TL;DR

- CME plans to launch small-scale crude oil and 1-ounce gold for 24/7 trading, filling the risk management gap during traditional market downtime.

- Binance, NYSE/ICE are also advancing around-the-clock tokenized assets, and the advantage of Hyperliquid’s "trade traditional assets anytime" is being repriced.

- Related assets: HYPE, CME, ICE, BNB, as well as crude oil, gold, and tokenized US stock related products.

The recent pullback of HYPE can easily be attributed to unlocks, large investors selling, or some issues with TradeXYZ's SpaceX pre-IPO. However, looking at a longer time frame, another issue is becoming more significant: the "anytime trading traditional assets" capability that Hyperliquid was previously rewarded for by the market is being replicated by traditional finance and centralized trading platforms.

On June 11, CME announced its plan to launch 24/7 small-scale WTI crude oil futures, pending regulatory approval, and to push the existing 1-ounce gold futures into around-the-clock trading. Almost simultaneously, it was reported that Binance launched bStocks, allowing users to trade tokenized US stocks like NVDA and TSLA with the liquidity from the Binance main site; NYSE/ICE is also developing its own 24/7 tokenized securities and on-chain settlement platform.

These products are not the same. CME deals with regulated futures, Binance bStocks is more akin to a tokenized stock entry point, while Hyperliquid focuses on on-chain perpetual contracts. But they are competing for the same demand: when oil, gold, and US stocks are closed in traditional markets, traders still want immediate exposure or immediate hedging against risks.

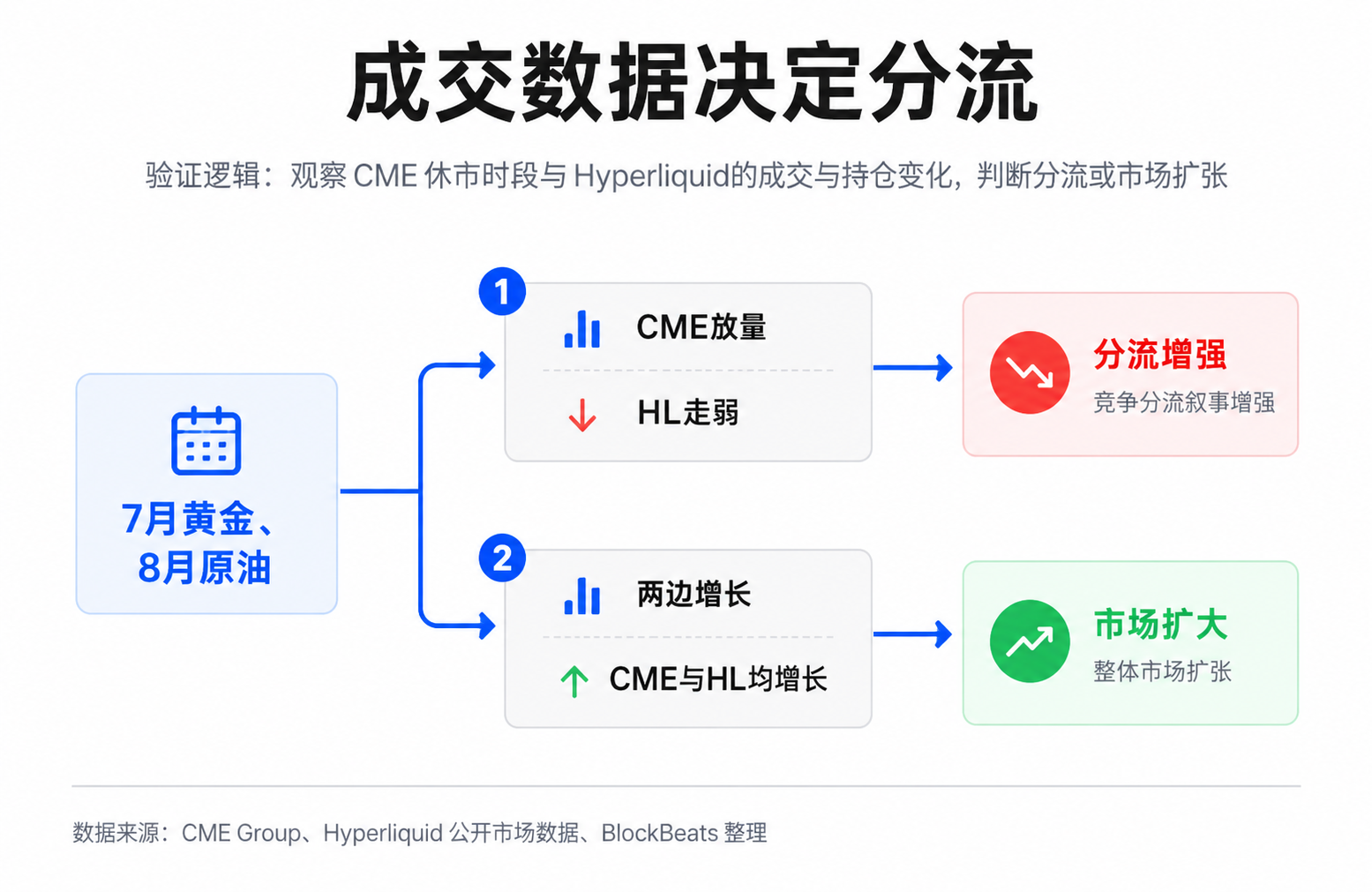

So this is not a story of “CME has already taken Hyperliquid's trading volume.” CME's new oil products are not yet on the market, and gold's 24/7 trading will not begin until July; actual diversion still requires transaction data verification. It feels more like a reassessment of expectations: if 24/7 trading is no longer a unique scarcity for Hyperliquid, how should the market understand HYPE's valuation anchor?

24/7 trading is evolving from a crypto advantage to a platform standard

Ordinary investors can initially simplify the question: news doesn’t wait for market opening.

Geopolitical conflicts may occur on weekends, leading to immediate changes in oil and gold prices. A US company’s earnings report, regulatory investigation, or sudden events may also happen outside traditional trading hours. In the past, traders either waited for the market to open and faced the risk of gaps or sought alternative tools for early hedging. The crypto market has always benefited from the natural ability to trade around the clock.

Hyperliquid seized this gap. It is not just a crypto perpetual trading platform but also moves traditional asset exposures like stocks, crude oil, and gold on-chain, with some third-party HIP-3 market and ecological products extending to earlier-stage assets. For some traders, Hyperliquid acts like an “always-open risk convenience store”: US stocks are closed, commodity futures liquidity is lacking, but on-chain contracts still allow them to express direction, hedge risk, or even engage in leveraged trading.

CME's entry point is precisely this pain point. According to CME's announcement on June 11, the new 10-Barrel WTI crude oil futures will be around 10 barrels, one-tenth of the existing Micro WTI, and are scheduled to launch on August 30, 2026, adopting cash settlement. The existing 1-ounce gold futures are set to begin 24/7 trading on July 26, 2026, also cash settled.

所谓小规格期货,白话说就是把原本很大的商品合约切成更小份,让交易者不用押太大资金,也能更精细地管理风险。CME 商品全球主管 Derek Sammann 在公告中表示,面对地缘政治不确定性,交易者需要规格合适、每周 7 天每天 24 小时可用的受监管产品,以便在消息发生时管理风险敞口。

This sentence emphasizes not just "24/7," but also "regulated" and "size appropriate." The former targets institutions and compliant funds, while the latter lowers the participation threshold. CME does not need to replicate Hyperliquid's high leverage and on-chain experience; it aims to provide another type of all-weather exposure: more traditional, more compliant, and more easily accepted by the existing financial system.

CME, Binance, NYSE are targeting the same layer of demand

The products launched by CME, Binance, and NYSE/ICE are different in form, but they all replicate the advantage that Hyperliquid has been easily understood by the market: trading traditional assets during market downtime.

CME's angle is commodities. Crude oil and gold are already core assets in global macro trading, and the demand for risk management during non-trading periods increases with geopolitical tensions. For traditional institutions, if CME can provide sufficient liquidity during the night and on weekends, they may not need to bear additional compliance, custody, and operational risks on on-chain perpetual platforms.

Binance's entry point is tokenized US stocks. According to reports, the first batch of bStocks includes NVDAB, TSLAB, CRCLB, MUB, SNDKB, etc., emphasizing 24/7 trading, 1:1 conversion, and self-custody support. It is important to distinguish this from Binance's other stock-related products; bStocks are closer to a tokenized stock entry point and should not be confused with stock perpetual contracts.

Tokenized stocks can be understood as "on-chain versions of stock certificates," which differ from Hyperliquid's synthetic perpetuals. Synthetic perpetuals resemble contracts that trade price movements without holding actual stocks. Tokenized stocks, however, aim to anchor price closer to real assets and enhance trust through conversion mechanisms.

NYSE/ICE’s direction seems more like underlying infrastructure. ICE/NYSE announced in January this year that they are developing a tokenized securities trading and on-chain settlement platform, aimed at supporting 24/7 trading, immediate settlement, dollar amount orders, and stablecoin fund transfers, all pending regulatory approval. If this direction materializes, traditional trading platforms will not simply extend trading hours but move part of the settlement and trading logic of the securities market closer to an on-chain experience.

These three cannot be equated directly. CME futures have margin, delivery, and regulatory frameworks; Binance bStocks resemble the tokenized stock entry within centralized trading platforms; Hyperliquid's perpetuals lean towards high leverage, on-chain margins, and fast speculation or hedging. Their users, risk control, leverage, and KYC requirements differ.

However, the market reassessment does not require them to be identical. As long as they cover some of the same demand, Hyperliquid's narrative will change. The previous narrative was that if you wanted to trade oil, gold, and US stock exposure anytime, on-chain perpetual was one of the most direct entry points. The current narrative has shifted: you can still go to Hyperliquid, but you can also choose CME or Binance, and in the future, you might even select NYSE's tokenized platform.

Hyperliquid needs to prove that traders are willing to stay

For supporters of Hyperliquid, the actions of CME and Binance do not mean complete substitution. The appeal of on-chain perpetual trading has never solely come from around-the-clock availability.

Hyperliquid’s advantages include high leverage, self-custody, on-chain speed, trading culture, and an already established liquidity network. For native crypto traders and some high-frequency speculative funds, less KYC, faster onboarding, and more flexible margin usage are experiences that traditional trading platforms find difficult to replicate. Even if CME offers 24/7 crude oil and gold, it won’t instantly cause all traders willing to take on on-chain risk and pursue higher leverage to migrate immediately.

Liquidity itself can form inertia. Traders go where they not only consider product specifications but depth, slippage, fees, available leverage, and counterparties. If Hyperliquid has already established a sufficiently deep order book on certain contracts, new compliant products may not immediately capture trading volume. Especially in the early stages, whether CME's night and weekend trading is actually active still needs actual transaction data, not just product announcements.

This pressure also stems from here: Hyperliquid can no longer rely solely on "we are 24/7" to prove the scarcity of traditional asset exposure. It needs to prove that even if other platforms trade around the clock, traders are still willing to keep positions, margin, and trading volumes here.

This will reflect on HYPE's pricing logic. Some investors typically understand HYPE as a trading platform asset related to platform trading volume and fees: the more trades there are, the more fees collected, and the stronger the protocol’s ability to repurchase HYPE, making it more likely to gain support from cash flow narratives. This fee and repurchase cycle has been a significant reason why HYPE differs from many purely narrative tokens in the past.

The actions of CME, Binance, and NYSE/ICE may not necessarily change Hyperliquid's actual revenue in the short term, but they will change the market's imagination regarding future revenue growth. The pullback of HYPE can be explained by many factors, including unlocks, large player behavior, overall risk appetite, and competition expectations; it cannot simply be said that new products from CME are the cause. However, as competitors begin to fill the 24/7 capability, the market will naturally ask whether the growth of trading volume for traditional asset perpetuals can still smoothly convert into fees and repurchases as it did in the past.

This is why this round of discussion feels more like a reassessment of expectations rather than a verification of performance. CME's new oil contracts are not yet launched, and there is no clear data on the user migration between Binance bStocks and Hyperliquid's stock perpetuals. What can be confirmed now is that Hyperliquid’s “uniqueness” in traditional asset exposure is declining; what cannot be confirmed is to what extent this will translate into actual trading volume loss.

July and August will provide the first round of validation

What is truly worth watching going forward is not which platform announced 24/7, but whether there are real transactions and depth during market downtimes.

CME's 1-ounce gold futures plan will begin 24/7 trading on July 26, 2026, and the new 10-barrel WTI crude oil futures are scheduled to launch on August 30, 2026. These two milestones will provide the market with the first batch of validation samples: whether the transactions during the night and on weekends are sufficiently active, whether the spreads are narrow enough, and whether institutions and professional traders are genuinely moving risk management back to the regulated futures system.

For Hyperliquid, a more direct observation metric is the trading volume, open interest, and fee contributions corresponding to the commodity and stock perpetuals. If CME’s new products for gold and oil begin to show volume while Hyperliquid’s corresponding market trading volume and open interest decline simultaneously, the narrative of competitive diversion will strengthen; if both sides grow, it indicates that 24/7 trading may be expanding the overall market rather than just moving from on-chain to off-chain.

The key for HYPE lies here. Unlocks and large trades will influence short-term prices, but the long-term valuation anchor still depends on whether the platform can continuously generate fees and convert those fees into repurchases. As long as the trading volume and the intensity of repurchases can cover new supply and emotional pressures, competitive expectations may not necessarily lead to trend-based harm. Conversely, if growth slows for traditional asset perpetuals while the around-the-clock liquidity of external platforms starts to materialize, the market’s pricing of HYPE will shift from "high-growth trading platform token" to a more cautious cash flow expectation.

It is not yet time to draw conclusions about Hyperliquid. More accurately, the demand it pioneered and validated is being recognized and replicated by larger financial platforms. The next round of data will determine whether this reassessment remains at the narrative level or continues to translate into revenue and token prices.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。