Glassnode believes that the foundational conditions required for the cryptocurrency market to bottom out are already in place, but the core signals confirming the bottom have yet to appear.

Written by: CryptoVizArt, Frederik Theissen, Glassnode

Translated by: Luffy, Foresight News

The price of Bitcoin has remained below the real market average and short-term holder cost benchmarks for five consecutive months, in a state of deep undervaluation.

The current scale of long-term holders cashing out losses has risen to 43% of the total on-chain realized losses, with a single-day peak loss cash-out amount of $280 million, marking the highest level since December 2022. Spot ETF fund outflows have eased somewhat, but continue to maintain a monthly net outflow status; the daily trading volume of ETFs remains between $650 million and $950 million, shrinking about 80% compared to the peak market levels in October 2025, indicating that institutional buying demand has yet to stabilize.

The derivatives position structure has turned cautiously bullish, with the put/call ratio dropping to a low for 2026; however, the options volatility surface still maintains a defensive premium, with spot prices significantly below the maximum pain price level. The market has entered the later stages of bottoming, and the continued narrowing of selling pressure from long-term holders is a crucial prerequisite for a market reversal and recovery.

Macroeconomic Perspective

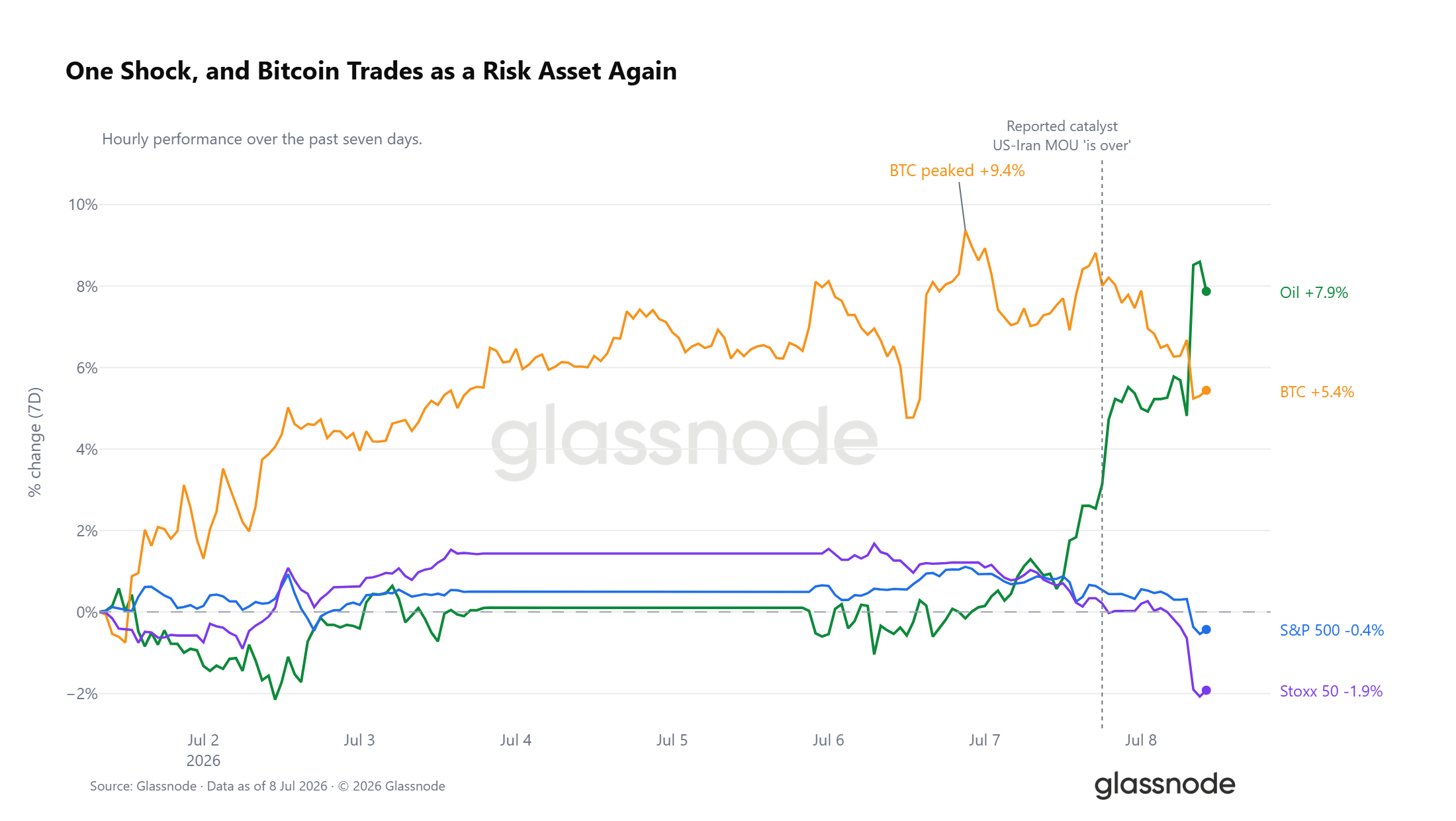

Surge in Crude Oil Prices, Risk Assets Under Pressure

Over the past seven trading days, WTI crude oil has accumulated a 7.9% increase, with most of the rise occurring recently. Reports suggest that the U.S.-Iran understanding memorandum has expired, and this shockwave has affected all asset markets. Bitcoin had risen as much as 9.4% this week, but is currently down to a 5% increase for the week; the S&P 500 and the STOXX Europe 600 index have all turned to decline, with European stocks leading global risk assets lower. At this stage, Bitcoin's trend is highly synchronized with risk assets.

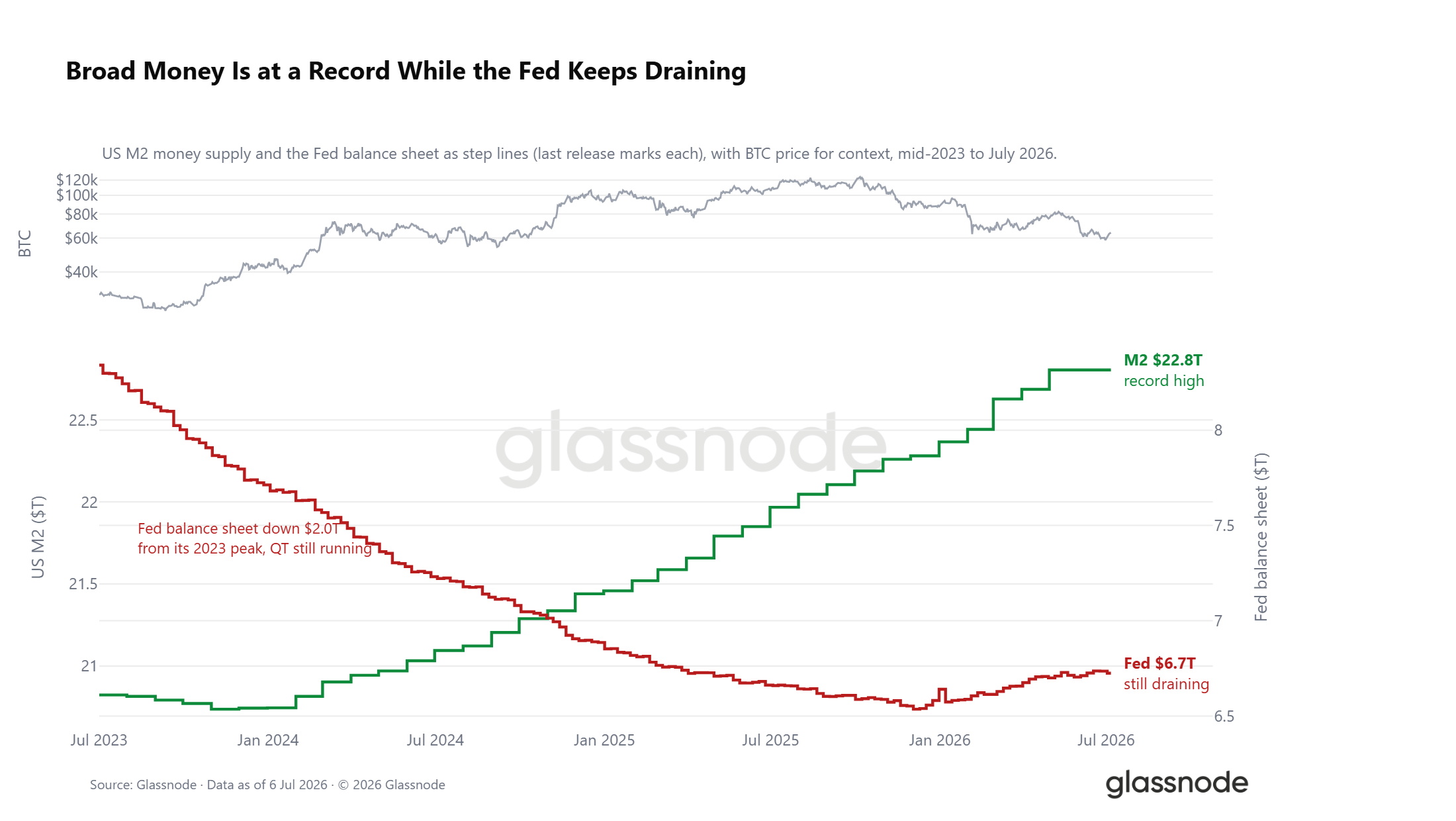

Liquidity Environment: Escalating Long-Short Discrepancies

Under the external shock from crude oil, the market's liquidity environment shows a tearing pattern. The total U.S. broad money supply M2 has surged to a historic high of $22.8 trillion; historically, broad money expansion cycles tend to boost market risk appetite. However, the Federal Reserve's balance sheet is still contracting, currently down by $2 trillion from its peak in 2023. These two liquidity signals form a strong hedge: the overall broad money continues to rise, while the quantitative tightening process has not stopped, with real interest rates hovering around 1%, resulting in a high opportunity cost for holding non-yielding digital assets. The positive macroeconomic window has not completely closed, but has also not formed a clear easing support.

On-Chain Data

Extended Period of Deep Undervaluation for Five Months

In the past week, Bitcoin rebounded from $58,300 to $64,400, showing short-term recovery, but the price remains significantly below the real market average of $76,600 and the short-term holder cost line of $72,200. Only by regaining the aforementioned two key price levels can the market exit the state of deep undervaluation; otherwise, it remains susceptible to declines triggered by external adverse factors.

The duration of this discounted market is particularly noteworthy. Since early February 2026, the price has consistently run below the active investor cost line and the breakeven line for recent entrants, lasting nearly five months—this is among the longest periods of deep discount in Bitcoin's history.

In the long-term discount range, the continuous turnover of chips has occurred, with new funds consistently positioned below the previous buyers and the market's active holding cost line, which has historically been the foundation for the formation of a cyclical bottom, presenting long-term appeal for value investors. Various indicators show that the bottoming process has entered the second half, but the possibility of a market retracement to $53,000 cannot be entirely ruled out.

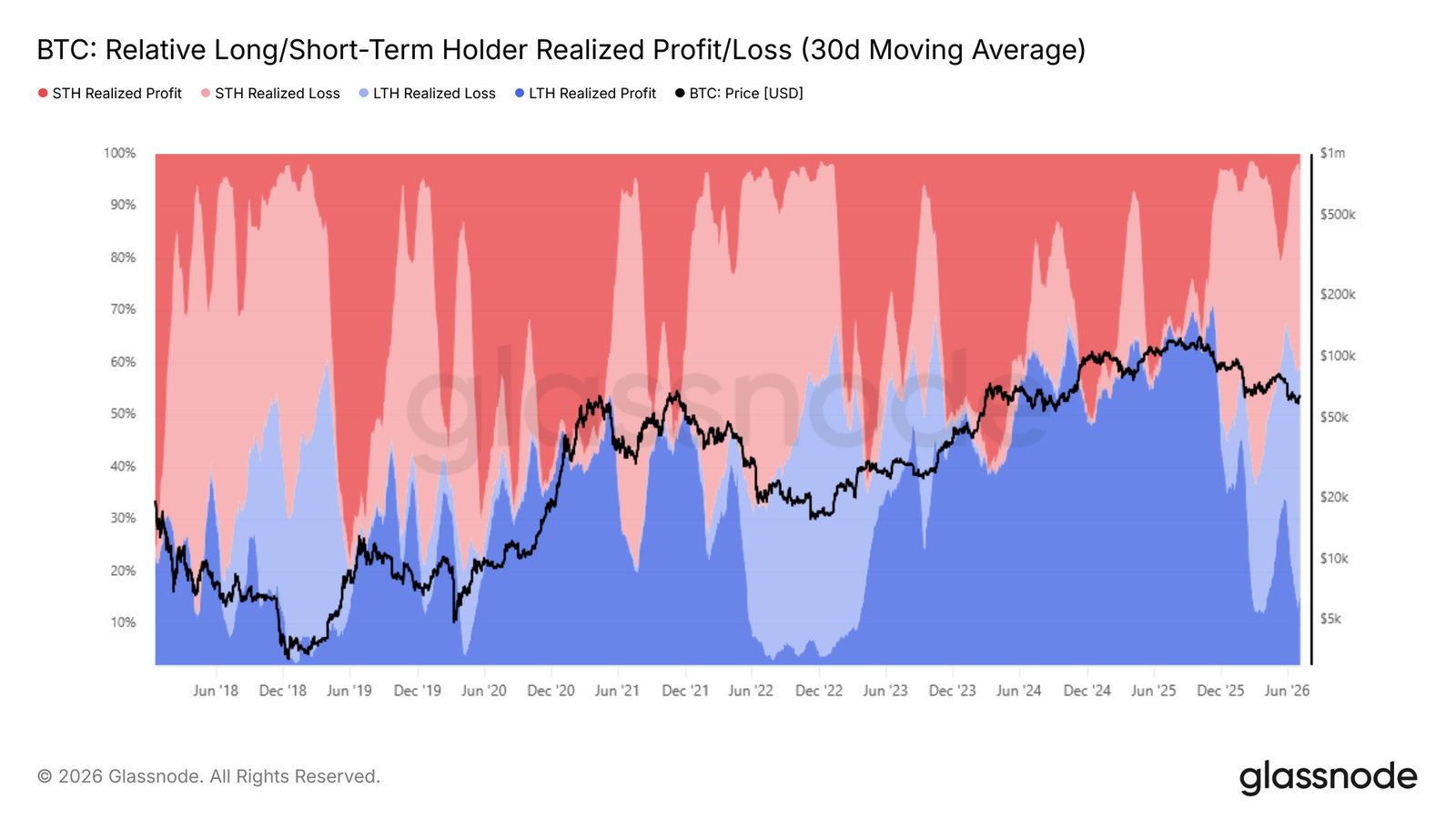

Long-Term Holders at High Positions Concentrating Stop Losses

The market is currently building a cyclical bottom, and the core question is to identify the primary source of downward selling pressure. The relative indicators of long and short holder realized gains and losses statistically reflect the distribution ratios of realized gains and losses across the entire market in long- and short-term holding groups, providing a direct view of the scale of realized gains and losses for these two types of chips.

When the price drops below the real market average, the cash-out amount of long-term holders’ losses, measured by the 30-day moving average, has risen from 15% in early February 2026 to the current 43%. The selling pressure generated by this group's unrealized losses has become the primary bearish force suppressing the price.

This group of investors mostly entered the market near cyclical highs, and after experiencing months of deep retracement, their confidence in holding has gradually worn thin, leading them to choose to exit all at once. This chip structure directly explains why every round of rebound has faced concentrated selling from deeply trapped positions, making it difficult for the price to stabilize at the upper edge of the current range.

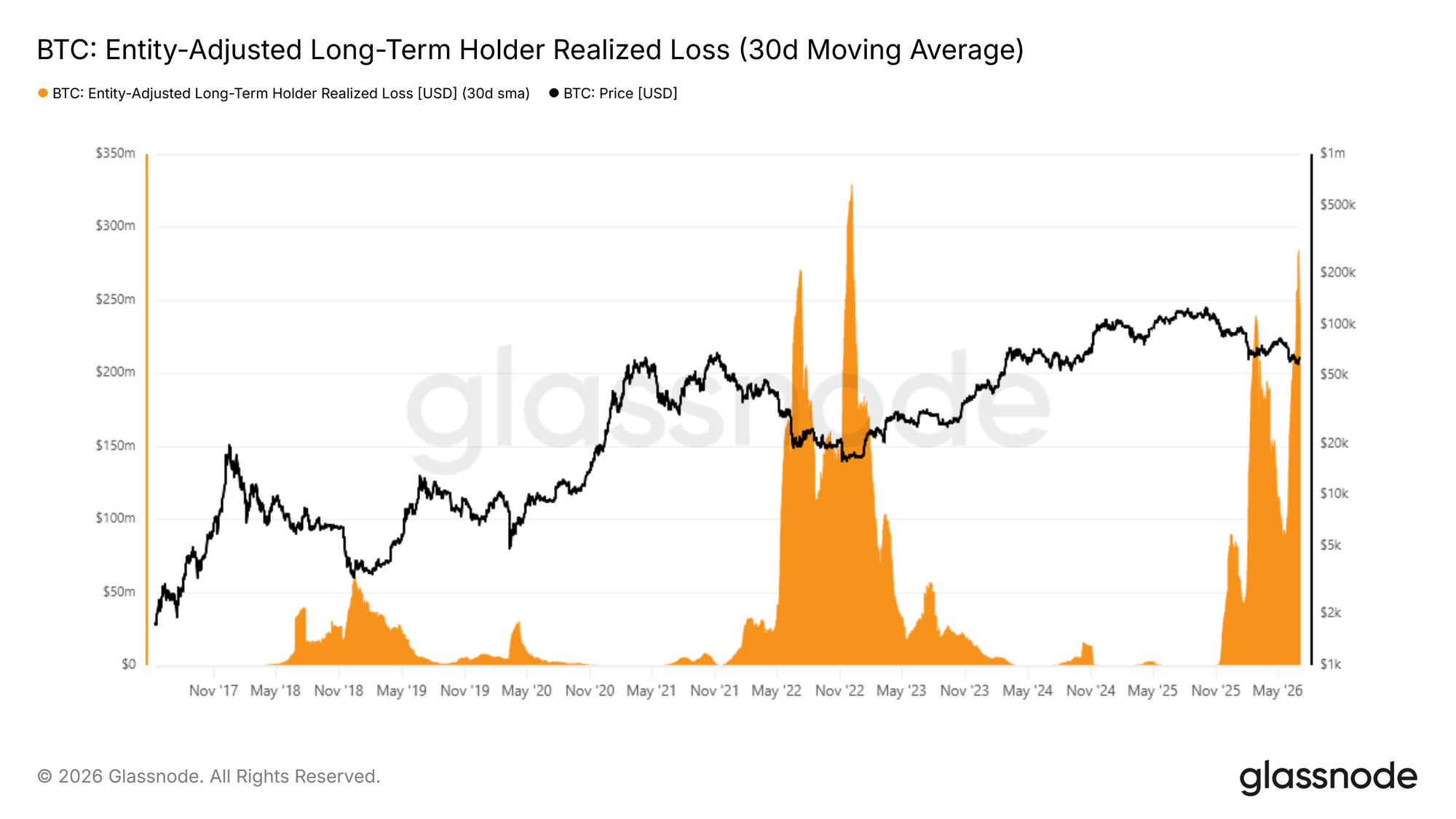

No Signs of Diminishing Stop Loss Selling Pressure Yet

The cashing out of losses by long-term holders has become a significant downward pressure on the market, with the next key observation indicator being whether this selling pressure will begin to wane.

The long-term holders that have adjusted have already realized loss metrics (30-day smoothed average) which statistic the amounts sold by users holding positions for over 155 days, excluding internal transfers, precisely reflecting genuine stop-loss exit behaviors. This metric recently reached a single-day peak, with daily loss cash-out scale reaching approximately $280 million, marking the highest level since December 2022 and representing a second wave of large-scale stop-loss among long-term holders in this bear market.

The key distinction is that after the first peak of stop-loss, the selling pressure showed a stage-wise decline, whereas this current wave of selling has yet to show any signs of scale reduction. Only with a significant downward movement in this metric can the market possess the foundational conditions necessary for a shift towards a bull market. In the coming weeks to months, the trend of this indicator will serve as the critical signal to determine whether the market has genuinely cleared the selling pressure.

Off-Chain Market

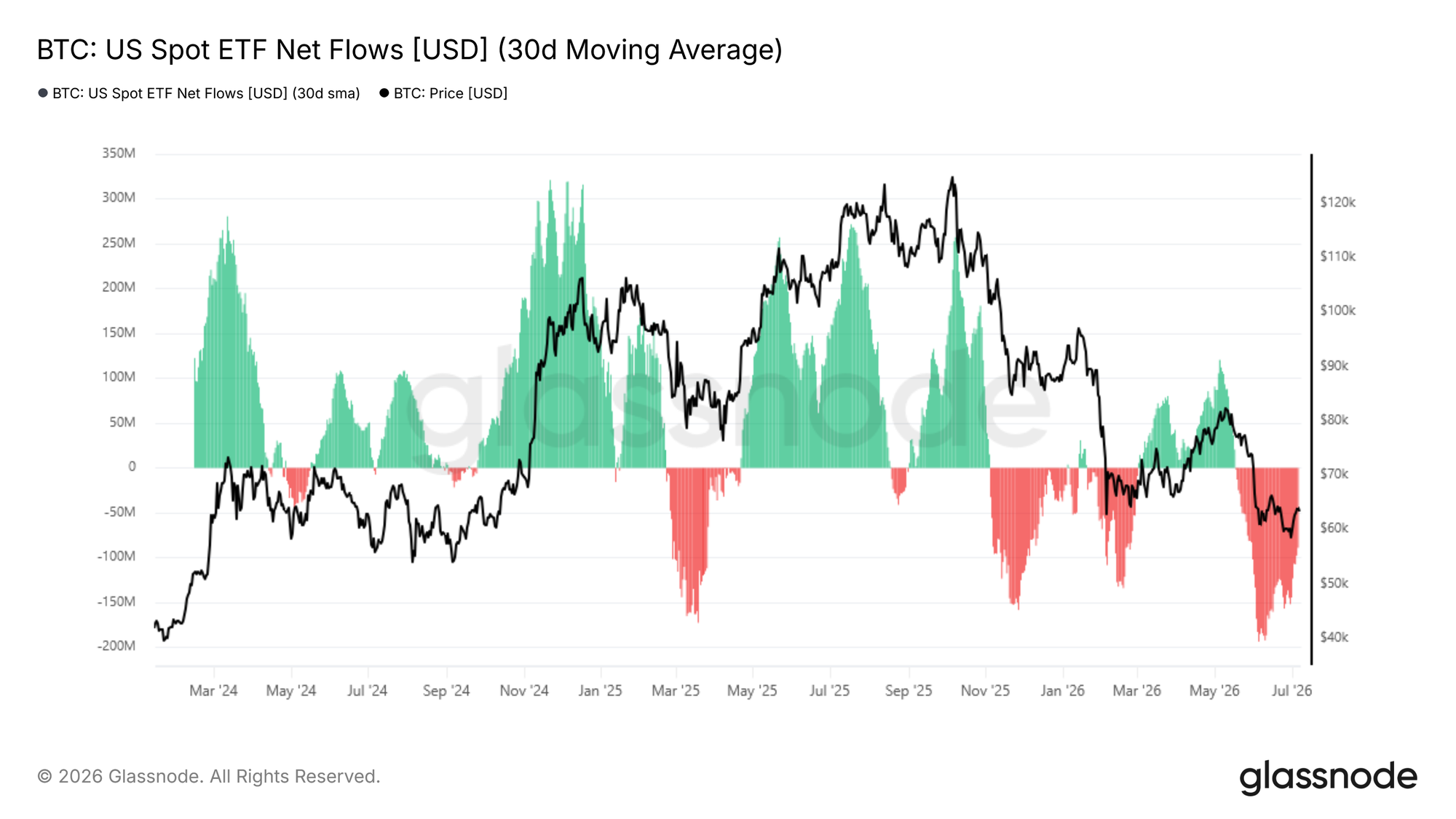

ETF Outflows Slow, but Outflow Trend Not Reversed

Shifting from on-chain to off-chain market, the flow of funds in spot ETFs can intuitively reflect institutional fund activities. The 30-day average of ETF net flows reflects the daily net inflows or outflows of the U.S. spot Bitcoin ETF, excluding single-day fluctuations, thereby revealing potential trends in institutional holdings.

Since mid-May 2026, this indicator has shifted into a zone of monthly net outflows, with a peak outflow of $193 million at the beginning of June, now receding to a single-day net outflow of $88.9 million. The slowing outflow scale is a slight positive, but the market continues to experience monthly financial hemorrhaging, and institutional buying demand has yet to stabilize. Only when the capital flow contracts continuously to a balanced range can there be grounds to predict short-term market expansion and price increases.

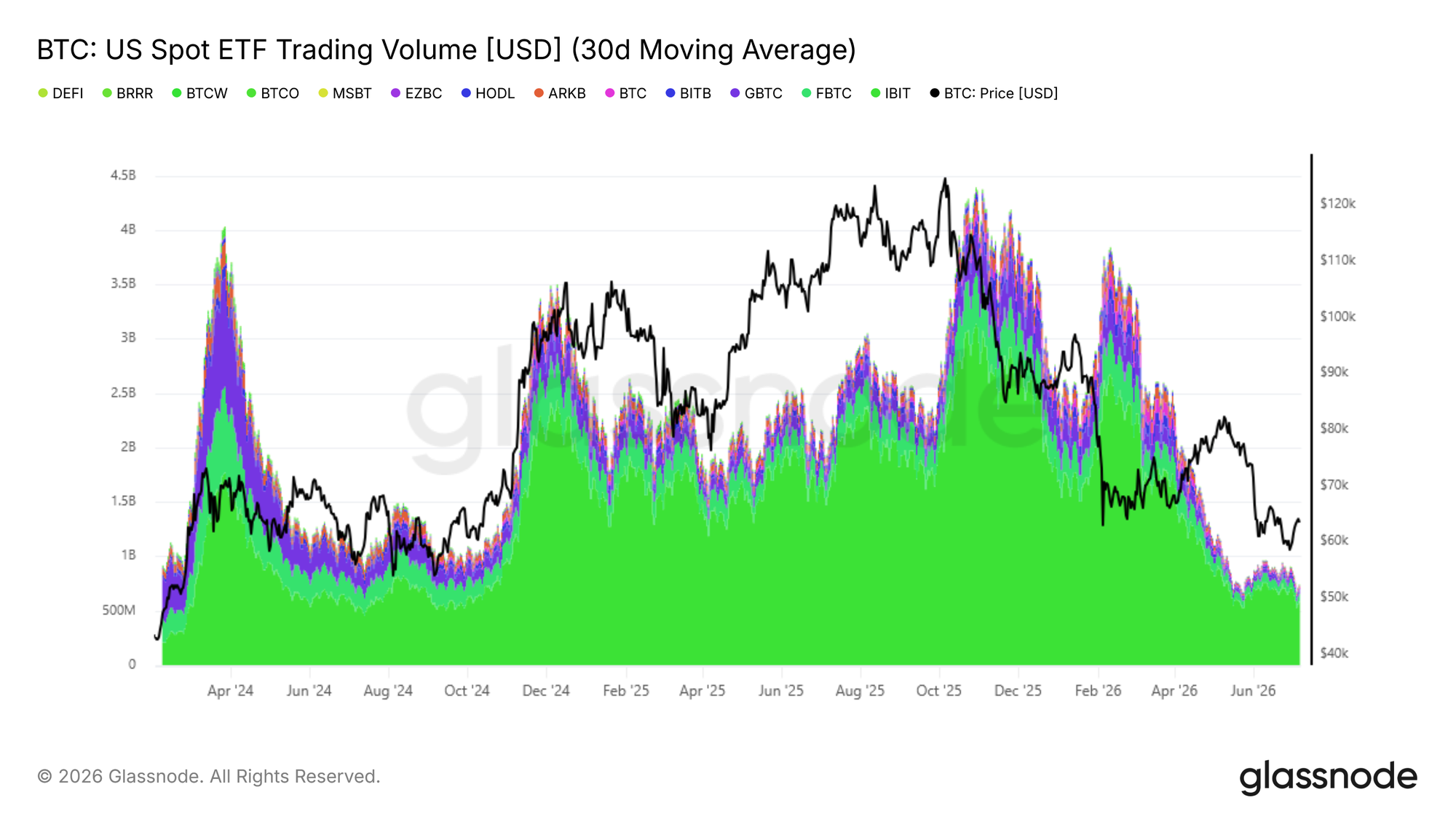

Institutional Trading Volume Still Dismal

Apart from net inflow data, the trading volume of U.S. spot ETFs can assist in assessing the extent of institutional confidence recovery. The 30-day average of daily trading volume for ETFs currently fluctuates between $650 million and $950 million, a level comparable to that of the fourth quarter of 2024, yet still about 80% lower than the daily peak of $4.4 billion set in October 2025.

The current trading scale merely represents the basic participation level of institutions and remains extremely low compared to the peak levels in a bullish market, indicating that long-term bullish confidence among ETF investors has not materially returned. Only with continuous increasing daily trading volume, alongside a continuous narrowing of net outflow scale, can both signals confirm that institutional demand is warming up. Until both indicators show synchronous improvement, the off-chain data and on-chain metrics will mutually corroborate, and the market as a whole will still be under a bear-dominated pattern.

Derivatives Market

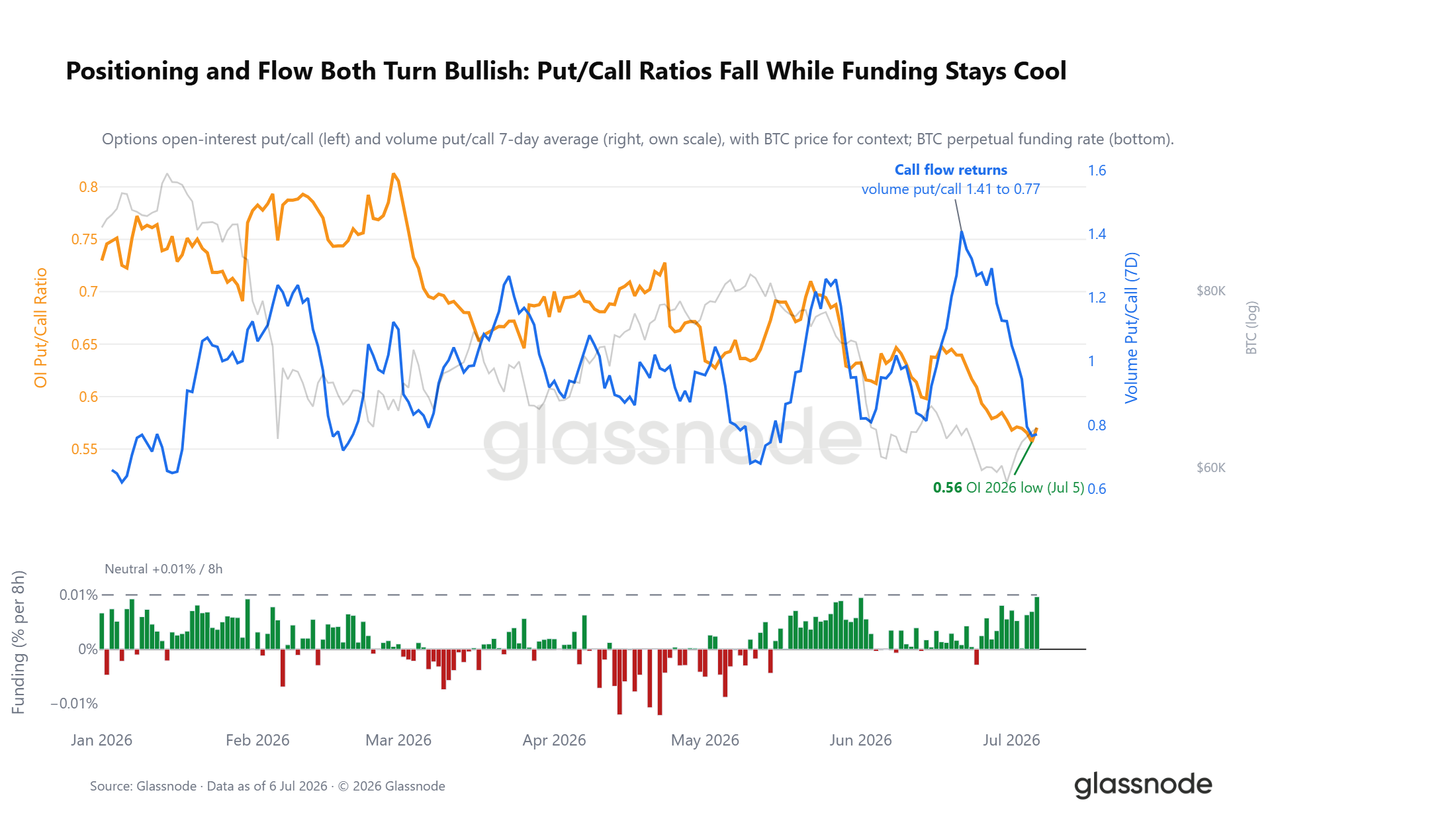

Bears Close Positions, Holdings Turn Cautiously Bullish

Under subdued risk sentiment, the structure of derivatives positions has shown an inverse change. The put/call ratio of options open interest has dropped to 0.56, the lowest level for 2026, with the market currently having two call options for every put option. The trading volume of options corroborates this trend: two weeks ago, when Bitcoin dipped to a low again, the market wildly bought put hedges, greatly increasing the put/call transaction ratio; as the call orders continued to return, this ratio quickly fell, even as spot prices only recovered part of their losses.

The perpetual contract funding rate also corroborates the shift in positions. The average funding rate for perpetual contracts has long been below the 0.01% long-short balance line, far from reaching a level indicative of overcrowded bullish conditions. The derivatives market has cleared bear risks and overall has turned cautiously bullish under external adverse shocks, contrasting sharply with the overcrowded short positions before the previous major downturn.

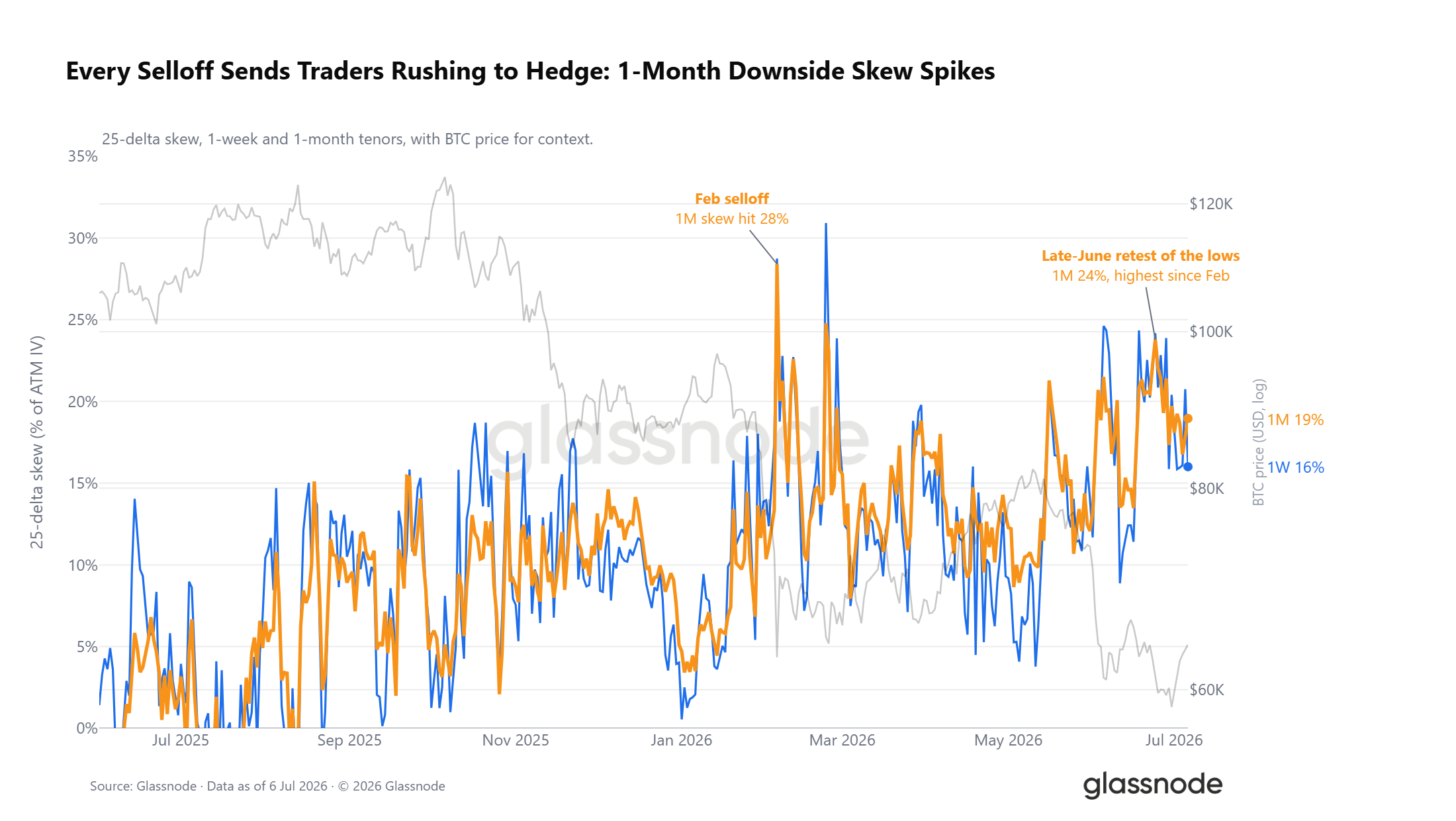

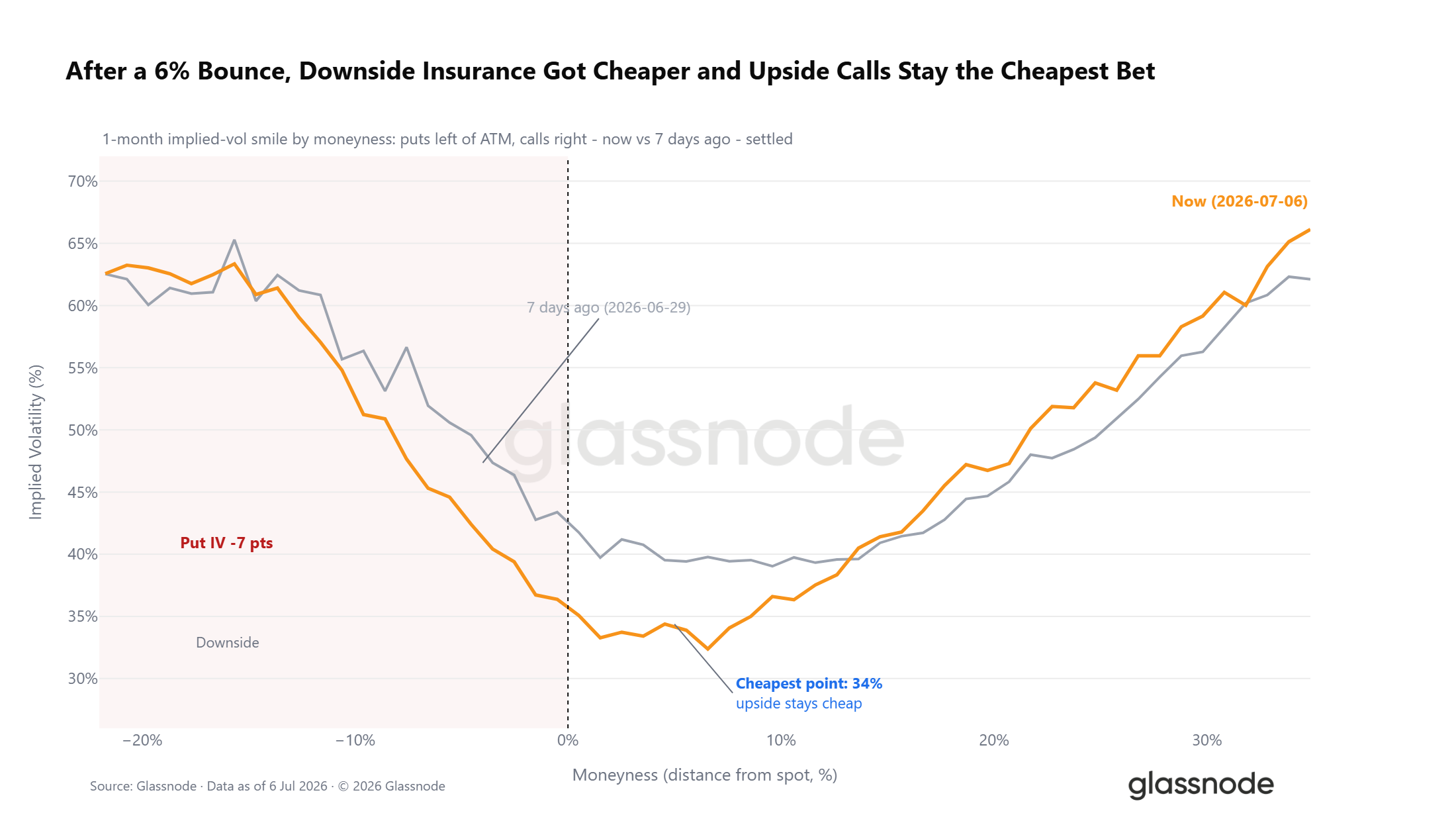

Options Surface Continues to Price Downside Risk

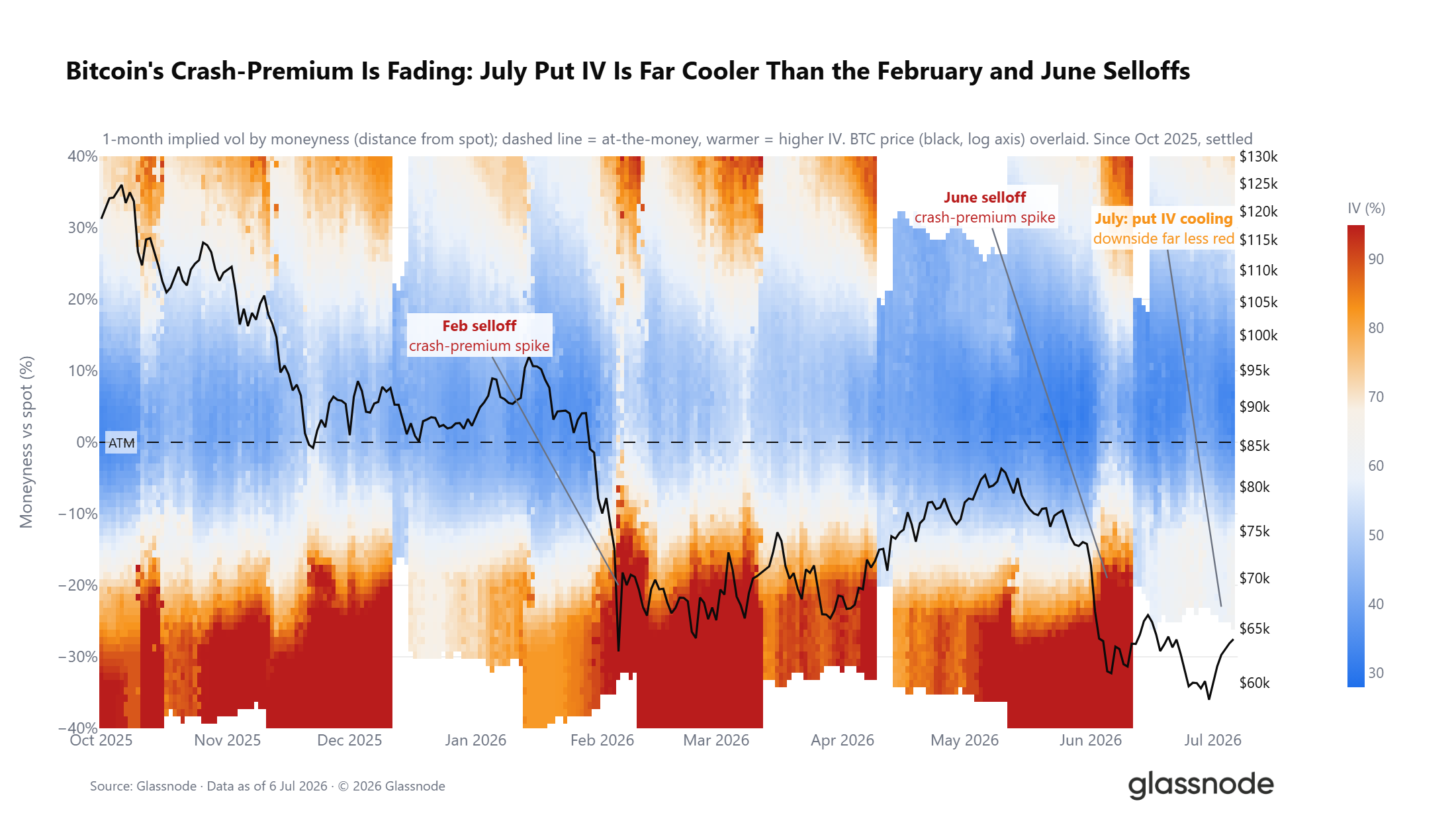

Overall positions are leaning bullish, but the options volatility surface signals a contrary message. The 25-delta skew indicator (the premium for downside protection relative to upside gain) maintains a premium state across all contract maturities. With each downward trend this year, this premium has risen; at the end of June, the indicator peaked at 24%, reflecting the strongest defensive sentiment in near-term contracts since the drop in February. Even as the overall positions lean toward bulls, traders remain willing to spend premiums on buying downside hedge tools.

Spot Prices Diverge from Maximum Pain Price Levels

Apart from position and volatility skew, the relative position of spot prices against the options market structure provides more trading clues. Currently, the spot price of Bitcoin is nearly 6% lower than the overall market's maximum pain price level of $66,000; the maximum pain price refers to the strike price at which the maximum number of open contracts becomes zero at options expiration, often drawing the market towards that price before expiry.

This week's decline has further widened the price gap between spot and maximum pain price levels, but the extent of divergence is far less extreme than during the February drop, remaining in the middle of the trading fluctuation range for 2026. The year's maximum pain price continues to serve as a gravitational center for market movement, with spot prices oscillating around that level and rarely exhibiting significant long-term deviations. If prices can continue to hold above $66,000, short-term trading signals will turn optimistic; if the gap continues to widen, it will strengthen the overall defensive trading sentiment in the options market.

Crash Hedge Costs Continue to Decline

Discrepancies exist between volatility skew and position structure signals, but the absolute cost trends for hedging downside risks are clear. As the market rebounds slightly, the pricing on the bearish end of the one-month volatility curve shifts downwards overall, with the implied volatility for put options at the 5% level below the spot price significantly retreating; the lowest pricing points on the volatility curve are centered around far-dated call options.

The overall defensive sentiment in the market remains, but the absolute costs traders pay to hedge against declines have significantly decreased. Prolonging the time dimension makes this trend even clearer: extreme bearish hedge demand during the drastic downturns in February and June led to volatility premiums, which have gradually faded since entering July. The DVOL volatility index has fallen to a 12-month low, signaling that the market has entered a low-volatility range; although cautious sentiment still dominates the trading landscape, the demand for hedging is gradually waning.

Conclusion

Data from on-chain, off-chain, and derivatives dimensions collectively indicate that the market clearly exhibits characteristics of a late bear market.

On-chain data shows that the five-month deep undervaluation cycle continues, with daily loss cash-out scale for long-term holders rising to $280 million, and a large-scale turnover of chips is underway; however, this stop-loss metric's continuous downward movement is a necessary prerequisite for an effective market reversal.

Off-chain data indicates that the scale of ETF fund outflows has narrowed from the peak in June, but monthly net outflows continue; the daily trading volume has shrunk by 80% compared to the peak in October 2025, reflecting a lack of bullish confidence among institutions.

From the derivatives perspective, market positions have turned cautiously bullish, with the put/call ratio reaching a new low for the year; however, the volatility skew and options surface continue to price downside risks.

Taking all indicators into account, the foundational conditions necessary for the market to bottom out have been fully established, yet the core signals confirming the bottom have not yet appeared. Future market movements need to satisfy three main conditions: the continuous cooling of long-term holders’ stop-loss selling pressure, stabilization of institutional fund flows, and effective stabilization of prices above real market averages. On this foundation, the probability of a transition to a bull market cycle will significantly increase.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。