The success of consumer-grade crypto largely depends on its ability to eliminate technical complexity and provide users with an intuitive, value-added experience.

Author: Morph & The Block Pro

With the continuous development of blockchain technology and the increase in mainstream adoption, an explosion of use cases has emerged, particularly in categories such as media, sports, entertainment, and gaming. A new special ecological field is beginning to take shape—this is the consumer-grade crypto ecosystem.

Recently, the global consumer-grade public chain Morph commissioned the overseas research institution The Block Pro (under The Block) to conduct research on the consumer-grade crypto ecosystem, resulting in an in-depth industry report exceeding 50,000 words (Read the full text: English version, Chinese version), aimed at revealing future development trends in the industry, providing important references for crypto investors, startups, developers, and regulators, and helping stakeholders understand and explore the consumer-grade crypto ecosystem.

It is reported that Morph is a global consumer-grade public chain that utilizes optimistic and zkRollup technologies to enhance accessibility, efficiency, and usability for developers and consumer-grade blockchains, having received support from top capital firms such as Dragonfly, Pantera, Bitget, Spartan Ventures, and Foresight Ventures. As a resource distribution center, Morph can assist developers throughout the entire process from project initiation to large-scale market expansion.

Summary of Key Insights from the Report

The report first defines the "consumer-grade crypto field." The consumer-grade crypto field refers to platforms, use cases, and services designed for public use that support blockchain to facilitate everyday activities. It includes everything from tokenized loyalty programs and crypto collectibles to blockchain-based games and decentralized social media platforms. On-chain consumer-grade products aim to fundamentally reshape the way we interact with and experience products and services, creating more efficient, transparent, and user-centered solutions that disrupt traditional consumer industry practices.

The use cases primarily discussed in the report focus on on-chain consumer goods with an emphasis on everyday practicality and participation, rather than a financial focus on speculative ecosystems; thus, DeFi, GameFi, or NFTFi are not within the scope of discussion.

1. Market Landscape of Sub-sectors

The report explores the current market landscape of the consumer-grade crypto ecosystem and traditional consumer brand activities, systematically categorizing the consumer-grade crypto field into two main categories: application layer and infrastructure layer.

The application layer sub-sectors include: community/brand engagement, decentralized social, gaming, media, and communications; the infrastructure layer sub-sectors include: wallets, payments, DePIN, metaverse, on-chain analytics, and identity management. The report also highlights noteworthy projects and venture capital trends within each sub-sector. The specific content is elaborated as follows:

(1) Community/Brand Engagement

Community and brand engagement refers to a series of applications aimed at strengthening connections within communities, including the relationship between brands and their audiences. Applications in this sub-sector include loyalty reward programs, social and fan tokens, NFTs, and digital collectibles, as well as subscription and membership products. These applications aim to enhance user engagement, encourage ongoing interaction, and foster loyalty. Representative projects are as follows:

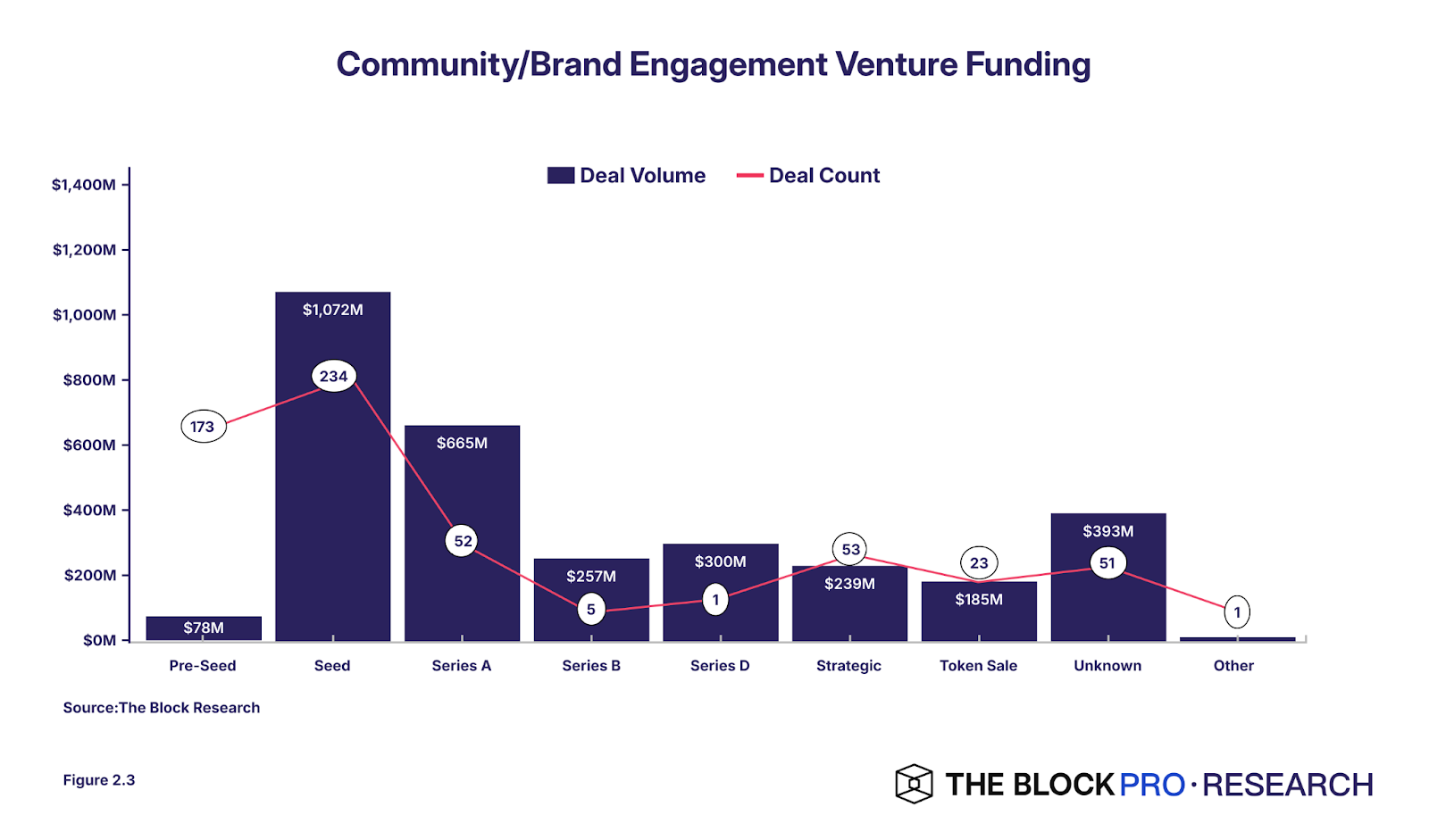

According to data from The Block, from 2019 to 2023, "community and brand engagement" raised approximately $3.2 billion across 593 transactions. Funding was primarily concentrated in earlier stages, with Series A, seed, and pre-seed rounds accounting for 57% of the total and 77% of the transaction count, a typical characteristic of emerging industries. As shown below:

(2) Decentralized Social

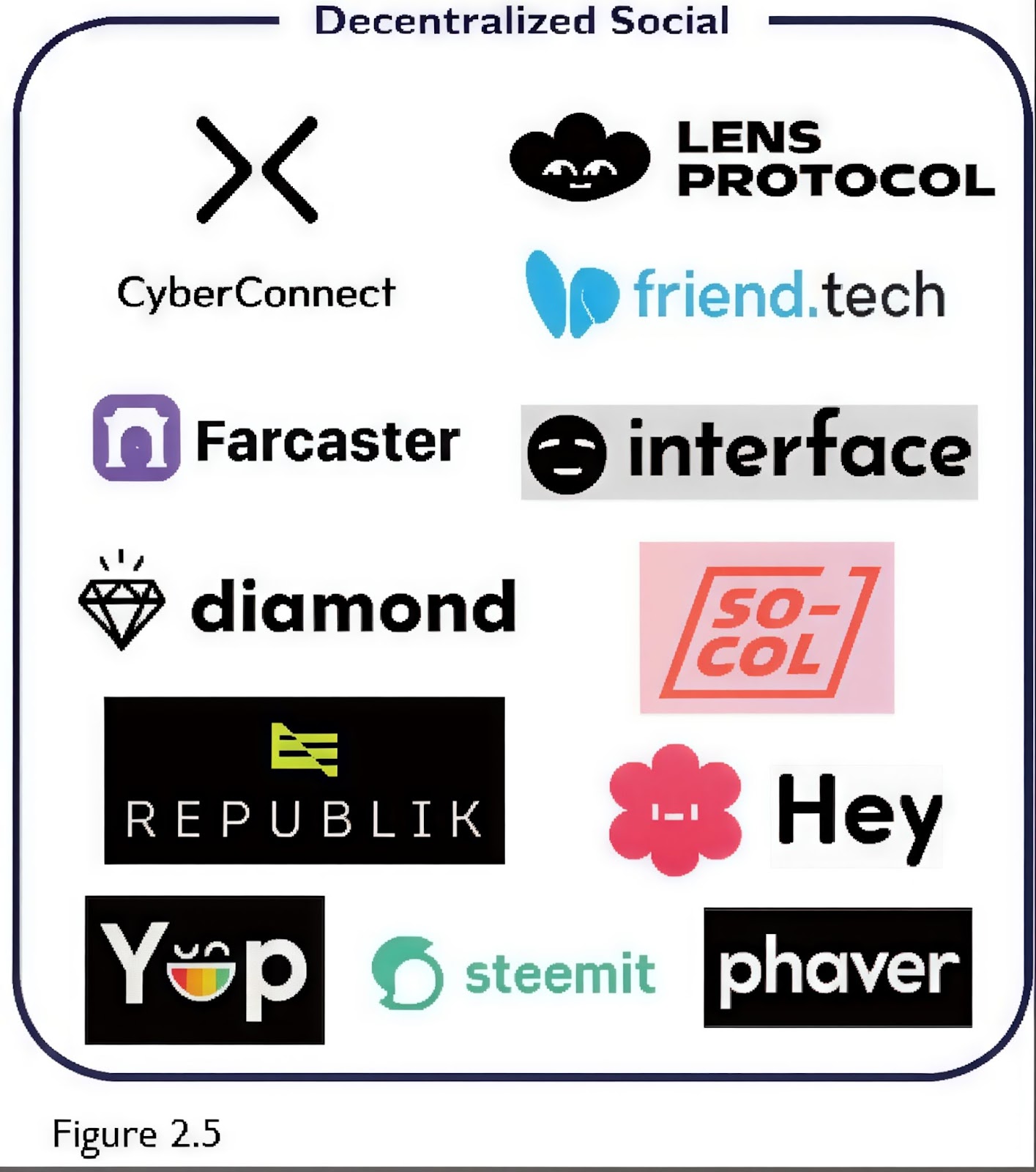

The decentralized social (DeSo) sub-sector encompasses blockchain-driven social network applications that enable users to create, share, and exchange information and content in a decentralized manner. DeSo represents a shift in how users interact, share content, and participate in online communities. The core features of DeSo emphasize censorship resistance, user control over data and content ownership, and incentivization through tokens. Representative projects are as follows:

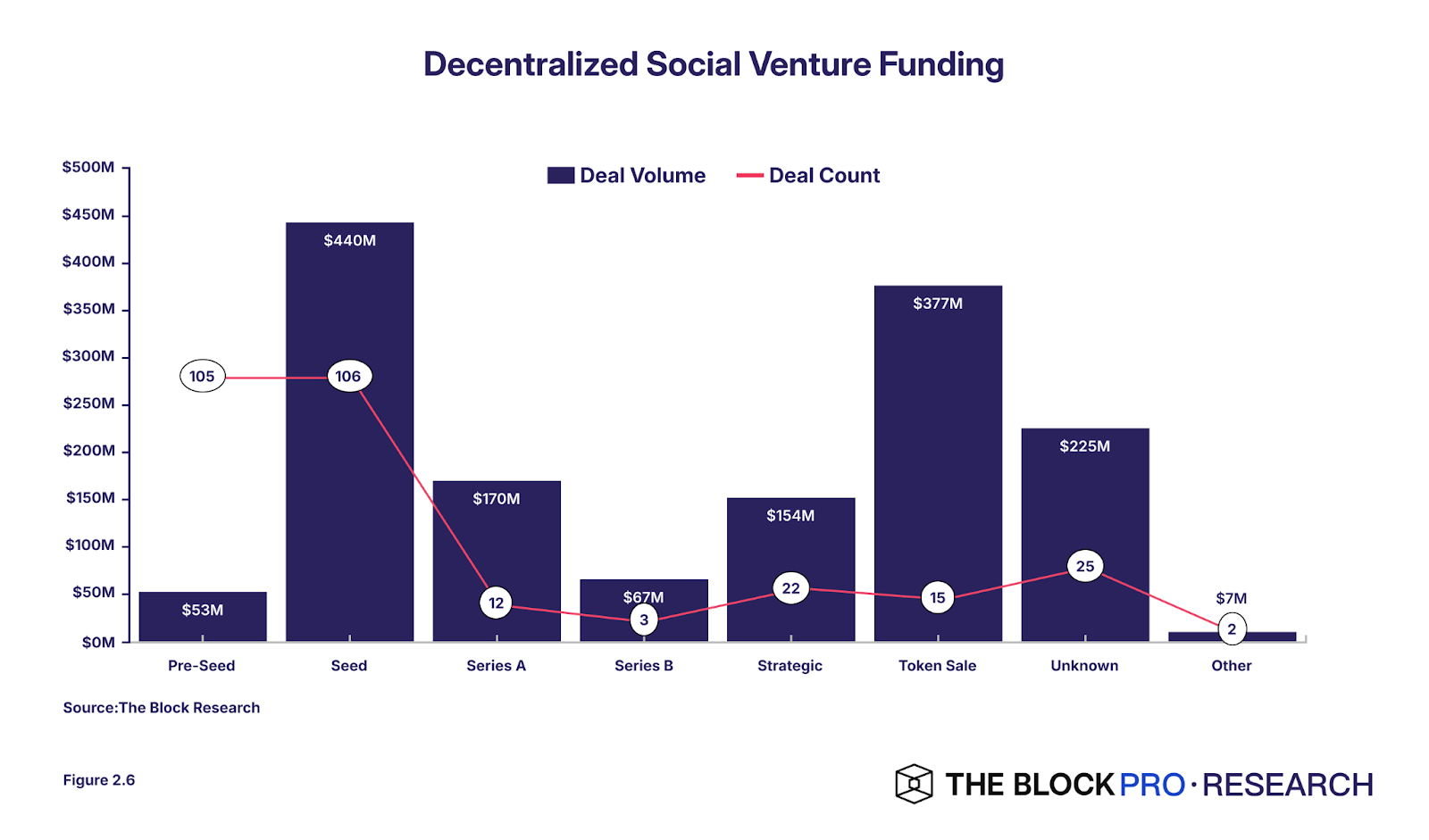

According to data from The Block, from 2019 to 2023, the decentralized social sub-sector conducted approximately 290 transactions, raising about $1.5 billion. The chart below shows that the top three funding rounds by transaction volume in the DeSo sub-sector were seed rounds, token sales, and Series A rounds, collectively accounting for nearly two-thirds of total funding.

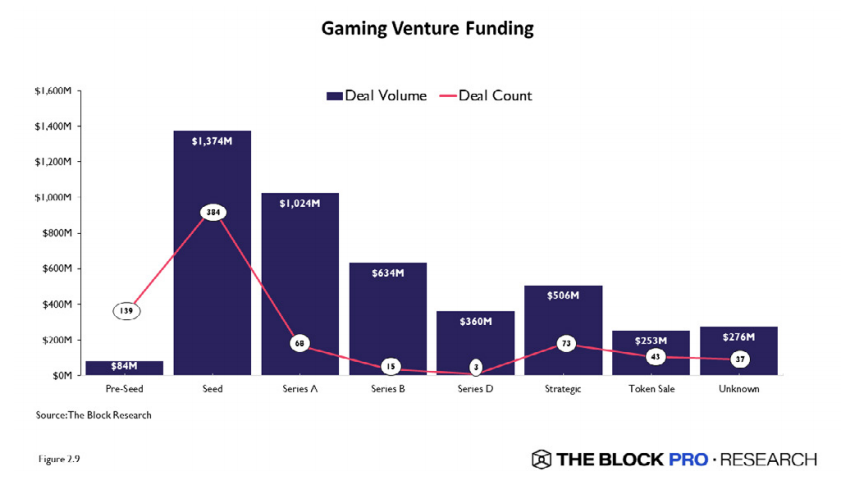

(3) Gaming

On-chain gaming transforms the traditional gaming industry by redefining the relationships between players, developers, and in-game assets through the use of blockchain technology. On-chain games create unique, player-driven economic systems where users can truly own, sell, and trade their digital assets, addressing the limitations of traditional gaming models. Additionally, the open-source nature of on-chain games fosters permissionless innovation, allowing developers to create mods, plugins, and custom game modes that can interoperate with the main game. Representative projects are as follows:

According to data collected from The Block's transaction dashboard, from 2019 to 2023, the on-chain gaming sub-sector raised approximately $4.5 billion across 762 transactions. The chart below shows that funding was primarily concentrated in seed and Series A rounds, which together accounted for 53% of transaction volume and 59% of transaction count.

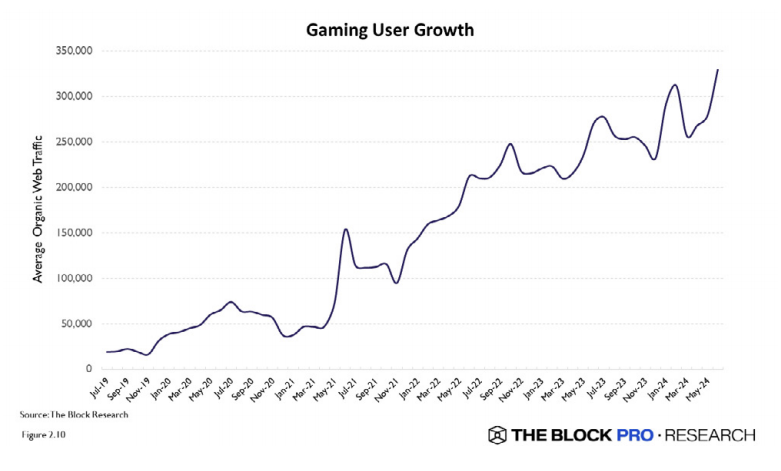

The investment surge from 2019 to 2023 coincided with a significant increase in user activity in the on-chain gaming sector. The chart below shows that, compared to other sub-sectors, user activity in on-chain gaming experienced a particularly noticeable upward trend, indicating that this emerging industry is gaining significant momentum. Furthermore, the growth in user activity remains relatively stable, suggesting that these applications may have higher user retention rates compared to other consumer-grade crypto sub-sectors.

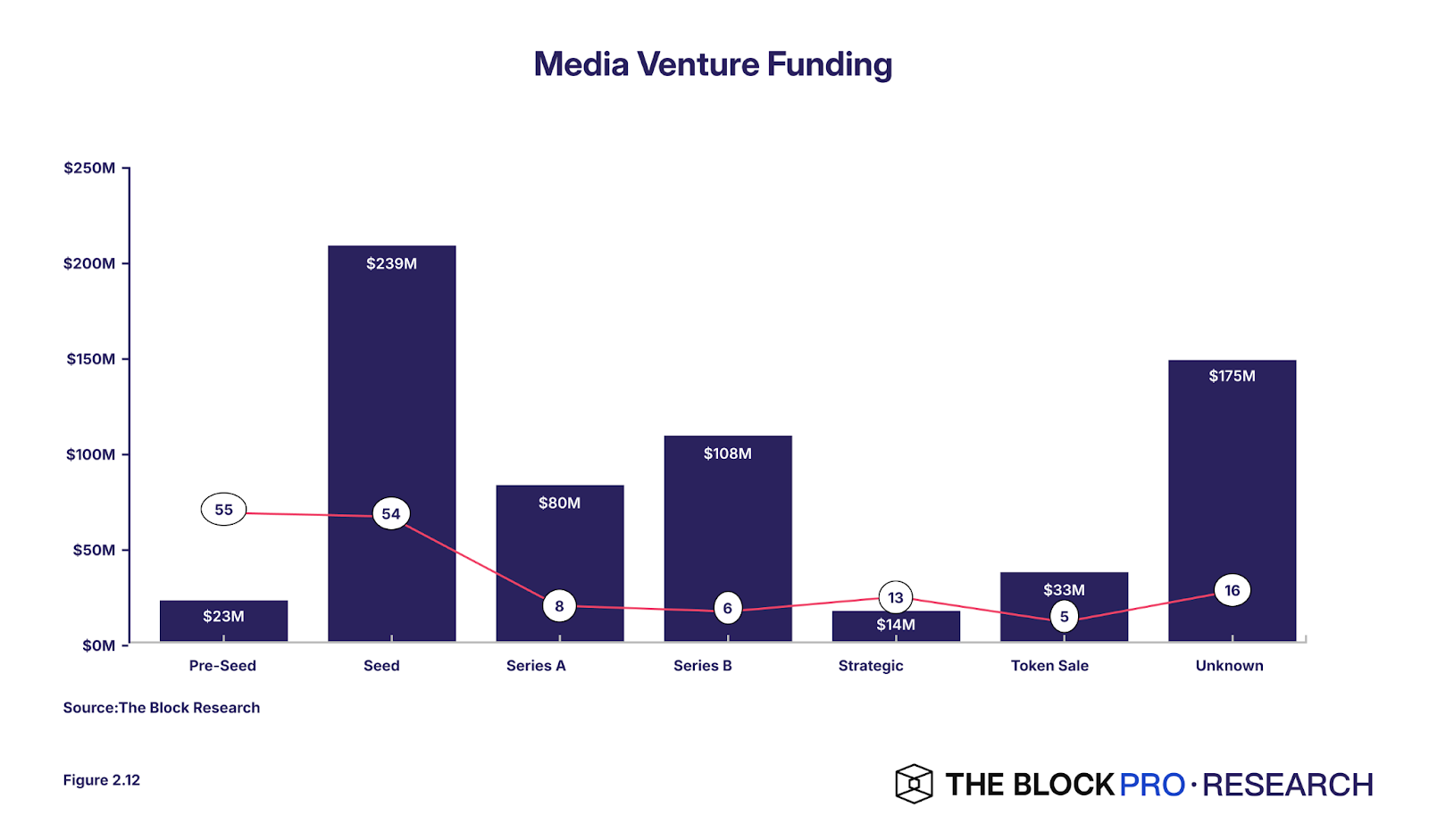

(4) Media

On-chain media applications leverage the immutable and transparent characteristics of blockchain technology to authenticate and establish ownership of digital content. By turning media assets into NFTs or other blockchain-based tokens, creators can prove their authorship and maintain control over the distribution and monetization of their works. Smart contracts enable automatic royalty payments, ensuring that creators receive a fair share of revenue each time their content is consumed or resold, reducing the need for intermediaries. Representative projects are as follows:

According to data from The Block, from 2019 to 2023, the decentralized media sub-sector raised approximately $672 million across 157 transactions. The chart below shows that funding was primarily concentrated in early stages. Series A, seed, and pre-seed rounds accounted for 51% of transaction volume and 75% of transaction count; over 80% of Series B transactions occurred in 2021 or later, indicating that as projects move beyond the initial funding phase, the industry's maturity is increasing.

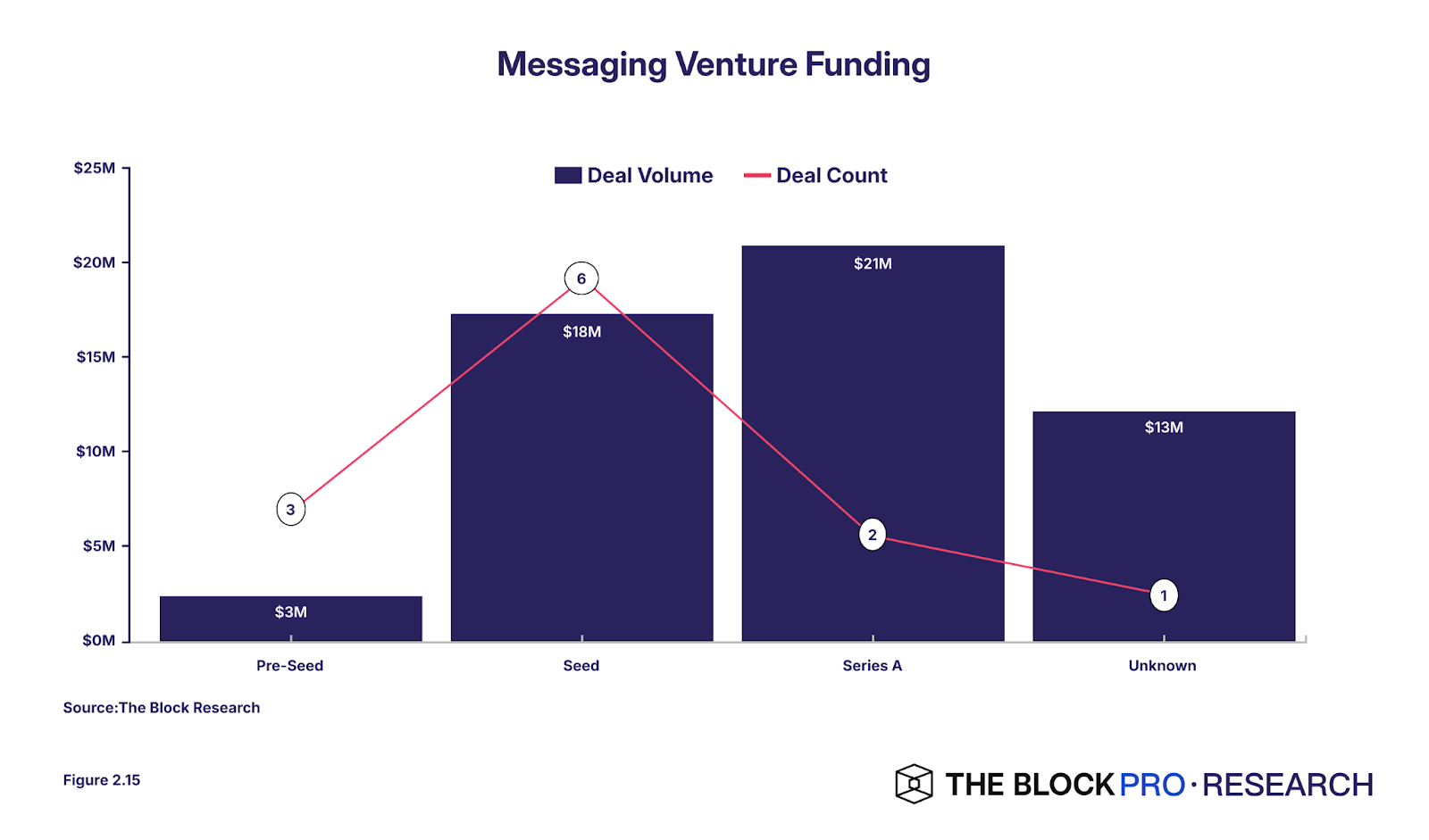

(5) Communications

On-chain communication protocols aim to address the limitations of centralized messaging platforms. In on-chain communication, messages occur directly between wallet addresses, eliminating the need for centralized intermediaries. Messages are encrypted and stored on decentralized networks, such as IPFS or blockchain. This decentralized approach ensures that no single entity controls the data, reducing the risk of data breaches, unauthorized access, and potential misuse of personal information. Representative projects are as follows:

According to data from The Block, on-chain communication raised approximately $54 million across 12 transactions from 2019 to 2023. The chart below shows that fundraising occurred primarily in Series A or earlier stages. This pattern may reflect a lack of a breakout application in the field, which typically attracts later-stage investment more easily. The focus on early stages indicates that, despite interest and potential in the on-chain communication field, it remains in its nascent stage.

(6) Wallets

Wallets are the key entry point for users to interact with decentralized applications and manage digital assets. Cryptocurrency wallets are software programs that allow users to store, send, and receive digital currencies, as well as interact with blockchain networks. The initial versions of wallet solutions included complex onboarding processes, the need for users to manage private keys, and cumbersome user interfaces. Improving the wallet user experience has been a key priority in driving mainstream adoption of on-chain products. Account abstraction and embedded wallets can simplify the user experience and lower the barriers to consumer participation. Representative projects are as follows:

(7) Payments

In the world of digital assets, on-chain payment infrastructure plays a crucial role, primarily serving two functions: facilitating exchanges between traditional finance and cryptocurrencies, and enabling transactions within the Web3 ecosystem. On and off-ramping solutions allow users to convert fiat currency to cryptocurrency and vice versa, making it easier for individuals to enter and exit the cryptocurrency space. On-chain payment infrastructure simplifies the process for consumers to manage cryptocurrencies, enhancing the utility of their on-chain funds. Representative projects are as follows:

(8) Networks

The network within the infrastructure layer refers to the foundational systems and protocols that support the efficient and secure transfer of digital assets, execution of smart contracts, and data storage. This sub-sector encompasses blockchain layer networks and networks built on existing consensus layers. These infrastructures form the backbone of the crypto ecosystem, providing the foundation for decentralized applications and services to operate. The emergence of new blockchain networks, such as Solana, Base, and Flow, has brought significant improvements to the network infrastructure layer. These networks prioritize faster transaction speeds, low latency, and cost-effectiveness, making them more suitable for consumer-grade use cases. Representative projects are as follows:

(9) Identity Management

Identity management refers to systems and protocols that enable users to manage their digital identities in a decentralized and autonomous manner. These solutions are designed to give users control over their personal data, allowing them to selectively share information with third parties while maintaining privacy and security. On-chain identity management solutions address the limitations of traditional centralized identity systems. Representative projects are as follows:

(10) Metaverse

The metaverse refers to a collective virtual shared space, which is a crucial infrastructure component of the consumer-grade crypto field. In this digital environment, users can interact with digital assets and decentralized applications in a more immersive way. Metaverse platforms provide consumers with a user-friendly and intuitive interface to access and interact with various on-chain products and services. Metaverse platforms can enable a wide range of consumer-grade use cases, creating new opportunities for brands and businesses to engage with consumers. Representative projects are as follows:

(11) Analytics

Web3 advertising and growth analytics platforms play a vital role in the consumer-grade cryptocurrency ecosystem. They provide projects and developers with the necessary tools and analytical insights to attract target audiences. The solutions offered by these platforms assist in user acquisition, advertising, and growth optimization. By aggregating data from various sources and analyzing user behavior across different touchpoints, these platforms enable projects to make data-driven decisions, measure the effectiveness of their marketing efforts, and ultimately drive adoption and growth. Representative projects are as follows:

(12) DePIN

DePIN is an emerging category of crypto networks that utilizes token incentives to deploy location-dependent hardware devices and generate non-fungible consumable resources. These networks play a crucial role in the consumer-grade crypto ecosystem by monetizing unique real-world data assets, supporting various consumer-facing applications and services. Representative projects are as follows:

The report also predicts the development directions of several sub-sectors. For example, decentralized social media platforms will offer customizable content filtering algorithms. The future of the on-chain gaming sector will expand to include different types of games, platforms, and economic models to cater to diverse player preferences. In the media sub-sector, blockchain technology will enable dynamic, interactive media assets, such as artworks or music. In the communications sub-sector, we will see the emergence of more sophisticated, feature-rich communication platforms that leverage the unique properties of blockchain to achieve secure, private, and censorship-resistant communication. In the community and brand engagement sub-sector, a new generation of "digital-physical NFTs" (digi-physical NFTs) platforms will become more immersive and interactive, utilizing advanced technologies to achieve dynamic, deeply perceived interactions between NFTs and the real world.

Additionally, the report explores the potential of some emerging sub-sectors, such as on-chain AI agents and tokenized personal data markets.

Adoption of Crypto by Fortune 100 Companies

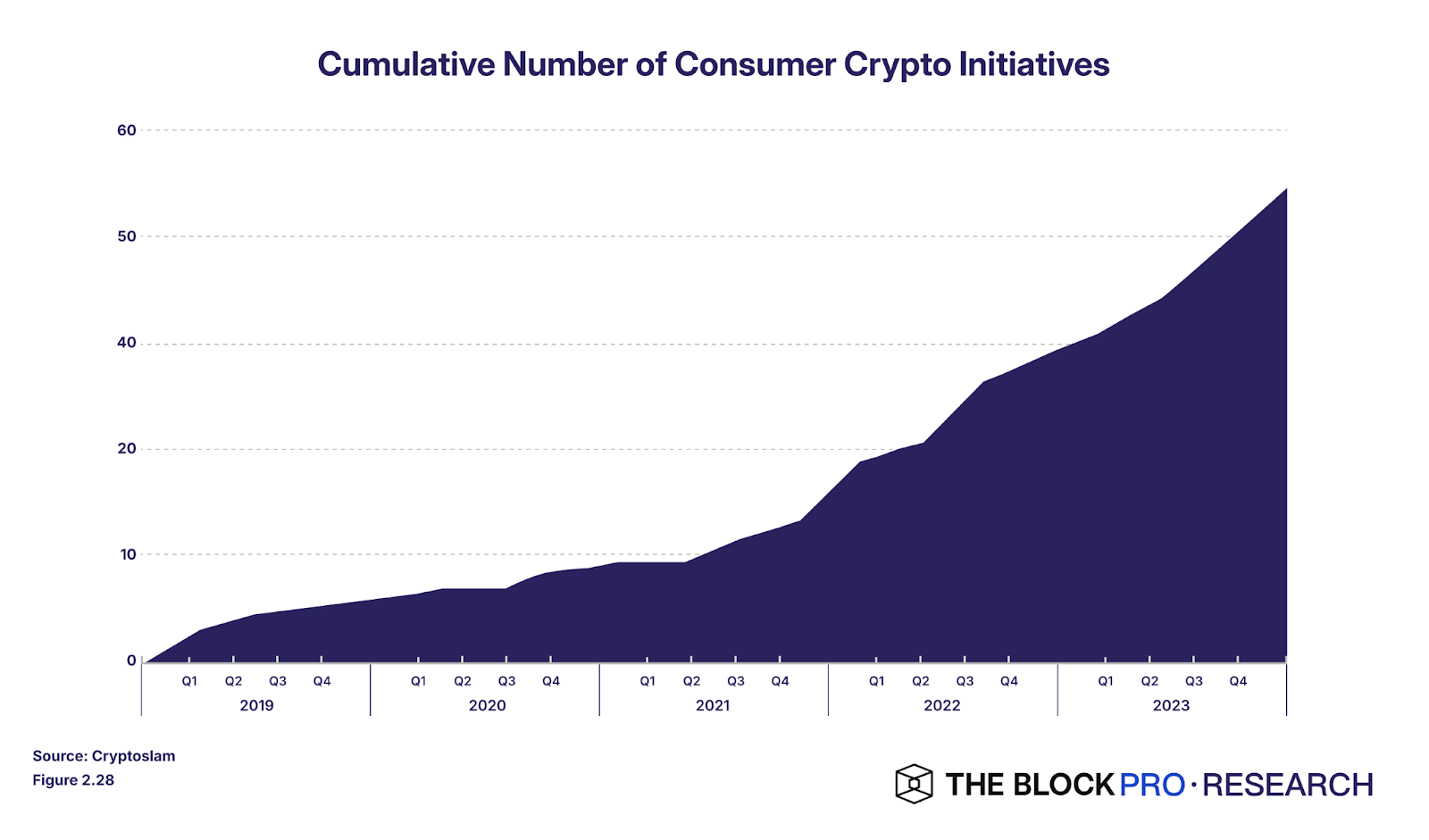

The report also compiles data from Fortune 100 companies to measure the adoption of consumer-grade crypto initiatives among traditional consumer brands.

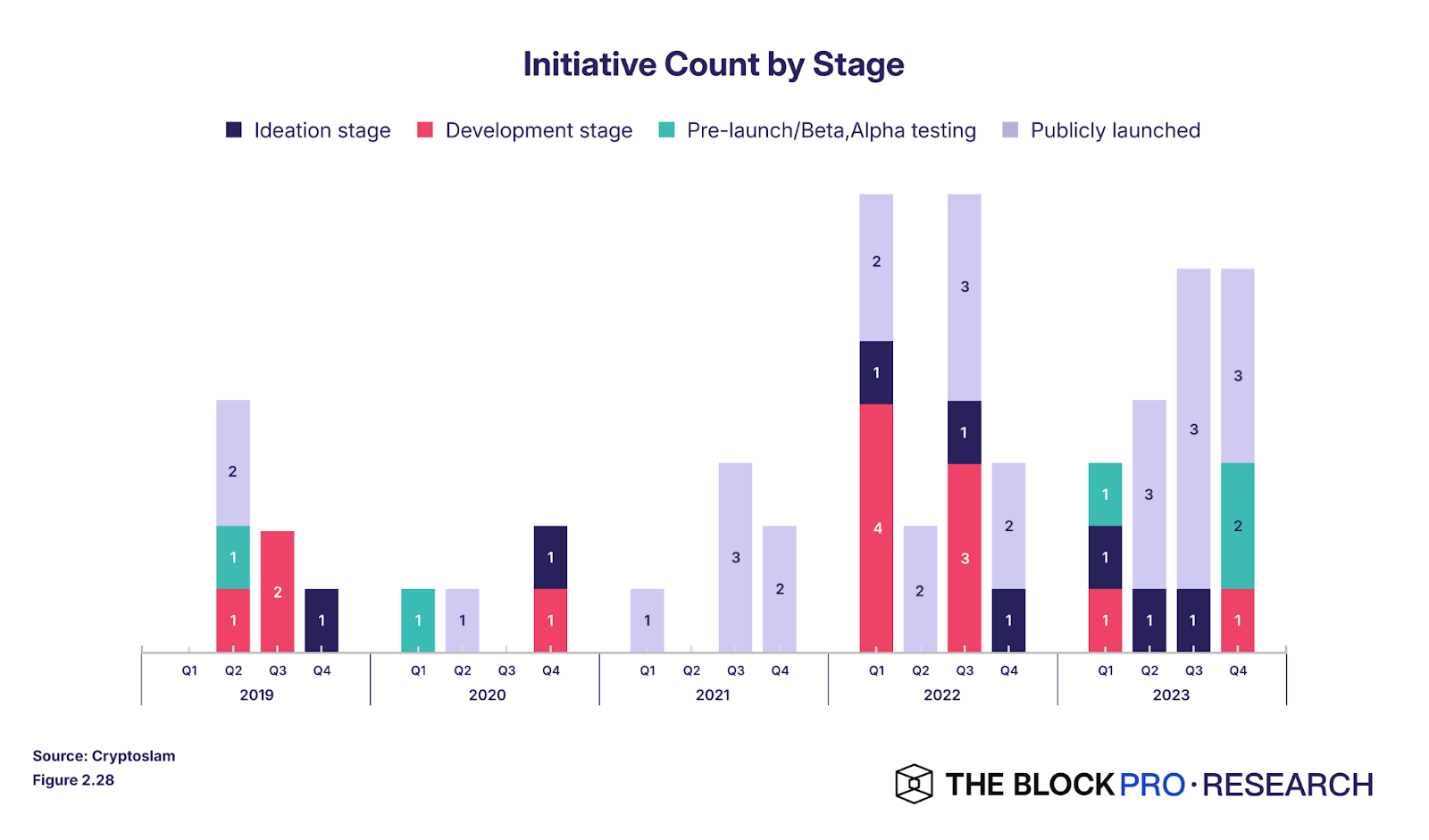

The data shows that nearly one-third of the companies (27 companies) have launched a consumer-grade crypto initiative at some stage. These 27 companies have a total of 55 crypto initiatives from 2019 to 2023. As shown in the chart below, the number of initiatives increased from 7 in 2019 to 19 in both 2022 and 2023, more than doubling the number of initiatives.

If initiatives are categorized into one of four different stages: conception, development, pre-release/testing, and public release to measure maturity, the chart also shows that the maturity of cryptocurrency initiatives has improved from 2019 to 2023. The proportion of initiatives in the conception stage decreased from 43% in 2019 to 37% and 11% in 2022 and 2023, respectively. Meanwhile, the proportion of publicly released initiatives increased from 29% in 2019 to 47% and 58% in 2022 and 2023, respectively. This trend indicates that companies are gradually moving beyond the initial conception stage and actively working on developing and refining their consumer-grade cryptocurrency projects.

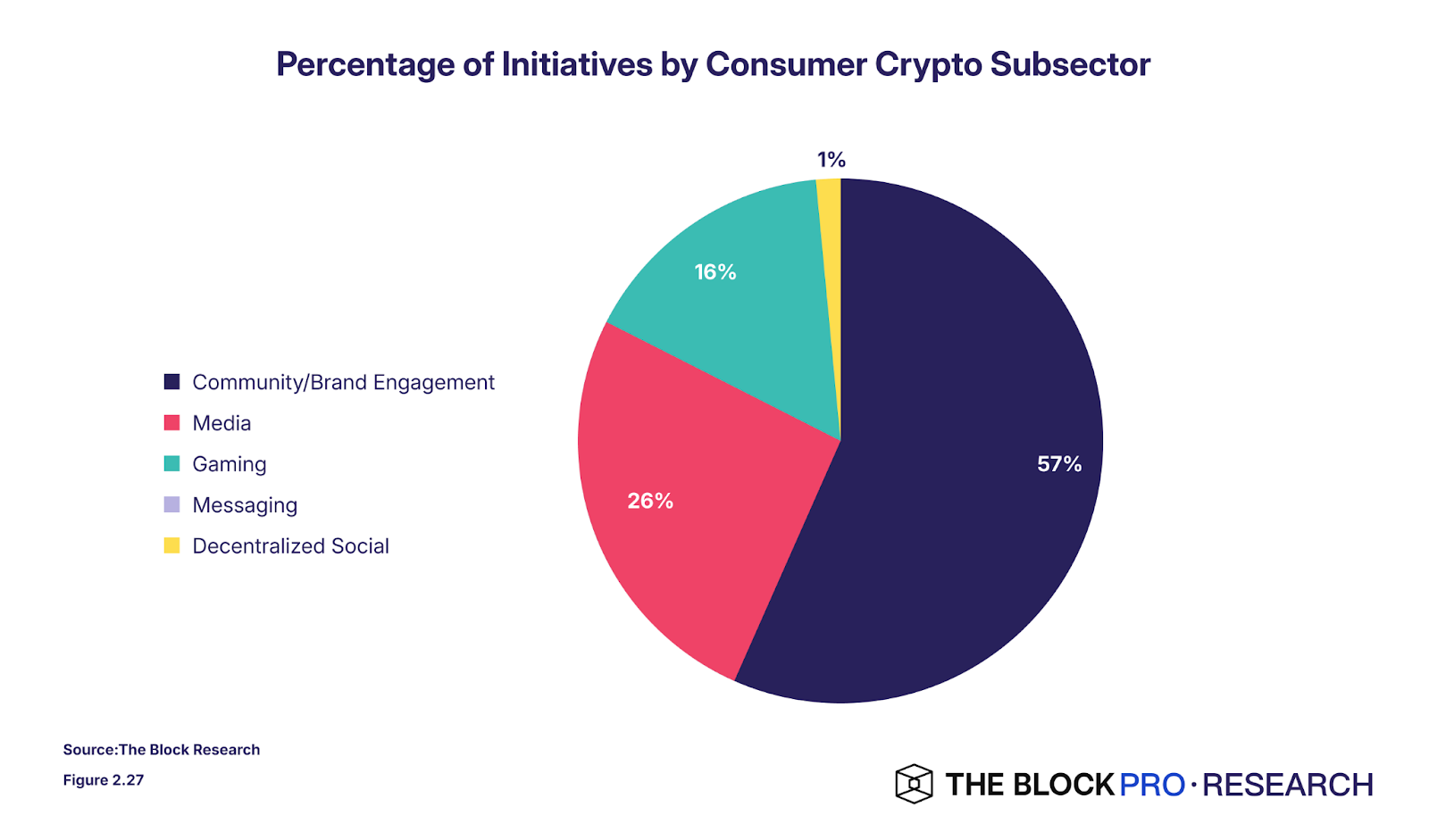

In three key sub-sectors, the concentration of initiatives is very high: community and brand engagement, media, and gaming, which together account for 99% of the initiatives, with specific proportions of 57%, 26%, and 16%, respectively. The main reason is that these sub-sectors help brands establish direct connections with their target audiences, and the applications and tools in these sub-sectors are relatively more mature and popular, with clear characteristics corresponding to traditional markets that traditional consumer brands are already familiar with.

Within different industries in the traditional consumer sector, there are varying levels of penetration for consumer-grade crypto. The technology, retail, and food and beverage industries are clear leaders, collectively accounting for 65% of all initiatives, with specific proportions of 27%, 20%, and 18%; the other six sub-sectors have a more average level of penetration, with each sector's initiatives accounting for less than 10% of the total initiatives.

Barriers to Mainstream Adoption and Regulation

The report points out that the consumer-grade crypto field is still in its early stages and identifies key barriers to mainstream adoption, such as high transaction fees, complex user experiences, negative public perceptions, and regulatory uncertainty, along with corresponding recommendations:

User Experience: On-chain consumer-grade products will need to prioritize the development of user interfaces and experiences; developers need to effectively utilize several key infrastructure components, such as wallet and key management solutions, various abstraction layers and middleware, and interoperable identity solutions.

Public Perception: Reducing the use of crypto jargon to lower cognitive barriers; improving product services to enhance user experience and public perception; increasing transparency of information.

Regulatory Uncertainty: The lack of standardization between different countries and regions further complicates the regulatory landscape for on-chain projects. Legal risks and uncertainties surrounding on-chain products may limit their ability to form partnerships with mainstream brands and enterprises.

The report also explores the regulatory direction for on-chain consumer-grade crypto by analyzing past enforcement actions and their potential impact on the future of consumer-grade crypto products, with a focus on the regulatory status of consumer-grade crypto in major markets in North America, Europe, and Asia (China, Singapore).

Finally, the report summarizes several significant trends and developments in the consumer-grade crypto field:

Mainstream Adoption Potential: Nearly one-third of Fortune 100 companies are developing consumer-grade crypto initiatives, indicating their increasing recognition of the potential of blockchain in consumer applications. Additionally, certain on-chain consumer products are showing signs of product-market fit.

Infrastructure Development: The emergence of user-friendly wallets, efficient payment systems, and robust identity management solutions is laying the groundwork for a more accessible consumer-grade crypto experience.

Regulatory Competition: The diverse global regulatory environment is creating a "natural experiment" for the development of consumer-grade crypto. This divergence may lead to unexpected innovations in less regulated markets, potentially forcing stricter jurisdictions to reconsider their approaches to remain competitive.

Emerging Use Cases: The rise of on-chain AI agents and tokenized personal data markets could fundamentally change how consumers interact with digital services and manage their personal information.

User Experience as a Key Driver: The success of consumer-grade crypto largely depends on its ability to move away from technical complexity and provide users with intuitive, value-added experiences.

Consumer crypto represents a growing field at the intersection of blockchain technology and the consumer space. While this field is still in its early stages of development, it shows potential to reshape how individuals interact and transact in their daily lives. The future of the consumer crypto space is promising.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。