Original authors: Li Dan, Ye Zhen

Original source: Wall Street Journal

The AI hardware sector has adjusted for two consecutive days, but what has truly drawn market attention is not the chip companies themselves, but the latest moves of two AI large model companies.

On Wednesday, it was reported that Meta is exploring the commercialization of surplus AI computing power, and a day later, another report stated that Anthropic is discussing cooperation with Samsung Electronics to develop their own AI chips and is considering using Samsung's 2-nanometer process for manufacturing.

Although these two pieces of news seem unrelated, they both touch upon the most sensitive topic in the AI industry chain at present—whether the AI capital expenditure, which has been rapidly expanding for two years, is entering a new stage.

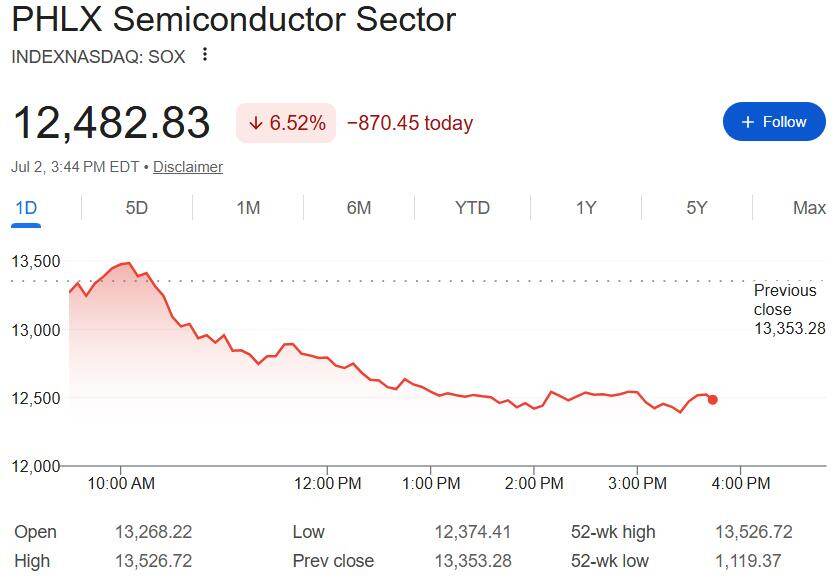

The market has chosen to reprice first. US chip stocks have continued to decline significantly over the past two days, with the Philadelphia Semiconductor Index (SOX) falling over 10% cumulatively on Wednesday and Thursday, marking the largest two-day decline in nearly a month. The semiconductor equipment sector, which is most sensitive to capital expenditure cycles, led the decline, with Teradyne (TER), Entegris (ENTG), KLA (KLAC), Applied Materials (AMAT), and Lam Research (LRCX) all dropping more than 10% during trading on Thursday. The leading European chip stock, ASML, saw its US shares (ASML) drop over 5% on Thursday at one point.

Goldman Sachs' basket of AI semiconductor stocks suffered heavy losses, recording the worst two-day performance since the imposition of tariff days.

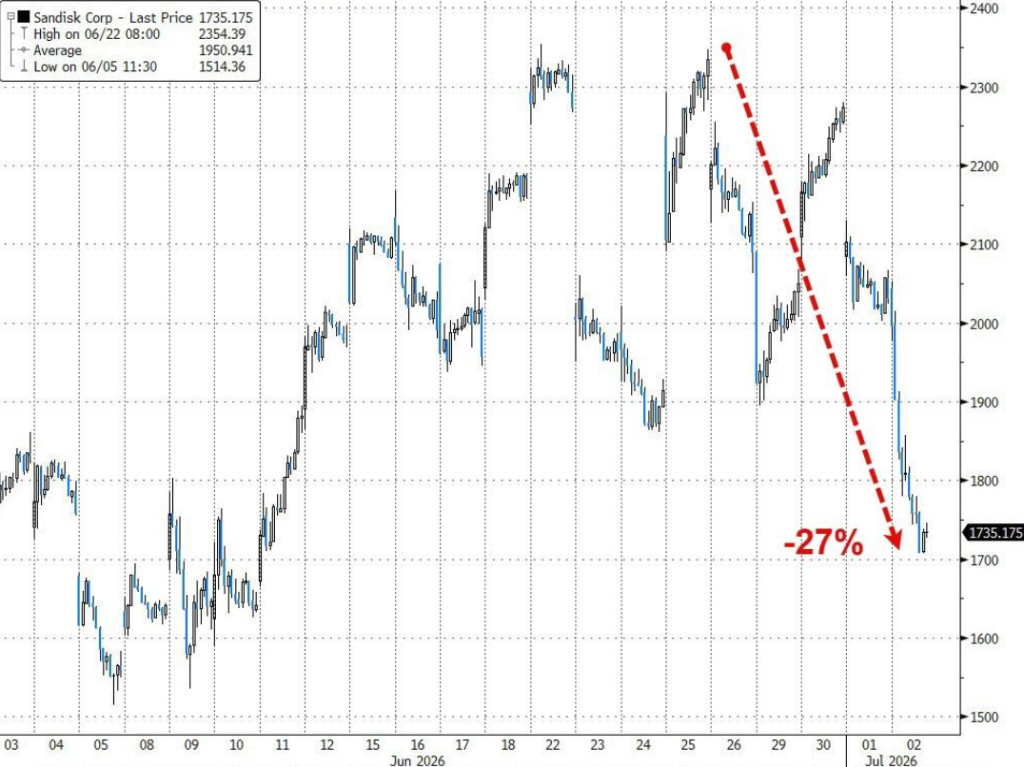

Memory stocks were hit hard, with Goldman Sachs' basket of memory stocks falling over 18% in the past two days, marking the most severe two-day drop in 12 years.

SanDisk even fell into a bear market.

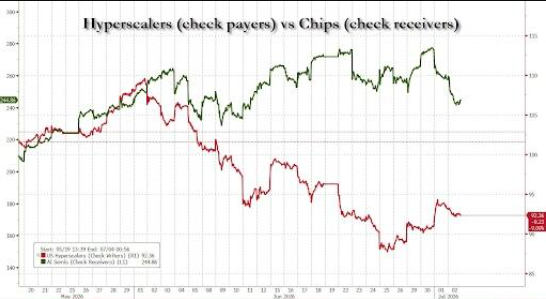

In contrast to the severe performance of funding recipients like chips, the share prices of hyperscale cloud service providers, which are the funding expenditure side, have stabilized slightly.

However, many institutions believe that the two pieces of news are more like catalysts for the market to reevaluate AI investment logic, rather than indicating a fundamental reversal in the prosperity of the AI industry. What the market is really trading is not whether "AI demand has peaked," but that the AI industry is moving from a phase of "competing for capital expenditure" to "competing for capital efficiency."

What the market is really worried about is not Anthropic making chips, but the change in AI capital expenditure logic

Over the past two years, the AI hardware sector has surged, and the core logic behind it has changed little: rapid iteration of AI models has resulted in a continuous explosion in computing power demand, GPUs have been in long-term short supply, and tech giants have constantly raised capital expenditures, thus driving a round of unprecedented "AI capital expenditure supercycle" in the demand for GPUs, high-bandwidth memory (HBM), high-speed networks, advanced packaging, and semiconductor equipment.

This logic not only propelled Nvidia to become the highest-valued company globally, but also made equipment manufacturers such as Applied Materials, Lam Research, ASML from the Netherlands, and KLA, as well as memory manufacturers like Micron and SanDisk, the biggest winners in the capital market.

However, the two pieces of news that appeared consecutively this week prompted the market to start discussing seriously: If the AI industry begins to focus more on capital efficiency instead of merely expanding investments, will this round of capital expenditure supercycle enter a new stage?

On Wednesday, it was reported that Meta is planning to build an AI cloud computing business, which may allow external clients to deploy AI models on Meta's infrastructure in the future or directly rent surplus AI computing power, achieving commercial returns on hundreds of billions of dollars in AI infrastructure investments.

Shortly after, on Thursday, news emerged that Anthropic is discussing the development of their own AI chips.

Looking at them independently, the two companies are taking different paths, but together they point to a change—AI companies are starting to consider how to improve the investment returns on existing infrastructure, rather than merely continuing to expand capital expenditure.

It is this expected change that has triggered the market to re-evaluate AI trading logic.

Anthropic's self-developed chip means AI companies are entering the "cost optimization era"?

Compared to the market's initial concerns about whether "self-developed chips will reduce GPU purchases," perhaps more attention should be paid to the commercial logic behind Anthropic's actions.

It was reported that Anthropic is discussing with Samsung Electronics to develop custom chips for AI training and reasoning, which is still in the early stages.

If advanced, Anthropic will become another foundational model company after Google, Amazon, Microsoft, and Meta to layout self-developed AI chips.

This does not mean abandoning Nvidia GPUs, but rather a natural evolution of the AI industry.

Over the past two years, the focus of competition among large model companies has been on who can acquire more GPUs and build more data centers; as the scale of models continues to expand, training and reasoning costs are rapidly climbing. Reducing the unit token cost, increasing computing power utilization, and decreasing dependency on a single supplier have begun to become new competitive focuses.

ASICs designed for specific models can achieve a better balance among performance, energy consumption, and cost, which is also a significant reason why Google's TPU, Amazon's Trainium, and Meta's MTIA have continued to advance in recent years.

In this sense, Anthropic's exploration of self-developed chips is more like an important sign of the AI industry moving from "competing on investment" to "competing on efficiency," rather than cutting AI investments.

Meta and Anthropic, two different paths point to the same goal

Meta and Anthropic have adopted different strategies, but their goals are highly consistent.

Meta aims to generate revenue from temporarily idle AI computing power to increase the return on hundreds of billions of dollars in capital expenditures; Anthropic hopes to lower long-term computing power costs through custom chips, enhancing its autonomy in infrastructure.

Whether selling surplus computing power or laying out ASICs, essentially neither is reducing AI investment, but rather looking for a more sustainable AI business model.

However, for the capital market, these two pieces of news could easily trigger another association: if AI companies start to focus more on capital efficiency, will future GPU purchases, cloud computing rentals, and new data center investments maintain the high growth of the past two years?

As a result, the market has begun to reassess whether AI capital expenditures can continue to maintain the previous expectation of almost "only increasing and not decreasing."

This is also why, during the two consecutive days of market adjustment, the biggest decline was not among model companies, but rather among semiconductor equipment companies closely linked to new capital expenditures. Compared to GPU and storage manufacturers, equipment orders often more directly reflect the future investment plans of wafer fabs and chip companies, thus being most sensitive to changes in capital expenditure expectations.

Institutions: The market is more like re-evaluating AI trading rather than denying the AI supercycle

Although semiconductor stocks have adjusted for several consecutive days, most institutions did not interpret the two pieces of news as an indication that AI demand is starting to cool.

Regarding Meta, many analysts believe that selling surplus computing power is more like seeking a commercialization outlet for massive AI capital expenditures, thereby increasing sustainability for future investments in GPUs, network equipment, data centers, and energy infrastructure, rather than cutting capital expenditures.

Regarding Anthropic, institutions generally believe that self-developed chips align with the long-term development trends of AI large model companies. Even as more companies begin to adopt ASICs, there will still be a reliance on advanced process manufacturing, HBM, high-speed interconnections, advanced packaging, and data center construction; the demand for AI infrastructure will not disappear because of this but may be redistributed across different segments.

More importantly, the current penetration rate of AI applications remains at a relatively low level. Industry insiders indicate that as inference demand continues to grow, the token consumption and computing power demand of large models remain significantly above previous expectations, and the construction of AI infrastructure is still quite far from truly maturing.

Therefore, this week, the market appears to be experiencing a phase re-evaluation of AI trading after a historic rally.

If, in the past two years, the competition in AI was about "who invests more," then the signals released by Meta and Anthropic indicate that the AI industry is entering a new stage—competition is shifting towards who can generate higher returns for every dollar of capital expenditure.

For the market, this expectation shift is sufficient to act as a catalyst for the adjustment of the AI hardware sector; but for the industry itself, it does not necessarily mean the end of the supercycle, but rather may signify that investments in AI infrastructure are beginning to move towards a more mature development stage that emphasizes commercial closure.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。