Original | Odaily Planet Daily

Author | Nan Zhi

The Ponzi scheme is a financial fraud method that promises high returns to investors to attract funds, but does not have a genuine external investment profit method. Instead, it uses the funds from later investors to pay the returns to earlier investors.

Axie Infinity triggered the GameFi craze in 2021, and various GameFi with "return on investment in N days" continued to emerge. In the third quarter of 2021, several GameFi appeared, allowing a group of users to quickly get rich, but also causing heavy losses to the users who entered the market last. The underlying economic models of these GameFi all belong to the Ponzi scheme.

Therefore, at the end of 2021, some people proposed that GameFi and blockchain games should be distinguished. The former is a (Ponzi) DeFi model with a game shell, while the latter is a game that introduces blockchain technology, focusing on different subjects.

In this article, Odaily Planet Daily will dissect the Ponzi economic models of some mainstream GameFi from 2021 to 2022, showing readers the details of the entire lifecycle of the bubble generation, regulation, and termination, and also serving as a reference for the current GameFi economic sector.

Participant and Process Deconstruction, Key Definitions

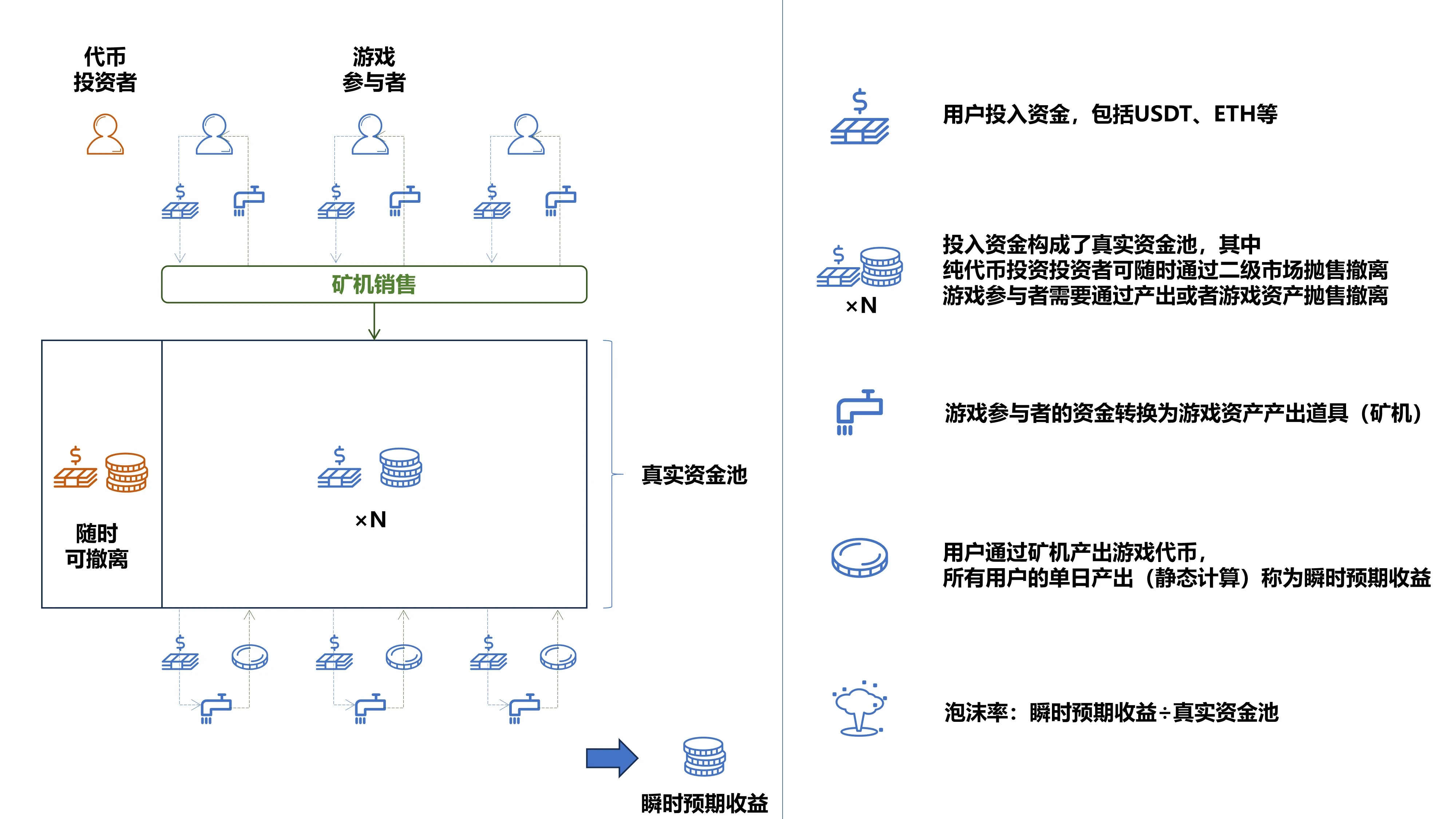

The participants in the lifecycle of a GameFi are as follows:

Game participants: Users who invest assets in the GameFi economy, earning tokens through game props;

Token investors: Purchase project tokens but do not participate in the GameFi economy, earning profits through secondary sales;

Project party: Responsible for the operation of the GameFi economy. They profit through entry and exit taxes, transaction market taxes, and their main responsibilities include attracting new users to join and controlling the pace of entry; controlling the intensity of user sales; and eliminating a certain amount of bubbles as much as possible.

The process of the GameFi economy is simplified as follows:

Users invest funds to purchase game assets to produce props (mining machines);

Users produce game assets through mining machines, which can be reinvested in the game or exchanged for stablecoins (such as USDT). The daily output of all users is recorded as instant expected earnings;

The funds invested by users minus the transferred funds constitute the real fund pool;

The ratio of instant expected earnings to the real fund pool is recorded as the bubble rate, measuring the degree of bubble development in the Ponzi economic system. As players continue to enter, the number of mining machines continues to increase, and the real fund pool continues to shrink, causing the value to increase, bringing the collapse closer;

Finally, under multiple factors such as lack of confidence: a decrease in reinvestment users, most users turning to withdraw funds from the fund pool; insufficient funds: the rate of entry users is insufficient compared to the mining machine output rate; fund loss: due to various mechanisms, entry funds do not enter the real fund pool, causing the economy to become fragile; excessive bubble: the bubble rate is too high to support, the bubble bursts, and the economy collapses.

Other key definitions are as follows:

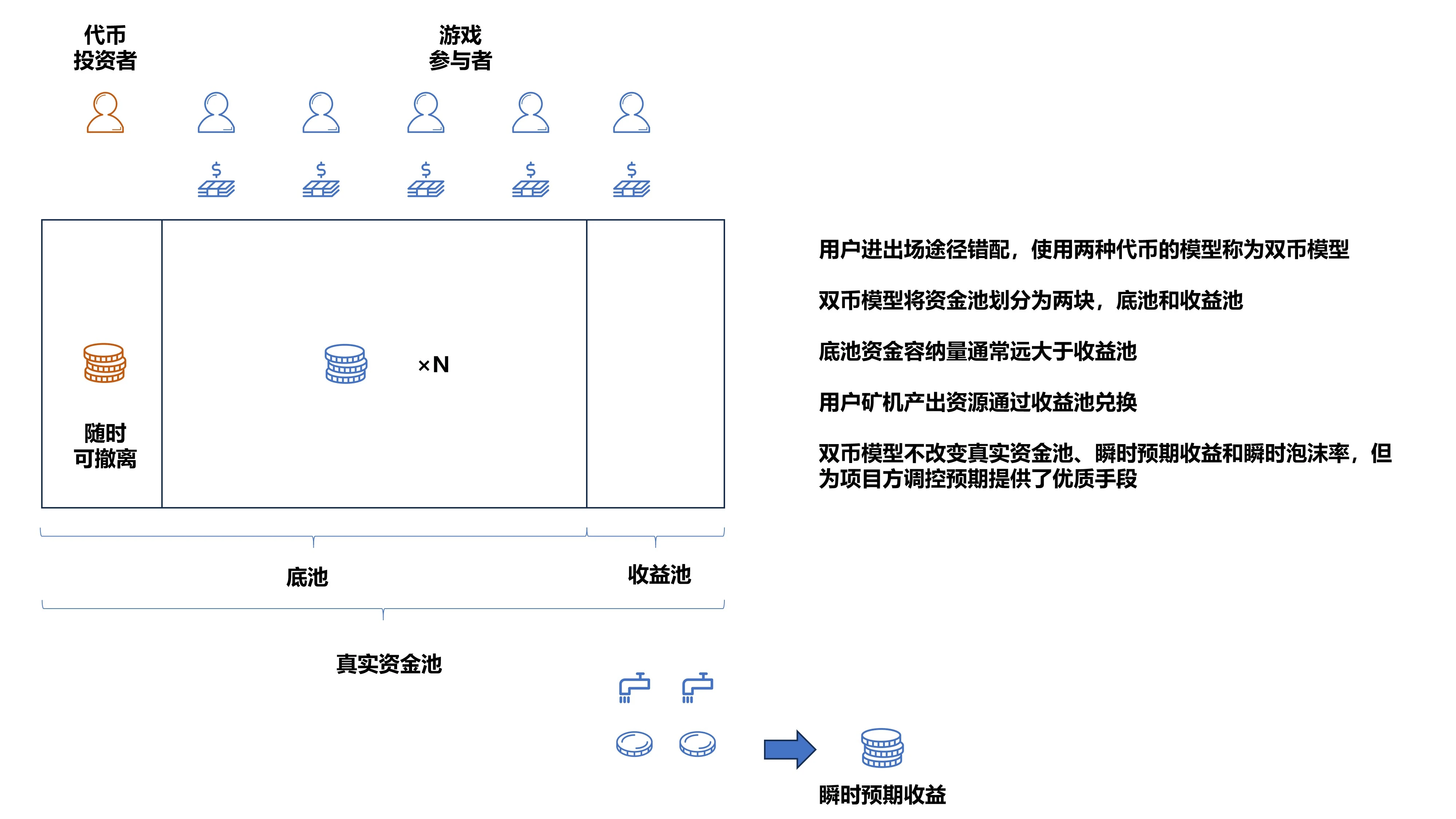

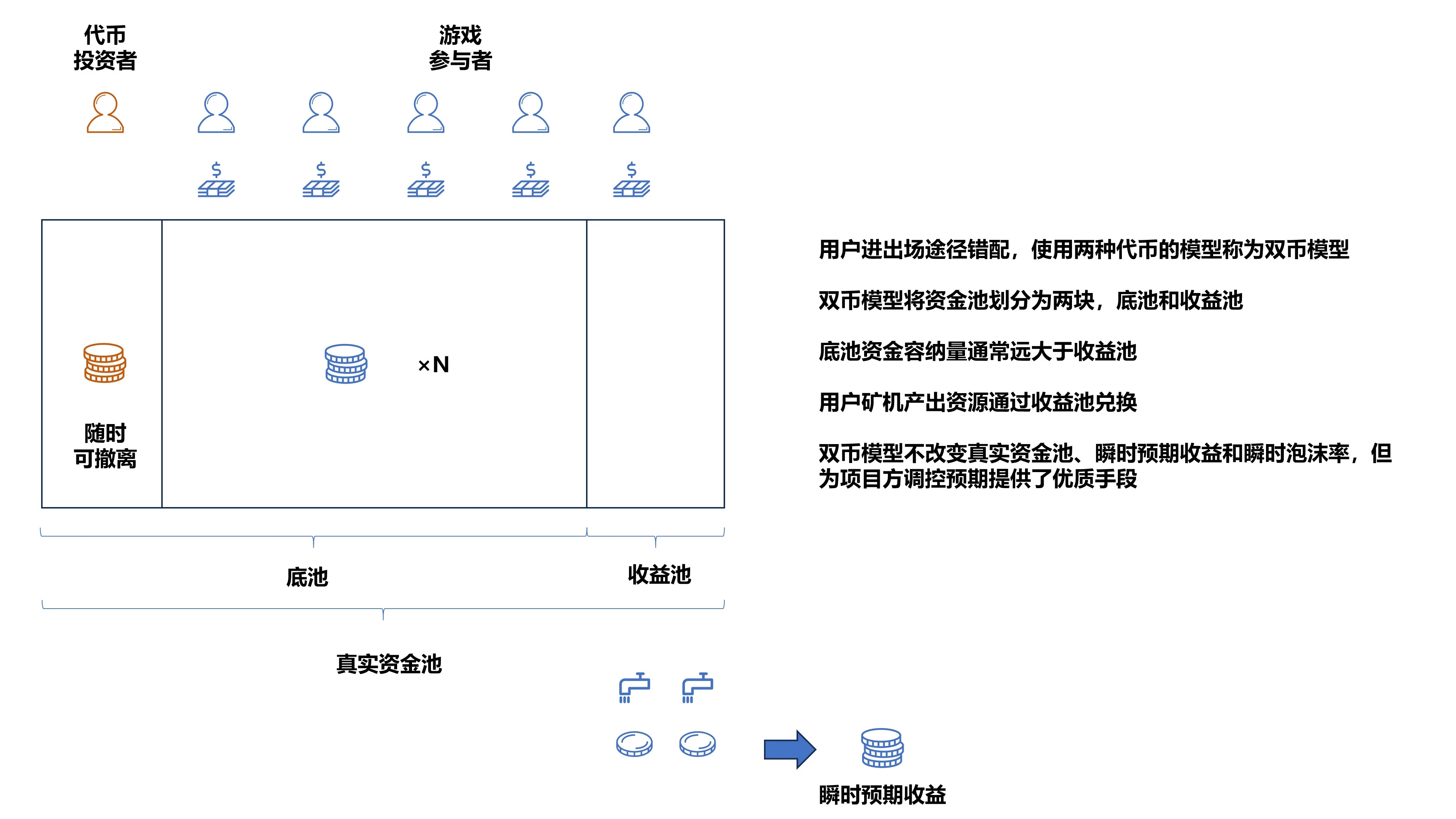

Dual-token model: The mismatch between the entry and exit paths of funds, using two types of tokens is called a dual-token model. There are governance tokens and game tokens, but governance tokens that do not participate in the economic cycle do not belong to the dual-token model.

Single-token model: Funds enter and exit using only one type of token.

Token-based: The user's output is a specific quantity of game tokens.

USDT-based: Also known as gold-based, the user's output is a specific quantity of stablecoins, which does not fluctuate with the game token.

Gacha model: As long as you have enough specific assets, you can obtain mining machines indefinitely.

Breeding model: Mining machines produce new ones through existing mining machines, usually with a quantity limit and increasing breeding costs.

Basic Model: Single-token + Token-based Model + Gacha

First, let's start with the purest single-token + token-based model + gacha. CryptoZoon went live on July 28, 2021, with the game token being ZOON. Players need to spend ZOON to purchase Eggs, then hatch ZOAN mining machines, and the mining machines then produce ZOON tokens.

The model and operation process are very simple, and the basic structure applied is shown on the left side of the following figure, with the GameFi shell applied as shown on the right side.

Key Reasons for the Burst of the Bubble

At the beginning, it was mentioned that the four major factors for the burst of the bubble are: lack of confidence, insufficient funds, fund loss, and excessive bubble. What were the main reasons for the collapse of CryptoZoon? The main reason was the excessive bubble, problems in the project's design, and a small part due to certain fund loss.

Excessive bubble: CryptoZoon's mining machine sales model is a gacha model, which means that users can enter quickly. As the first batch of GameFi on BSC after Axie's popularity, the rapid sale of mining machines led to the rapid peak of instant expected earnings and bubble rate.

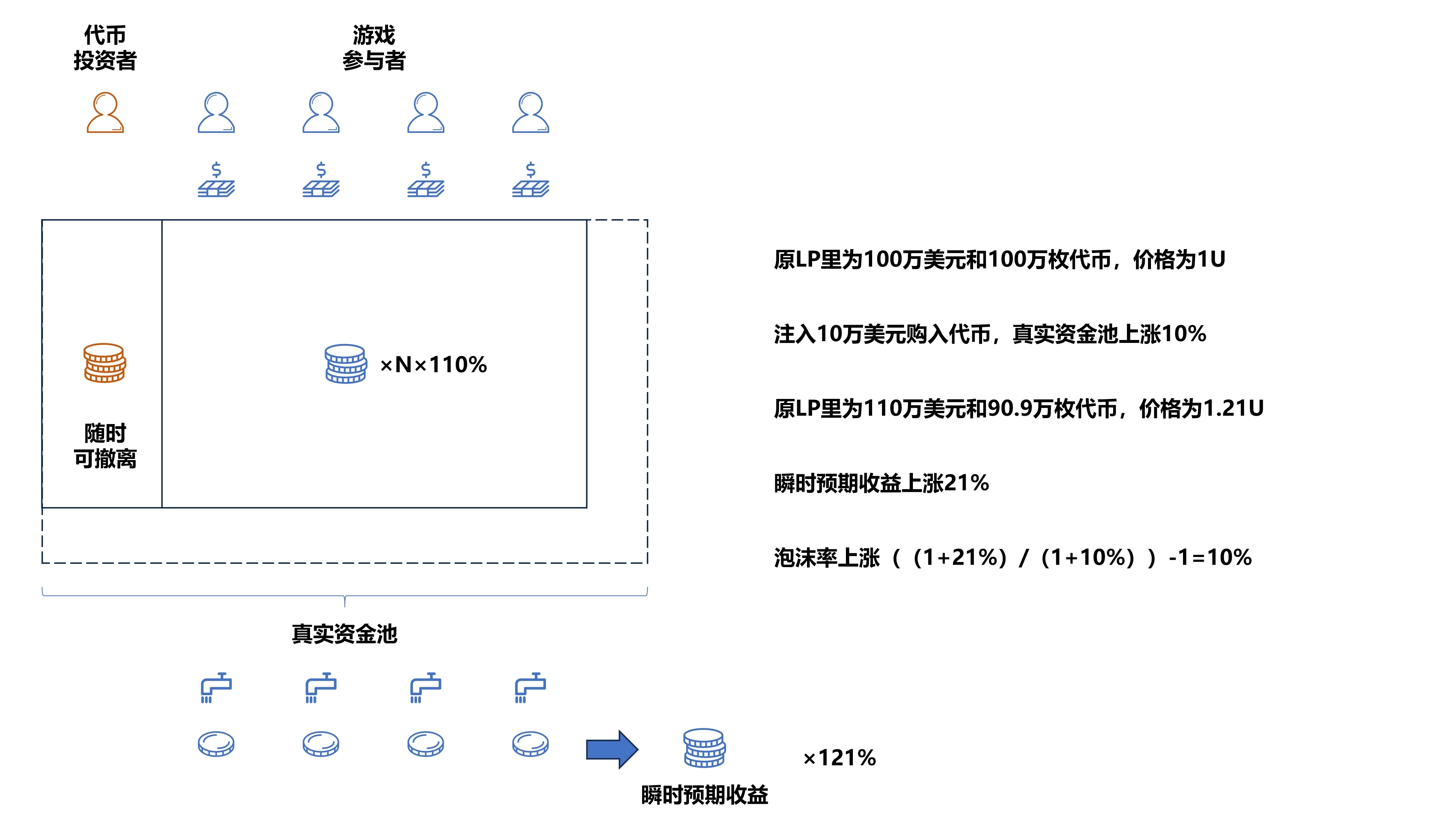

Here, let's first consider a question: in a static situation without considering the exit of token investors and game output, what is the relationship between fund entry and bubble rate?

Due to the AMM mechanism, the token price is squared with the inflow of funds. If the fund pool increases by 10%, the token price increases by 21%;

For static calculations, the user's instant expected earnings also have a squared relationship with the fund pool, also rising by 21%;

The bubble rate correspondingly increases, linearly related to the entry funds.

In summary, in a static situation, the more funds that flow in, the higher the bubble rate. Why is this? Because it assumes that the mining machines can extract real funds from the inflated prices (the more cashed out, the larger the bubble). What are the actual differences?

After the token rises, token investors tend to sell for profit, shrinking the real fund pool. However, it is worth noting that under the single-token model, the impact is usually not too significant;

The selling of tokens by token investors and game participants will affect the AMM price curve, and the rate of inflation of actual instant expected earnings will not grow quadratically.

In short, because of the AMM curve, profit sales, and the entry of funds, the bubble rate increases.

Fund loss: The following chart shows the price trend of the game token ZOON, with the closing price one hour after the token went live as the baseline, with the highest increase being about 6.5 times.

In the single-token model, the real fund pool of the token is its LP pool. The steep V-shaped trend means that the funds used to buy tokens to participate in the game during this period were earned by token investors, and did not effectively enter the fund pool to maintain the economy. On the other hand, the CryptoZoon project party set a limit on the sale of mining machines, causing the bubble rate to quickly reach its peak, and funds did not have a channel to flow in significantly, leading to the eventual collapse.

Dual-token Model: Give Me a Lever and I Will Move a Million-dollar Pool

Mismatch of Entry and Exit Paths for User Funds, Using Two Types of Tokens is Called the Dual-token Model. There are governance tokens and game tokens, but governance tokens that do not participate in the economic cycle are not part of the dual-token model. For example, although Axie Infinity has two tokens, the governance token AXS is only minimally consumed in the breeding process, essentially still a single-token model.

The dual-token model has the following characteristics:

BinaryX

BinaryX is the epitome of the dual-token model, with two tokens BNX and GOLD in the game. The economic operation process is as follows:

Users purchase BNX for hero lottery (obtaining mining machines);

Users spend GOLD to upgrade heroes (upgrading to advanced mining machines);

Users stake heroes to produce GOLD (the main output of mining machines, and funds are transferred from the reward pool);

Users use heroes to battle bosses, earning BNX, GOLD, and equipment (the secondary output of mining machines).

BinaryX matches the characteristics of the dual-token model as follows:

Mismatch of entry and exit paths: Users need to purchase both BNX and GOLD, but the main output is GOLD, causing the BNX price to slowly rise in the pool, while GOLD has a smaller upward pressure;

Base pool and reward pool: BNX is the base pool, with a lot of funds and little volatility, while GOLD is the reward pool, much smaller and more volatile;

The dual-token model does not change the real fund pool (BNX+GOLD), instant expected earnings (calculated based on GOLD price), and instant bubble rate, but it provides the project party with effective means of regulation.

What regulatory measures does the dual-token model's characteristics provide for the economic operation of BinaryX?

Small market controls large market

Since users' profit expectations are calculated based on the GOLD price, and the LP pool volume of GOLD is extremely small, about tens of thousands of dollars, only a small amount of funds is needed to adjust user expectations, thereby driving the rise of BNX in the large pool. In a single-token model, it would be difficult to carry out "regulation" operations due to the base pool of over a million dollars.

Secondary speculation

Due to the separation of the dual pools, funds enter through BNX and GOLD, but mainly flow out through GOLD, causing BNX to rise more easily, and the situation of secondary speculation becomes more apparent. In extreme cases, the base pool may have no output, leading to the unilateral rise model of BNBH that appeared later.

At the same time, this also limits the secondary users' speculation on the output of tokens, as the extremely small fund pool can easily lead to an excessive increase in token prices, becoming the profit of game users.

In summary, the dual-token model, with separate base and reward pools, provides effective economic regulation measures for the project party, while intensifying the speculation of the mother token and suppressing the speculation of the child token.

In addition to the inherent characteristics of the dual-token model, BinaryX also introduces a certain degree of randomness, providing potential means of regulation for the game economy:

Controllable mining machine attributes

The mining machines in BinaryX are called heroes, produced by consuming BNX for lottery output, with differences in attributes that greatly affect the output of mining machines. Therefore, by adjusting the probability of mining machine attributes, the outflow rate of funds can be influenced in the long term.

Random dungeons

In BinaryX, users can consume BNX to enter dungeon battles, with outputs including BNX, GOLD, and equipment, with the possibility of high returns in a single battle, but not every battle is profitable. The project party can adjust the overall difficulty and output to achieve a certain bubble elimination.

The dual-token model does not change the Ponzi properties, but it leaves ample means to adjust user expectations. BinaryX operated effectively for about 3 months, making it a long-lived player in the Ponzi GameFi, but ultimately perished due to excessive bubble and insufficient entry funds.

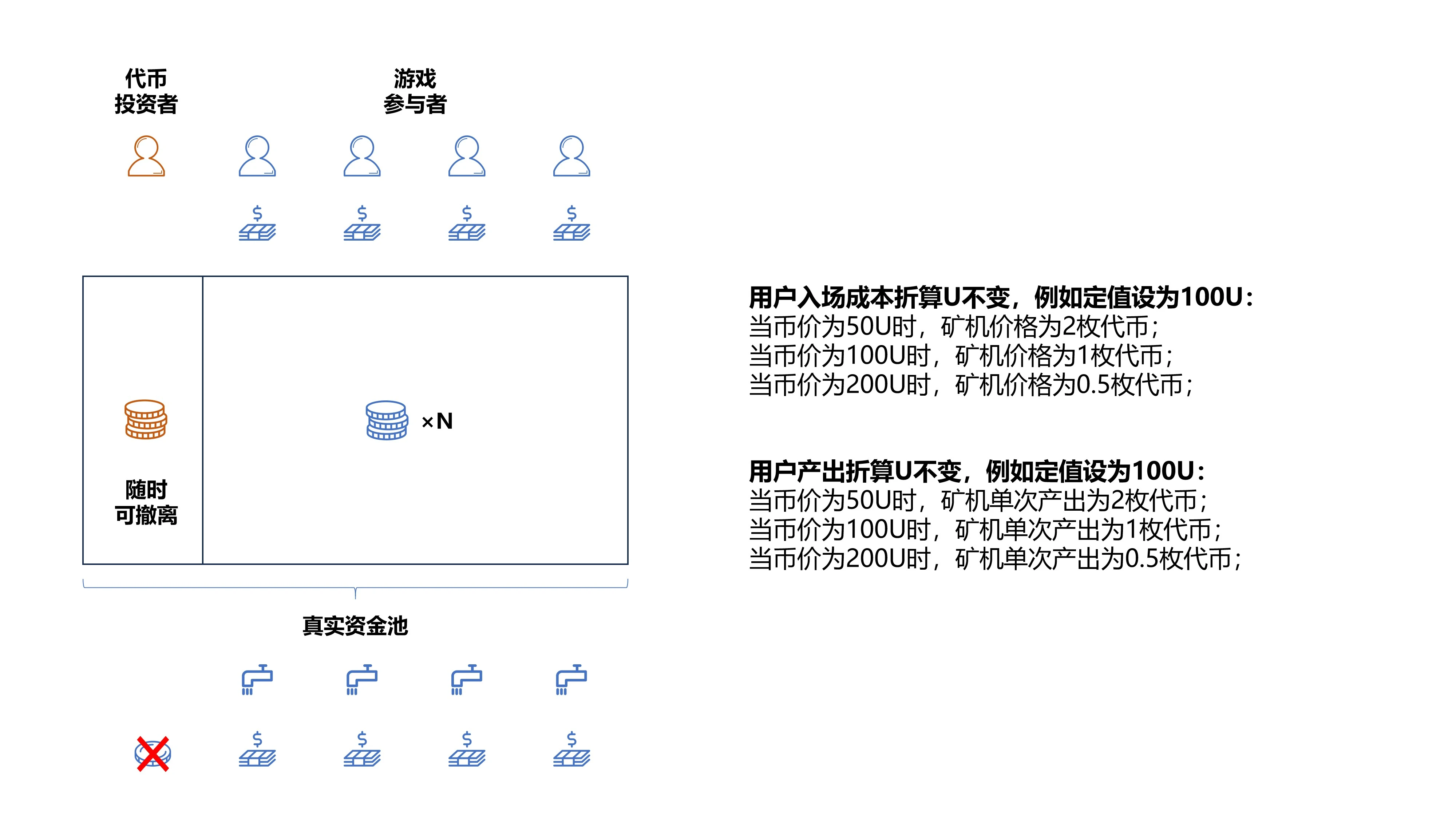

U-based Model: It Only Takes 8.8 Seconds to Jump from the Empire State Building

In addition to the single-token and dual-token models mentioned above, at that time, GameFi also distinguished between token-based and gold-based (U-based) models. In the token-based model, both entry and output are priced in tokens, while the U-based model uses a fixed stablecoin price for calculation. This model can be considered to have been first popularized by Valk (Valkyrie), further developed by CryptoMines (Spaceship), and has become a swan song due to its extreme nature.

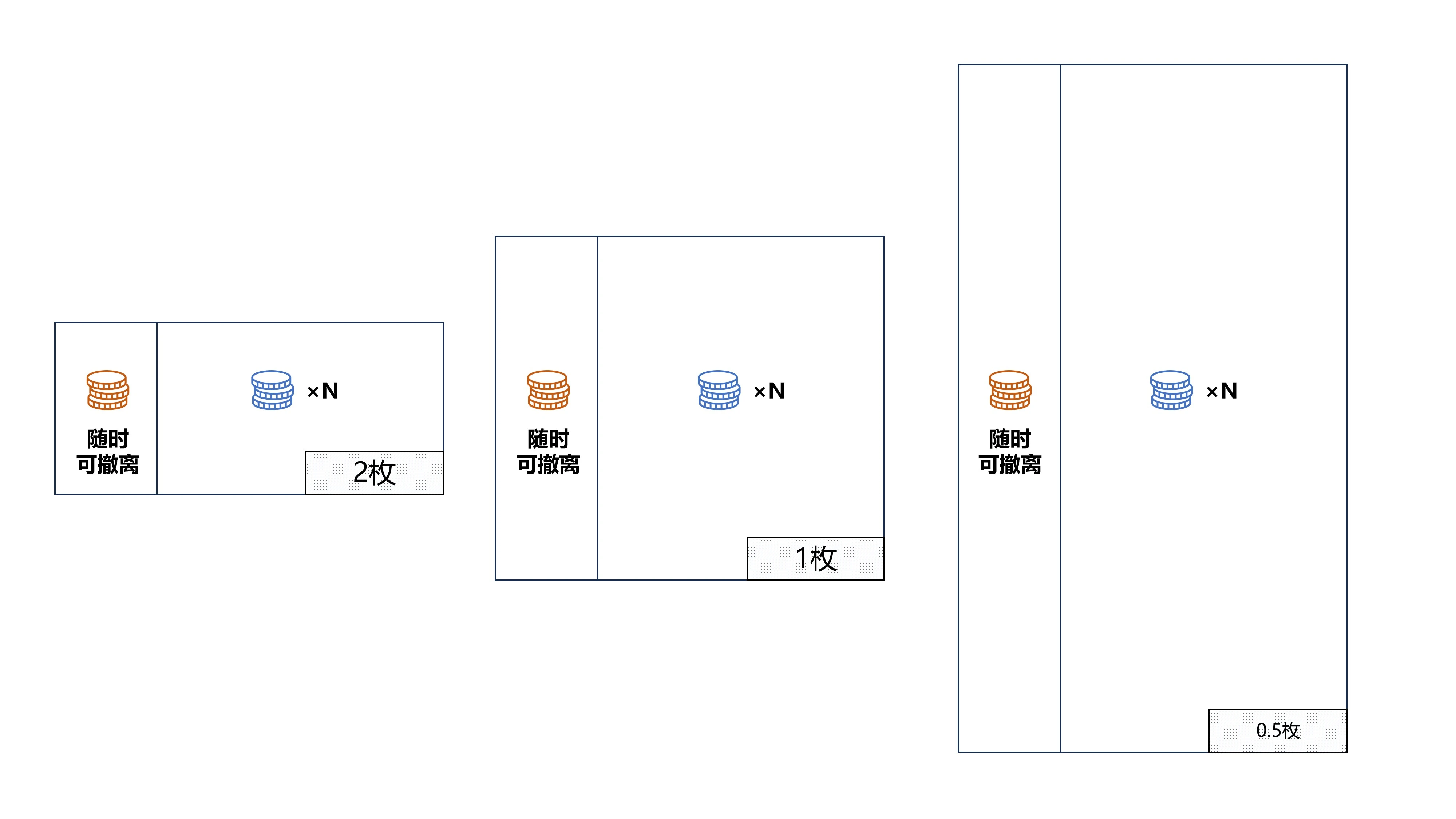

In the U-based model, the user's entry cost is converted to a stablecoin, for example, set at a fixed value of 100U:

When the token price is 50U, the mining machine price is 2 tokens;

When the token price is 100U, the mining machine price is 1 token;

When the token price is 200U, the mining machine price is 0.5 tokens;

In the token-based model, the purchasing power of one token is fixed and does not change with the fluctuation of token prices.

Similarly, the user's output is also converted to a specific stablecoin, and at any given time, if the output is immediately sold, the amount of stablecoin obtained remains unchanged.

Extreme Positive and Negative Feedback

Does using a fixed amount of stablecoin for input and output reduce the Ponzi properties?

The answer tends to be negative. Although this model weakens the selling pressure from mining assets, it greatly enhances the inflation and bursting of the bubble.

Small asset sales pressure

In the token-based model, the number of tokens to purchase mining machines does not change, so as the token price rises, the mining machine price will also rise, especially in the dual-token model, by driving the rise in the price of the small pool, the expected earnings of the mining machine will also rise, causing prices to rise rapidly.

In the absence of any signs of collapse and with sufficient market liquidity, mining machine holders can sell a large amount of mining assets to realize profits.

Under the U-based model, regardless of how much the price rises, the mining machine price remains unchanged, so users will not choose to sell the mining machines, but continue to produce tokens.

Rapid bubble inflation and bursting

In the absence of selling pressure from mining machines, the only pressure comes from the selling of tokens, and under the U-based model, the positive and negative spiral effects are evident, with basically only one unilateral rise and one unilateral fall leading to the end.

During the rise, the output of tokens decreases as the price rises, and users will find that if they hoard the output tokens, their asset value will rapidly inflate.

For example, with the U-based value set at 100U, at this time, users can produce 1 token worth 100U. When the token price reaches 200U, the output is only 0.5 tokens, so compared to users who entered later, it can be considered that the number of tokens has doubled, the price has doubled, and they have a very obvious advantage. Therefore, during the rise, users have a clear reluctance to sell and positive emotional response, leading to a small upward spiral.

Similarly, during the fall, the output of tokens continues to increase, and if not sold first, subsequent users will produce more tokens, and at relatively lower prices, leading to a continuous increase in selling pressure and a downward spiral, consistent with the bubble bursting process of LUNA.

CryptoMines experienced a round of unilateral rise and a round of unilateral fall, with its token price rising from 1 USDT to over 800 USDT in two months, and the LP pool peaking at over 30,000 BNB. However, its collapse took less than a week, with the token price falling by over 50% daily, and ultimately due to excessive token issuance, exceeding the predetermined total token limit, liquidity dried up and users were completely unable to exit.

Token Investors' Bloodsucking

As mentioned earlier, users participating in the game have a reluctance to sell the output tokens, leading to a significant increase in token prices. Additionally, CryptoMines also imposed restrictions on the withdrawal of output tokens, with a penalty for early withdrawal within a 15-day period.

The above situation allowed token investors to profit significantly and have the advantage of being able to exit at any time from the peak, causing a rapid and substantial loss of funds from the pool.

As shown in the figure below, without increasing the number of mining machines, the share of output from game participants decreases as the price rises, but the selling ability of holders does not decrease, becoming a potential significant selling pressure when it reaches a certain level.

In the end, the U-based model of GameFi saw an increasing number of users choosing to only hold tokens without participating in the game process, leading to a shorter game lifecycle and becoming purely secondary speculation, ultimately leading to the demise of this model.

Breeding Model: Ineffective Market Regulation

In addition to the single-token and dual-token models, as well as the token-based and U-based models mentioned above, there is another key distinction in the way mining assets are sold, which this article refers to as the gacha model and the breeding model:

The gacha model refers to mining machines being directly sold by the game system, with a constant price and usually no quantity restrictions.

Under the breeding model, offspring mining machines are produced through the synthesis of other users' mining machines, with prices determined by the market and quantities controlled by the number of parent mining machines and market sentiment.

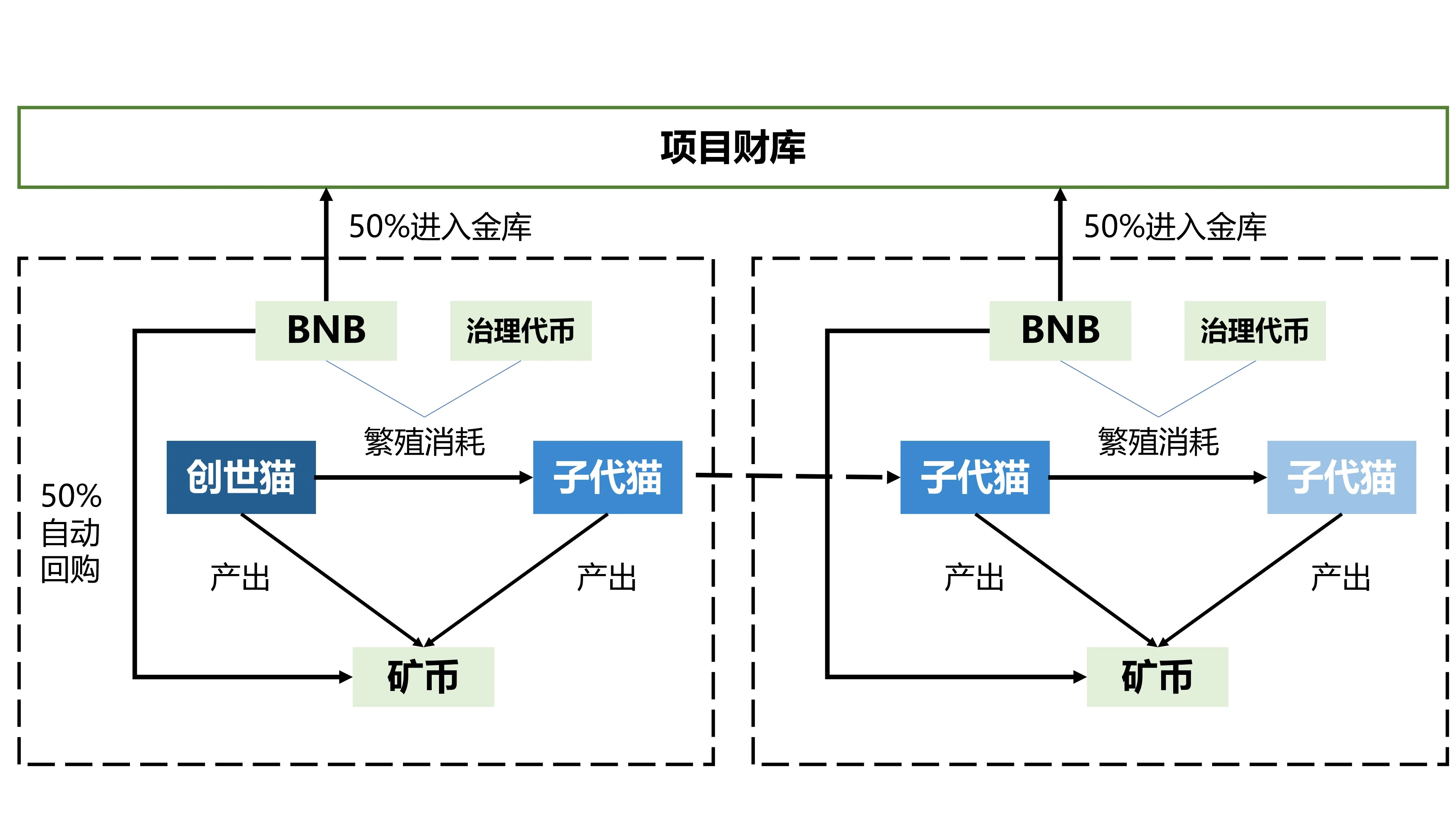

Nine Lives Cat (DNA×CAT)

All offspring cats come from previous generations of breeding. During breeding, users need to consume BNB and a minimal amount of governance token DXCT, with 50% of the BNB automatically repurchasing SFC, and the rest entering the treasury to be operated by the project party.

SFC is the sole token of the game economy, and mining machines produce SFC by participating in game activities, with the consumed BNB serving as their nurturing power.

Under the breeding model, quantities and prices are determined by the market. Can this mechanism reduce Ponzi properties and achieve longer-term operation through self-regulation of the market? The answer is still negative.

- High prices, profits entirely captured by early players:

Under the breeding model, early assets in the game are extremely rare, so the prices will be very high. On the other hand, since mining machines are directly produced and sold by players, the price difference between the selling price and the cost is directly captured by early players.

How is the price difference calculated? In Nine Lives Cat, the hatching of a single offspring cat takes 5 days, and the price difference can be considered as the output of a single mining machine over 5 days. Assuming a static calculation where mining machines break even in 20 days, it means that 25% of the profits flow directly into the hands of the hatchers. In contrast, under the gacha model, user funds enter the LP pool and are extracted from the overall ecosystem, showing that the breeding model significantly reduces the thickness of the fund pool.

- Exponential breeding, rapid bubble inflation

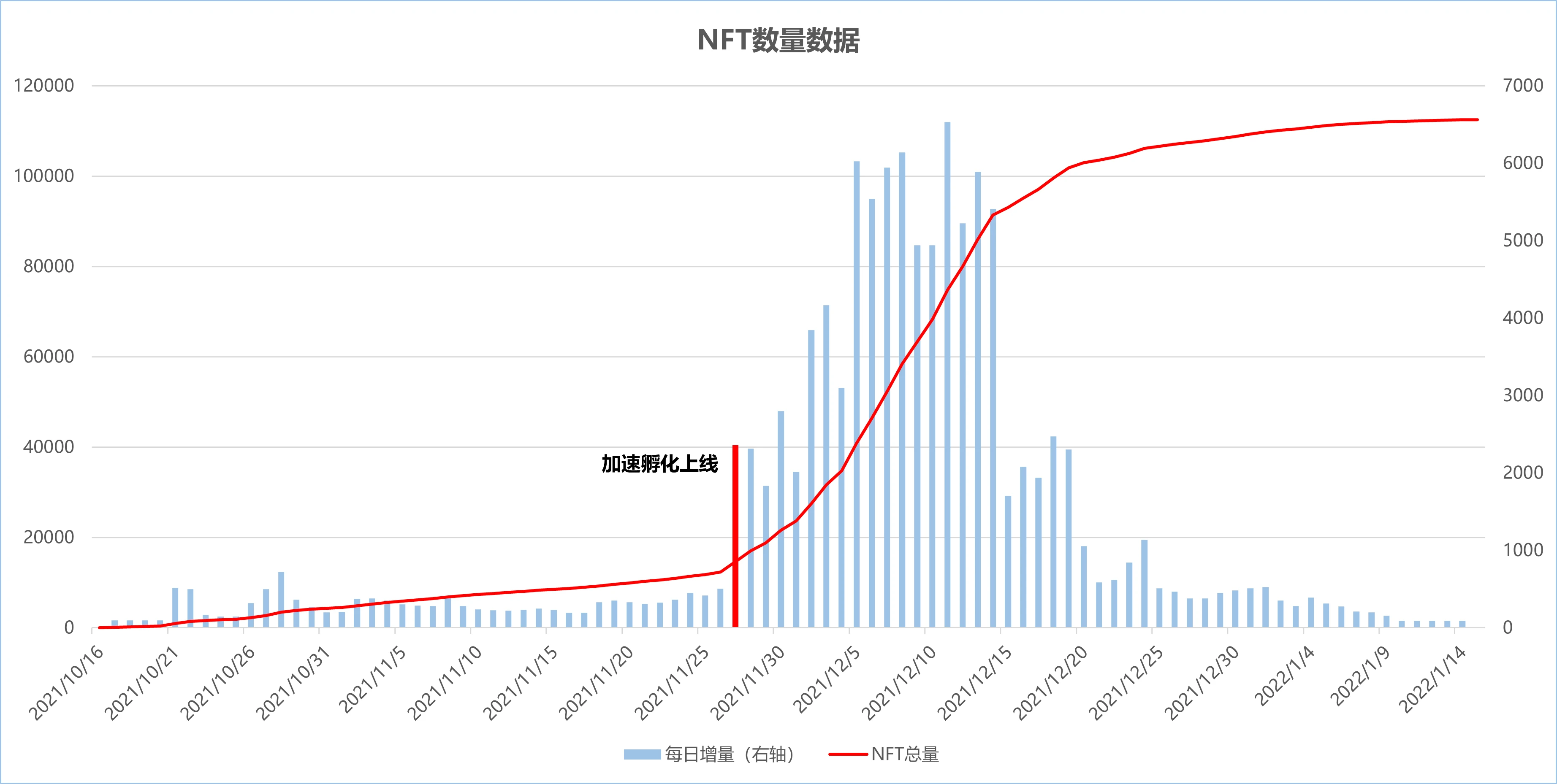

From 2021 to the present, in the breeding model of GameFi, typically a pair of parent mining machines can produce 7 offspring mining machines, which will lead to the continuous production of mining machines as long as there is any profit space, leading to a situation where profits eventually become zero. This causes assets and bubbles to rise exponentially.

The chart below shows the NFT quantity statistics for Nine Lives Cat from 2021. Initially, the production of offspring required a five-day incubation period, but after the acceleration incubation feature was enabled (which allows tokens to be spent to complete incubation directly), the quantity began to soar, token output doubled rapidly, the supply and demand relationship of mining machines changed, and ultimately the difficulty of fund acceptance exploded, leading to a collapse after only 18 days.

From Nine Lives Cat in 2021 to Gas Hero in 2024, once the game starts with excessive hype before or at the beginning, the initial assets are often excessively speculated, leading to a trend of exponential increase in the number of mining machines combined with a decrease in prices, ultimately leading to a rapid collapse.

Conclusion

The summary of the above economic designs is as follows:

Single-token model: Relatively stable for all parties, but therefore more difficult to adjust expectations and control the market;

Dual-token model: Differentiates volatility into two pools, making it relatively easy to achieve expected regulation;

Token-based model: Relatively stable, without self-feedback effects, and prone to asset-side appreciation pressure;

U-based model: Extremely unstable, with significant positive and negative spiral effects, and prone to holding pressure from speculators;

Gacha model: Can control the flow of funds in combination with other designs, but prone to excessive inflows on a single day;

Breeding model: Prone to excessive FOMO at the opening, suitable for the project party to effectively control the operational rhythm and market supply and demand.

In addition to the basic models mentioned above, there have been many effective mechanisms and innovations. For the project party, the fundamental goal is how to expand the bubble and delay the time of collapse, involving various aspects such as economic model design and operational rhythm coordination, encouraging user lockups/reinvestment, creating emotions and events, and controlling the entry and exit of funds throughout the entire cycle.

However, at present, there are very few pure Ponzi scheme GameFi models, but the financial attributes as a natural attribute of Web3 cannot be ignored.

For users, what are the key points to consider?

One is that the time to exit is when there is a lot of buzz, not based on the price, but on the liquidity of the valuation exit. In the Ponzi scheme GameFi, claiming to break even in N days is a basic element, but often cannot support many N days. The time of buzz is the time to cash out at the highest valuation, without taking the risk of continuing to mine and sell for N days.

On the other hand, the GameFi market assets are mainly P2P, requiring counterparties to accept, and a time of buzz means the best exit liquidity. When entering a downward trend, the P2P market will face a liquidity collapse and the problem of difficulty in selling.

What users most need to understand is that the design of the economic model can only affect the general development process and methods. For a Ponzi scheme model, the rise and fall of the economy is not determined by the quality of the economic model design, but by the inflow and outflow of funds, fundamentally a game of negative and positive sum between people. Rational investment and risk control are the fundamental elements.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。