数字资产的托管正在发展,无论是技术本身、大量新的通证化投资产品,还是将资产留在中心化交易所等服务提供商那里的风险,无论是真实的还是被感知到的。

Hedgehog Technologies的CEO Colton Dillion 分析了数字资产托管的发展,重点关注财富向自托管的转移以及顾问如何支持这种转变。

在“问专家”中,Sound Advisory的 Jessy Gilger 回答了有关在IRA账户内直接拥有比特币的问题。

–S.M.

您正在阅读《顾问的加密货币》,CoinDesk每周发布的为金融顾问解读数字资产的新闻简报。在此订阅,每周四获取最新内容。

Web3的基础设施最终将吞噬传统金融,这是毫无疑问的。

数字资产行业市值高达2.3万亿美元,但在超过110万亿美元的股票市场之前,它还有很多成长空间。但如果您还没有留意,现实世界资产(RWAs)和稳定币最近受到了Blackrock、Stripe、Franklin Templeton等主要参与者的大笔投注。

这些公司正在逐渐复制像货币市场基金和共同基金这样的传统证券,以供链上消费和无缝点对点转账,监管机构只是时间问题,它们将允许以与传统证券交换相同的方式交换传统证券,例如财富500公司的股票或交易所交易基金(ETF)。最终,每种传统资产也将成为链上资产。我们需要的只是时间。

那么,这对托管人意味着什么?

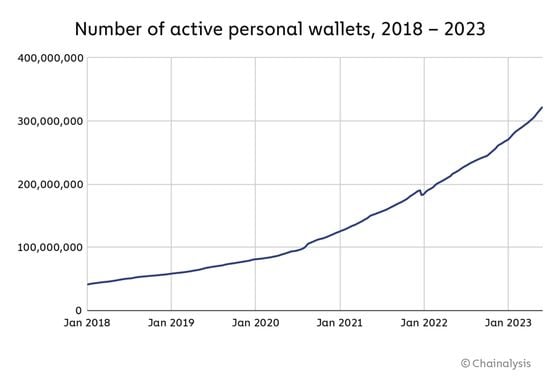

Chainalysis报告称,即使资产被发送回交易所的数量在季度间逐渐减少,个人钱包数量却呈指数增长。零售客户和机构客户都选择将他们的资产保留在链上,而不是将其托管给可能会成为另一个FTX或以其他方式将其资金置于高度相互关联的再质押网络中的托管人。如果您能避免将您的资金锁定在Silvergate的破产程序中,您会选择避免吗?

尽管Coinbase、Kraken和Gemini都至少支持一个现货比特币ETF作为主要托管人,机构使用案例迁移速度较慢,但对于Web3资产持有者来说,有一个明显的趋势,即一旦他们达到一定的复杂程度,就开始将他们的财富转移到自托管。一旦保险方法赶上钱包被破坏的情况,我们预计大多数个人和机构都会选择直接处理其账户的隔离,并要求控制自己的私钥。

作为顾问和受托人,我们有责任为客户要求支持自托管解决方案的那一天做好准备。对于勇敢的自托管者来说,有许多选择,从多重签名账户到账户抽象(AA)智能合约钱包,从机构硬件到多方计算(MPC)钱包,但每种方法都涉及其自身的安全性和可用性权衡,以及成本考虑。

多重签名

Gnosis Safe是基于以太坊网络的原始多重签名解决方案,并配备了一些方便的工具,用于在多人必须同意后才能进行交易的钱包中管理您的资金。在其他链上,您必须找到其他解决方案,比如支持Shamir's Secret Sharing的专用钱包软件。花费不到500美元,您就可以建立一个m个n签名(例如3个中的2个或9个中的8个必须签署才能进行有效交易)的钱包,但是如果不包括新的账户抽象提案,例如ERC-4337,这些账户的权限较弱。如果您拥有其中一个签名,您可以帮助签署Safe账户上的任何特权。

账户抽象

这是另一个目前仅适用于EVM的解决方案,但原则上,任何支持智能合约的链都可以支持这个标准。账户抽象允许精明的开发人员在标准账户的基础上添加额外的权限和功能,以便某些签署者只能对特定类型的交易进行签名。许多提供商还利用这些功能来添加交易批处理、非本地Gas代币、交易宽恕等功能。这些参与者包括Gnosis Safe以及ZeroDev、Biconomy和Fun等团体。

机构冷存储

许多托管人提供冷存储解决方案,利用硬件安全模块和强大的物理安全性,将您的资产保存得像福特诺克斯下的金条一样安全。通过使用极其昂贵的专用芯片,它们可以为您生成私钥并安全地代表您签署交易,但没有热钱包的灵活性和速度。根据提供商的不同,这些解决方案通常与多重签名、AA或MPC解决方案结合在一起,但成本通常会达到两位数的基点,且需要高额的最低余额和账户维护费用。

多方计算

MPC是目前最灵活的选择之一,它不受智能合约限制于特定网络,但需要对潜在的不透明合作伙伴进行信任。MPC更接近加密的基础层,即私钥熵,MPC钱包中的所有参与者共同参与重新创建私钥,而不是让多个私钥发送自己的有效签名。对于更懂技术的人来说,有Qredo和Lit协议,这是完全去中心化的解决方案,但对于希望得到更多专业服务并愿意与受信任的第三方合作的顾问来说,Anchorage刚刚发布了他们的企业解决方案Porto,而我的公司Hedgehog刚刚发布了一个以基金管理、子顾问和一站式资产管理计划为重点的MPC账户管理产品。

显然,我们同意Anchorage的CEO Nathan McCauley的看法,他在总结选择MPC作为解决方案的理由时表示:

“目前,许多人寻求自托管解决方案,以便在区块链上进行更灵活的活动。我们真的认为这是扩张性和增值的。”

无论您作为顾问选择什么,都很重要的是要牢记托管规则,并确保您对客户账户没有任意的提取特权。对于一些这些账户结构,还没有太多的指导,关于任何特定的多重签名、AA或MPC协议是否具有对客户资金的实质控制,仍然有一些需要澄清的地方。然而,我们必须开辟前进的道路,否则就会被客户抛在身后。

– Colton Dillion, CEO, Hedgehog Technologies

问:能在IRA账户中持有比特币吗?

是的,有几种方法可以在传统和罗斯IRA账户中获得比特币的投资。最简单的方法是通过在主要券商交易的现货比特币ETF之一。然而,这种方式只提供对比特币价格波动的美元曝光,而不是实际硬币的直接所有权。

对于许多比特币投资者来说,首选的选择是通过专门提供直接所有权和存储比特币的IRA账户。在这里,关键的控制至关重要——您能够保持私钥意味着您完全拥有和控制IRA中的比特币,而不是将其委托给第三方托管人。这避免了其他选择中的集中化和交易对手风险。

问:在IRA中持有比特币的好处是什么?

主要优势在于能够将比特币作为长期价值储存进行投资,同时享受IRA账户的税收优惠。由于许多人认为比特币是一种更优越的储蓄形式,它与退休账户的长期视野非常契合。

具体的好处包括税延或免税增长(传统或罗斯),使您的比特币持有在数十年内更有效地复利增长。比特币在历史上以一致的4年周期升值,因此免税地获得这些收益可以显著加速您的退休时间表。

在IRA中持有比特币还使得可以以比特币本身进行分配,而不必出售换取美元并实现应税收益。对于希望拥有完全主权的客户来说,对其IRA中的比特币的关键控制至关重要,以避免第三方托管风险。不利的一面是相对于标准券商账户,流动性降低,规则和年龄限制增加。但对于长期投资者来说,相信比特币作为硬通货的角色,IRA的税收优惠可能会超过这一点。

- Jessy Gilger, CCO & Senior Advisor, Sound Advisory

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。