Original Title: 《Dissecting Divergences》

Authors: CryptoVizArt, UkuriaOC, Glassnode

Translation: Ladyfinger, BlockBeats

Editor's Note: In this in-depth analysis, we focus on several key dynamics in the Bitcoin market, from the evolution of technical protocols to macro changes in market structure. Of particular note is the balancing effect of neutral cash and carry trading strategies on buyer momentum, despite the influx of funds from the US spot ETF bringing vitality to the market, leading to a neutralizing effect on price impact. Additionally, the sharp contrast between the decrease in active addresses on the Bitcoin network and the surge in transaction volume prompts thoughtful consideration of the underlying reasons. By dissecting the impact of emerging technologies such as the Runes protocol, we reveal its direct influence on the decrease in active addresses. At the same time, we also observe the significant role played by the amount of Bitcoin held by major entities and Coinbase in shaping the current market landscape.

While the influx of funds from the US ETF is impressive, the neutral basis trading (Cash-and-Carry Trade) in the market seems to be mitigating buyer momentum, and the market needs non-arbitrage demand to further drive price increases. At the same time, we also analyze the significant differences between the decrease in active addresses and the surge in trading volume.

BlockBeats Note: Basis trading, also known as cash-and-carry trade, refers to simultaneously buying (selling) spot bonds and selling (buying) bond futures. The basis trading strategy is based on the price difference of an asset in two different markets (such as the price difference between the spot market and the futures market). If executed properly, it can yield returns. Generally, traders executing the basis trading strategy need to manage two different contracts simultaneously, making the process relatively complex and lengthy.

Abstract

- With the emergence of the Runes protocol, an unexpected divergence has emerged between the decrease in active addresses and the increase in transaction volume.

- Currently, major marked entities hold an astonishing 4.23 million BTC, accounting for over 27% of the adjusted supply, while the US spot ETF now holds a balance of 862,000 BTC.

- The basis trading structure seems to be a significant source of ETF inflow demand, with ETFs being used as a tool to obtain long spot exposure, while the net short positions of Bitcoin accumulate in the CME futures market.

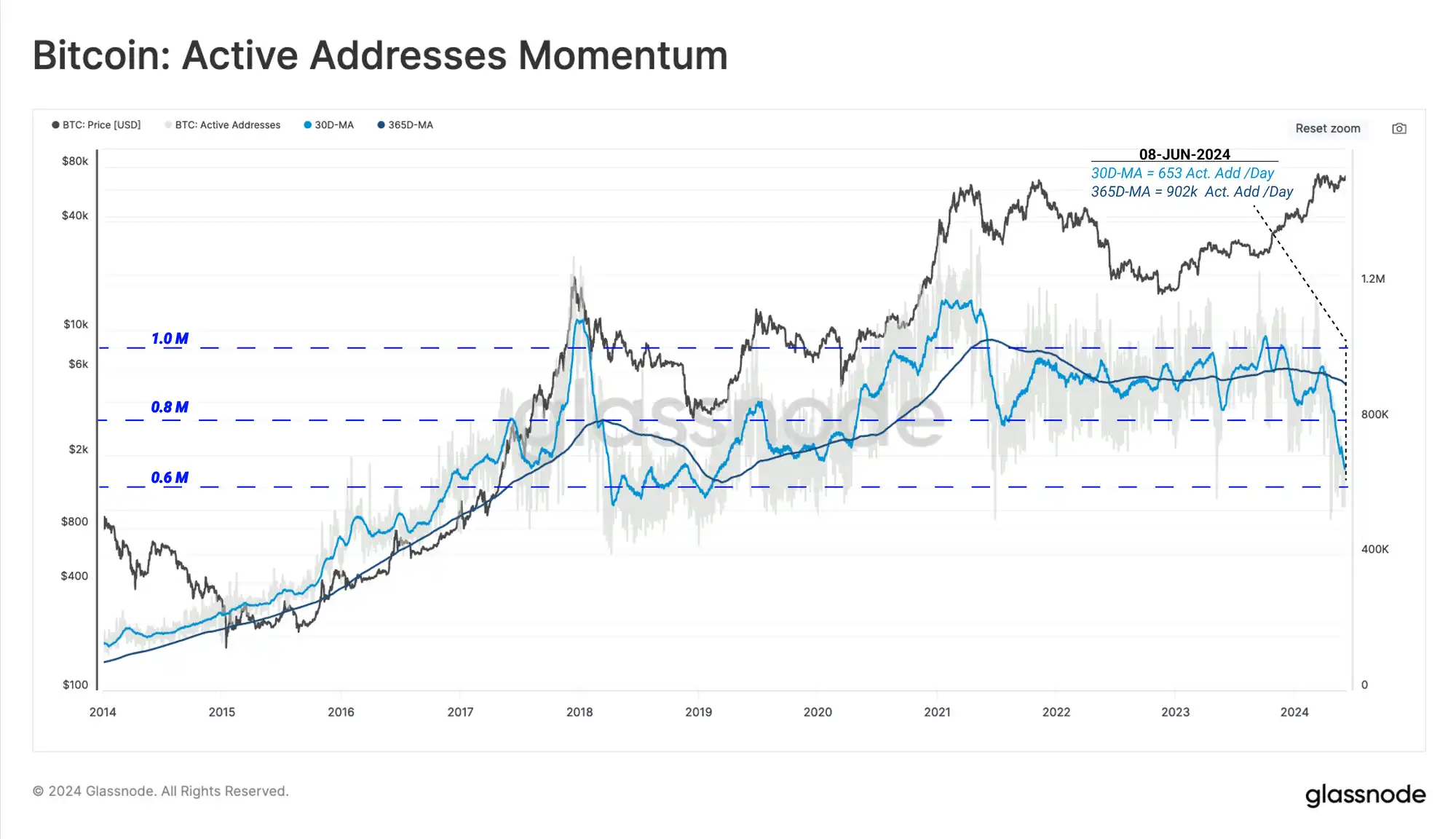

Activity Divergence

On-chain activity indicators, including active addresses, transaction volume, and transaction amount, are crucial tools for evaluating the development and efficiency of blockchain networks. In mid-2021, China imposed restrictions on Bitcoin mining, leading to a sharp decrease in the number of active addresses on the Bitcoin network, with the daily average active addresses dropping from over 1.1 million to just 800,000.

The Bitcoin network is currently experiencing activity contraction, which is fundamentally different from the past. In the following chapters, we will delve into emerging concepts such as inscriptions, ordinals, BRC-20 tokens, and runes, and how they have fundamentally transformed analysts' understanding and predictions of future trends in activity indicators.

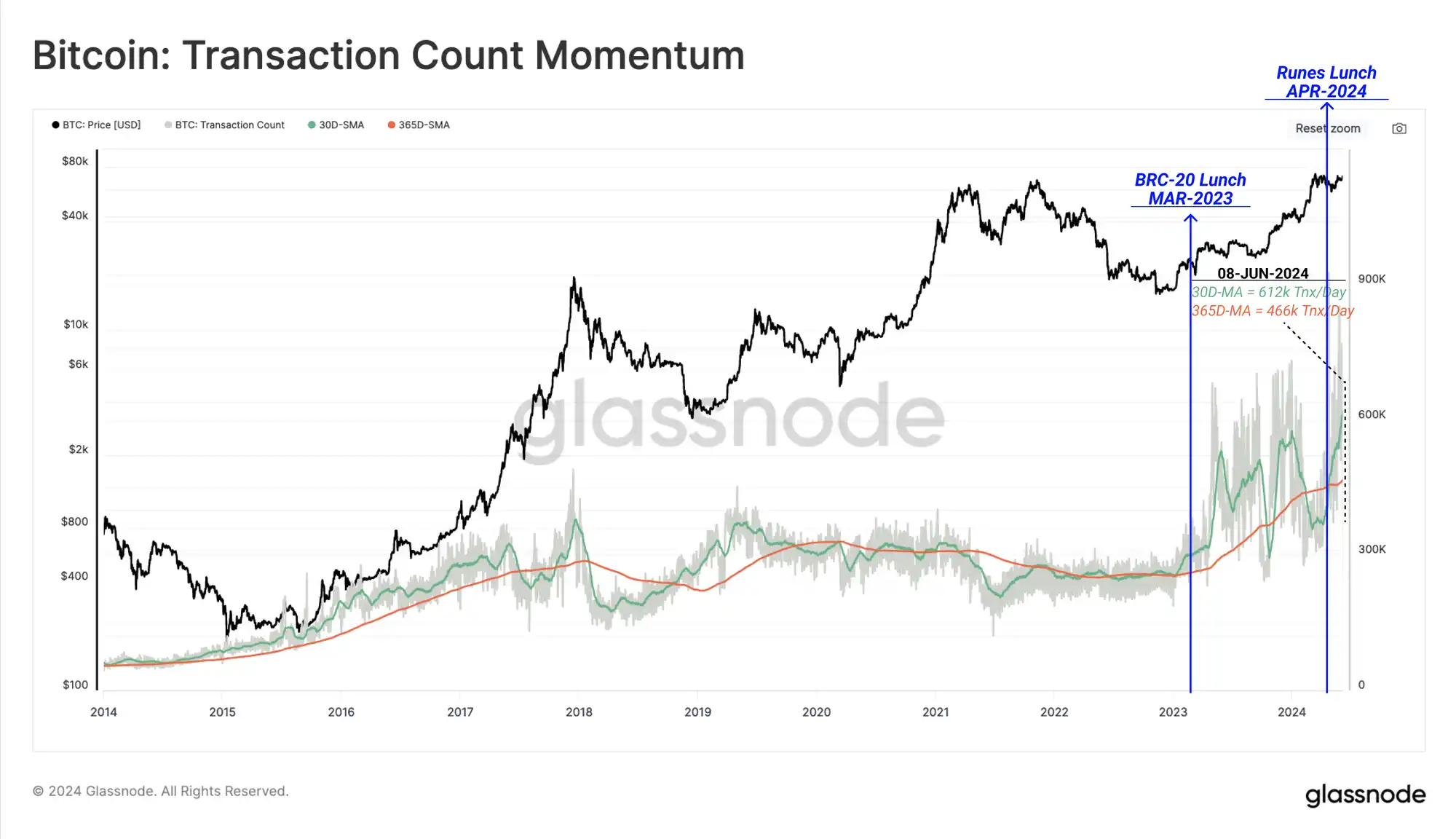

While historically, strong market momentum is usually accompanied by an increase in active addresses and daily transaction volume, this trend is currently deviating.

Despite the apparent decrease in the number of active addresses, the Bitcoin network's transaction processing volume is approaching historical highs. The current monthly average transaction volume has reached 617,000 transactions per day, 31% higher than the annual average, indicating a relatively high demand for Bitcoin block space.

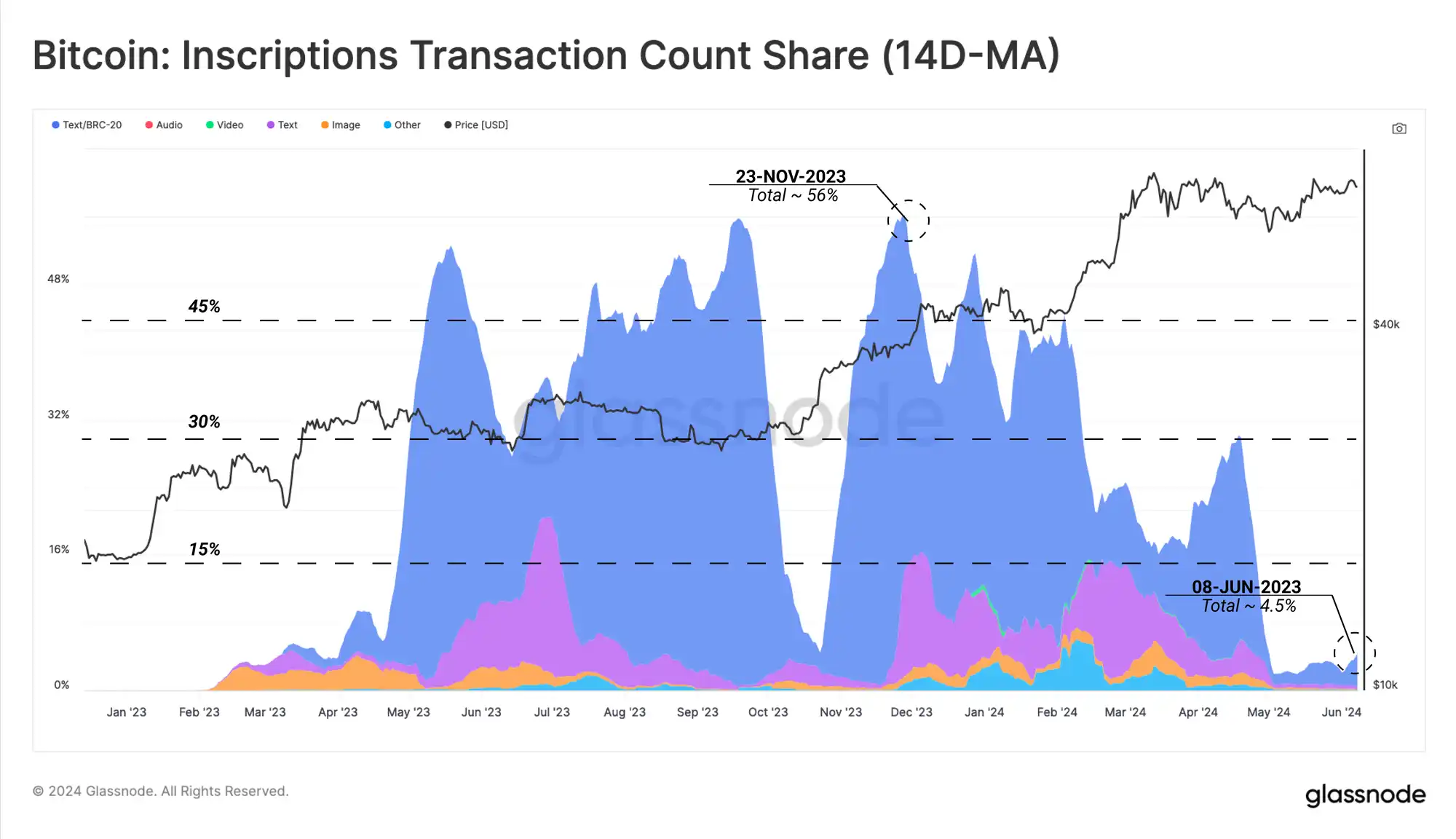

In contrast to the recent decrease in active addresses and the trading share of inscriptions and BRC-20 tokens, we can observe a strong correlation. Of particular note is the sharp decline in the number of inscriptions since mid-April.

This indicates that the decrease in the number of active addresses is mainly due to the reduced use of inscriptions and ordinals. It should be noted that in this field, many wallets and protocols will reuse the same address, and if an address has multiple activities within a day, it will not be counted multiple times. Therefore, even if an address generates ten transactions in a day, it will still only be counted as one active address in the statistics.

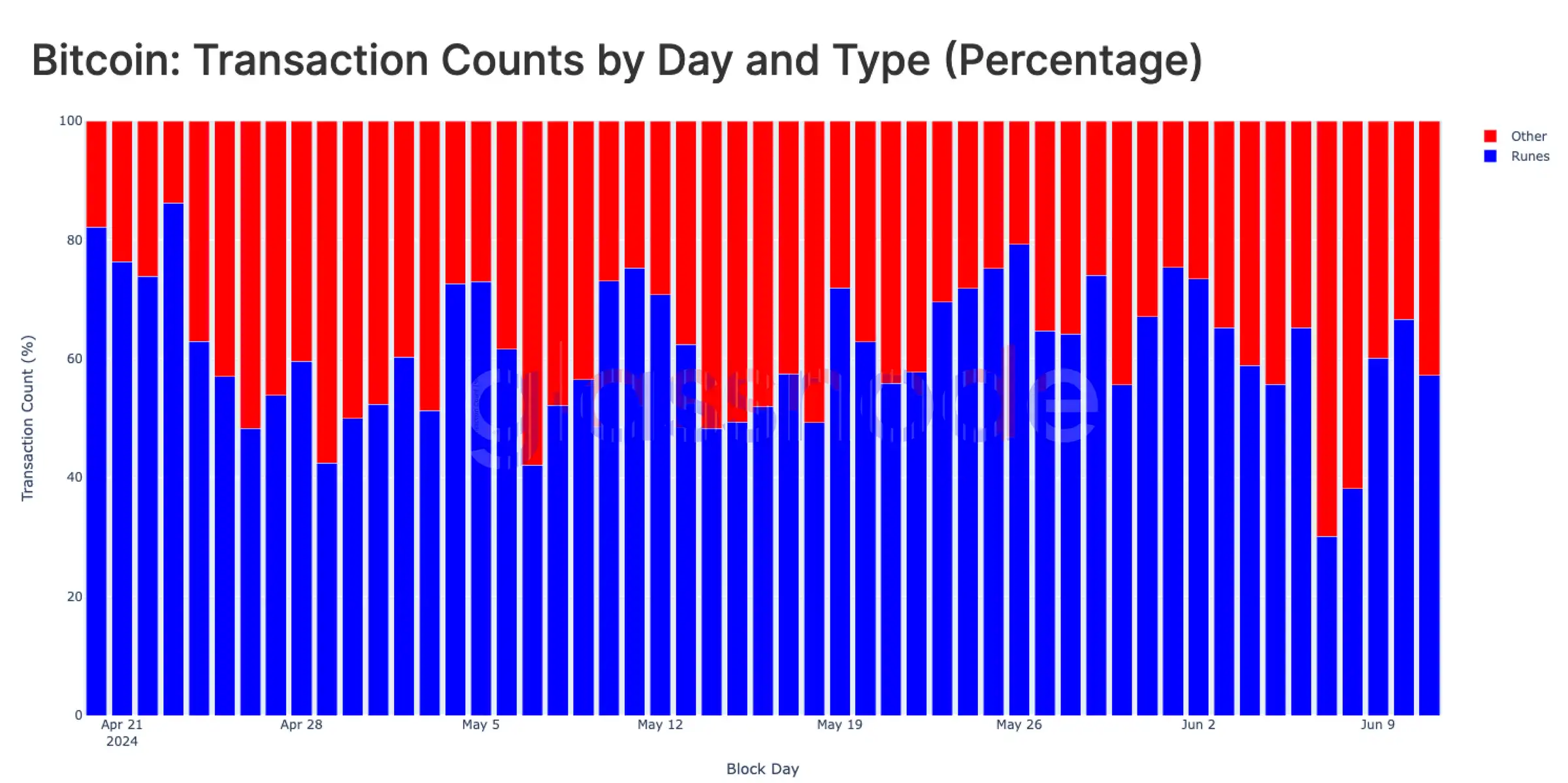

To explain the decrease in inscription activity, we can focus on the emergence of the runes protocol, which claims to introduce a more efficient method for introducing fungible tokens on Bitcoin. The runes protocol went live at the time of the Bitcoin halving, explaining the decline in the number of inscriptions in mid-April.

Runes use a different technical mechanism from inscriptions and BRC-20 tokens, utilizing the OP_RETURN field (80 bytes) to encode arbitrary data on the blockchain, significantly reducing the demand for block space while maintaining data integrity.

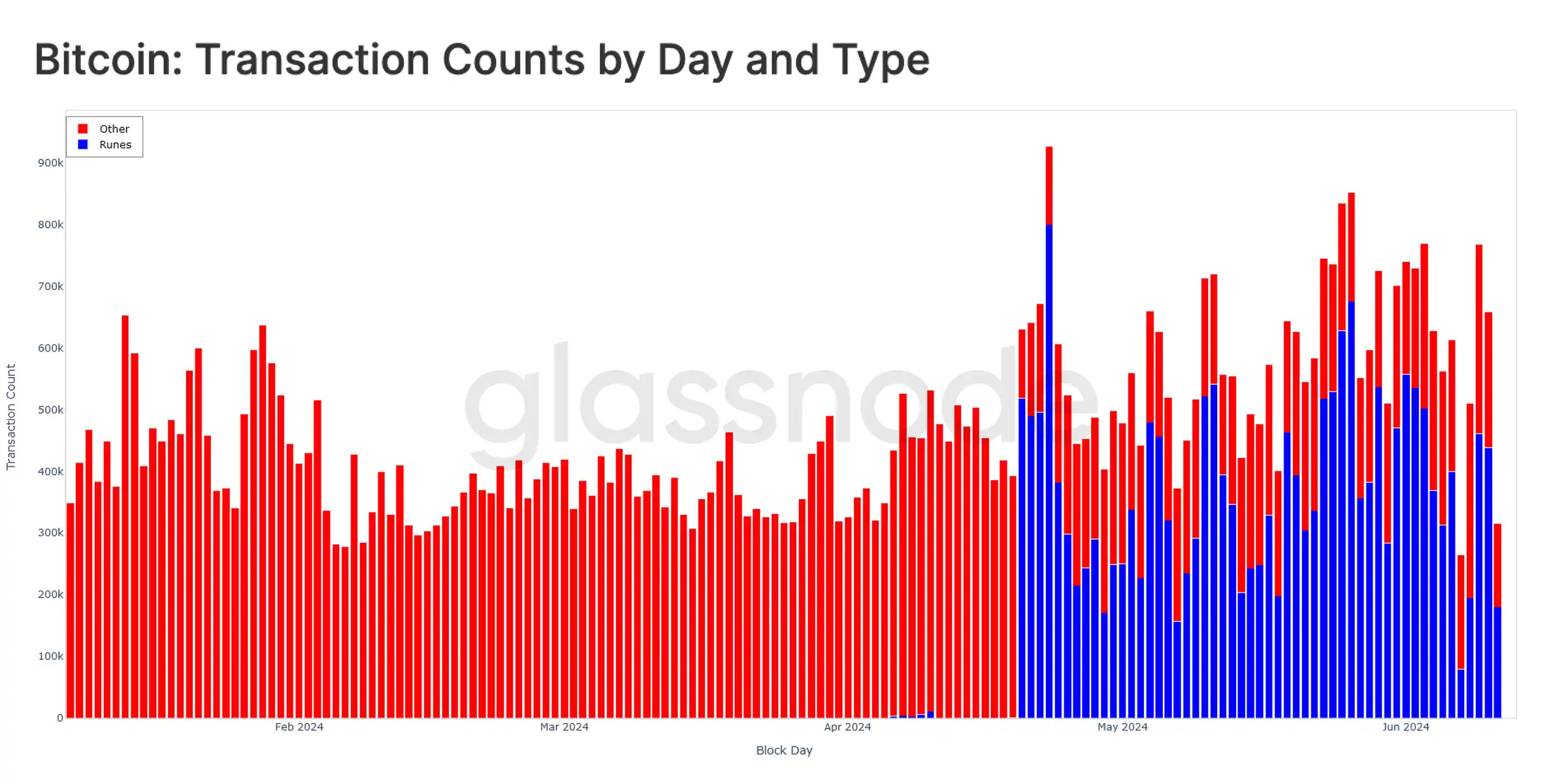

Since its launch at the time of the Bitcoin halving on April 20, 2024, the runes protocol has rapidly gained market traction, with daily trading demand increasing to 600,000 to 800,000 transactions, and this trading volume has remained at a high level.

Image Indicator

Currently, rune-related transactions account for as much as 57.2% of the daily trading volume, significantly surpassing BRC-20 tokens, ordinals, and inscriptions. This phenomenon indicates that user speculative interest may have shifted from inscriptions to the emerging rune market.

Image Indicator

Differences in ETF Demand

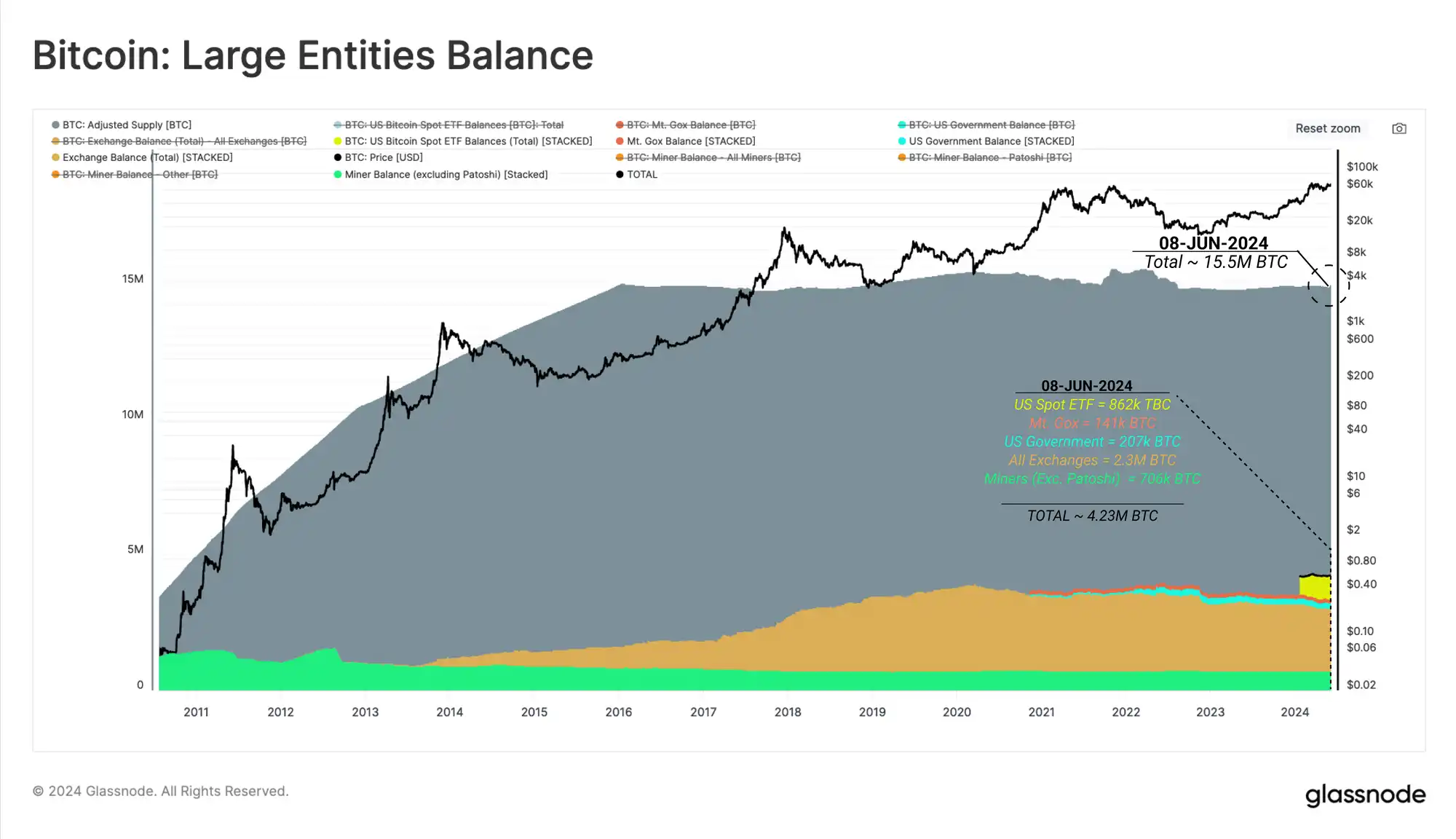

A recent issue of particular market concern is that despite the massive influx of funds from the US spot ETF, prices have shown a stagnant sideways trend. To further analyze and evaluate the demand side of the ETF, we can compare the current holdings of the ETF (862,000 BTC) with the holdings of other major marked entities in the market.

The US spot ETF holds 862,000 BTC, Mt. Gox creditors hold 141,000 BTC, the US government holds 207,000 BTC, all exchanges collectively hold 2.3 million BTC, and miners (excluding Patoshi) hold 706,000 BTC. The total holdings of these major entities amount to approximately 4.23 million BTC, accounting for 27% of the adjusted circulating supply of Bitcoin, which refers to the Bitcoin supply that excludes coins that have not been moved for over seven years.

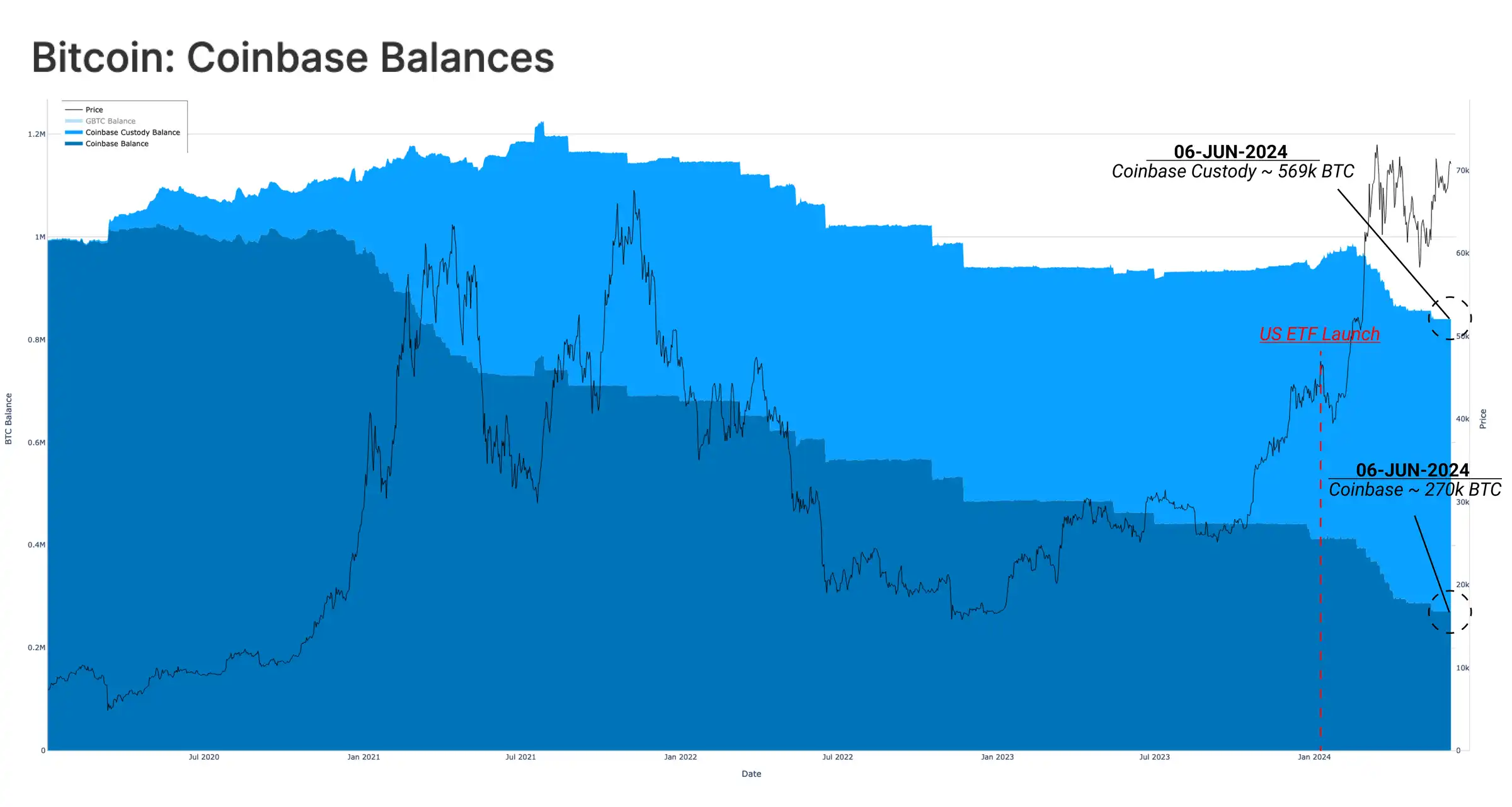

As a leading cryptocurrency platform, Coinbase controls a vast amount of exchange assets, and its custody service also manages the Bitcoin holdings of the US spot ETF. It is estimated that Coinbase Exchange and Coinbase Custody currently hold approximately 270,000 and 5.69 million BTC, respectively.

Image Indicator

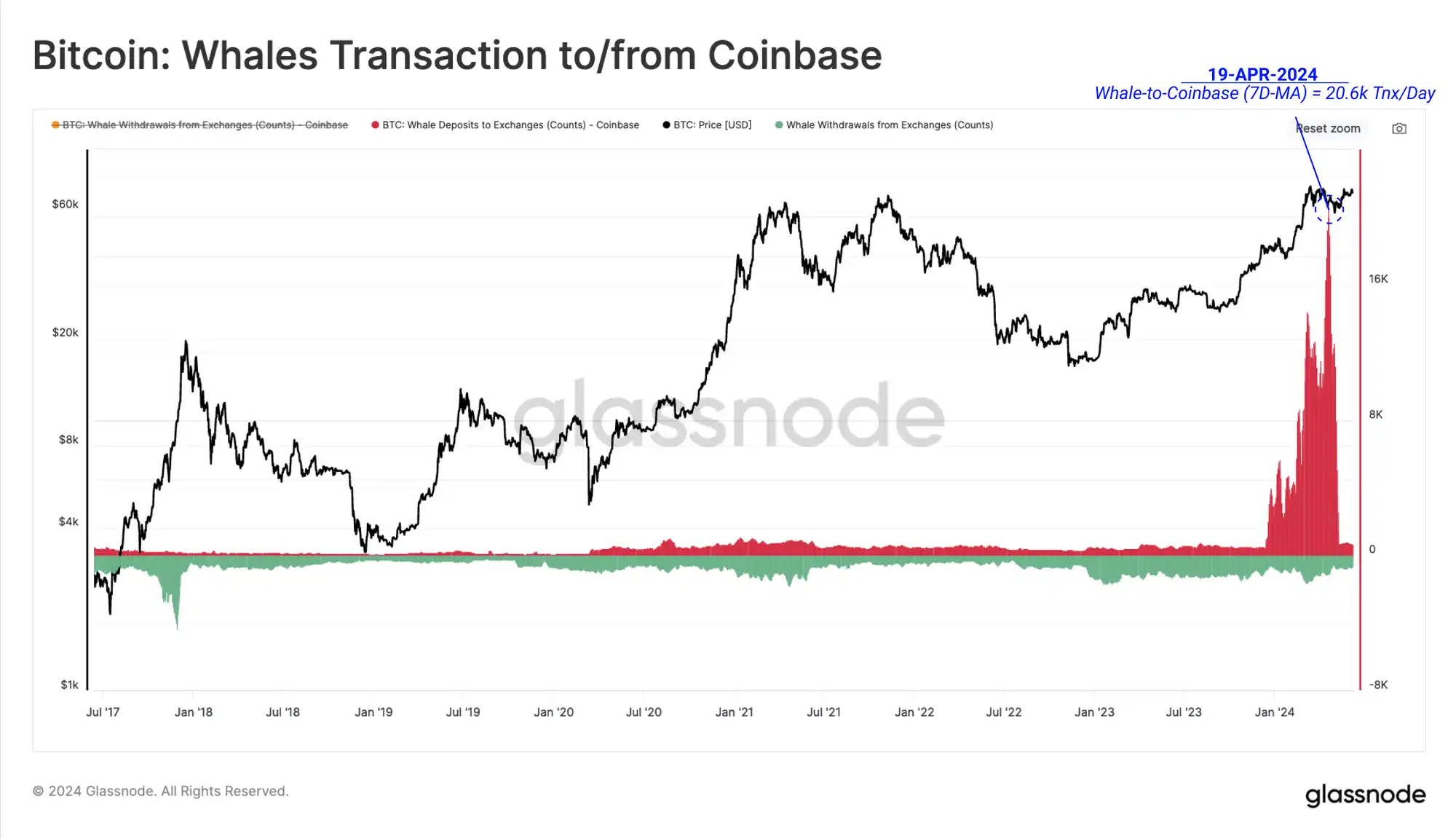

Coinbase's influence on the market price mechanism is increasing due to its service to ETF clients and traditional on-chain asset holders. Observing the dynamics of large deposits into Coinbase Exchange wallets, there has been a significant increase in deposits after the ETF launch.

Most of the deposited Bitcoin is closely related to the continuous outflow of GBTC addresses, which has become a key reason for the year-long Bitcoin supply surplus.

In addition to the selling pressure brought by GBTC in the Bitcoin market reaching historical highs, there has recently been another factor suppressing the demand for the US spot ETF.

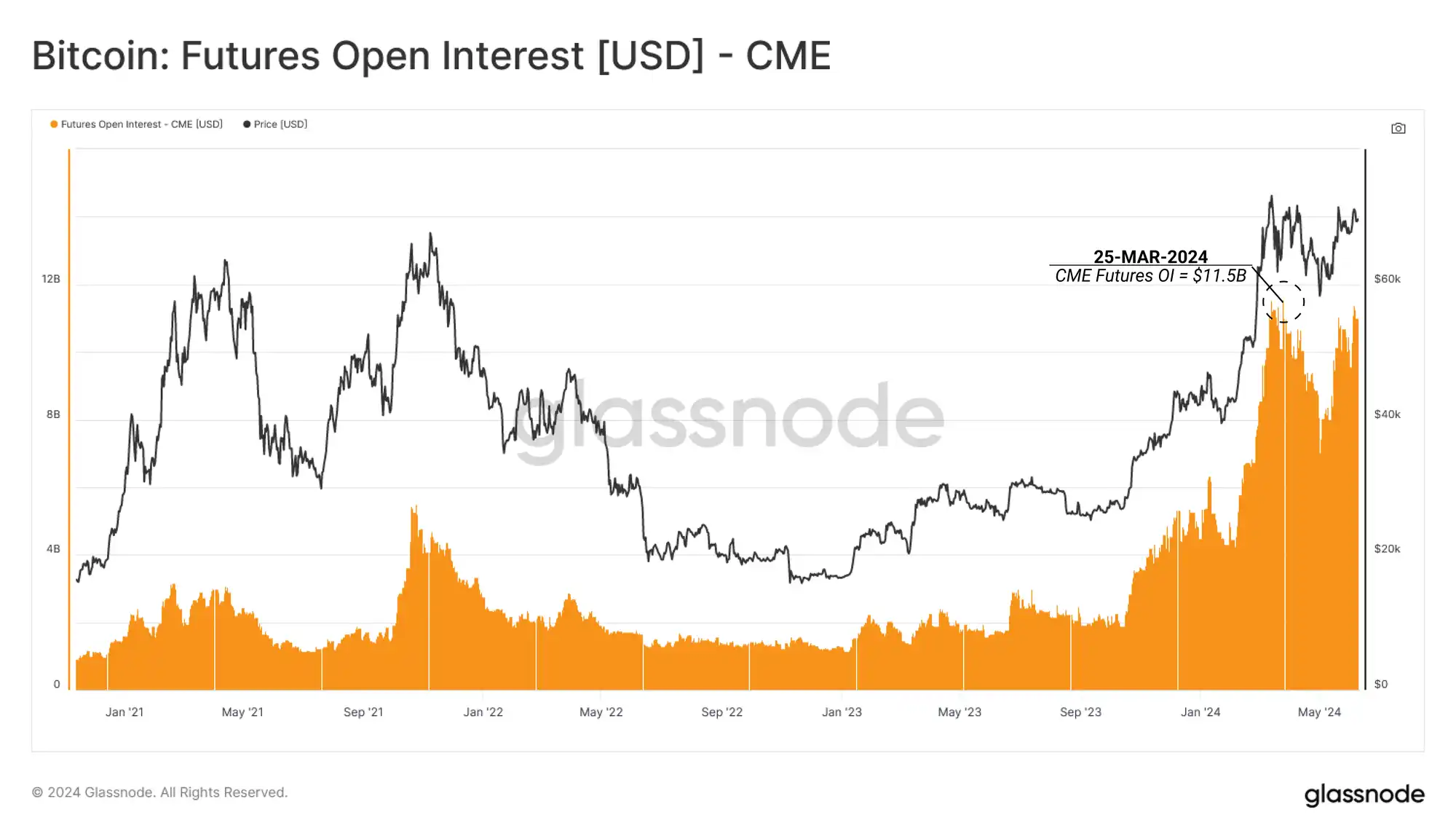

Looking at the CME Group futures market, open interest reached a record high of $11.5 billion in March 2024 and has since remained above $8 billion. This trend may reflect the increasing use of cash and carry arbitrage strategies by traditional market participants.

This arbitrage strategy takes a market-neutral position, involving the simultaneous purchase of long spot positions and the sale (shorting) of futures contracts for the same asset, which becomes the subject of the trade due to the existence of a premium.

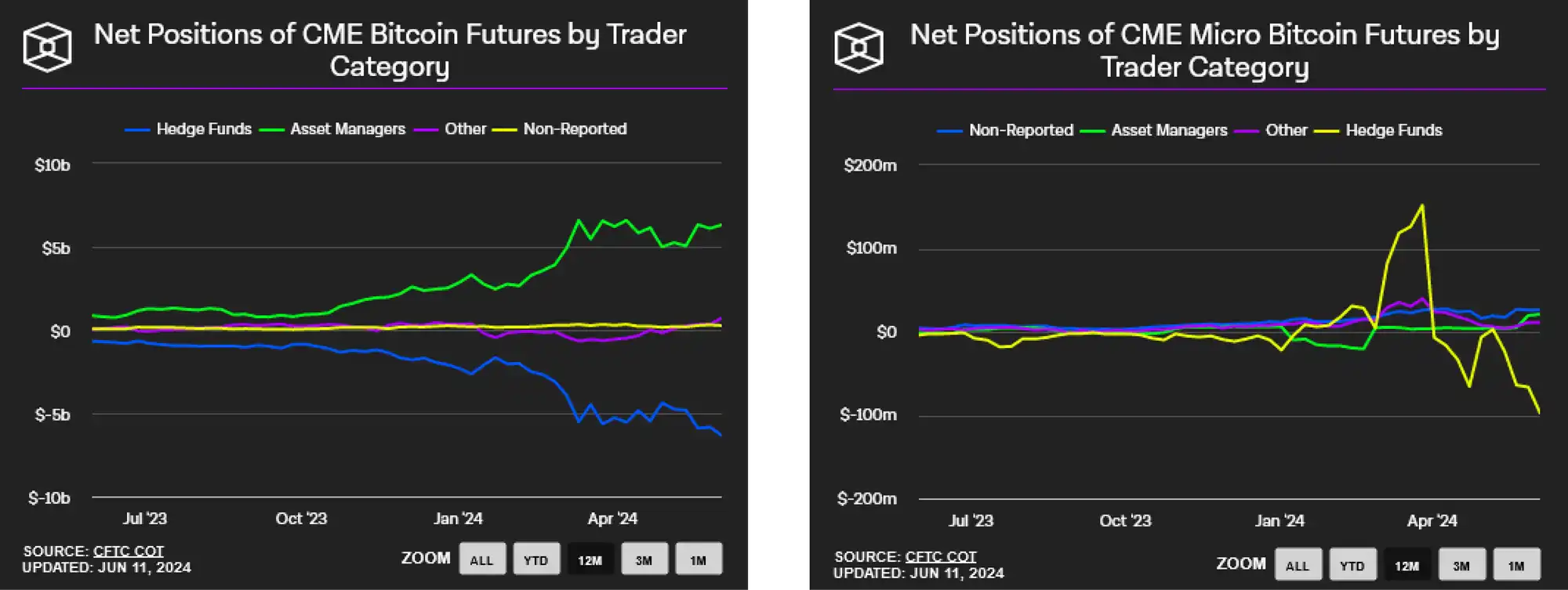

Observations show that investors classified as hedge funds are building increasingly large net short positions in Bitcoin.

This indicates that the basis trading structure may be a key driver of ETF fund inflows, using ETFs as a means to obtain long-term spot Bitcoin. Since 2023, the CME Group exchange has seen significant growth in open interest and market leadership, revealing itself as the preferred platform for hedge funds to short futures.

Currently, hedge funds hold a net short position of $6.33 billion in Bitcoin futures on the CME market, and a net short position of $97 million in micro CME Bitcoin futures.

Summary

The popularity of the runes protocol significantly exacerbates the divergence between activity indicators, as this protocol allows for multiple transactions from a single address through address reuse. Meanwhile, the cash and carry arbitrage behavior between the US spot ETF product and futures shorting trades conducted through the CME Group exchange effectively counteracts the inflow of ETF funds. This market phenomenon neutralizes the impact on prices, implying the market needs non-arbitrage natural buying pressure (i.e., real buyers) to drive price increases.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。