TL;DR

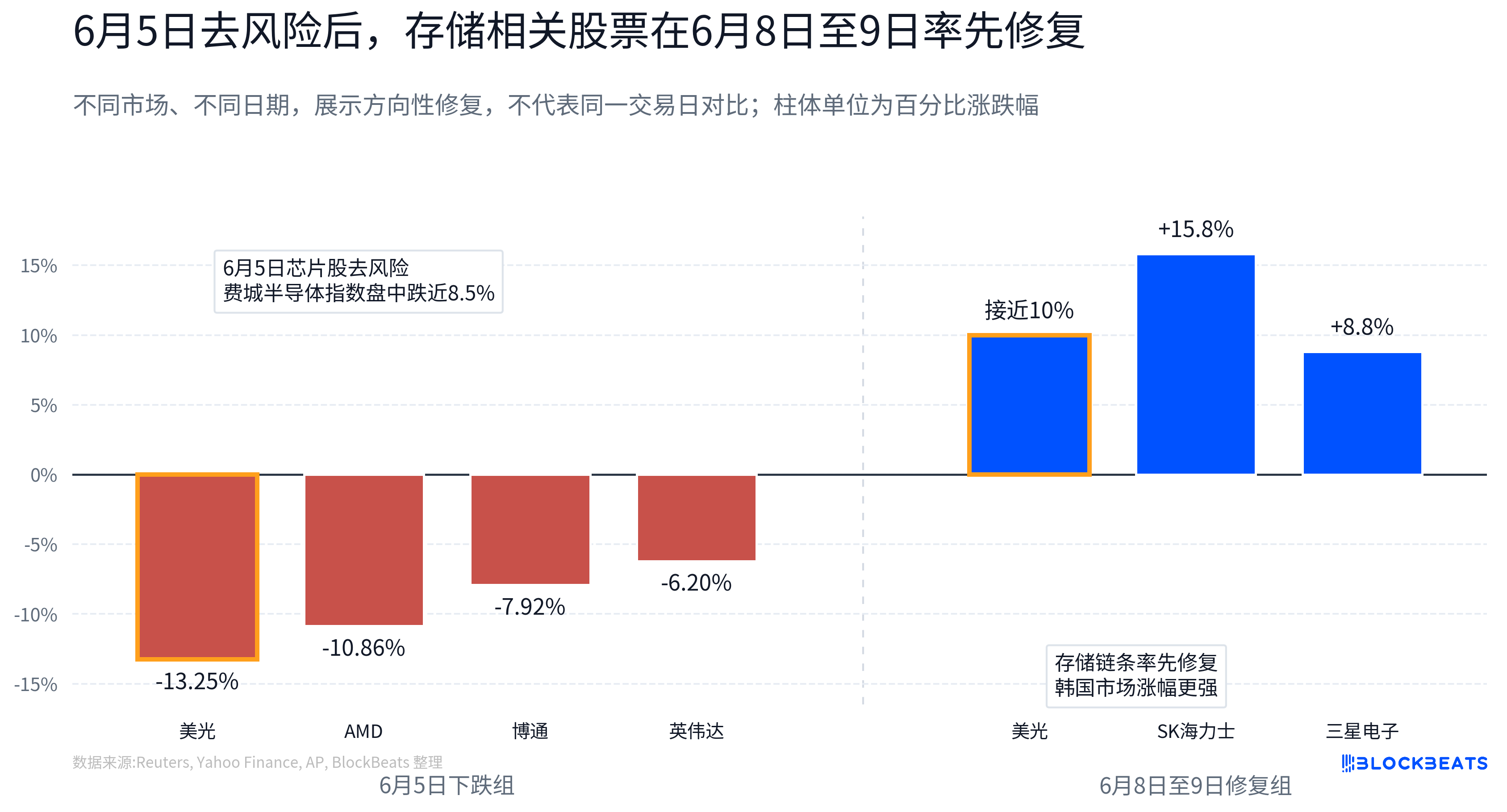

- After a significant de-risking of U.S. chip stocks on June 5, Micron rebounded nearly 10% on June 8, followed by a recovery in the South Korean market with notable gains in SK Hynix and Samsung Electronics on June 9.

- Combining earnings reports, DRAM/NAND price increases, and Korea's chip export data, storage is currently more easily priced by the market with EPS revisions.

- Relevant stocks: Micron, SK Hynix, Samsung Electronics, Western Digital, SanDisk, Nvidia, Broadcom, Marvell, Coherent, Credo, SOXX Semiconductor ETF, SMH Semiconductor ETF.

After the semiconductor crash on June 5, market attention quickly shifted from "why it fell" to another question: after the drop, who will recover first.

The answer is not uniform. According to Reuters, U.S. listed chip stocks saw a market value evaporate to over $1 trillion at one point, with the Philadelphia Semiconductor Index dropping nearly 8.5% during the session. On a stock level, Micron fell about 13.25%, Nvidia about 6.2%, AMD about 10.86%, and Broadcom about 7.92%. However, by June 8, Micron quickly rebounded nearly 10%; on June 9, SK Hynix and Samsung Electronics in the South Korean market also showed strength simultaneously.

Funds did not leave AI semiconductors but instead were reallocated within the sector. As valuations began to face scrutiny, the market's focus shifted from "who owns the AI story" to "who can most quickly translate AI demand into profit." Compared to other AI hardware sectors still trading on expectations of future product cycles, client onboarding, and capital expenditure expansion, the growth in storage demand has been more directly reflected in orders, prices, and earnings reports.

This is also why storage received a funding influx first. The market bought back not just storage itself but also the underlying EPS growth logic that is more easily validated.

Sharp declines mean revaluation of high expectation trades

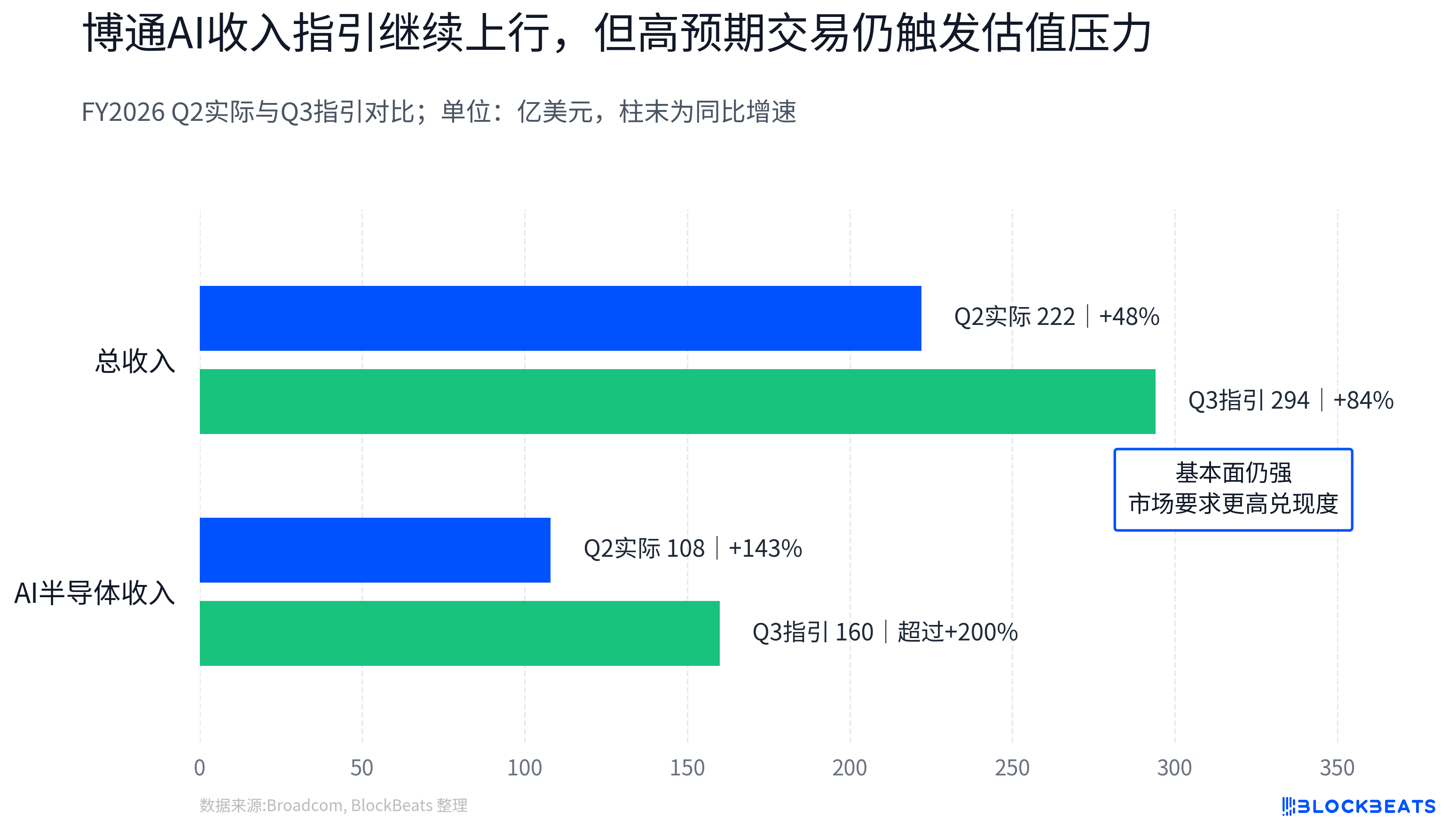

One of the triggers for this round of de-risking was the expectation gap following Broadcom's earnings report.

Looking at absolute numbers, Broadcom's fundamentals are not weak. According to the company's announcement, FY2026 Q2 revenue was $22.2 billion, a year-on-year increase of 48%. The company expects total revenue for FY2026 Q3 to be approximately $29.4 billion and predicts AI semiconductor revenue to reach $16 billion, a year-on-year increase of over 200%.

However, the market chose to sell. The reason is not that AI demand suddenly disappeared but that AI semiconductor assets have accumulated very high expectations over the past year. When a fundamentally strong company also triggers selling pressure due to AI revenue guidance falling short of some expectations, it indicates that the market's pricing threshold has changed. Being part of the AI chain alone is no longer sufficient; growth rates, profit realization, and next quarter guidance must also align with valuations.

This is the significance of the plunge on June 5. It was not a demand collapse test but a pressure test for high expectation trades.

In the past, the main theme of AI semiconductors resembled "who is closer to AI CAPEX (capital expenditure)." GPUs, ASICs (custom chips), high-speed optical modules, copper connections, and equipment materials could receive a premium as long as they fit into the AI cluster expansion chain. However, when the market began to worry about crowded trades, excessive valuations, and pacing of guidance realization, the question shifted from "who has the AI story" to "who can most quickly convert AI demand into financial results."

For the stock market, what ultimately determines valuation is not the orders themselves but whether those orders can be converted into earnings per share (EPS). Over the long term, stock prices essentially reflect the company's profitability. When the market begins to focus on next quarter's profits rather than stories three years down the line, changes in EPS often become more important than the narratives themselves.

Broadcom's role is therefore significant. It is one of the core assets in the AI ASIC and network chip chain. Its strength led to the stock price reaction after the earnings report, indicating that the AI semiconductor chain is undergoing higher validation standards.

Why storage: Prices and profits are already in the model

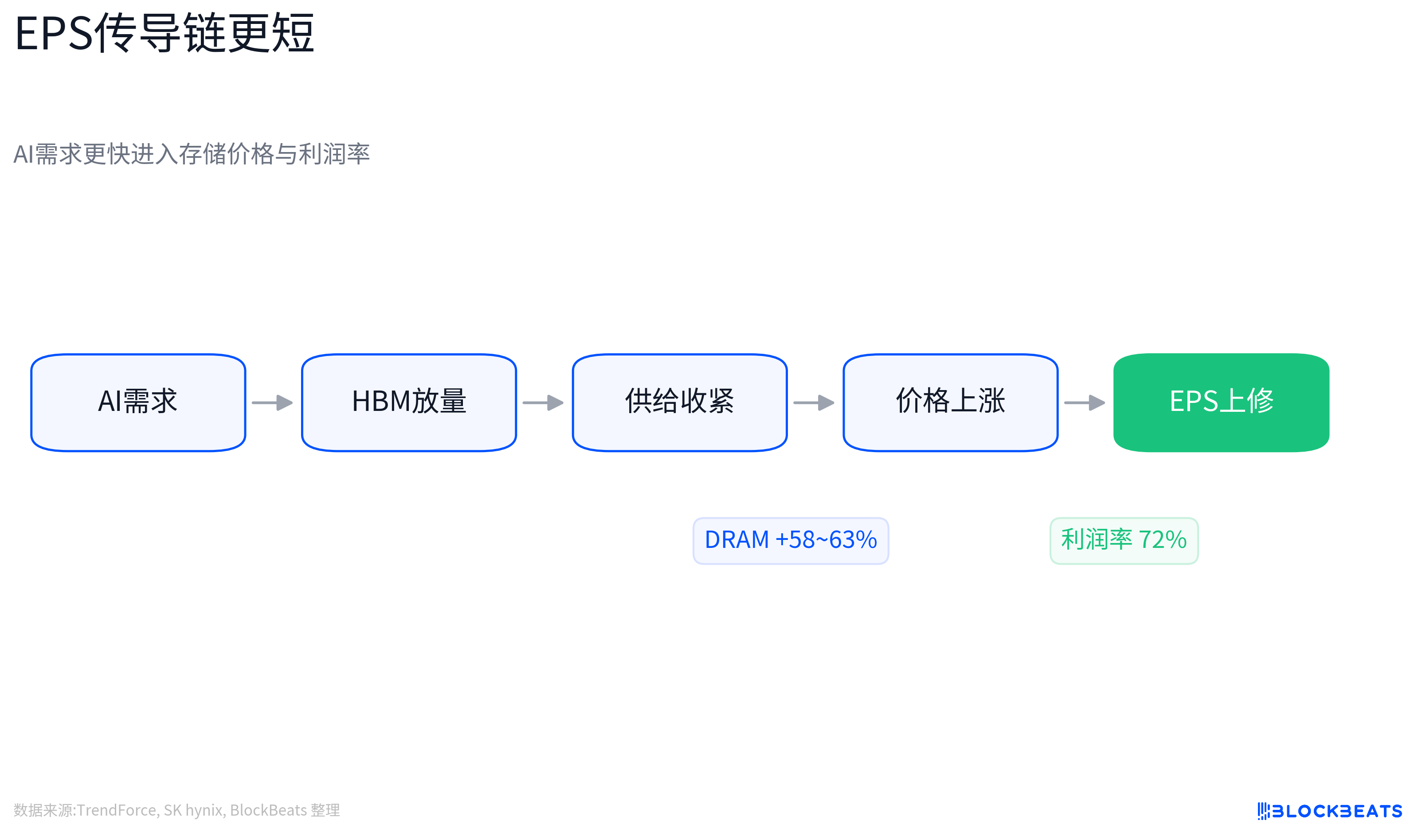

The advantage of storage is that the EPS transmission chain is shorter.

The first products affected by AI server demand are high-value items such as HBM (High Bandwidth Memory), server DRAM, and eSSD (enterprise-level solid-state drives). Cloud vendors and AI system vendors require more computing power, which means they need more GPU-compatible memory, higher capacity server memory, and larger scale data center storage.

As storage manufacturers shift production capacity toward HBM and high-end server products, the supply of traditional DRAM and NAND will also be further compressed, leading to an increase in contract prices. This link does not rely entirely on future expectations but will more quickly translate into revenue, gross margins, and EPS.

Micron's earnings report already reflects this change. According to the company's announcement, FY2026 Q2 set records in revenue, gross margin, EPS, and free cash flow, with substantial year-on-year growth in data center-related revenue, and guidance for FY2026 Q3 indicates further significant new highs. For Micron, AI storage is no longer a distant vision but a revenue source reflected in the current quarterly report.

SK Hynix's report is even more direct. According to the company’s announcement, 1Q26 revenue was 52.5763 trillion won, with operating profit of 37.6103 trillion won and an operating profit margin of 72%. The company stated that growth was driven by high-value products such as HBM, high-capacity server DRAM modules, and eSSD. For investors, this profit margin reflects a combination of product structure, supply-demand gap, and pricing power entering the report.

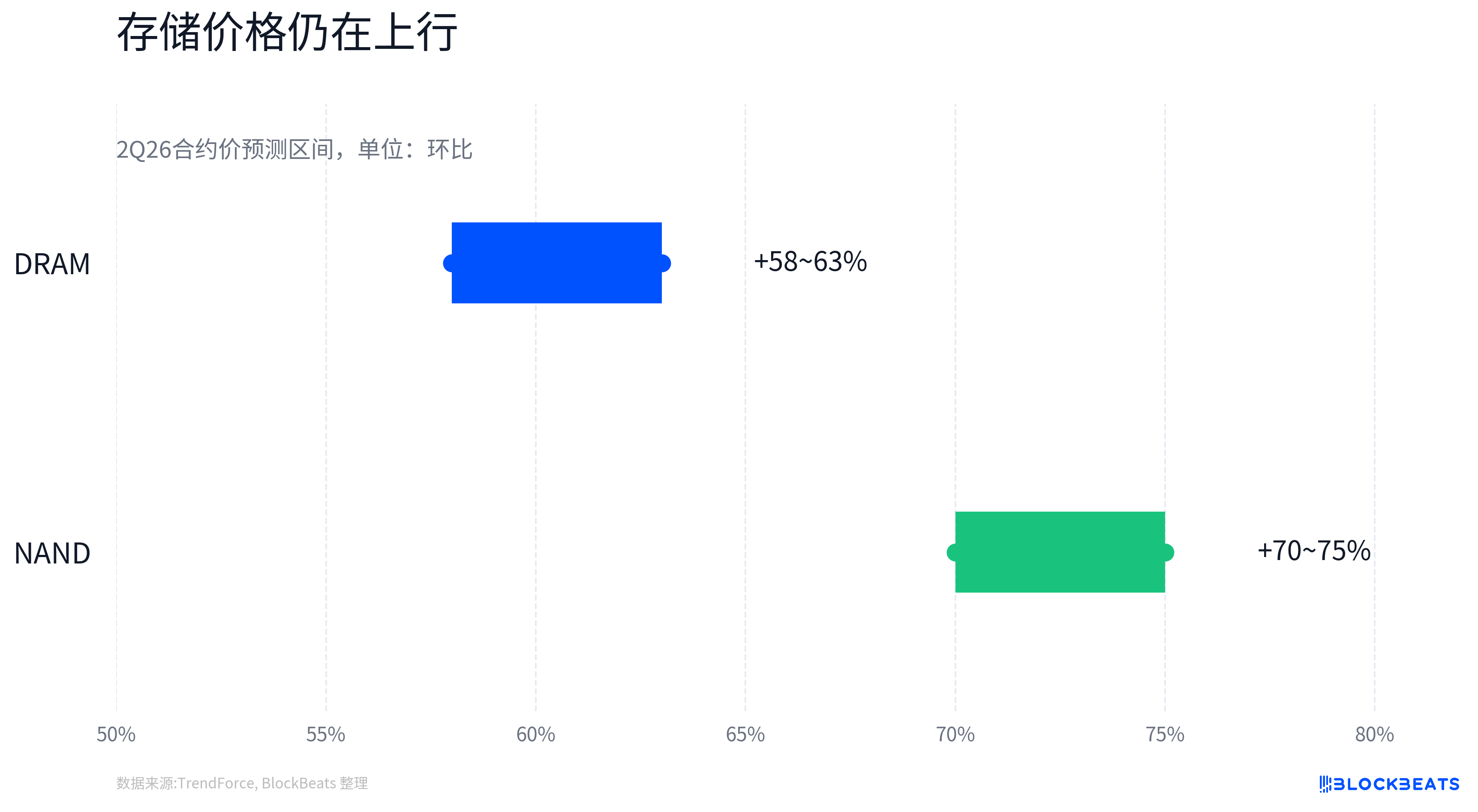

Industry price data also supports the same logic. TrendForce projects that 2Q26 conventional DRAM contract prices will increase by 58% to 63% quarter-on-quarter, and NAND Flash contract prices will rise by 70% to 75% quarter-on-quarter. Their report also indicates that 1Q26 DRAM industry revenue grew by 81% quarter-on-quarter.

Price does not equal profit, but in a phase of supply shortages, product mix upgrades, and strong demand, rising prices will improve the market's modeling of EPS for the upcoming quarters. South Korean export data also provides early verification at the industry level. According to Reuters and South Korean media, South Korea's exports hit a record in May 2026, with semiconductor exports increasing by 169.4% year-on-year to approximately $37.16 billion, with chips accounting for over 40% of total exports for the first time.

This cannot be directly equated to SK Hynix or Samsung Electronics' earnings per share but indicates that the storage industry's prosperity has been reflected in the accelerated revenue at the national export level.

Storage is not a stronger narrative, but a faster validation

In this round of revaluation, the difference between storage and other AI semiconductor directions is not whether there is growth, but how that growth is validated.

Nvidia remains the overall valve of AI demand. GPU platform iterations determine AI server architectures, HBM capacity needs, and supply chain qualifications. However, the market is already highly familiar with Nvidia's growth and profits, and valuations have long concentrated on the strongest AI assets. In the short term, it is more susceptible to export controls, supply chain constraints, platform switching rhythms, and expectation gaps.

The ASIC direction also has real logic. Cloud vendors' self-developed chips, custom accelerators, and rising AI inference demand all drive the long-term potential of assets like Broadcom and Marvell. But ASICs resemble project-based businesses; customer concentration, single project onboarding rhythms, mass production windows, and next-generation platform switching will influence market assessments of revenue visibility.

Optical modules and copper connections also have EPS realization pathways. Companies such as Coherent and Credo benefit from bandwidth upgrades within AI clusters, and changes in 1.6T, 3.2T optical modules and cluster interconnect architectures will bring demand. But pricing in these directions is more reliant on future architectural routes, customer certifications, shipping rhythms, and capital expenditure cycles. When the market is willing to offer premiums, their elasticity is strong. When market validation is required, they are also more susceptible to questioning when orders will translate into revenue.

In contrast, the current pricing basis for storage is more direct. HBM demand drives high-end products, capacity shifts compress the supply of traditional DRAM/NAND, contract price increases improve revenue, and product mix shifts elevate gross margins, ultimately translating into EPS.

This chain does not mean there are no risks, but it is easier to validate than "a certain next-generation architecture will bring large-scale orders." This is what makes storage more amenable to modeling. It does not imply that storage is more important than GPUs, ASICs, or optical modules, but rather that in this phase of AI semiconductor de-risking, the market favors assets that can be validated through prices, orders, profit margins, and export data.

EPS logic is strengthening, but it has not yet become a consensus

A one or two day rebound cannot prove that AI semiconductor trades have completely shifted from PE expansion to EPS validation.

Micron's near 13% drop on June 5, followed by a nearly 10% rebound on June 8, might include technical corrections, short covering, and a warming of risk appetite. SK Hynix's rise was also catalyzed by news related to collaboration with Nvidia's data center. News, positions, and fundamentals are often compounded in short-term market movements, and not all increases can be attributed to EPS certainty.

Storage itself remains a cyclical industry. Rapid increases in DRAM and NAND prices will improve supplier profits, but they may also stimulate supply expansion or suppress purchasing intentions among some end clients. Changes in the annual contracts, yield ramp-ups, customer qualifications, and share allocation for HBM are still in flux, and it cannot be simply assumed that all price increases will seamlessly enter the income statement.

SK Hynix and Micron are already highly sought-after AI storage targets in the market, and their stock price elasticity does not always synchronize with their fundamental elasticity. If the rate of price increases for DRAM/NAND slows, or if HBM share falls short of expectations, or if customer reorders are disproven, the EPS revision logic will also be challenged.

Conversely, this does not negate the potential of ASICs, optical modules, copper connections, and equipment materials. If these areas provide stronger orders, clearer customer onboarding, or better-than-expected guidance, the market may still assign valuation premiums anew. AI semiconductors are not limited to just storage; rather, at this current stage, storage can more easily explain through reports why it should be bought back.

A more prudent judgment in this round of market conditions is that the plunge on June 5 raised the market's verification threshold for AI assets. Corrections on June 8 to 9 indicated that funds within the AI chain prefer sections with a shorter EPS realization path. Storage happens to be in a position where orders, prices, capacity, and profit margins are all visible at the same time.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。