7月,骄阳似火,盛夏的加密圈迎来美股代币化的热浪。

Robinhood 高调宣布,欧洲用户可通过 Arbitrum 链上交易美股且24小时不打烊;xStocks联手 Kraken 和 Solana,推出60种热门美股的链上代币,Coinbase 也向SEC申请推出代币化证券...

一时间,美股代币化成了沉闷的加密圈里为数不多的叙事正确,这股热潮已经占据了所有人的时间线。

但这并不是美股代币化的第一次。

死去的记忆开始重新攻击我,让我怀念五年前的那个夏天。

2020年8月,DeFi 之夏如烈焰般席卷加密圈,Uniswap 的流动性挖矿点燃狂热,Terra 的 Luna 链和 UST 扶摇直上,链上金融实际上已经做出了许多创新,这其中就包括美股的代币化。

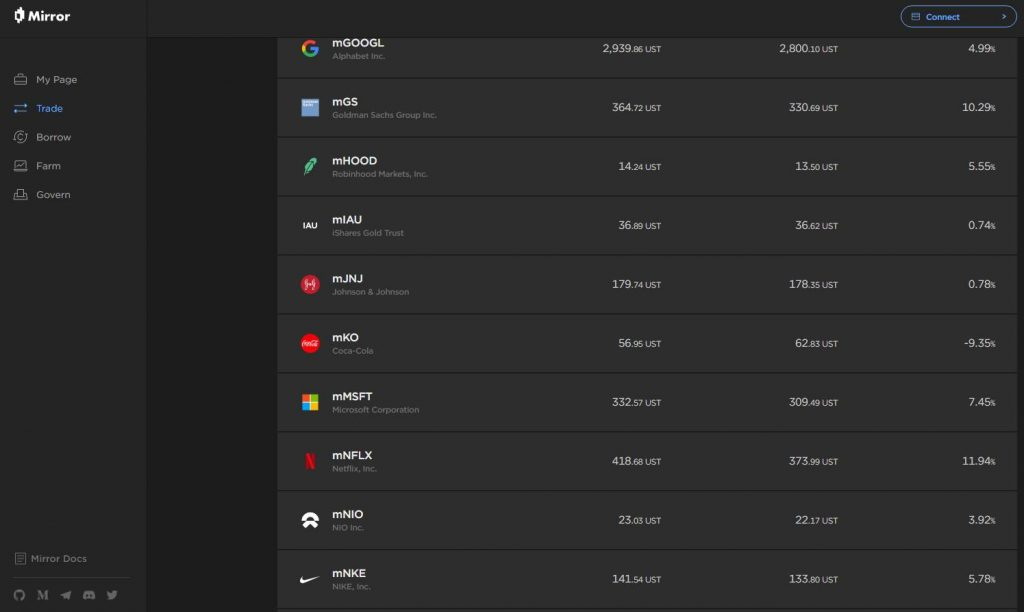

彼时 Luna 上有一个叫做 Mirror 的协议,我当时在 Terra Station 用几美元的UST铸造了mAAPL(Apple股票对应的代币),无需KYC,无需开户,第一次绕过券商触碰苹果股价的脉动。

但有句歌词,可以完美形容老韭菜在经历这一切之后的心情:

“你在我生命留下喧哗,离开后却安静的可怕。”

Luna 最终崩盘了,Mirror 也被 SEC 的诉讼碾碎,2020年的梦碎了一地。除了交易哈希,似乎没有什么能证明早在5年前的夏天,代币化的美股已经存在过。

而今,xStocks、Robinhood 卷土重来,链上美股再度点燃希望。这次会成功吗?与五年前相比,事情又有什么不同?

那年夏天,Mirror 的自由乌托邦

如果你已经不记得 Mirror Protocol,或者是当时根本没有进圈,让我帮你重拾一下久远的记忆。

Mirror Protocol 的核心思路是:利用链上合成资产,来追踪现实世界里美股的股价。这一玩法也就诞生了一类叫做 mAssets 的资产。

所谓的“合成资产”mAssets,,是通过智能合约和预言机模拟股票价格的代币,持币者不持有实际股票,只像“链上的影子”来追踪价格波动。

比如mAAPL(苹果)、mTSLA(特斯拉)、mSPY(标普500 ETF),它们靠 Band Protocol 的去中心化预言机获取实时美股数据。

虽然这和直接买美股存在区别,但胜在便利:

铸造 mAssets很简单,用当时 Terra链上的稳定币 UST 超额抵押150%-200%,在 Terra Station操作即可获取对应的代币化股票,无需KYC,交易费仅0.1美元左右。

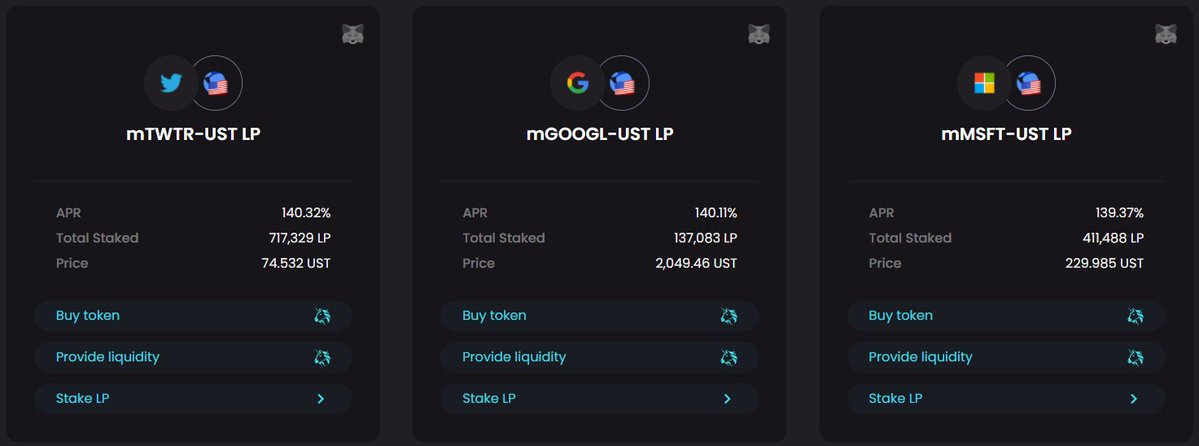

这些代币不仅能在 Terraswap (当时 Terra 的 DEX)上24/7交易,像 Uniswap 的代币对一样灵活;还能在自家生态里的另一个借贷协议 Anchor Protocol 中当抵押品,进行借贷或赚利息。

既能享受美股上市公司的成长收益,又能利用链上金融的灵活性,5年前的DeFi,似乎已经把美股代币化玩明白了。

但好景不长,那场夏天的梦碎得让人措手不及。

2022年5月,加密圈著名的黑天鹅事件降临。Terra 的算法稳定币 UST 脱钩,Luna 从80美元快速暴跌至几分钱,mAssets 一夜清零,Mirror 几乎停摆。

更雪上加霜的是,美国SEC出手,指控 mAssets为未注册证券,Terraform Labs及其创始人 Do Kwon 深陷诉讼泥潭。

从“坐稳扶好伙计们” 到“对不起我们失败了”,Terra 系的覆灭也让美股代币化在链上消失的无影无踪,在感慨和追忆的同时,反过来你也能看到它的致命弱点:

合成资产严重依赖预言机和UST的稳定,毫无实际股票支撑,底层的倒塌将使上层资产成为泡影。此外,匿名交易虽吸引用户,却也势必触碰监管红线;彼时的监管和政策,远不像今天这么开明与宽松。

合成资产的脆弱、稳定币的风险、监管的缺位,让这场实验付出了惨痛代价。

这次,有什么不一样?

当时不成功,不意味着现在不成功。

2020年的夏天过去了,这次 Kraken、Robinhood 和 Coinbase们,带着更成熟的技术和合规姿态,试图改写故事。

作为一个见证过DeFi之夏的老玩家,我忍不住对比:这次与五年前的 Mirror 相比,到底有什么不一样?

我们或许可以从产品、参与主体和市场环境三个部分来看。

-

产品:从链上影子到真实锚定

如前所述,像mAAPL、mTSLA这样的代币,只是智能合约模拟的“链上影子”,不持有实际股票,仅模拟价格波动。

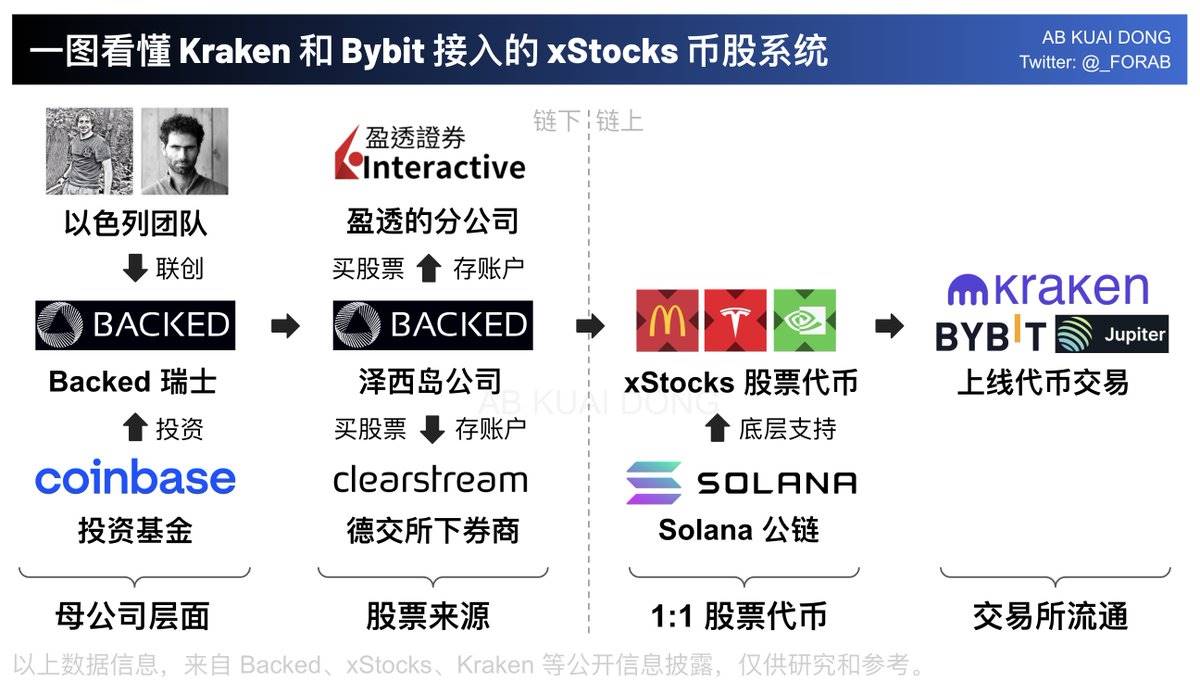

而现在的 xStocks 则走上另一条路。xStocks 由受监管的经纪商托管,确保购买股票后的可兑换现金价值。

这套美股代币化流程,背后操盘的是Backed Assets,一家注册于瑞士的代币发行商,负责购买和代币化资产。

它通过Interactive Brokers 的 IBKR Prime 渠道(一个连接美股市场的专业经纪服务)买入股票,如苹果或特斯拉,再将资产转移至Clearstream(德意志交易所的托管机构)进行隔离存储,确保每枚代币1:1对应实际持仓,并接受法律审计。

简言之,就是你的每一笔链上购买,背后都有真实股票的购买行为做锚定。

(图片来源:X用户 @_FORAB)

此外,xStocks 支持代币持有者通过 Backed Assets 反向赎回实际股票,这一功能让它跳脱Mirror的纯链上投机框架,连接链上与链下。

-

参与主体:从 DeFi 原生到 TradFi 融合

Mirror的舞台属于DeFi原生玩家。Terra社区的散户和开发者是主力,Discord和Twitter上的热议驱动了mAssets的流行。Mirror的成功,离不开Terra生态的Luna和UST热潮,社区的实验精神让它如彗星般闪耀。

这也不得不让人感慨,大人时代变了。

这波美股代币化,主导者主要是传统金融巨头与圈内合规企业。

比如 xStocks 由 Kraken 提供合规平台,Robinhood 将传统券商经验带入链上,贝莱德的代币化试点更标志着机构入场。

Solana的 DeFi生态(如Raydium、Jupiter)确实也为xStocks增添活力,散户可将代币用于流动性挖矿或借贷,保留了部分DeFi基因。

但相比Mirror的社区驱动,xStocks 更像一场由交易所和TradFi巨头导演的大戏:规模更大,野性更少。

-

市场与监管环境:从灰色地带到合规为王

2020年的 Mirror 诞生于监管的灰色地带。DeFi之夏几乎无人问津合规,匿名交易是社区的默认规则。2022年,SEC认定mAssets为未注册证券,Terraform Labs深陷诉讼,匿名性成了致命伤。

那时的市场还小,DeFi更像一群极客的试验场。

2025年的市场与监管截然不同。xStocks等项目以合规为先,强制KYC/AML,符合欧盟MiCA法规和美国证券法。

特朗普政府2025年1月上任后,SEC 新主席Paul Atkins将代币化称为“金融的数字革命”,宽松政策也在为创新松绑。2025年6月,Dinari 获美国首个代币化股票经纪牌照,进一步为Kraken、Coinbase铺路。

主流金融的拥抱和市场环境的变化,让 xStocks 和 Robinhood 以合规姿态规避了Mirror的法律雷区,但也似乎让链上美股少了当年的草根味道。

夏天的余韵

加密圈这么几年,像是变了,又好像没变。

5年前 DeFi 里的美股代币化,像一场未经雕琢的狂欢,充满了激情却缺乏稳定性。5年后的今天,加密穿上了合规的外衣,路走的更稳了,却也少了几分随性和草莽气质。

类似的产品,不同的光景。

当更多人将 BTC 视作数字黄金,当机构们摩拳擦掌,当加密逐渐变成做高传统资本市场股价的工具,圈内外的两波人,或许已经在不经意间完成了疑问的转换:

以前炒美股的人不理解为什么加密市场这么火爆;现在炒币的人开始疑惑带加密标签的美股为何越涨越高。

只是那年夏天,那份人人都争先恐后上场的 FOMO 狂热,那种无处不在的草莽和极客精神,或许早已随风而逝。

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。