On June 9th, Beijing time, Apple WWDC26 officially brought the long-awaited answers to the forefront:

Can Apple AI really make up for it?

As is well known, over the past two years, the strongest players in the AI landscape have been tech giants like NVIDIA, Google, Microsoft, Meta, and large model companies such as OpenAI and Anthropic. In contrast, although Apple boasts the world's strongest hardware access — with iPhone, iPad, Mac, Apple Watch, and Vision Pro, as well as a complete App Store ecosystem — the implementation pace of Apple Intelligence and Siri has consistently fallen short.

Thus, the core focus of this WWDC is not merely whether Apple will discuss AI, but rather whether it can convince the market that Apple Intelligence will truly become an AI entry point capable of reigniting the upgrade cycle, developer ecosystem, and application ecosystem.

1. WWDC may not necessarily boost Apple, but it's likely to create a gap in expectations

First, let's look at historical performance.

In past years, WWDC has not been an event where "Apple's stock price is guaranteed to rise." Based on a rough calculation from the Friday closing price a week before WWDC to the Friday closing price during the WWDC week:

- In 2022, during the WWDC week, AAPL dropped about 5.7%;

- In 2023, during the week of the Vision Pro release, AAPL remained basically flat;

- On the day of the Apple Intelligence release in 2024, AAPL first dropped about 1.9%, but then the market reinterpreted the logic of "on-device AI + upgrade cycle," and ultimately rose about 7.9% that week;

- After WWDC in 2025, the market was dissatisfied with the delays regarding Siri and AI progress, resulting in an approximate drop of 2.4% that week;

So, WWDC itself is not a stable upward event, but it often creates "expectation gap trades." From this perspective, if this time is merely a routine system update, the stock price may respond flatly; but if AI, Siri, on-device capabilities, and the developer ecosystem exceed expectations, it could bring about a short-term wealth effect.

This is also why this year's WWDC is worth paying attention to in advance.

2. The decisive factor for Apple AI: not the model, but the entry point and upgrade cycle

It is worth mentioning that many companies create AI with models first, then look for user entry points, while Apple does the opposite; it already has the entry point, but needs to enhance its AI capabilities.

Because Apple's real advantage is not in the parameter count, but in the system-level entry — it can embed AI into iOS, macOS, iPadOS, watchOS, and visionOS, allowing AI to directly access Mail, Photos, Calendar, Messages, Notes, App Store, and third-party applications.

This is why Siri is important.

If Siri continues to be just "check the weather, set an alarm," it will be difficult to support a reevaluation of Apple AI. However, if Siri can read user context, call different apps, and complete cross-application tasks, it will no longer just be a voice assistant but will become an AI Agent entry point within the Apple ecosystem.

So, the first key point to watch at WWDC is whether Siri upgrades from a "voice assistant" to a "system-level AI entry point."

The most directly corresponding stock to this line is, of course, AAPL.M. If Apple continues to leverage external models or cloud inference, GOOGL.M, MSFT.M, and AMZN.M may also be mapped by the market.

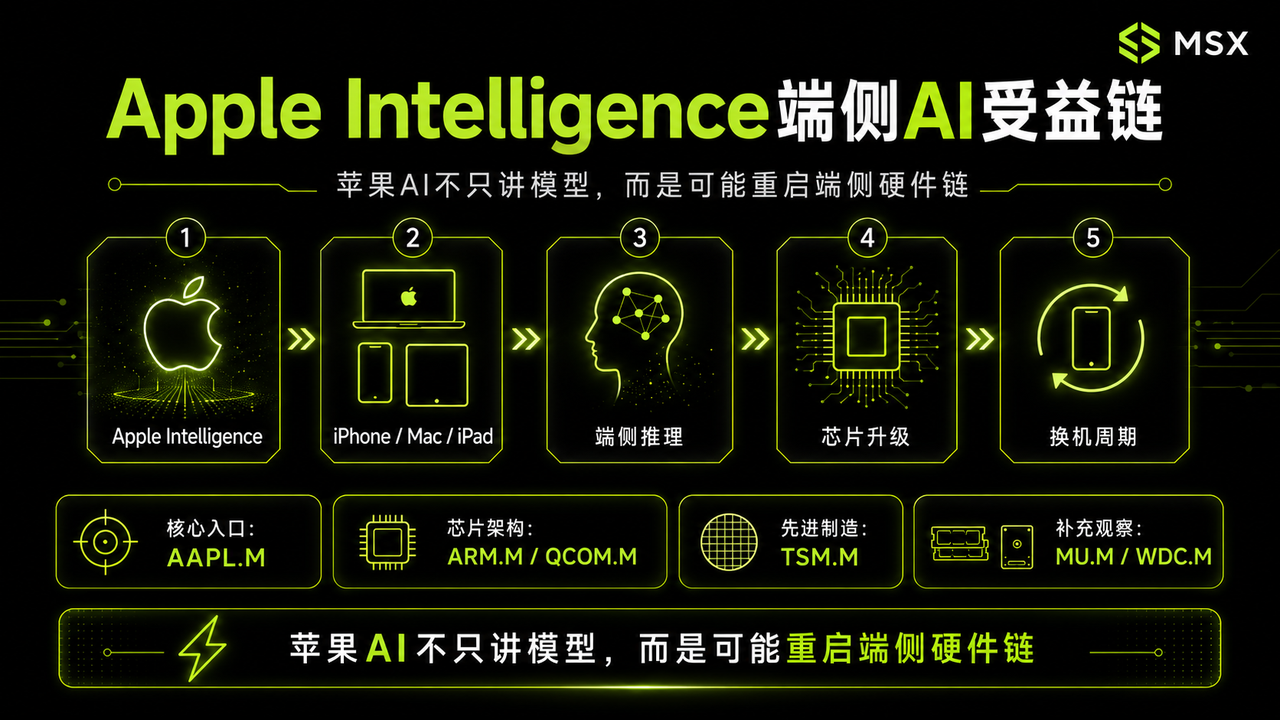

However, the real wealth effect of Apple AI may lie not only at the software level but also at the hardware level. If the new features of Apple Intelligence require stronger chips, larger memory, and better local inference capabilities, then it will shift from a simple software update to a hardware upgrade logic.

The advantages of on-device AI are clear; it allows many tasks to not rely entirely on the cloud, leading to quicker response times. It also better aligns with Apple's long-standing emphasis on privacy and security; more importantly, it can naturally bind with new hardware, encouraging users to migrate from old iPhones and old Macs to new devices.

After Apple launched Apple Intelligence in 2024, one important reason the market re-priced after a brief divergence was that people began to contemplate if the AI functionality tied to new devices would trigger a new upgrade cycle.

This is also one of the key sources of wealth effects expected from this year's WWDC.

The on-device AI chain can focus on AAPL.M, ARM.M, TSM.M, QCOM.M. Among them, AAPL.M is the terminal entry; ARM.M represents low-power architecture; TSM.M is an important foundry for Apple chip manufacturing; QCOM.M, while both a competitor and collaborator with Apple, will also be compared in the on-device AI and mobile chip ecosystem.

3. The real spillover opportunity: from the chip chain to the app ecosystem

It is important to note that WWDC is not just one day, nor is it merely Apple's own conference; it is essentially a developer conference.

If Apple only adds a few AI features to the system, it will be more of a story for AAPL itself. However, if Apple opens AI capabilities to developers, allowing third-party apps to call local models, system-level Agent capabilities, privacy computation frameworks, and new developer tools, then Apple Intelligence will evolve from Apple's story into an ecosystem story.

This line is significant.

Because Apple's true moat is not individual AI functionalities but the App Store ecosystem. As long as developers can integrate Apple Intelligence into creative, office, documents, e-commerce, finance, and productivity applications, it could lead to a multitude of new AI application scenarios.

From an investment mapping perspective, Apple Intelligence concept stocks can be divided into five layers.

The first layer is the core entry AAPL.M. If Siri and Apple Intelligence exceed expectations, the direct beneficiary will still be Apple itself, as it controls hardware access, system authority, and application distribution. Once AI capabilities are truly embedded into the system, the first to be reevaluated will still be AAPL.M.

The second layer is the on-device AI chain, such as ARM.M, TSM.M, QCOM.M. If Apple places more AI capabilities to run on local devices, low-power chip architecture, advanced processes, and mobile AI capabilities will be revisited.

The third layer is model and cloud collaboration, such as GOOGL.M, MSFT.M, AMZN.M. If Apple continues to enhance Apple Intelligence through external models or cloud capabilities, these giants will also be reflected in the market, especially against the backdrop of Apple insisting on privacy, security, and cloud collaboration routes, who becomes a partner for underlying models or cloud inference will influence the market’s short-term imagination regarding these companies.

The fourth layer is developer tools, including MSFT.M, TEAM.M, DDOG.M, GTLB.M. If WWDC emphasizes AI programming, Xcode upgrades, developer APIs, and application building efficiency, the AI development ecosystem may be stimulated. For the market, this line of trade is not about how much direct revenue these companies gain from Apple but rather the fact that "the barriers to AI application development continue to be lowered."

The fifth layer is the app ecosystem, such as ADBE.M, DOCU.M, INTU.M, SHOP.M. These companies are not direct beneficiaries of Apple AI, but if system-level AI capabilities are opened up, applications in creative, documents, finance, and e-commerce sectors are most easily integrated with new features. They appear more as potential mapping targets once Apple Intelligence spills over to the application layer.

Of course, while this line has a lot of imagination, it also carries risks.

First, Apple AI might be "loud thunder with little rain." If it turns out to be just a routine system update without any substantial upgrade to Siri or open developer capabilities, the market is likely to be disappointed.

Second, the spillover targets may not immediately translate to income, such as ADBE.M, SHOP.M, DOCU.M, INTU.M. Even if they may access Apple AI capabilities in the future, it might not be quickly reflected in their financial reports.

Third, Apple's enhancement of AI capabilities may benefit AAPL.M more directly; if the new capabilities are mostly confined within Apple's system, the gains for external concept stocks will be relatively weak.

Fourth, AAPL.M's valuation recovery will ultimately depend on iPhone demand. AI can tell stories, but hardware sales, service income, and profit margins are the core for long-term pricing.

Therefore, Apple Intelligence concept stocks can be seen as expectation trades, but they cannot simply be understood as "WWDC is guaranteed to rise."

In conclusion

Before WWDC, the market trades on expectations; after WWDC, the market will begin to validate whether Apple AI has any substantive changes.

If Apple merely adds a few AI features, it may be just an ordinary software update.

However, if Siri becomes a system-level AI entry point, on-device AI binds with new hardware, and developer tools open up new capabilities, then Apple Intelligence will not just be Apple's story but may drive a new mapping chain in the U.S. stock market.

It all depends on whether it can embed AI into the world's largest consumer electronics ecosystem.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。