The White House forked the code repository, the Treasury Secretary submitted a pull request, and finance ministers from various countries quickly clicked to merge, hardcoding the dollar into every future trade cycle.

Written by: Sumanth Neppalli, Decentralised.co

Compiled by: Jinse Finance xiaozou

In July 1944, representatives from 44 Allied nations gathered in the rural ski town of Bretton Woods, New Hampshire, to redesign the global monetary system. They pegged national currencies to the dollar, while the United States pegged the dollar to gold. This system, designed by British economist John Maynard Keynes, ushered in an era of exchange rate stability and frictionless trade.

Let’s imagine that summit as a GitHub project: the White House forked the code repository, the Treasury Secretary submitted a pull request, and finance ministers from various countries quickly clicked to merge, hardcoding the dollar into every future trade cycle. Stablecoins are today’s digital equivalent of that merge commit—while the rest of the world is still debugging its own code repositories, trying to build a future without the dollar.

Within 72 hours of Trump returning to the Oval Office, he signed an executive order that included a directive that sounded more like a crypto Twitter (CT) fan fiction than fiscal policy: "Promote and protect the sovereignty of the dollar, including through globally legitimate, dollar-backed stablecoins."

Congress then introduced the GENIUS Act (Guidance and Establishment of a National Innovation Framework for U.S. Stablecoins)—the first bill to establish basic rules for a stablecoin framework and encourage the global use of stablecoin payments.

The bill has passed debate and is submitted for Senate consideration, with a vote expected this month. Staff believe that suggestions from the Democratic coalition have been incorporated into the latest draft, and the bill is likely to pass.

But why has Washington suddenly developed a fondness for stablecoins? Is it just political theater, or is there a deeper strategic layout behind it?

1. Why Overseas Demand Remains Crucial

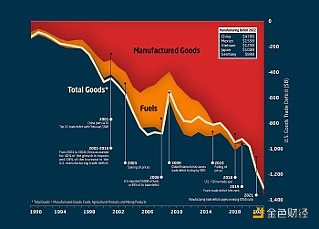

Since the 1990s, the United States has outsourced manufacturing to China, Japan, Germany, and Gulf countries, paying for each batch of imported goods with newly issued dollars. With imports consistently exceeding exports, the U.S. has maintained a massive trade deficit. A trade deficit is the difference between a country's total imports and total exports.

These dollars put exporting countries in a dilemma: if they convert dollars into their local currency, it will appreciate the exchange rate, weaken product competitiveness, and harm their own exports. Therefore, central banks choose to absorb dollars and invest in U.S. Treasury bonds, achieving capital circulation without disrupting the foreign exchange market. This move allows them to earn bond yields while the credit risk is almost equivalent to holding idle dollars.

This mechanism creates a self-reinforcing cycle: exporting to the U.S. to earn dollars → investing in U.S. bonds to earn interest → maintaining a weak local currency to continue expanding exports. This "supplier financing cycle" formed with exporting countries contributes about a quarter to the U.S. $36 trillion debt, locking in a key advantage. If this cycle is broken through a prolonged trade war, the U.S.'s cheapest financing channel will gradually dry up.

Deficit financing mechanism: U.S. government spending consistently exceeds tax revenue, creating a structural budget deficit. The deficit pressure is shared by selling Treasury bonds overseas: short-term Treasury bills (T-bills) mature within one year, while long-term Treasury bonds have terms of 20-30 years.

Low-interest rate effect: High demand for Treasury bonds suppresses yields (interest rates). When major buyers like China push up bond prices, yields fall, thereby reducing financing costs for the government, businesses, and consumers. This low-cost funding sustains economic growth and supports expansionary fiscal policy.

Cornerstone of Dollar Hegemony: The dollar's status as a reserve currency depends on global confidence in U.S. assets. Foreign holdings of U.S. bonds symbolize trust in the U.S. economy, ensuring the dollar's dominance in international trade, oil pricing, and foreign exchange reserves. This privilege allows the U.S. to finance at extremely low costs and exert economic influence globally.

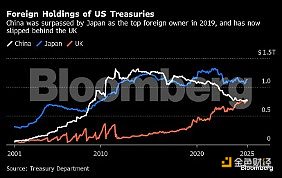

If this demand is lost, the U.S. will face soaring financing costs, a depreciating dollar, and declining geopolitical influence. Crisis warnings have already emerged. Warren Buffett admitted upon retirement that he was most worried about an imminent dollar crisis. For the first time in a century, the U.S. lost its AAA credit rating from all three major rating agencies—this is the "gold standard certification" of the bond market, indicating that the safety level of its debt has peaked. After the downgrade, the U.S. Treasury had to raise yields to attract buyers, while interest expenses will also rise as national debt continues to soar.

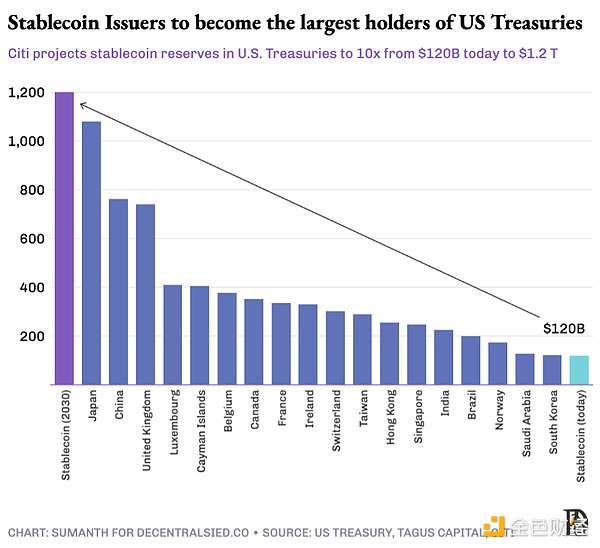

If traditional buyers begin to withdraw from the bond market, who will absorb the newly issued trillions of dollars in debt? Washington's bet is that regulated, fully reserved stablecoins will open new channels. The GENIUS Act mandates that stablecoin issuers purchase short-term Treasury bonds, which explains why the government is embracing digital dollars while making strong trade statements.

2. Lessons from the Eurodollar System

Such financial innovations are not new to the U.S. The $1.7 trillion Eurodollar system also experienced a journey from complete resistance to full acceptance. Eurodollars refer to dollar deposits held in overseas banks (mainly in Europe) that are not subject to U.S. banking regulations.

The Eurodollar was born in the 1950s when the Soviet Union deposited dollars in European banks to evade U.S. jurisdiction. By 1970, its market size had reached $50 billion, growing fiftyfold in a decade. The U.S. was initially skeptical; French Finance Minister Valéry Giscard d'Estaing referred to it as a "hydra-headed monster." After the 1973 oil crisis, when OPEC actions quadrupled global oil trade volumes in a matter of months, these concerns were temporarily set aside—the world needed dollars as a stable medium of trade.

The Eurodollar system enhanced the U.S.'s ability to project influence without military force. As international trade and the Bretton Woods system solidified dollar hegemony, the system continued to expand. Although Eurodollars were only used for payments between foreign entities, all transactions had to be settled through a global network of correspondent banks with U.S. banks.

This created powerful leverage for U.S. national security objectives: officials could not only block transactions within the U.S. but also kick bad actors out of the global dollar system. As the U.S. acted as a clearing center, it could trace the flow of funds and impose financial sanctions on nations.

3. Stablecoins: The Digital Upgrade of the Dollar

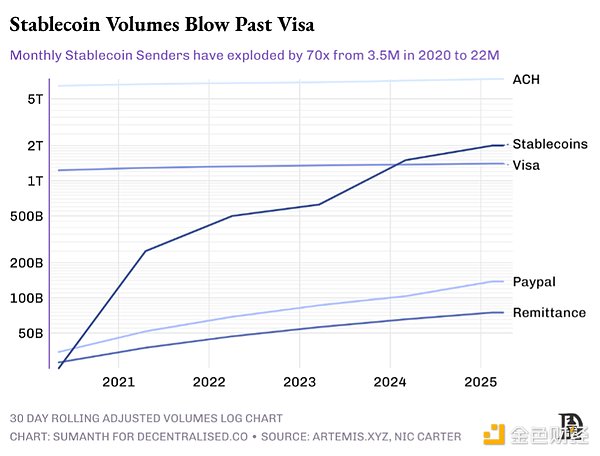

Stablecoins are the contemporary Eurodollars equipped with public blockchain explorers. Dollars are no longer stored in London vaults but are "tokenized" through blockchain. This convenience brings real scale: by 2024, on-chain dollar token settlements are expected to reach $15 trillion, slightly surpassing the Visa network. Currently, of the $245 billion in circulating stablecoins, 90% are fully collateralized dollar stablecoins.

As investors seek to lock in returns and avoid cyclical market fluctuations, demand for stablecoins is increasing daily. Unlike the volatile market cycles of cryptocurrencies, stablecoin activity continues to grow, indicating that its use has far exceeded the realm of transactions.

The earliest demand emerged in 2014 when Chinese cryptocurrency exchanges needed non-bank dollar settlement solutions. They chose Realcoin (later renamed Tether), a dollar token based on the Bitcoin Omni protocol. Tether initially connected with fiat currency channels through Taiwanese banks until Wells Fargo terminated its agency relationships with these banks due to regulatory pressure. In 2021, the U.S. Commodity Futures Trading Commission (CFTC) fined Tether $41 million for misreporting reserves, accusing it of not achieving full collateralization for its tokens.

Tether's operating model is a classic banking approach: absorb deposits → invest idle funds → earn interest spread. It converts about 80% of its issued reserves into U.S. Treasury bonds, with a 5% yield on short-term bonds, yielding $6 billion annually from a $120 billion position. In 2024, Tether is expected to achieve a net profit of $13 billion, while Goldman Sachs' net profit during the same period is $14.28 billion—but the former has only 100 employees (averaging $130 million profit per employee), while the latter has 46,000 employees (averaging $310,000 profit per employee).

Competitors are trying to build trust through transparency. Circle publishes monthly USDC audit reports detailing minting and redemption records. Even so, the industry still relies on the credit endorsement of issuers. In March 2023, the collapse of Silicon Valley Bank left Circle with $3.3 billion in trapped reserves, causing USDC to briefly drop to $0.88 until the Federal Reserve intervened to restore its peg.

Washington is working to establish a regulatory framework. The GENIUS Act explicitly requires:

- 100% reserves must be in Treasury bonds / reverse repos or other high-quality liquid assets (HQLA);

- Real-time audit verification through licensed oracles;

- Regulatory interfaces: issuer-level freeze functions, compliance with FATF rules;

- Compliant stablecoins can access Federal Reserve master accounts and reverse repo liquidity support.

A graphic designer in Berlin can now hold dollars without needing a U.S. account or going through a German bank or SWIFT documents—so long as Europe does not enforce a digital euro, a Gmail account and KYC selfie will suffice. Funds are flowing from bank ledgers to wallet applications, and companies controlling these applications will function as global banks without branches.

If this bill becomes law, existing issuers will face a choice: either register in the U.S. to accept quarterly audits, anti-money laundering reviews, and reserve proof, or watch as U.S. trading platforms shift to compliant tokens. Circle, which has placed most of its collateral in SEC-regulated money market funds, clearly occupies a more advantageous position.

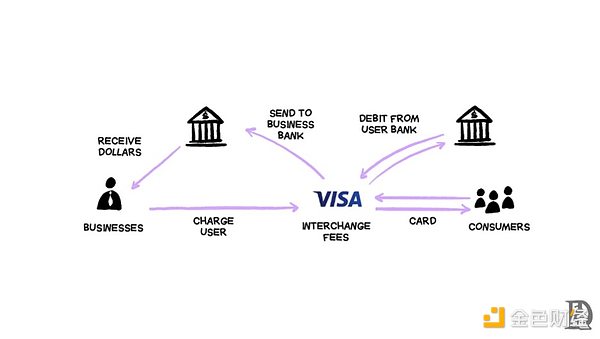

But Circle will not monopolize this blue ocean. Tech giants and Wall Street have every reason to enter the fray—imagine Apple Pay launching "iDollars": deposit $1,000 to earn returns and spend in all contactless payment scenarios. The yield on idle funds far exceeds existing card transaction fees, while completely bypassing traditional intermediaries. This may be the reason Apple terminated its credit card partnership with Goldman Sachs: when payments are made in on-chain dollars, the original 3% transaction fee will shrink to a per-transaction fee on the blockchain network.

Large banks such as Bank of America, Citigroup, JPMorgan Chase, and Wells Fargo have begun exploring the joint issuance of stablecoins. The GENIUS Act prohibits issuers from distributing interest earnings to users, which has relieved banking lobbyists. This model essentially becomes a super cheap checking account: instant, global, and never-ending.

It is not surprising that traditional payment giants are rushing to lay out their plans: Mastercard and Visa have launched stablecoin settlement networks, PayPal has issued its own stablecoin, and Stripe completed the largest cryptocurrency acquisition to date this year (acquiring Bridge). They are well aware that change is imminent.

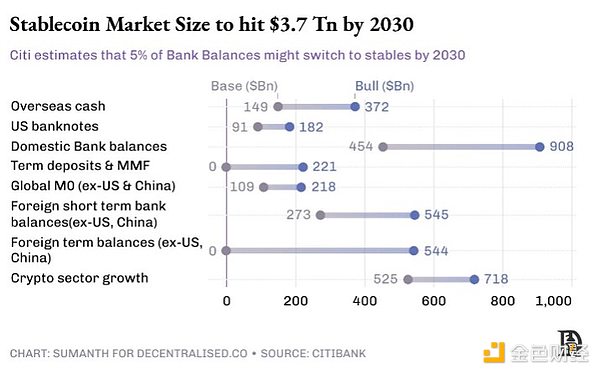

Washington is equally aware. Citibank predicts that under a baseline scenario, the stablecoin market will grow sixfold to $1.6 trillion by 2030. Research from the U.S. Treasury indicates that this figure could exceed $2 trillion by 2028. If the GENIUS Act mandates that 80% of reserves be allocated to Treasury bonds, "stable dollars" will replace China and Japan as the largest holders of U.S. debt.

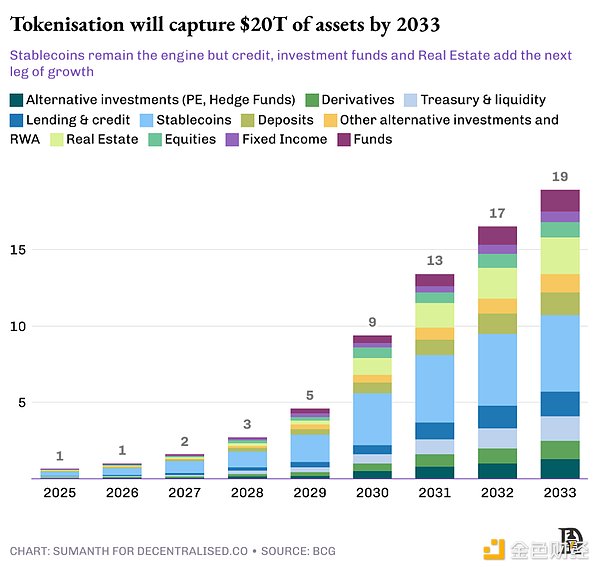

4. Assets Queueing to Go On-Chain

As "dollar stablecoins" become widespread, they will serve as the liquidity driving the entire token economy. Once cash is tokenized, people will conduct off-chain routine operations—savings, lending, and collateralization—at internet speed (rather than bank speed). This endless liquidity will continuously seek the next tokenization target, bringing more "real-world assets" (RWA) onto the blockchain and granting them equal advantages.

24/7 Settlement: The traditional T+2 settlement cycle will become obsolete, as blockchain validators can confirm transactions in minutes (rather than days). For example, a trader in Singapore could purchase a tokenized New York apartment at 6 PM local time and receive ownership confirmation before dinner.

Programmability: Smart contracts embed behavioral logic directly into assets. This makes complex financial operations possible: interest payments, distribution rights, and compliance parameters at the asset level can all be executed automatically.

Composability: Tokenized Treasury bonds can serve as collateral for loans and enable automatic distribution of interest earnings among multiple holders. An expensive beachfront villa can be split into 50 equity shares and rented out to hotel operators managing bookings through Airbnb.

Transparency: Part of the 2008 financial crisis stemmed from the opacity of the derivatives market. Regulators can now monitor on-chain collateral ratios in real-time, track systemic risks, and observe market dynamics without waiting for quarterly reports.

The main obstacle lies in regulation. The protective mechanisms of traditional exchanges are hard-won lessons, and investors are well aware of the protections they can expect. Take the example of "Black Monday" in 1987: the Dow Jones Industrial Average plummeted 22% in a single day, triggered by price fluctuations that activated automated sell-offs, leading to a chain reaction. The SEC's solution was a circuit breaker—pausing trading to allow investors to reassess the situation. Today, the NYSE mandates a 15-minute trading halt if prices drop by 7%.

Tokenization of assets is not technically difficult; issuers only need to guarantee the rights to the real assets corresponding to the tokens. The real challenge is ensuring that the underlying systems can enforce all applicable offline rules: this includes wallet-level whitelisting, national identity verification, cross-border KYC/AML, citizen holding limits, and real-time sanctions screening—all of which must be encoded into the system.

The European Markets in Crypto-Assets Regulation (MiCA) provides a complete regulatory framework for digital assets, while Singapore's Payment Services Act serves as a starting point for Asia. However, the global regulatory landscape remains fragmented.

This process will almost inevitably advance in waves. The first phase will prioritize on-chain financial instruments that are highly liquid and low-risk, such as money market funds and short-term corporate bonds. The operational benefits of instant settlement will be immediately apparent, and compliance processes will be relatively simple.

The second phase will move toward the higher end of the risk-return curve, covering high-yield varieties such as private credit, structured financial products, and long-term bonds. The value of this phase lies not only in efficiency gains but also in releasing liquidity and composability.

The third phase will achieve a qualitative leap, expanding to illiquid asset classes: private equity, hedge funds, infrastructure, and real estate mortgage debt. To achieve this goal, there must be widespread recognition of tokenized assets as collateral, and a cross-industry tech stack must be established to serve these assets. Banks and financial institutions will need to provide credit while also custodizing these real-world assets (RWA) as collateral.

Although the pace of tokenization varies across different asset classes, the direction of development is clear. Each wave of new "stable dollar" liquidity is pushing the token economy toward a higher stage.

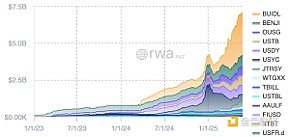

(1) Stablecoin Landscape

The dollar-pegged token market exhibits a duopoly, with Tether (USDT) and Circle (USDC) collectively holding 82% market share. Both are fiat-collateralized stablecoins—the euro stablecoin operates on the same principle, supporting each circulating token by storing euros in banks.

In addition to fiat models, developers are exploring two experimental schemes to achieve decentralized pegging without relying on off-chain custodians:

Cryptocurrency-collateralized stablecoins: These use other cryptocurrencies as reserves, typically over-collateralized to withstand price fluctuations. MakerDAO is a leader in this field, having issued $6 billion in DAI. After the 2022 bear market, Maker quietly converted more than half of its collateral into tokenized Treasury bonds and short-term bonds, smoothing out ETH volatility while earning returns; this allocation currently contributes about 50% of the protocol's income.

Algorithmic stablecoins: These stablecoins do not rely on any collateral but maintain their peg through an algorithmic mint-and-burn mechanism. Terra's stablecoin UST reached a market cap of $20 billion but triggered a bank run during its de-pegging event due to a collapse of confidence. Although new projects like Ethena have scaled to $5 billion through innovative models, this field still needs time to gain widespread recognition.

If Washington only grants "qualified stablecoin" certification to fully fiat-collateralized stablecoins, other types may be forced to abandon the "dollar" designation in their names to comply with regulations. The fate of algorithmic stablecoins remains uncertain—the GENIUS Act requires the Treasury to conduct a year-long study of these protocols before making a final determination.

(2) Money Market Instruments

Money market instruments include Treasury bonds, cash, and repurchase agreements, which are high liquidity short-term assets. On-chain funds achieve "tokenization" by encapsulating ownership rights as ERC-20 or SPL tokens. This vehicle supports 24/7 redemptions, automatic yield distribution, seamless payment integration, and convenient collateral management.

Asset management companies retain their existing compliance frameworks (anti-money laundering/identity verification, accredited investor restrictions), but settlement times are reduced from days to minutes.

BlackRock's U.S. Institutional Digital Liquidity Fund (BUIDL) is a market leader. The firm has appointed SEC-registered transfer agent Securitize to handle KYC access, token minting/burning, FATCA/CRS tax compliance reporting, and shareholder registry maintenance. Investors must have at least $5 million in investable assets to qualify, but once on the whitelist, they can purchase, redeem, or transfer tokens around the clock—flexibility that traditional money market funds cannot offer.

BUIDL's assets under management have grown to approximately $2.5 billion, distributed among over 70 whitelist holders across five blockchains. About 80% of the funds are allocated to short-term Treasury bills (primarily with 1-3 month maturities), 10% to longer-term Treasury bonds, and the remaining portion held in cash positions.

Products like Ondo (OUSG) operate as investment management pools, allocating funds to tokenized money market fund portfolios from institutions like BlackRock, Franklin Templeton, and WisdomTree, while providing a free entry and exit channel with stablecoins.

Although a $10 billion scale is insignificant in the face of a $26 trillion Treasury market, its symbolic significance is immense: top asset management firms on Wall Street are choosing public chains as distribution channels.

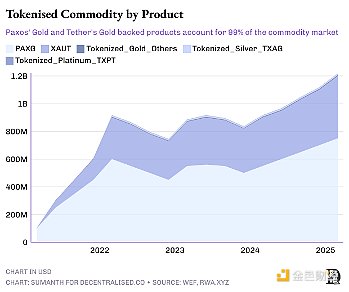

(3) Commodities

The tokenization of hard assets is transforming these markets into platforms for 24/7, click-to-trade transactions. Paxos Gold (PAXG) and Tether Gold (XAUT) allow anyone to purchase tokenized shares of gold bars; Venezuela's 1 PETRO is pegged to 1 barrel of oil; small pilot projects have linked token supplies to soybeans, corn, and even carbon credits.

The current model still relies on traditional infrastructure: gold bars are stored in vaults, crude oil is stored in tank farms, and auditing firms sign reserve reports monthly. This custodial bottleneck creates concentration risks, and physical redemptions are often difficult to achieve.

Tokenization not only enables fractional ownership of assets but also makes traditional illiquid physical assets easier to use as collateral for financing. This sector has reached a scale of $145 billion (almost entirely backed by gold), compared to a $5 trillion physical gold market, indicating significant room for growth.

(4) Lending and Credit

DeFi lending initially emerged in the form of over-collateralized cryptocurrency loans. Users must pledge $150 worth of ETH or BTC to borrow $100, operating similarly to gold-backed loans. These users wish to hold digital assets long-term in anticipation of appreciation while needing liquidity to pay bills or open new positions. Currently, the Aave platform has a lending scale of approximately $17 billion, capturing nearly 65% of the DeFi lending market.

The traditional credit market is dominated by banks, which underwrite risks through decades of validated risk models and strictly regulated capital buffers. Private credit, as an emerging asset class, has developed in parallel with traditional credit to a global management scale of $30 trillion. Companies no longer rely solely on banks but finance themselves by issuing high-risk, high-yield loans, which are particularly attractive to private equity funds and asset management institutions seeking higher returns.

Bringing this field on-chain can expand the pool of lenders and enhance transparency. Smart contracts can automate the entire loan lifecycle: fund disbursement, interest collection, while ensuring that the conditions for triggering liquidation are clearly visible on-chain.

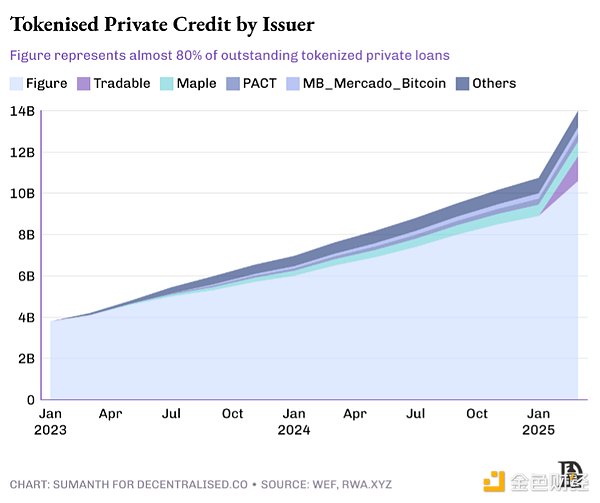

Two models of on-chain private credit:

"Retail" Direct Lending: Platforms like Figure tokenize home renovation loans and sell fractional notes to wallets seeking returns globally, akin to a debt version of Kickstarter. Homeowners can achieve lower financing costs by splitting loans into smaller shares, while retail savers receive monthly interest payments, and the protocol automatically handles the repayment process.

Pyse and Glow package solar projects, tokenize power purchase agreements, and manage the entire process from panel installation to meter readings. Investors can simply sit back and earn an annual return of 15-20% directly from their monthly electricity bills.

Institutional Liquidity Pools: Private credit desks present their offerings in a transparent on-chain format. Protocols like Maple, Goldfinch, and Centrifuge bundle borrower demand into on-chain credit pools managed by professional underwriters. Depositors mainly consist of accredited investors, DAOs, and family offices, who can earn floating returns (7-12%) while tracking asset performance on a public ledger.

These protocols aim to reduce operational costs, allowing underwriters to conduct due diligence on-chain and complete disbursements within 24 hours. Qiro employs a network model for underwriters, where each underwriter uses an independent credit model, and analysis work is rewarded accordingly. Due to higher default risks, this sector is growing slower than mortgage lending. When defaults occur, protocols cannot use traditional collection methods like court orders and must rely on traditional collection agencies, leading to increased disposal costs.

As underwriters, auditors, and collection agencies continue to move on-chain, market operating costs will keep decreasing, and the lender's capital pool will deepen significantly.

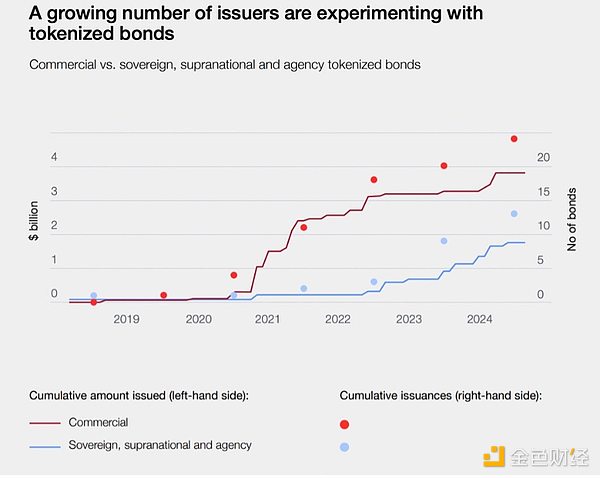

(5) Tokenized Bonds

Bonds and loans are both debt instruments, but they differ in structure, standardization, and issuance and trading methods. Loans are one-to-one agreements, while bonds are one-to-many financing tools. Bonds use a fixed format—such as a bond with a 5% coupon rate and a 10-year term, which is easier to rate and trade in the secondary market. As publicly regulated instruments, bonds are typically rated by agencies like Moody's.

Bonds are usually used to meet large-scale, long-term capital needs. Governments, utility companies, and blue-chip firms issue bonds to raise budget funds, build factories, or obtain bridge loans. Investors receive interest payments regularly and recover principal at maturity. This asset class is enormous: as of 2023, its nominal value is approximately $140 trillion, equivalent to 1.5 times the total market capitalization of global equities.

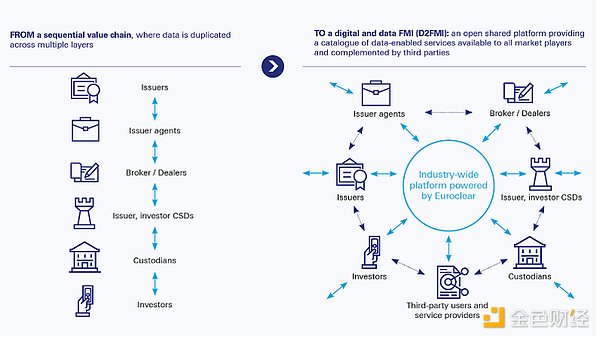

The current market still operates on outdated infrastructure designed in the 1970s. Clearing institutions like Euroclear and the Depository Trust & Clearing Corporation (DTCC) require multiple custodians for transactions, leading to delays and creating a T+2 settlement system. In contrast, smart contract bonds can achieve atomic settlement in seconds, automatically distribute dividends to thousands of wallets, embed compliance logic, and connect to global liquidity pools.

Each bond issuance can save 40-60 basis points in operational costs, and financial officers can access a 24/7 secondary market without paying exchange listing fees. As a core settlement and custody channel in Europe, Euroclear holds €40 trillion in assets, connecting over 2,000 institutions to 50 markets. The agency is developing a blockchain-based settlement platform for issuers, brokers, and custodians, aiming to eliminate redundant operations, reduce risks, and provide clients with real-time digital workflows.

Companies like Siemens and UBS have issued on-chain bonds as part of a pilot project with the European Central Bank. The Japanese government is also collaborating with Nomura Securities to experiment with on-chain bond solutions.

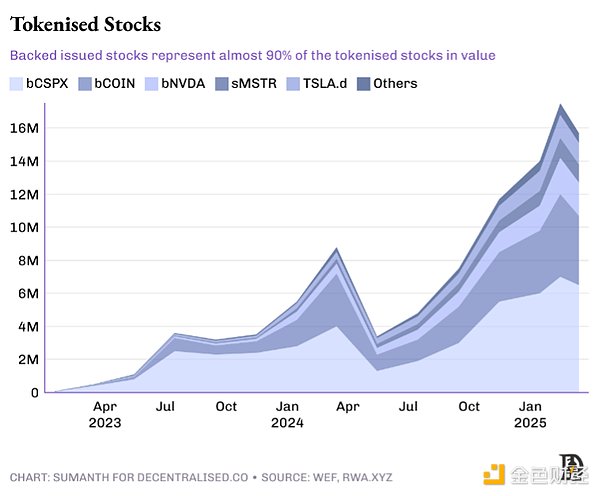

(6) Stock Market

This field inherently possesses development potential—the stock market already has a large number of retail participants, and tokenization can create a 24/7 "internet capital market."

Regulatory barriers are the main bottleneck. The current custody and settlement rules of the U.S. Securities and Exchange Commission (SEC) were established before the blockchain era, mandating the involvement of intermediaries and maintaining a T+2 settlement cycle.

This situation is beginning to loosen. Solana has applied to the SEC for approval of an on-chain stock issuance plan, which includes KYC verification, investor education processes, broker custody requirements, and instant settlement features. Robinhood has followed suit with its application, arguing that tokens representing U.S. Treasury stripping certificates or Tesla shares should be viewed as securities themselves, rather than synthetic derivatives.

Demand in overseas markets is even stronger. Thanks to relaxed regulations, foreign investors hold approximately $19 trillion in U.S. stocks. The traditional path is to invest through local brokers like eTrade (which must collaborate with U.S. financial institutions and pay high foreign exchange spreads). Startups like Backed are providing alternatives—synthetic assets. Backed purchases equivalent underlying stocks in the U.S. market and has completed $16 million in business. Kraken recently partnered with them to offer U.S. stock trading services to non-U.S. traders.

(7) Real Estate and Alternative Assets

Real estate is the asset class most constrained by paper certificates. Each deed is stored in government registries, and each mortgage document is locked away in bank vaults. Large-scale tokenization is difficult to achieve until registries accept hashes as legal proof of ownership. Currently, only about $2 billion of the $400 trillion global real estate market has been tokenized.

The UAE is one of the regions leading the transformation, with $3 billion worth of property deeds already registered on-chain. In the U.S. market, real estate tech companies like RealT and Lofty AI have achieved over $100 million in residential asset tokenization, with rental income flowing directly to digital wallets.

Five, The Desire for Fluidity in Capital

Crypto-punks view "dollar stablecoins" as a regression to bank custody and whitelisted permissions, while regulators are reluctant to accept permissionless channels that can transfer a billion dollars in a single block. However, the reality is that true adoption is born precisely at the intersection of these two "discomfort zones."

Crypto purists will still complain, just as early internet purists despised centralized institutions issuing TLS certificates. But it was HTTPS technology that allowed our parents to safely use online banking. Similarly, dollar stablecoins and tokenized Treasury bonds may seem "not pure enough," yet they will become the way billions of people first silently engage with blockchain—through an application that never mentions the term "cryptocurrency."

The Bretton Woods system locked the world into a single currency, while blockchain has liberated the temporal shackles of currency. Every asset that goes on-chain can shorten settlement times, release collateral sleeping in clearinghouses, allowing the same dollar to secure three transactions before lunch arrives.

We continually return to the same core point: the velocity of money circulation will ultimately become the killer application scenario for cryptographic technology, and the on-chain of real assets aligns perfectly with this theme. The faster value settlements occur, the higher the frequency of capital redeployment, and the larger the market pie becomes. When dollars, debts, and data flow at internet speed, business models will no longer rely on transfer fees but will profit from the potential of liquidity.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。