This article is from:a16z crypto

Translated by|Odaily Planet Daily ( @OdailyChina ); Translator|Moni

Tokenized Assets, commonly referred to as "Real World Assets (RWA)," are changing the forms, liquidity, and the construction of financial systems for assets.

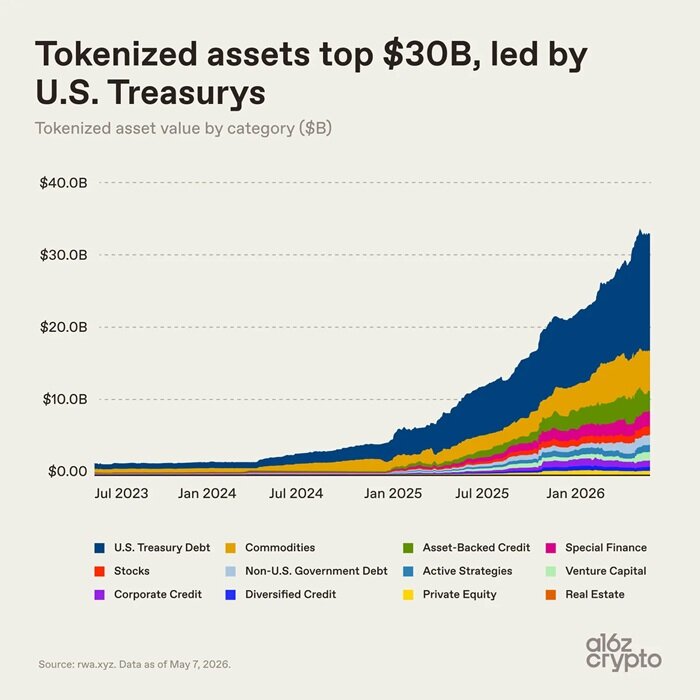

Just last month, the market size for tokenized assets surpassed $30 billion and is currently stabilizing at around $34 billion (excluding stablecoins). This scale is roughly equivalent to that of a regional bank or a top university endowment fund. Although still very small compared to the global financial system, it has produced a significant impact.

It's noteworthy that two years ago, the market size for tokenized assets was less than $3 billion, but since then, seismic changes have occurred in the market: the U.S. GENIUS Act has provided a clearer regulatory framework for stablecoins, institutional-level on-chain infrastructure is gradually maturing, and many financial institutions began deploying blockchain technology almost simultaneously—driven by these factors, the tokenized asset market has grown tenfold in less than two years. (Note: Although stablecoins are not included in the aforementioned statistics, they have substantially contributed to market growth by greatly simplifying on-chain payments and settlements.)

This article will analyze the reasons behind the rise of tokenized assets and their future trajectory through seven charts.

The Takeoff of Tokenized Assets: U.S. Treasuries as the Biggest Growth Engine

U.S. Treasuries are the main driving force behind the recent growth of the tokenized asset market.

The advantages of tokenized U.S. Treasuries are clear and intuitive: investors can hold stable, income-generating assets in digital form, and trading is more efficient and flexible; financial institutions can improve settlement and collateral asset allocation efficiency, seamlessly connecting to the digital financial market.

Crypto investors can also utilize tokenized government bonds to activate idle stablecoins and earn traditional currency market returns, prompting asset management institutions like BlackRock and Franklin Templeton to position themselves, creating a market worth hundreds of billions.

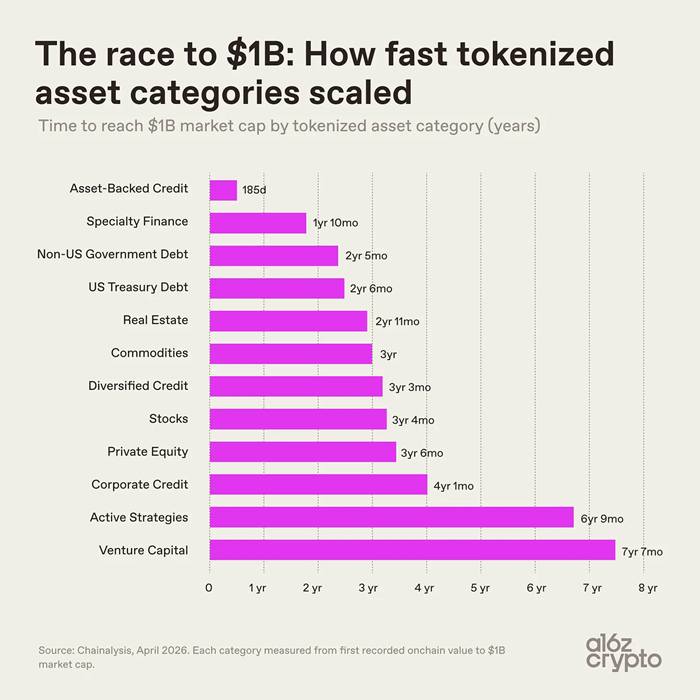

It is important to note that the growth rate disparities among various tokenized assets stem from the differing technical and compliance difficulties of bringing different assets on-chain, as well as the market acceptance after product rollout.

- The growth rate of asset-backed credit assets far outpaces others, with these tokenized assets mainly including home equity credit token, lending vault tokens, reinsurance contracts, Bitcoin mining receipts, and other specialized financial assets, with a market cap of $1 billion achieved within two years.

- Venture capital-type assets took over seven years to surpass a market cap of $10 billion, with actively managed assets taking a similar timeframe. These assets have complex structures and long investment cycles, with higher operational and regulatory barriers.

- The on-chain pace for government bonds and commodities is moderate, breaking the $10 billion mark within 2 to 3 years, and they are now mainstream categories in the market.

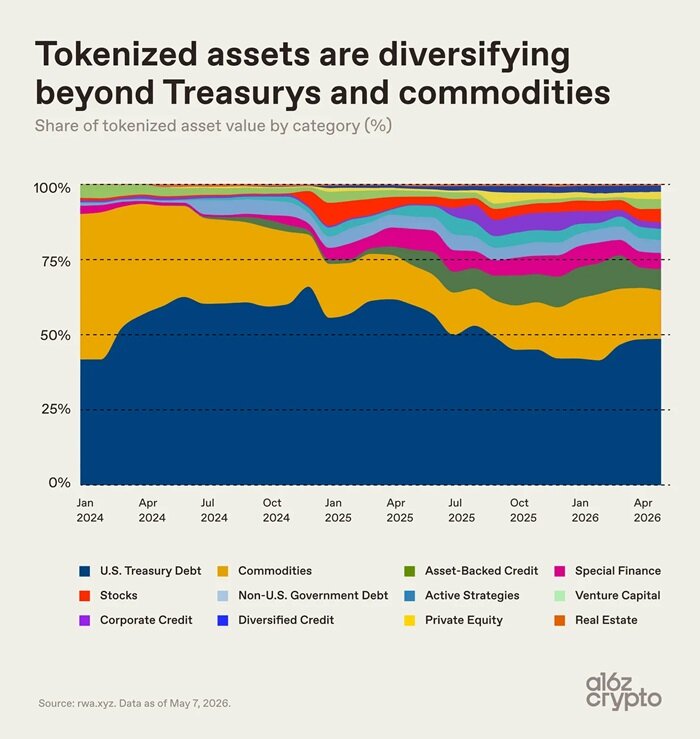

By early 2024, government bonds and commodities will nearly account for all tokenized asset market share. After 2024, the shares of credit, specialized finance, and stocks will steadily increase, but market concentration will remain relatively high. Currently, U.S. tokenized government bonds and commodities together occupy about two-thirds of the market share.

Market Segmentation of Tokenized Assets

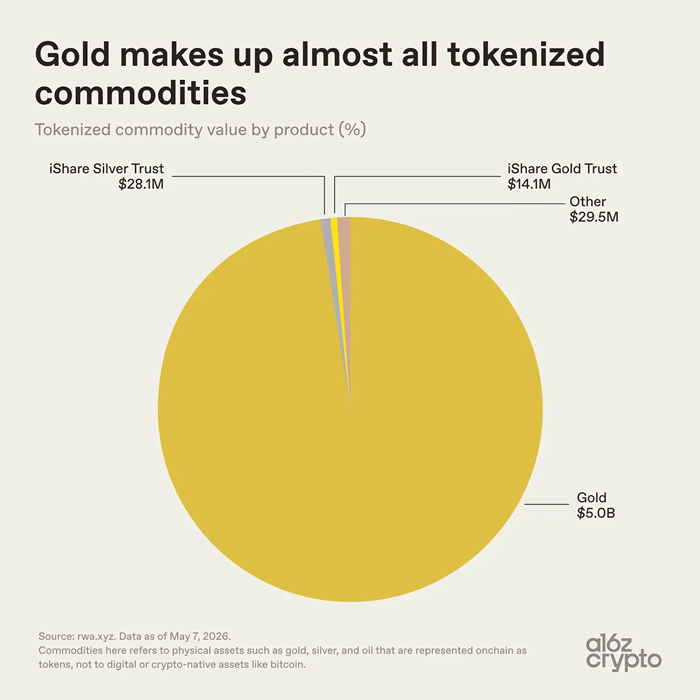

The commodity tokenized asset track is highly concentrated internally, with gold tokens dominating the vast majority of the share, totaling approximately $5.1 billion, of which gold tokens amount to $5 billion. Silver and other category tokens only account for $57.6 million, making up less than 0.01%.

Gold naturally fits the tokenized asset model, and currently, the commodity token market is mainly led by gold due to its globally uniform standards, easy storage, low wear, and its reliance on rights certificates for trading for a long time.

Moreover, crypto market investors have historically favored gold assets, with Bitcoin being dubbed digital gold in its early years. Products like Tether's gold token XAUT and Paxos' gold token PAXG map the ownership of gold in the vault to the blockchain, converting physical gold rights into digital tokens that can be held in on-chain wallets.

The market share of tokenized assets in oil, agricultural products, and emerging categories like energy and computing power is extremely low, and the industry is still in its infancy.

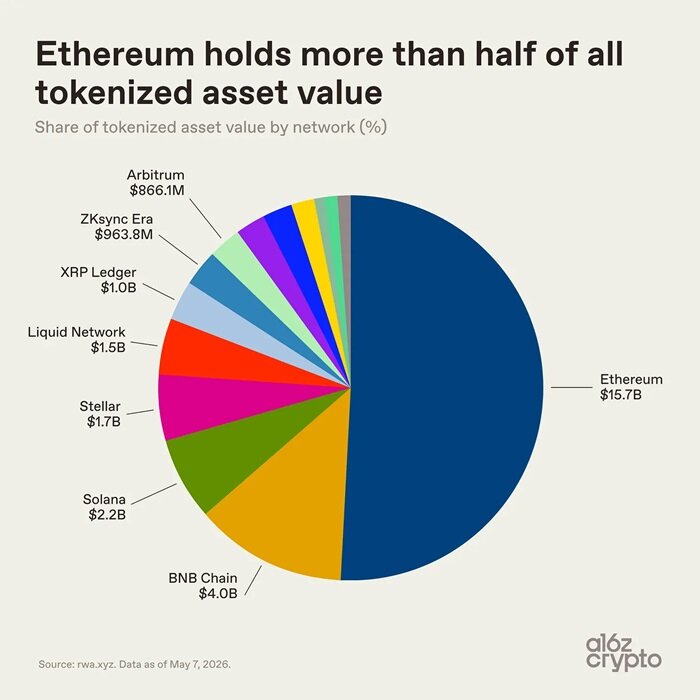

From the perspective of underlying public chain layouts, the ecology of tokenized assets is more diverse. Ethereum maintains its leading position with its early advantage in decentralized finance and institutional landing, carrying an asset scale of $15.7 billion, commanding over half of the market share.

The remaining tokenized asset market is dispersed across several public chains: BNB Chain's tokenized asset market is about $4 billion, Solana around $2.2 billion, Stellar about $1.7 billion, and Bitcoin's sidechain Liquid Network about $1.5 billion, with XRP Ledger, ZKsync Era, and Arbitrum's on-chain tokenized assets each approaching $1 billion.

The tokenized asset industry has not been unified under a single public chain; assets are distributed across various blockchain ecosystems based on transaction costs, liquidity, compliance requirements, and business partnerships. However, the most telling data point is not the scale of the tokenized asset market but rather how these assets are used.

Let us continue analyzing—

Most Tokenized Assets Currently Lack “Composability”

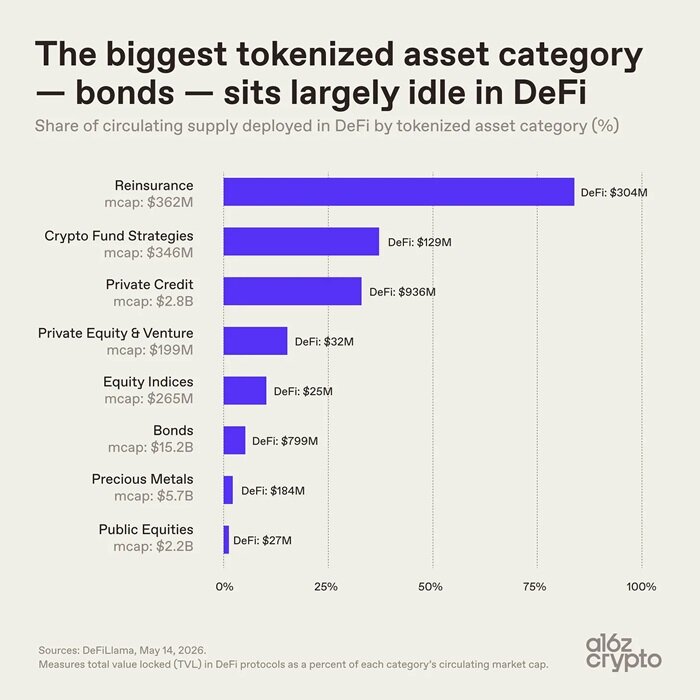

Market size is not the only core indicator; the practical application value of assets holds more significance.

Bonds are the largest category of tokenized assets, with a market cap of $15.2 billion, but only 5% of the circulation is applied in DeFi protocols, amounting to approximately $800 million. The utilization rate of precious metal tokenized assets is similarly sluggish, with most tokenized assets used merely for on-chain storage, and have not yet become freely combinable financial basic modules.

In contrast, niche tokenized asset categories show completely different performances: the $362 million market cap in reinsurance tokens has a 84% on-chain protocol usage rate; private credit tokens have a utilization rate of 33%, with these two asset types designed from the outset to fit on-chain combinatory application scenarios. In contrast, top tokenized assets like government bonds and gold primarily simplify on-chain holding and transfer, without altering the original operational logic of the assets. This situation highlights a core divergence in the tokenized asset industry: the degree of on-chain native characteristics varies widely across different tokenized assets.

Some assets can flow freely across chains, while others merely use blockchain as a bookkeeping tool, limited in asset transfer and combinability functions. Most tokenized assets currently are essentially just digitalizations of assets, merely transferring the bookkeeping to the chain, without unleashing the combinative potential of the assets. Composability is the core value of on-chain finance and key to upgrading the financial system.

The Pantera Capital token native index shows that over 70% of tokenized assets are at the lowest level of on-chain native characteristics. A large number of tokens are simply digital certificates of offline physical assets, with actual asset control still relying on offline ledgers and intermediaries.

The tokenized asset industry remains in the early stages of development: one type is merely digital record assets on-chain, while the other type consists of deep-rooted on-chain assets that align well with blockchain characteristics.

The infrastructure for on-chain composability technology is already complete, and asset categories are gradually enriching, but deep integration applications are just beginning.

Future Development Trends of Tokenized Assets

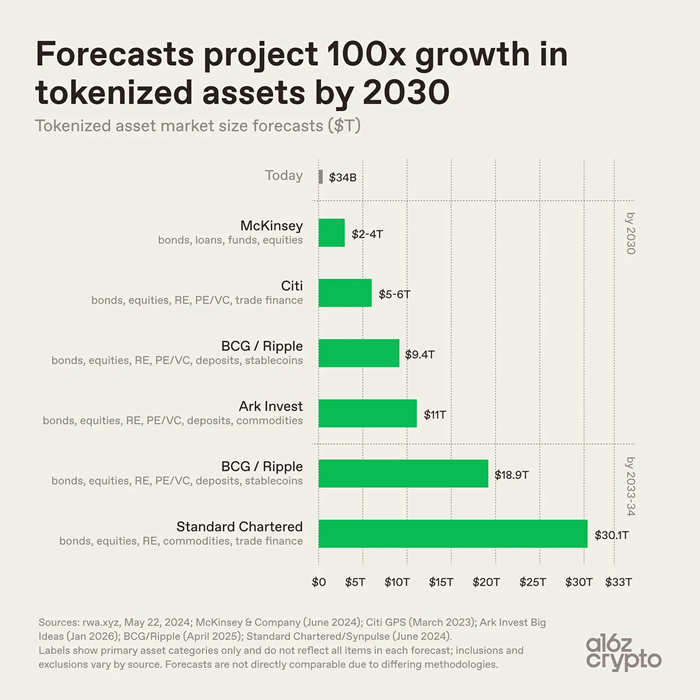

Industry predictions for the long-term scale of the tokenized asset market vary, but in general, they all judge that the market will continue to expand.

- McKinsey predicts that the market size of tokenized assets will reach $2 to $4 trillion by 2030;

- Ark Invest estimates the market size of tokenized assets to be $11 trillion;

- Boston Consulting, in conjunction with Ripple, calculates that the market size of tokenized assets will reach $9.4 trillion by 2030, climbing to $18.9 trillion by 2033;

- Standard Chartered predicts that the tokenized asset market will break $30 trillion by 2034.

Based on these institutional estimates, relative to the current market size of $34 billion, the long-term growth potential of the tokenized asset market can reach a hundredfold. Of course, the numerical differences do not stem from divergent predictions of industry adoption speeds, but rather from differences in statistical definition standards. Different institutions have variances in scope of statistics, including asset categories, whether stablecoins and deposits are counted, and the definition of tokenization. For example: McKinsey's statistics focus on bonds, credit, funds, and stocks; Standard Chartered includes commodities and trade finance; Boston Consulting and Ripple additionally include deposits and stablecoins. However, despite differences in statistical metrics, the industry widely recognizes that the scale of tokenized assets is set to expand significantly.

Looking at the global financial landscape, the current size of tokenized assets remains negligible.

- The total scale of global bonds exceeds $140 trillion, with tokenized bonds amounting to just $15.2 billion, accounting for 0.01%;

- The total market value of global physical gold reaches trillions of dollars, with tokenized gold at $5 billion, accounting for less than 0.02%;

- The total market value of global stocks exceeds trillions of dollars, with tokenized stocks at $1.5 billion, accounting for only 0.001%.

Now, emerging tracks have already taken shape steadily, with assets such as U.S. Treasuries, gold, and private credit, which have clear pricing, stable demand, and simple ownership, being the first to complete their on-chain implementation. Currently, tokenization has yet to disrupt the underlying attributes of assets, only optimizing the methods of asset settlement and transfer; the deep integration of assets with the digital financial system is still exploratory.

Currently, tokenized assets remain primarily at the digitalization level, struggling to achieve programmable combined applications. The next stage of the industry faces hardcore challenges: to bring more complex parts of the financial system on-chain and to integrate tokenized assets deeper into a composable, internet-native financial infrastructure.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。