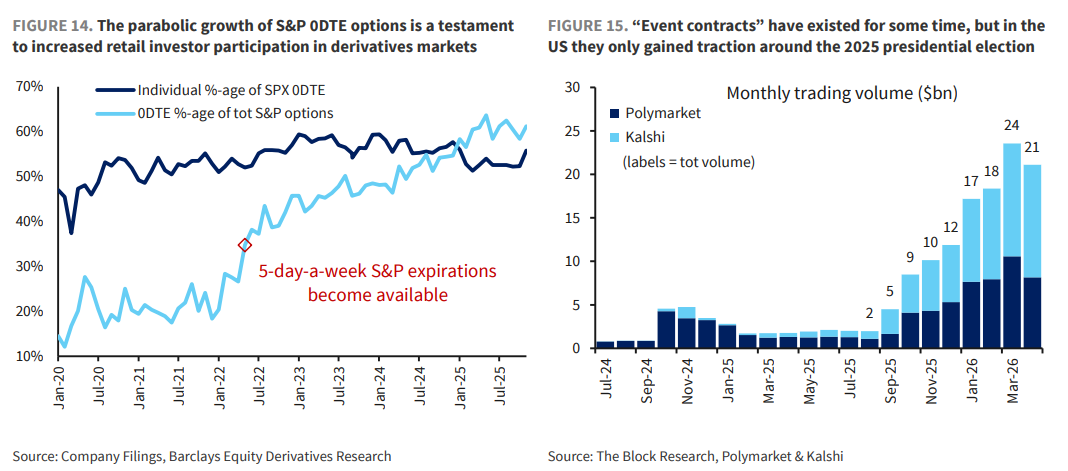

Risk budgets are quietly flowing into prediction markets, with Kalshi and Polymarket's monthly trading volume soaring from 5 billion to 20 billion dollars over the past year.

Written by: Zhao Ying

Source: Wall Street Insights

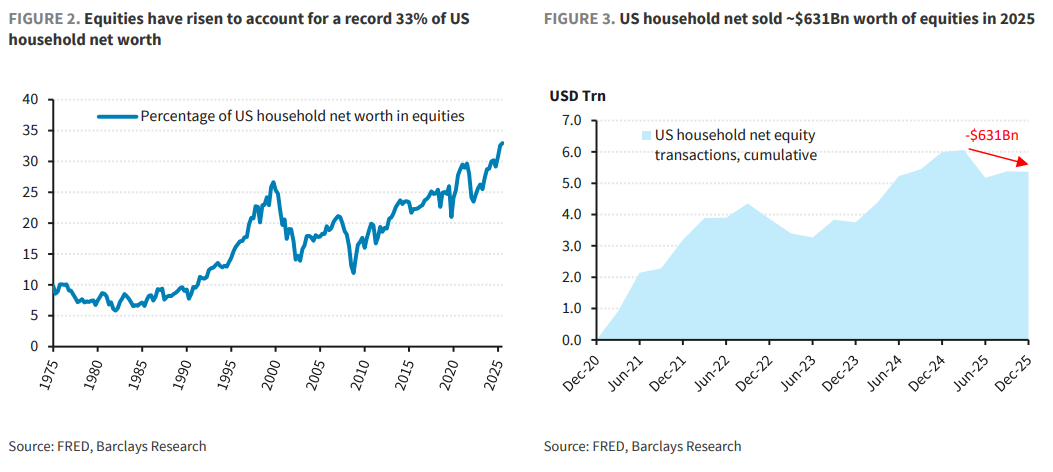

The story of retail investors in the U.S. stock market is changing. It's not that individual investors are completely exiting, nor is there another round of GameStop-like frenzy, but rather that long-term allocations remain, while short-term speculation is retreating. U.S. households' exposure to stocks is still high, but in 2025, the household sector net sold about 631 billion dollars of stocks while simultaneously adding about 1.4 trillion dollars in cash-like assets in the fourth quarter, making it difficult to support the narrative of "everyone chasing the rally".

According to the Wind trading desk, Barclays U.S. stock strategist Venu Krishna and others expressed this judgment in their latest research: "Retail investors have reengaged, but they cannot yet be said to have returned." This statement captures the essence: in April, nearly 80 billion dollars flowed into U.S. stock funds, likely containing considerable retail funds; however, compared to the peaks of 2024 and 2025, participation has not fully returned, especially among those willing to use leverage, chase hot trends, and engage in short-term trading, who are evidently more cautious.

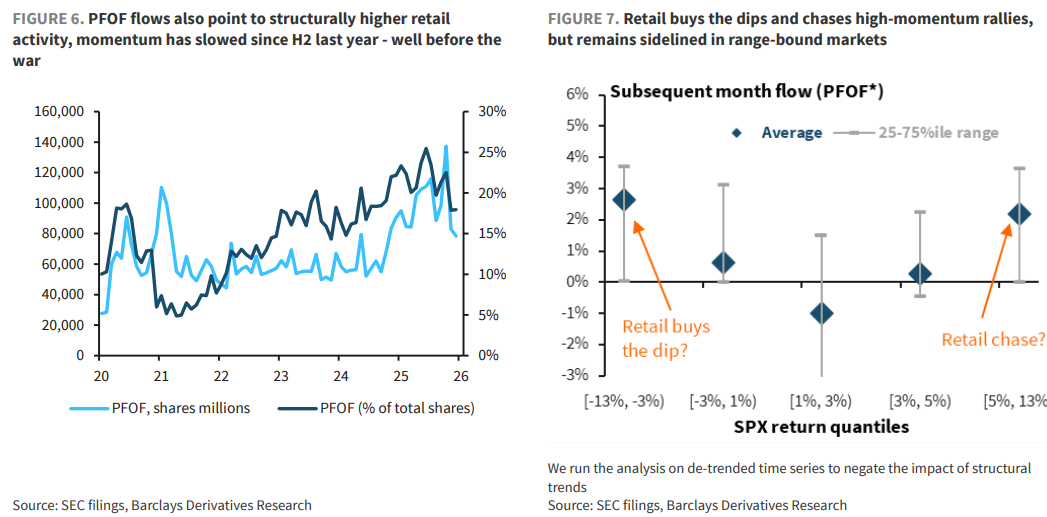

The real change is structural. Low-cost index ETFs continue to experience stable inflows, with funds for retirement accounts, systematic investment plans, and long-term allocations remaining unbroken; however, leveraged long index ETFs have seen outflows, and inflows into leveraged single-stock ETFs have slowed. PFOF data shows that retail trading momentum has also begun to cool since the second half of last year. This is not simply about retail investors "not buying stocks," but rather that the risk budgets previously allocated for high turnover and high speculation may have been redirected.

Redirected where? One new destination is the prediction markets. Kalshi and Polymarket's nominal monthly transaction volume has risen from less than 5 billion dollars a year ago to about 20 billion dollars now. The scale is still far smaller than the S&P 0DTE options, but it is no longer a small toy. In the coming months, if prediction markets and sports betting and other non-financial speculative channels cool off seasonally, some funds may return to the stock and options markets; but whether this can be sustained will ultimately depend on whether consumer confidence can recover.

Stocks account for a record high of household net worth, but buying pressure is not strong

As of the end of 2025, the proportion of stocks in U.S. household net worth has risen to a record 33%. On the surface, this indicates that retail investors are embracing stocks; however, looking deeper, the logic is the opposite: the household sector net sold about 631 billion dollars of stocks throughout the year. On a rolling basis in the fourth quarter, this represents the most significant net outflow since the second quarter of 2023; on an annual basis, it is the largest net outflow since 2018.

This means that household balance sheets have become "more stock-like," mainly due to market gains, rather than households accelerating their purchases.

This does not contradict the expansion of retail investors following the zero-commission trading in 2019-2020. Zero commissions indeed raised the baseline for retail participation in the U.S. stock market, transforming retail investors from sporadic participants into forces influencing short-term prices, options demand, and fund flows. However, the marginal pricing behavior is changing: retail investors are still in the market, but they are not acting with as much fervor as in the previous years.

The reflex of "buying the dip and chasing the rise" has slowed down

Long-term data shows that retail investors have two habits when it comes to buying stocks: one is being more active at the beginning of the year, with capital flows often concentrated in the first half; the other is preferring to act during two types of markets - buying the dip after significant drops or chasing trends during strong upward movements. Sideways fluctuations tend to be the most challenging to stimulate trading desires.

The problem is that from the second half of 2025 to the first quarter of 2026, this impulse to "buy the dip / chase the rise" has weakened. PFOF data has shown slowing momentum since the second half of last year, and this timing predates recent geopolitical shocks.

Household cash behaviors also reveal the same signal. Since 2022, the proportion of cash-like assets in financial assets has declined, seemingly indicating that cash is being consumed and risk appetite is increasing; however, the rise in risk assets itself compresses the proportion of cash. By the fourth quarter of 2025, U.S. households increased their liquid assets in checking accounts, savings, and money market funds by nearly 1.4 trillion dollars, of which 1.1 trillion dollars went into checking deposits. This resembles a re-raising of cash cushions rather than a full-scale offensive.

Consumer confidence is also not cooperating. The University of Michigan's consumer confidence is nearing historical lows, with the Conference Board's expectations index hovering below 80, a level historically often used to assess recession risks. Meanwhile, households' expectations of "whether stocks will be higher a year later" have become more volatile from 2025 to 2026. Unstable beliefs hinder decisive bottom-fishing.

What is retreating is not index allocations, but leveraged speculation

ETF fund flows offer a clearer view of layered retail investors.

Low-cost, highly liquid index ETFs continue to attract funds, with monthly net inflows approximately equivalent to 1% of fund assets. These funds resemble pensions, automatic deductions, and long-term asset allocations and are unlikely to withdraw quickly due to short-term sentiment changes.

What is weakening are speculative tools. In the fourth quarter of 2023 and the first quarter of 2024, leveraged long U.S. stock index ETFs experienced significant outflows, but during that time, leveraged single-stock ETFs saw accelerating inflows, indicating that the risk budget merely shifted from the index level to single-stock expressions. By the second half of 2025, the situation is different: leveraged index ETFs experienced renewed outflows while inflows into leveraged single-stock ETFs also began to slow.

This signals a colder message: high-speculation retail investors are not simply switching to another category of stock tools but may be withdrawing entirely from the stock market or reallocating their risk budgets outside of stocks.

Prediction markets have become a new outlet for speculation

The appeal of prediction markets is straightforward: using "yes/no" contracts to bet on the outcomes of specific events, with prices corresponding to the market's implied probabilities; those who bet correctly receive the entire nominal value. They are not like traditional stocks or standard options, but are essentially quite similar to digital options around event catalysts.

Kalshi and Polymarket's transaction volume is growing rapidly. Their monthly nominal transaction volume surged from less than 5 billion dollars a year ago to about 20 billion dollars so far this year. Around the presidential election, this type of "event contract" began to gain more attention and has not rapidly retreated thereafter.

Of course, it is still far from comparing with S&P 0DTE options. In March 2026, the nominal transaction size of S&P same-day options was about 57 trillion dollars, nearly equivalent to the entire market capitalization of the S&P; S&P 0DTE options now account for more than half of total S&P options transactions, whereas five years ago, they accounted for only about one-fifth.

However, compared to other retail speculation products, prediction markets are not insignificant. Their scale is comparable to some popular leveraged ETPs and can be roughly compared to certain index and single-stock options overlay strategies. More importantly, much of the prediction market transactions are related to non-economic events, such as sports betting, which means they may be competing for the same pool of "willing high-frequency bettors" for risk budgets.

April's inflow is real, but it is not a 2024/2025-style frenzy

After the ceasefire news between the U.S. and Iran at the end of March, retail investors seem to have returned to the U.S. stock market. In April, net inflow into U.S. stock funds approached 80 billion dollars, with a considerable portion almost certainly coming from retail investors.

However, this round of inflow has noticeable reservations. Households increased a large amount of liquid assets at the end of last year, indicating that risk appetite has not fully recovered; doubts about the sustainability of the rise remain. Recent movements in leveraged long and short QQQ ETFs show that some retail investors are more inclined to make contrarian trades on the V-shaped rebound driven by technology stocks, rather than unconditionally chasing in.

Short-term, there might be a potential window: the trading volume of political event prediction contracts often weakens in the summer, and sports betting revenues also decline after the NBA, NHL, NFL, and college basketball seasons. If these non-financial speculative channels cool off, some high-risk capital may flow back into financial markets, possibly igniting additional stock demand before the traditional off-season for funds arrives in the third quarter.

However, looking further ahead, the key is still consumer confidence. Improved financial conditions, resilient labor markets, and decreases in inflation and geopolitical uncertainties could reactivate broader retail participation. Conversely, energy shocks could be a drag: U.S. gasoline prices have exceeded 4 dollars for five consecutive weeks, and if disruptions in global energy markets continue beyond Memorial Day, demand destruction may become inevitable.

This framework does not portray the "return of retail investors" as a one-sided bullish stance. Using May 8, when the S&P 500 index was at 7399 points, as a benchmark, the year-end scenario estimates set a baseline target of 7650 points, corresponding to about 3.4% upside; the bull case would be 8200 points, corresponding to about 10.8% upside; and the bear case would be 5900 points, corresponding to about 20.3% downside.

This means that retail reengagement can provide incremental buying support, especially if high-speculation funds return from prediction markets, sports betting, and other channels, which might temporarily boost demand for risk assets. However, if consumer confidence continues to weaken and cash preferences remain high, retail investors will find it difficult to resume their previous roles of "buying the dips and chasing the rises." U.S. stocks still have retail investors, but the most aggressive segment is no longer as loyal to the stock market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。