TL;DR

- SpaceX is advancing at least $20 billion in bond financing after the IPO to repay previous bridge loans; the company has ample cash on hand, but the market is beginning to reassess future capital expenditure pressures.

- Nvidia's bond issuance during the same period received strong demand, providing a contrasting reference: the AI narrative has entered income and profit validation, while SpaceX's space narrative still requires more phased proof.

- Related targets: SPCX, Nvidia, AMD, TSMC, AI data centers, satellite and space commercialization targets.

Around June 22, SpaceX advanced at least $20 billion in bond financing after the IPO to repay prior bridge loans; subsequently, SPCX, related to SpaceX, faced pressure in the secondary market, trading around $154.60 on June 23, below the initial closing price but still above the $135 IPO price.

This price change should not be simply attributed to a single bond event, but the financing news indeed became one of the triggers. It quickly brought the newly public space narrative back to cash flow issues: the market began to reassess how much funding SpaceX's long-term projects would require and which business unit would cover it.

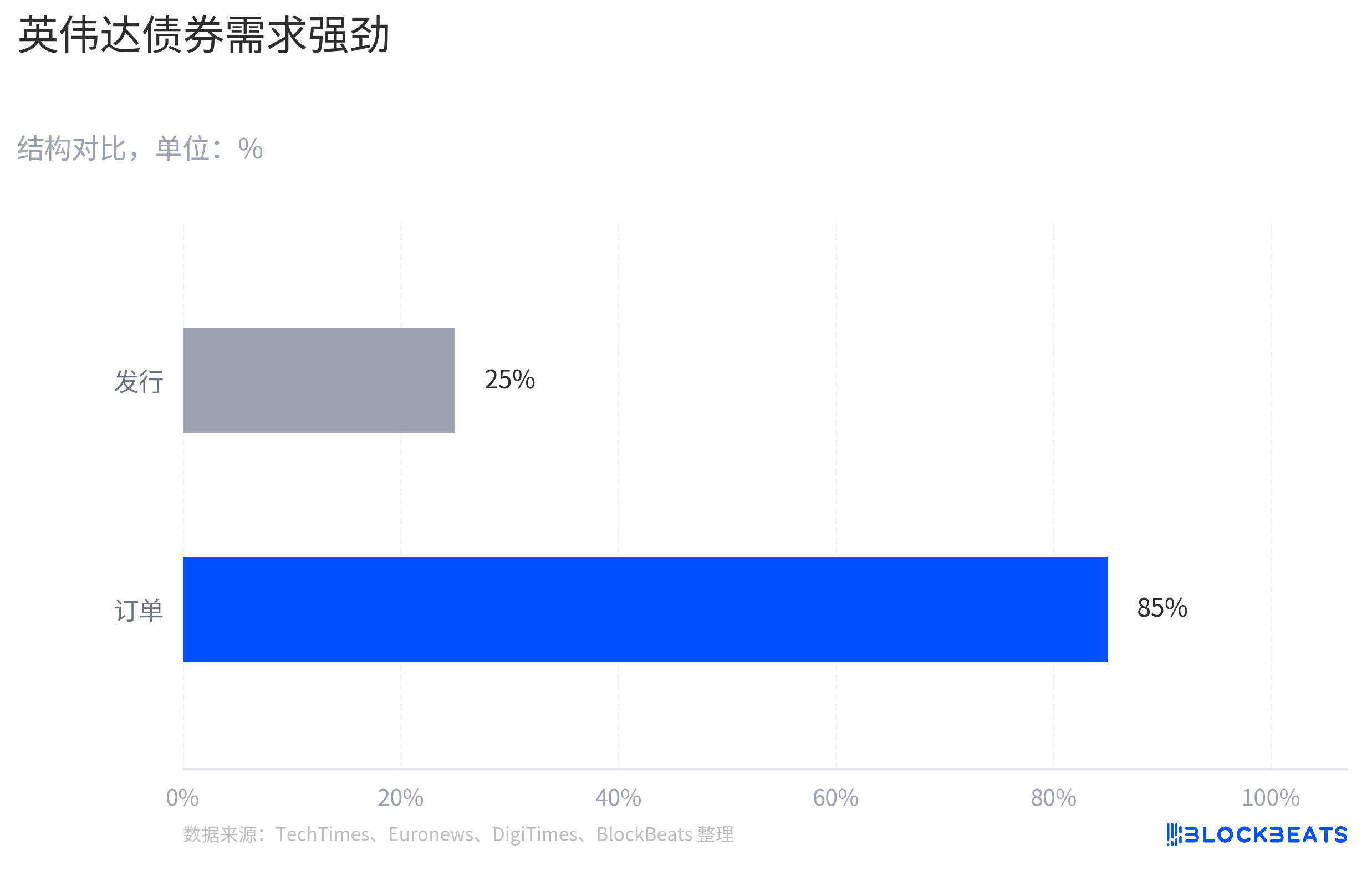

Nvidia is the most important reference. On June 15, Nvidia issued $25 billion in high-rated bonds, with order demand reaching around $85 billion at one point, and the issuance size was increased from the original plan of about $20 billion. Both companies are financing within a super narrative, but the market feedback is entirely different: Nvidia's bond issuance is more easily seen as locking in long-term capital, while SpaceX's bond issuance is immediately subjected to capital expenditure pressure testing.

The difference lies not in the act of issuing bonds itself but in the market's level of trust in cash flow. Nvidia's AI demand has already entered revenue and profit validation through data center income, customer orders, and profit margins, with investors discussing how long this growth curve can last. For Nvidia, issuing bonds resembles increasing funding flexibility on an already realized growth curve; for SpaceX, another question needs to be answered: can the money earned from Starlink support Starship, satellite networks, AI infrastructure, and more ambitious space visions.

SpaceX's financing prompts the market to reassess capital expenditure

The bond issuance itself is not the issue. For a high-credit company, replacing short-term bridge loans with long-term debt is often just capital structure management. This at least $20 billion bond financing for SpaceX is mainly reported as a repayment of the previous bridge loan, and should not be simply interpreted as a negative.

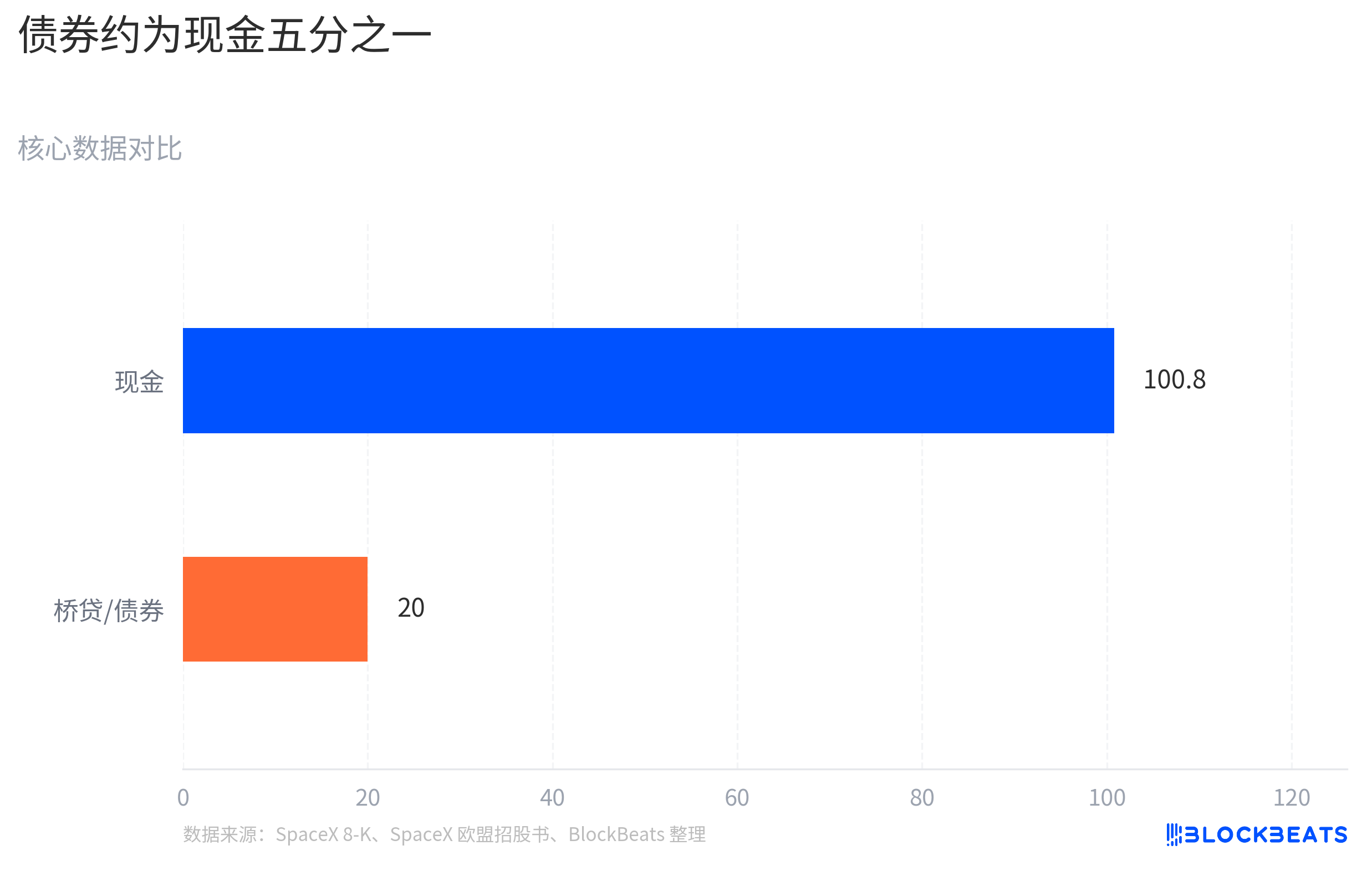

SpaceX also does not rely on the bond market for survival. According to regulatory filings, as of June 19, the company's cash and cash equivalents were about $100.8 billion. The cash on the books post-IPO reaching the $100 billion level at least indicates that the company's financial structure is not poor.

But having a lot of cash does not mean the market will not reassess the future spending pace. More critically, there is the bridge loan structure: SpaceX had $20 billion in unsecured bridge loans as of March, maturing on September 2, 2027, with extension options. The subsequent at least $20 billion in bond financing is mainly described as refinancing or repaying this bridge loan.

Bonds will change how the market views SpaceX. Equity investors can prepay for Starship, Mars transportation, and space infrastructure because they are buying future upside potential; debt investors are more concerned about cash flow, capital expenditures, and debt repayment pace. When SpaceX pushes for large bond financing right after going public, the market will naturally shift its focus from "how big can Musk make the space story" to "how much more will it cost before these projects materialize."

SpaceX already has a business that can generate profits, and the market is questioning whether this business can cover the long-term projects the company is pursuing simultaneously. Starlink is currently the clearest cash flow engine, with satellite internet users and revenue growth differentiating it from many purely conceptual space companies.

However, SpaceX's valuation is not solely based on Starlink; it is also built on the high-frequency reuse of Starship, global satellite network expansion, Mars transportation, and potentially new narratives related to AI infrastructure. These narratives are all ambitious and expensive. Starship requires continuous testing, iteration, and launch capability building; the satellite network needs replenishment and updates; if AI infrastructure further ties into SpaceX's capital story, investors will need to assess when this portion of investment will generate revenue.

Therefore, the bonds are not the only reason for SpaceX's decline, but they are a clear trigger. They remind the market that after the space narrative enters the public market, it needs not only to prove that the vision is significant enough but also that the self-sustaining ability is strong enough.

AI narrative and space narrative are at different realization stages

Nvidia's bond issuance during the same period provided the market with a clear reference. On June 15, Nvidia issued $25 billion in high-rated bonds, with order demand reaching around $85 billion at one point. The market did not initially perceive this bond as a pressure; rather, it is closer to viewing it as a strong company locking in long-term capital.

The difference comes from the cash flow stage behind the bonds. Nvidia's AI demand has entered its financial reports through data center revenues, customer orders, and profit margins, and investors are discussing how long this growth curve can last. For Nvidia, issuing bonds is more like adding financial flexibility on an already realized growth curve.

SpaceX's situation is different. It also has Starlink, a cash flow engine, and sufficient cash after the IPO, but the company’s valuation comprises more yet-to-be-fully-commercialized heavy capital projects. When the market sees SpaceX issuing bonds, the question is not "can it borrow money," but rather "will the funding consumption of future projects outpace cash flow realization."

This does not mean that space commercialization has lost value or that the market has negated SpaceX. A more accurate statement is that the AI narrative for Nvidia has already become visible revenue, while the space narrative for SpaceX still requires more phased proof. The value of Starship will have to wait until higher frequency, lower cost, and more stable reuse capabilities are proven; Mars transportation and space infrastructure are further out; if AI infrastructure becomes a new growth point, it also requires real customers, real revenue, and explainable capital returns.

This is exactly the difference that deep tech investment is most likely to overlook. A company can simultaneously possess strong technology, strong brands, and strong founders, but as long as cash flow validation lags behind capital input, debt will be viewed as a source of pressure by the market.

The phrase "Mars burning money" is catchy but incomplete. SpaceX has commercialization paths, but multiple future projects need capital to continue their momentum. Nvidia's contrasting response makes this clearer: the market rewards not the vision label but the speed at which stories convert into revenue, profits, and free cash flow.

Cash flow coverage speed determines repair space

SpaceX's room for repair depends on whether the market can see Starlink profit expansion covering heavier capital expenditure curves. As long as Starship is still in a high-investment phase, the satellite network requires continuous updates, and AI infrastructure still lacks clear payment paths, investors will repeatedly calculate funding consumption.

Bond pricing will first give a signal. If the eventual issuance spread, coupon rate, and order demand indicate that the credit market is willing to provide long-term funds at a relatively low cost, it suggests that investors still accept SpaceX developing the space infrastructure story over longer cycles; if financing costs are relatively high, or the market demands thicker risk compensation, equity valuations will remain under pressure.

More importantly, however, is the business side. If Starship provides stronger validation in high-frequency reuse and launch costs, the commercial models for Starlink, deep space transportation, and even space infrastructure will be revalued. Conversely, if subsequent disclosures indicate that Starlink growth cannot cover the expansion of other projects, debt will continue to remind the market: SpaceX is still in the stage of heavy capital visions.

This is also the core contradiction of SpaceX's current pricing. It has a cash balance of over $100 billion and a cash flow engine like Starlink, but the public market will not price solely based on cash balance. Only when Starlink profits, Starship reuse progress, and capital expenditure boundaries become clearer can debt potentially transform from a pressure item back into a growth tool.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。