclusion signifies Wall Street's first forced embrace of decentralized, non-sovereign currency assets under rule-driven conditions.

Block's Bitcoin Affinity

To understand why Block is so firmly betting on Bitcoin, one must first understand the evolution of its founder Jack Dorsey's values. His career has not been about chasing trends but about solving the same core issue: breaking the restrictions that centralized institutions impose on individual rights.

The story begins dramatically. His co-founder Jim McKelvey is a glass artist who missed a $2,000 sale because he could not accept credit card payments. This experience deeply pained the two founders—why, in the 21st century, are small merchants still excluded from the modern payment system?

This pain point gave birth to Square (the predecessor of Block), a company that leveraged a small white card reader to disrupt the entire payment industry. When traditional banks set numerous barriers for small merchants, Square enabled anyone to accept credit card payments using a smartphone. This was Dorsey's first successful transfer of power from the center to the periphery, achieving what he called "payment democratization."

However, what truly made him obsessed with decentralization was his experience with Twitter. The platform he co-founded initially carried a utopian vision of information democratization—allowing everyone to speak freely and equally. But as the platform's influence grew, the pull of reality began to take effect. The business model required advertising revenue, the government pressured for content moderation, and the public demanded accountability from the platform. Twitter had to play the role Dorsey least wanted to assume: that of a content arbiter.

"It is too great and dangerous a power for a single company to decide who can speak and what content can be disseminated," Dorsey later reflected. He attempted to build Twitter on a decentralized protocol through the "BlueSky" project, but it was too late. This failure made him realize that true decentralization is not rooted in benevolent "company charters," but in cold "code protocols."

It was in this disillusionment that Bitcoin entered his vision. In this global financial protocol that requires no permission, is resistant to censorship, and does not belong to any single entity, he saw the ideal that Twitter failed to achieve.

Block's embrace of Bitcoin began at the product level. In 2018, its Cash App started supporting Bitcoin transactions, allowing millions of ordinary Americans to purchase Bitcoin as easily as buying stocks for the first time. This decision was quite controversial at the time—traditional finance circles viewed cryptocurrencies as speculative bubbles, but Dorsey saw it as an extension of financial inclusion.

The turning point came in October 2020. At that time, Bitcoin's price was hovering around $10,000, and Block suddenly announced it had used company funds to purchase 4,709 Bitcoins, investing $50 million. Wall Street analysts were puzzled, "Why would a payment company hold such a 'speculative' asset?"

Dorsey's thoughts were clear: "Bitcoin represents the native currency that the internet needs."

In February 2021, Block made another move, spending $170 million to acquire 3,318 Bitcoins. The total investment from the two purchases reached $220 million, holding 8,027 Bitcoins. The market began to realize that this was not a fleeting financial operation, but an expression of faith.

Subsequently, the Bitcoin strategy was further deepened in 2023. Block launched the "Bitcoin Blueprint" plan, announcing that 10% of the gross profit from its Bitcoin-related businesses would be used to purchase Bitcoin each month.

What does this mean? Bitcoin is no longer a static investment lying on the balance sheet, but a dynamic engine deeply tied to the company's business growth. Every Bitcoin transaction on Cash App contributes to an incremental increase in Block's Bitcoin reserves.

This programmatic, predictable accumulation strategy sends a clear signal to the market: Block's commitment to Bitcoin is algorithmic, not emotion-driven.

Moreover, Block's ambitions go far beyond mere holding. In recent years, the company has launched an infrastructure-building campaign around Bitcoin. Cash App integrated the Lightning Network, making small Bitcoin payments as simple as sending a text message; the TBD department focuses on developing decentralized protocols, attempting to build financial infrastructure that does not rely on any centralized entity; the open-source hardware wallet project allows ordinary users to truly control their Bitcoins; and even investments in mining chips aim to make the Bitcoin network more decentralized.

"We are not betting on Bitcoin going up; we are betting on Bitcoin becoming a part of the global financial system."

If this bet holds, companies building related infrastructure will gain a significant advantage.

This comprehensive investment ultimately paid off. When the S&P Dow Jones Index Committee evaluated Block, they did not see a simple company holding Bitcoin, but a "Bitcoin-native enterprise" that deeply integrates Bitcoin into its business model and is committed to promoting its adoption.

For Jack Dorsey, Block's inclusion in the S&P 500 is more like a means to achieve his ultimate vision—using Wall Street's money to build a future that ultimately does not belong to Wall Street.

From Square enabling small merchants to accept credit cards, to Twitter attempting to allow everyone to speak freely, to Block going all-in on Bitcoin, his journey has never changed: to decentralize power from the center to the periphery.

In the world of Bitcoin, he found the utopia he has always sought that cannot be hijacked by commercial interests.

However, achieving this utopia requires not only ideals but also tangible resources and execution capabilities.

Jack Dorsey's Ultimate Goal: Build Decentralized Roads with Wall Street's Money

Block's business structure clearly serves Jack Dorsey's vision.

The two traditional businesses are the blood engines of this machine. Square provides payment and financial services to millions of merchants, contributing continuous cash flow. Cash App is a high-growth financial application aimed at consumers, having launched Bitcoin trading as early as 2018, accumulating a large and loyal user base.

These profits and users are continuously funneled into Block's internal future departments:

On the software side, the Spiral and TBD departments focus on building the underlying infrastructure for Bitcoin. They develop the Lightning Development Kit (LDK), allowing developers to easily integrate Bitcoin micropayment features into any application; at the same time, they are building decentralized identity (DID) and tbDEX protocols, aiming to bypass centralized exchanges for seamless, peer-to-peer exchanges between fiat and Bitcoin.

On the hardware side, the Bitkey wallet aims to solve the problem of Bitcoin self-custody, achieving a balance between security and usability through technologies like "2 of 3 multisig." Additionally, the Proto department is developing an open-source Bitcoin mining system, aiming to challenge the monopoly of existing mining machine giants and maintain the decentralized nature of the Bitcoin network.

This is not a one-sided money-burning endeavor, as the Bitcoin business itself is a powerful engine for user and revenue growth. At the peak of the bull market, Bitcoin trading alone generated $10.02 billion in revenue for Cash App, accounting for an astonishing 81.5%, proving that the model of attracting users and generating revenue through Bitcoin business provides strong financial support for investing in these "future departments."

Thus, a perfect closed loop is formed: using profits from traditional financial businesses to invest in and build Bitcoin infrastructure; then leveraging Bitcoin's appeal to acquire new users, feeding back into the growth of traditional businesses.

Block Also Has Fatal Flaws

Behind Block's grand narrative lies hidden concerns.

First, its technological dependence is the primary risk. The deep binding to the Bitcoin protocol means that any black swan event at the protocol level could have devastating effects. Technologies like the Lightning Network, which the payment business relies on, are still in the early stages of development, and their stability remains to be tested over time.

Secondly, its execution risk is also not to be underestimated. Projects like TBD, Proto, and Bitkey have high technical barriers, and their commercialization prospects are still shrouded in uncertainty. Rating agency Morningstar maintains a "very high" uncertainty rating for Block, bluntly stating that being included in the index "has not changed the company's fundamentals."

At the same time, Block's financial performance has also raised concerns. According to the Economic Times, Block's revenue growth has slowed, and its operating profit margin is below the average level of the S&P 500. Analysts believe the company needs to translate its vision of "Bitcoin is the future" into tangible returns for shareholders.

In Conclusion

For the crypto world, Block represents a possibility: not through confrontation, but through construction and integration, pushing Bitcoin from the margins to the center. This "Trojan horse" style of infiltration may be more effective than any radical revolution.

However, when trillions of dollars in passive funds are "forced" to embrace Bitcoin, there is always a fundamental question that cannot be avoided: is this the beginning of Bitcoin conquering Wall Street, or the prelude to Wall Street taming Bitcoin?

Recommended Reading:

Solana and Base Founders Start a Debate: Does Content on Zora Have "Fundamental Value"?

Soaring 30 Times This Month, Is Graphite Protocol the "Tax Collector" Behind Bonk.fun?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。