Strategy sacrificed the core indicator of "Bitcoin holdings per share" of MSTR for the development of STRC.

Written by: 100y

Translated by: Chopper, Foresight News

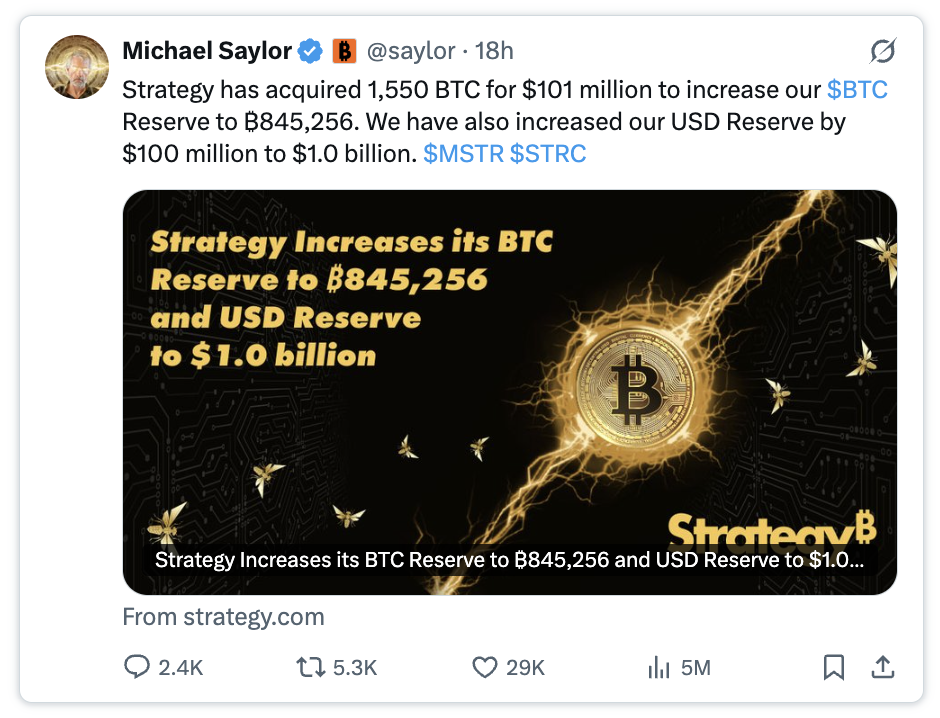

The Bitcoin treasury company Strategy first sold 32 Bitcoins and then made a significant purchase of 1,550 Bitcoins.

I do not wish for Strategy (MSTR) to decline, but some truths must be spoken. In my view, this is an extremely poor transaction.

On the surface, this operation seems quite impressive. The Strategy company made a large purchase of Bitcoin at relatively low prices while also raising the dollar reserves for paying preferred dividends from $900 million to $1 billion.

Does this mean that Strategy is about to see a turnaround?

If you only see positive aspects from this, it means you do not truly understand how this company operates.

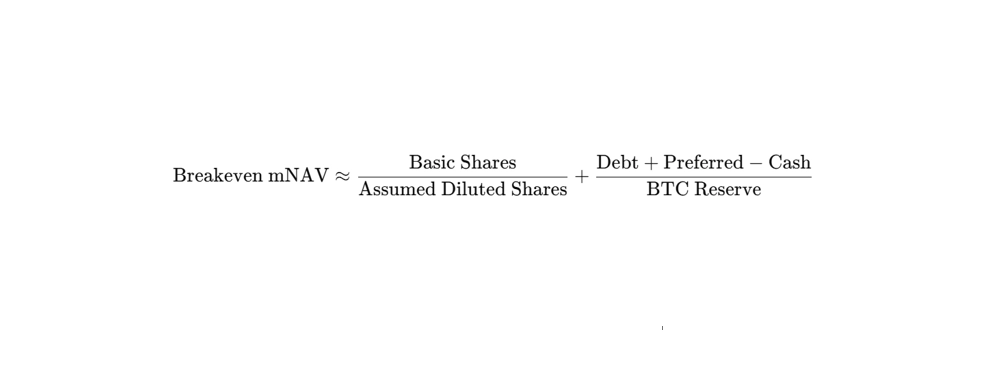

First, understand the adjusted net asset value (mNAV) at the breakeven point

Increasing Bitcoin holdings per share (BPS) is one of the core objectives of Strategy to create value for MSTR shareholders.

The logic for increasing Bitcoin holdings per share is quite clear: issue common stock at a premium above the market price, and then use all the raised funds to buy Bitcoin.

So, how high of a premium does MSTR need to achieve to actually increase Bitcoin holdings per share through timely stock issuance?

According to information disclosed during the Q1 2026 earnings call, the adjusted net asset value (mNAV) must be above 1.22, a value referred to in the industry as the breakeven adjusted net asset value.

The underlying logic of this standard is simple: the funds raised from selling 1 share of MSTR stock must be able to buy more Bitcoin than the current Bitcoin holdings corresponding to that stock. The complete derivation of this can be found in my previous content. (https://research.4pillars.io/en/research/strategys-magic-number-122)

Ultimately, the calculation method for the breakeven point mNAV is as follows:

It is worth noting that the current breakeven adjusted net asset value is no longer 1.22. Before the operation of purchasing 1,550 Bitcoins, this value had already risen to 1.30.

Why this is a bad deal

Let us return to the acquisition of 1,550 Bitcoins.

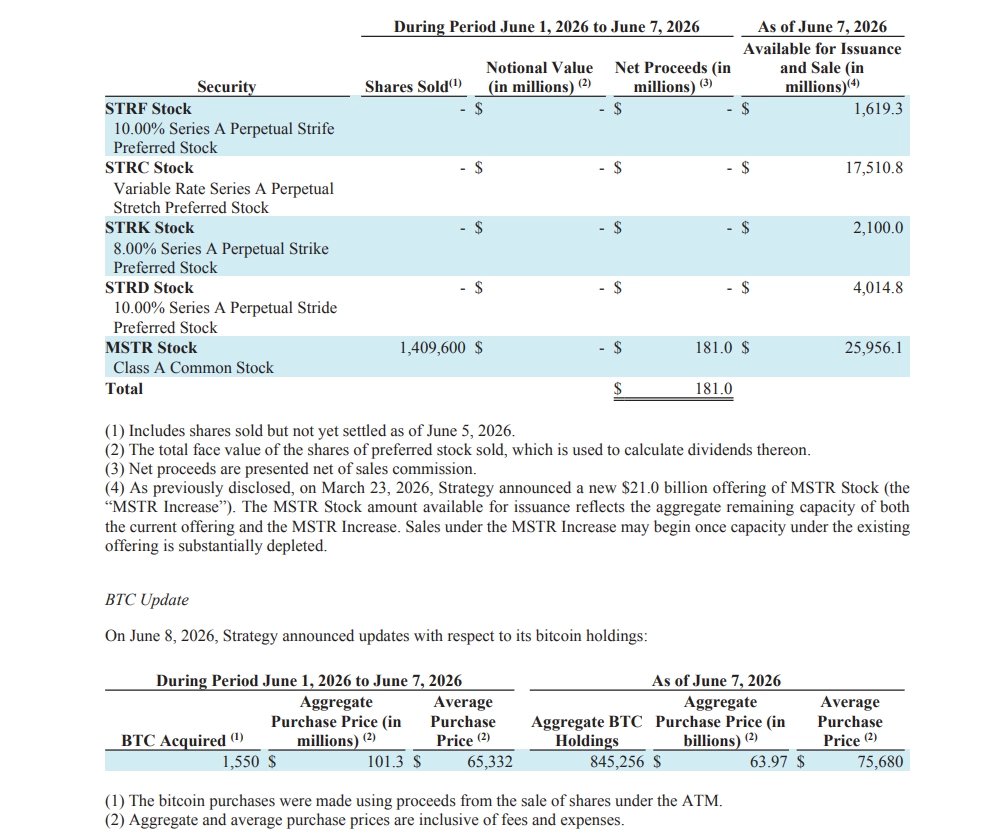

Strategy raised a total of $181 million through MSTR's timely issuance model and then used $101.3 million of that to purchase 1,550 Bitcoins. This operation has two major core issues:

First, the adjusted net asset value (mNAV) corresponding to this timely MSTR stock issuance was below 1.30, the breakeven point. If stocks are issued before the adjusted net asset value reaches the breakeven line and the raised funds are used to buy Bitcoin, it will not only fail to increase Bitcoin holdings per share, but instead cause that indicator to decline.

Second, and more critically, the funds raised from this issuance were not fully allocated to purchasing Bitcoin. The logic of the breakeven adjusted net asset value calculation is based on the premise that 100% of the raised funds are used to purchase Bitcoin. Even if the adjusted net asset value is high, as long as only a portion of the raised funds goes into Bitcoin, it will ultimately lower Bitcoin holdings per share.

It is reported that the remaining funds from this issuance that were not used to buy Bitcoin were allocated to the company's dollar reserves.

In other words, Strategy sacrificed the equity value of MSTR shareholders and Bitcoin holdings per share to ensure the normal operation of STRC-related businesses.

After this transaction, the company's Bitcoin holdings per share decreased by about 0.19% compared to before. And what was the result? The company's dollar reserves extended the period for operational support from about 6.3 months to 7 months.

A gamble for Strategy

Michael Saylor stated in the Q1 2026 earnings call: "Our core goal is to increase Bitcoin holdings per share, and we will spare no effort to achieve this goal."

However, from this transaction, it can be seen that Strategy, for the development of STRC, chose to sacrifice the core indicator of Bitcoin holdings per share of MSTR, which is no different from a gamble.

If sacrificing MSTR leads to a recovery of market sentiment, stabilization and rebound of STRC coin prices, while also pushing the adjusted net asset value back to a reasonable range, then the company can continue to rely on MSTR and STRC's stock issuance channels to raise funds, allowing the entire system to operate healthily.

But once market sentiment does not improve, the situation can turn sharply downward. At that time, Strategy may only be able to continually sacrifice MSTR's interests to survive.

The worst situation will follow, where the company will either be forced to delay issuing STRC dividends or gradually decline due to continued internal consumption.

In the end, I hope that the prices of Bitcoin, MSTR, and STRC will all experience a recovery.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。