On June 23, from the South Korean stock market to the US stock market, global technology assets underwent a severe emotional cooling.

First, during the Asian session, the KOSPI index fell nearly 10% in a single day, and both Samsung Electronics and SK Hynix dropped over 12%, triggering a temporary market-wide suspension, and the selling sentiment quickly spread to the US stock market that evening. Over the past year, the strongest performing AI and storage assets became the epicenter of this round of global tech stock corrections.

Ironically, this sharp market turbulence coincided with Micron Technology's announcement of its third-quarter financial results for fiscal year 2026 on June 24, making the timing quite delicate.

On one hand, global AI storage stocks are collectively retreating, as the market begins to reassess high valuations and crowded trades; on the other hand, Micron is about to present a performance report that carries high expectations. The combination of both makes the significance of this financial report transcend the quarterly performance of a single company, resembling a concentrated stress test for the entire storage sector.

After all, in the past period, the core logic that has driven the continuous rise of global storage stocks—explosive demand for HBM, price increases for DRAM and NAND, persistent supply tightness, and rapid gross margin growth—needs to gain renewed confidence verification. The question has thus become more direct: After the stock price and market expectations have been pushed to high levels, can Micron still deliver answers beyond imagination?

In other words, a "meeting expectations" financial report may no longer be enough. What the market is really waiting for is whether Micron can once again raise expectations and prove that the supply-demand gap in AI storage is far from over.

1. Why is this Micron financial report so important?

From the data of the previous quarter, it is difficult to describe Micron's fundamentals with the ordinary term "exceeded expectations."

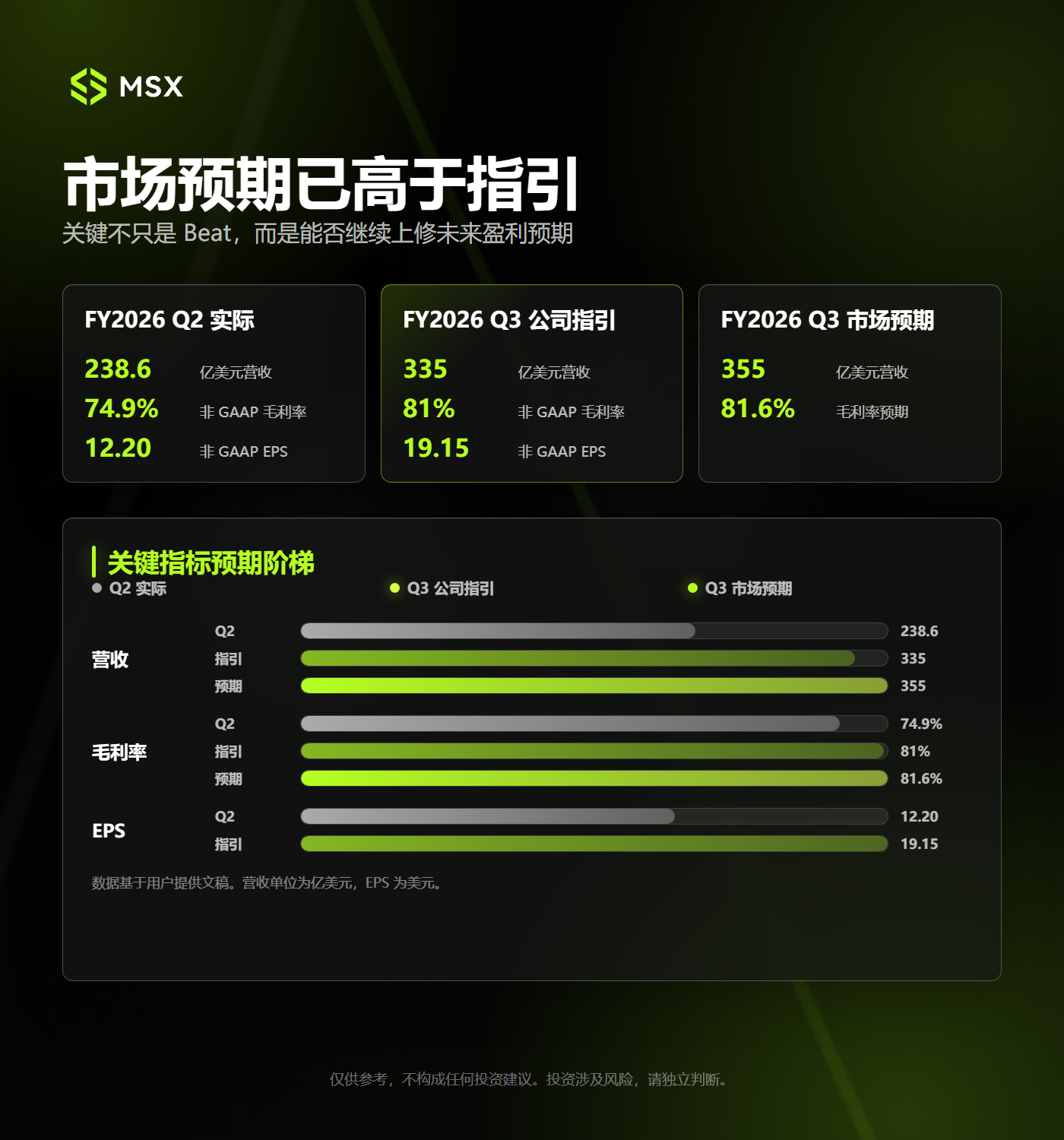

In the second quarter of fiscal year 2026, Micron's revenue reached $23.86 billion, nearly doubling year-over-year; non-GAAP gross margin rose to 74.9%, and non-GAAP earnings per share reached $12.20, both setting corporate records.

More importantly, the guidance provided by Micron for the third quarter is considered aggressive: revenue is expected to be $33.5 billion, with a non-GAAP gross margin of approximately 81%; non-GAAP earnings per share are projected at $19.15.

However, the appetite of the capital market has increased faster than the company's guidance. Currently, the market consensus for Micron's third-quarter revenue expectation has reached around $35.5 billion, exceeding the upper limit of the company's previous guidance range; the expected gross margin is approximately 81.6%, which also signifies that the market has already factored in yet another performance exceeding expectations.

This also constitutes the biggest contradiction in this financial report, namely that Micron's performance has to not only exceed the company's guidance but also surpass an already very optimistic market expectation.

Therefore, this financial report should not only be assessed on whether revenue and EPS have "beat" but also on whether the market is willing to continue revising upwards its profit forecasts for the coming quarters after the report is published. To put it simply, if the financial report is merely "ordinary good," that may still not be enough, but if the report is strong enough to keep revising guidance upwards, then yesterday’s drop may turn out to be an early washout.

After all, for a stock that has already risen significantly with high expectations, the most dangerous situation is often not poor performance, but rather that performance, while good, is not good enough to support a higher valuation.

Micron is currently facing such a pricing environment.

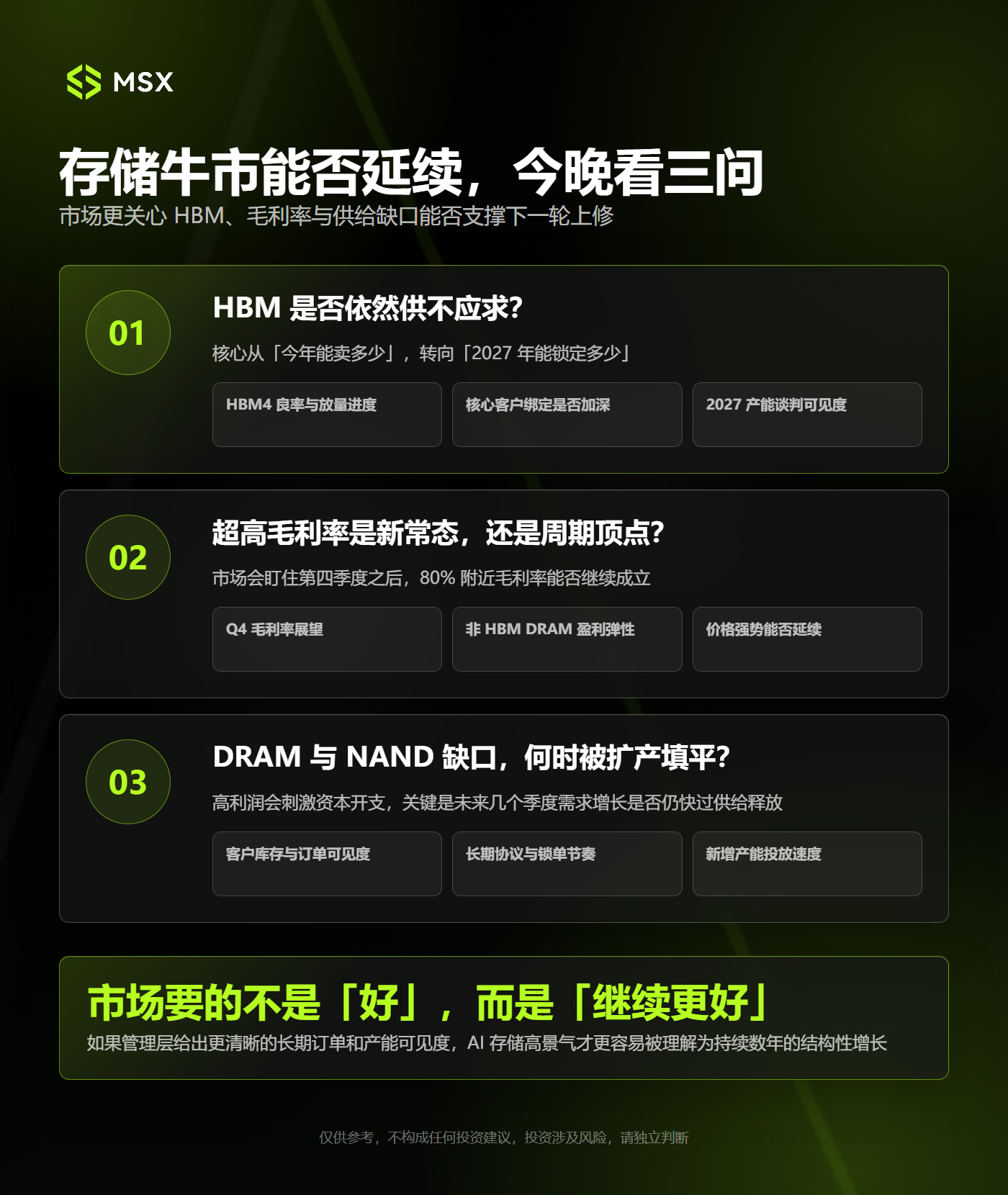

2. Can the storage bull market continue? Tonight's focus is on three questions

1. Is HBM still in short supply?

Micron's core growth narrative remains focused on HBM.

As is well known, AI servers do not only need GPUs. With the continuous improvement in computing power, power consumption, and data throughput of single AI accelerators, HBM has evolved from a regular supporting component into a key factor determining the performance of the entire AI system.

Micron has already begun advancing the mass production and shipment of HBM4, using it in NVIDIA's new Vera Rubin platform, and the HBM capacity for 2026 already has clear directional plans. Therefore, the market's focus this time will gradually shift from "how much can be sold this year" to "how much can be secured for 2027."

During the earnings call, investors may primarily seek answers to several questions:

Are the yield and ramp-up pace for HBM4 meeting expectations? Is Micron's binding with key customers continuing to deepen? What is the status of negotiations for 2027 capacity? Can subsequent products like HBM4E further narrow the gap with SK Hynix?

If Micron can provide clearer long-term orders and capacity visibility, the market will more easily interpret the current high demand for HBM as a structural growth phase lasting several years, rather than a product cycle nearing its peak.

Conversely, if the management is vague about the demand and orders for 2027, the market may begin to doubt whether the most intense phase of HBM and its pricing power has already been priced in by the stock price.

2. Is the super high gross margin a new normal or the peak of the cycle?

For Micron, profit elasticity comes not only from shipment volume but also from pricing and gross margins.

It should be noted that Micron's non-GAAP gross margin reached 74.9% in the last quarter, and the third-quarter guidance is as high as about 81%, indicating that for every $100 in revenue, Micron expects to retain over $80 in gross profit.

This level of gross margin is not common in past storage cycles. This is driven by an increased proportion of high-value products like HBM, comprehensive price increases for DRAM and NAND, constrained supply, and a continuous shift in product structure towards data centers.

It is worth noting that it is not only HBM driving Micron's margin increase. Micron's management has previously stated that the profitability of some non-HBM DRAM products is also very strong, sometimes even exceeding that of HBM, indicating this storage cycle is no longer limited to a single high-end segment but is beginning to spread to the broader DRAM market.

Therefore, the most important aspect of this financial report is not just whether the gross margin can reach 81%, but how management describes the trends for the fourth quarter and beyond.

If Micron continues to provide an outlook for gross margins exceeding 80%, it would indicate that the supply-demand gap and price increase trends remain strong, allowing the market to continue revising profit expectations upwards. However, if the gross margin just barely meets the guidance or if management's comments about future margins become conservative, the stock price may experience a "Sell the News" reaction.

3. When will the gaps in DRAM and NAND be filled by capacity expansion?

Any storage bull market ultimately returns to the same question: when will supply catch up with demand?

This round of market conditions has continued to exceed market expectations partly due to the rapid growth in AI data center demand for HBM, server DRAM, and enterprise SSDs; on the other hand, storage capacity cannot be released synchronously in the short term.

Especially for HBM, its production will take up more wafers and advanced packaging resources. Manufacturers shifting capacity towards HBM will also somewhat compress the supply of traditional DRAM, pushing prices up across the entire product line.

Micron previously stated that in the medium term, it could only meet about half to two-thirds of customer demand, while some new wafer fabs' meaningful output will not come until a later stage. This means that at least in the short term, newly added capacity will struggle to quickly fill the supply-demand gap.

However, the market will also pay attention to the other side. Because, under the stimulus of high profits, Micron, Samsung, and SK Hynix are all increasing capital expenditures, and if the speed of newly added capacity release exceeds the growth in AI demand, the storage industry may still revert to the cycle of price competition and inventory adjustment.

Therefore, within this earnings call, management's statements regarding customer inventory, order visibility, long-term agreements, and the pace of new capacity deployments may prove to be more important than the single-quarter shipment volume, as everyone may be more concerned about whether Micron can prove that over the coming quarters, demand growth still outpaces supply release.

3. What is the market betting on with a 13% implied volatility for options?

Apart from the fundamentals, the options market has already provided another answer.

Based on the option quotes before and after the close on June 22, the total price of near-the-money Call and Put contracts expiring on June 26 is about $159, relative to Micron's stock price of around $121.1 at the time, indicating that the options market implies a report volatility of around 13%.

This means that if you buy options now, theoretically, for Micron's stock to rise or fall over 13% after earnings, it would be relatively easier to beat the premium cost; for investors holding the stock, this figure also implies that a double-digit gap after the earnings report would not be surprising.

In other words, the options market is no longer pricing small fluctuations but is instead pricing a very sharp reaction to the earnings report.

More importantly, high implied volatility itself reflects the current market divergence: some capital believes that AI storage is still in the early stages of supply-demand imbalance, while others fear that the stock price has already overdrawn too much future growth.

From the possible outcomes post-earnings, MSX Research Institute believes three scenarios may arise:

Scenario 1: Performance exceeds expectations, guidance continues to be revised upwards

This is the most ideal outcome.

If Micron's revenue, EPS, and gross margin all exceed current market expectations while providing a strong fourth-quarter guidance and continuing to emphasize the smooth ramp-up of HBM4, improved visibility for 2027 orders, and sustained strength in DRAM and NAND prices, the logic of the storage bull market will be further confirmed.

In this case, Micron's rise may also lead to a resurgence across the entire storage supply chain, including SanDisk, Western Digital, Samsung, SK Hynix, as well as some semiconductor equipment and AI server-related stocks.

However, even if the earnings report is strong enough, attention should be paid to profit realization among high-level funds. As mentioned earlier, the options market has already factored in significant volatility, and a surge post-earnings does not necessarily mean a sustained upward trend on the second trading day.

Scenario 2: Performance is good, but guidance does not improve

This could be the most concerning situation for this earnings report.

Micron could very well deliver a record-breaking performance, but if the results only match previous guidance or if the fourth-quarter gross margin and revenue outlook do not continue to be revised upwards, the market may still choose to sell.

This is not because Micron's fundamentals have suddenly deteriorated but because the market has already traded on "exceeding expectations." Ultimately, for high-valued, highly crowded stocks, meeting expectations can sometimes equate to falling below them.

The recent sharp volatility in the Korean market has also reinforced this risk. On June 22, the Korean regulatory authority publicly reflected on the previous rapid approval of single-stock leveraged ETFs for Samsung and SK Hynix; the following day, the KOSPI index plummeted nearly 10%, and both memory giants fell over 12%.

This pullback does not necessarily imply a reversal in the long-term demand for AI storage, but it does remind the market that when high valuations, leveraged funds, and crowded trades converge on the same main line, any information falling short of expectations can be quickly magnified.

Therefore, the decline in Korean storage stocks is more of a stress test ahead of Micron's earnings report: If Micron is strong enough, it can stabilize market confidence again; if Micron is only "normally good," the pullback in the Korean market may be interpreted as a signal that the entire storage trade is starting to cool.

Scenario 3: Gross margin or forward guidance below expectations

If Micron reveals content in HBM4 progress, gross margin, product prices or fourth-quarter guidance that is significantly below market expectations, the stock price could face greater pressure.

The reason is that Micron's current stock price reflects at least three layers of expectations:

- The first layer is the long-term storage demand brought about by the expansion of AI computing power;

- The second layer is the price increase cycle driven by the tight supply-demand balance of DRAM and NAND;

- The third layer is the continuous enhancement of Micron's share and profitability in the high-end HBM market;

If any of these layers show signs of weakness, the market may simultaneously cut future profit forecasts and valuation multiples, impacting not only Micron but potentially spreading throughout the entire storage and AI hardware chain.

Conclusion

From the information currently available, Micron's long-term logic has not been undermined.

AI servers are still consuming more HBM and DRAM, data center SSD demand continues to grow, and the traditional NAND market is also recovering; newly added capacity is unlikely to be released quickly in the short term, and supply constraints continue to provide storage manufacturers with strong bargaining power.

However, strong fundamentals do not mean that stock prices are without risk.

When revenues, margins, and stock prices have continuously broken records, the market's standards for evaluating Micron will also change: in the past, it only needed to prove that the industry was recovering; now, it needs to demonstrate that this round of high prosperity can not only continue but also be stronger than investors have already imagined.

Therefore, the real suspense of this earnings report is not whether Micron can again deliver a good performance but whether it can continue to elevate the market's expectations for the future.

In summary, what Micron needs to prove is no longer that the storage bull market is still ongoing, but rather that the endpoint of this bull market remains farther away than the current market pricing suggests.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。