The original text is from Ethereum founderVitalik Buterin

Translated by|Odaily Planet Daily Qin Xiaofeng(@QinXiaofeng888)

Special thanks to Vladimir Novakovski, Curve developers, and others who provided feedback and review for this article.

Assuming you have a price index code T, which represents a certain price index in terms of ETH. For example, T could be the USD/ETH price (i.e., the inverse of ETH/USD), or CPI/ETH (i.e., CPI/USD * USD/ETH), or any other commodity price index, even more peculiar indices (like the average rent of a city). You want to enable users to gain risk exposure to T.

In simple terms, your goal is to create a synthetic asset tracking T in an ecosystem where only ETH is a "trustless" asset (or that can also be extended to other trustless assets), without relying on centralized issuers. The only trust dependency is on the oracle, but oracles can achieve trust minimization, unlike issuers.

If T is viewed as the USD/ETH price, then this issue is essentially the same as "algorithmic stablecoins." In reality, it is perpetual futures.

All attempts to provide this functionality must face a fundamental issue: the whole system can only hold ETH, and the net assets and liabilities valued in T must sum to zero. Therefore, for each user holding a positive T position, there must be another user holding the same amount of a negative T position. What happens if T rises too high, bankrupting the negative T holders?

In traditional algorithmic stablecoins, this issue is resolved through forced liquidation.

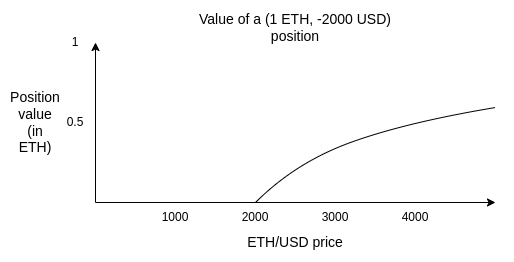

For example, suppose the ETH price is $2500, and a user holds a position (1 ETH, -$2000). If the ETH price falls to $2000 (actually to trigger with a safety margin at a slightly higher price), the system must be able to "force liquidate" that user: allowing anyone else to put in $2000 and take the underlying 1 ETH, so that the entire system does not get into trouble due to an insufficiently collateralized $2000 debt.

The problem with relying on liquidation is that liquidation depends on real-time oracles. You need an oracle that can provide a binding ETH/USD price value and do so in real-time.

Real-time oracles are difficult to secure. You can only rely on a limited number of participants who observe real-time signals in an automated way. You cannot use any mechanism with recourse. You also cannot adopt the currently most effective technology that can build secure and cheap oracles: placing a prediction market in front of a secure but expensive oracle and only using that expensive oracle when there is a severe divergence.

This article proposes a disruptive idea that allows synthetic assets to rely only on "slow" oracles: we completely remove the concept of liquidation, changing the system's "building blocks" from debt to options. Based on this, you can choose to build an asset tracking the index as a higher-level structure, or completely avoid that, allowing users to rebalance themselves. Decoupling these two mechanisms will lead to stronger stability and flexibility.

Synthetic Options

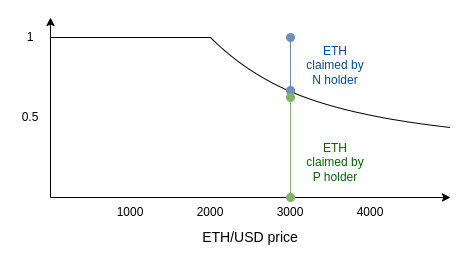

We define two assets: P and N.

The parameters include: (i) code T, (ii) strike price S, (iii) expiration date M.

At any time, a pair (P, N) can be generated by splitting 1 ETH. Similarly, you can merge P and N at any time to exchange for 1 ETH.

At time M, call the oracle to determine the value of T. Let that value be x. Once the oracle is determined:

- P receives

min(1, S / x)ETH - N receives

max(0, 1 - S / x)ETH

Note: P + N = 1. Therefore, there is no possibility of liquidation.

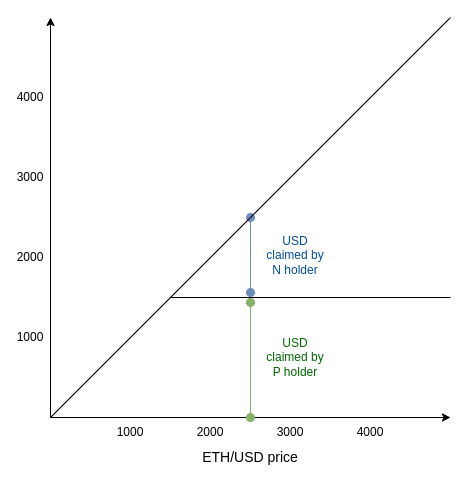

Additionally, for ease of understanding, here is the same chart priced in dollars:

An interesting feature of this design is that it "actually" functions as a prediction market, which has existed and traded for many years. See: Scalar Markets | Seer.

This means this design can share the same oracle with prediction market systems, thus improving security.

How to Use Synthetic Options

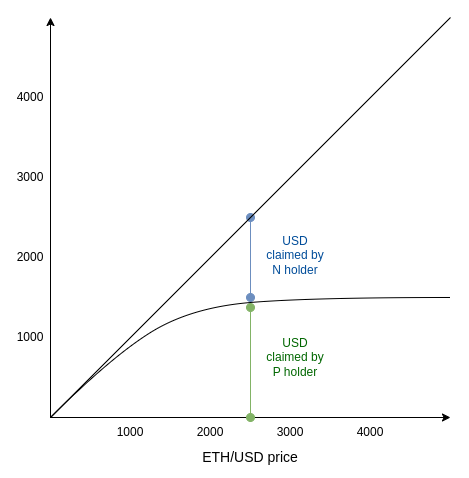

Assuming the current price is 2500, and you as a user want to construct a portfolio with a certain dollar risk exposure. You buy some (P 1500), which is a P asset with a strike price far below 2500 (in this case, 1500). Is that enough?

Not quite. Although the current price is far above 1500, the price could still fall below 1500 at the expiration date. The greater this risk, the more the dollar value of (P 1500) will deviate from its maximum value. In fact, it will start to deviate from 1 dollar in a quadratic manner. The chart is as follows:

Note that this is just a smoothed version of the curve above. The degree of smoothing depends both on the current price's distance from 1500 and the market's expectation of future price volatility.

To understand its principle, suppose M is two weeks away, and the current price is 1499. At that time, how much is (P 1500) worth? It corresponds to the possibility of "the ETH/USD price being above 1500 in two weeks." ETH can fluctuate significantly at times, and this value can be high or low, say around 50 dollars. What if the current price drops to 1399? The price of P will decrease but will not go to zero completely, as there is still a possibility that the price will recover above 1500 before M arrives.

When ETH/USD is far below 1500, the value of N approaches zero. When ETH/USD is far above 1500, the value of N approaches price - 1500. In the intermediate region, it is a smooth curve transitioning from one mode to another.

The Black-Scholes equation is a formal method that attempts to estimate the fair pricing of (P 1500) (at least applicable when index T represents some price, rather than more peculiar underlying like weather). However, since 2008, the Black-Scholes equation has become synonymous with catastrophic fragility caused by over-reliance on mathematical models – which is not without reason. Therefore, we should not overly trust the specific details of the curve, at least because we do not want to introduce another oracle that needs to measure expected volatility, skew, or kurtosis.

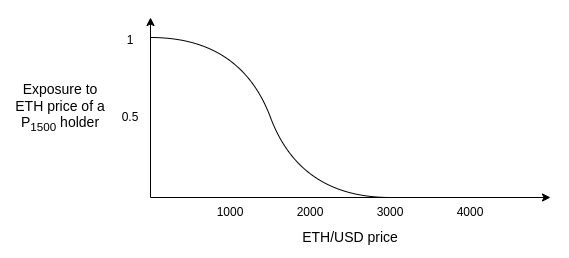

Instead, we should remember this graph, which is the derivative of the previous graph. It tells you: at the current price level, how much ETH risk exposure does each unit of (P 1500) correspond to?

Remember, as a holder of (P 1500), your goal is to "hold" dollars, with no risk exposure to ETH. This graph tells you that the prudent strategy is to hold deep "in-the-money" options and once the price approaches the strike price, roll it into options with a lower strike price.

For example, you could follow an algorithm like this: if the current price is X, buy a PS with a strike price S X/2, expiration date in the next 1-2 months. If the price drops below S * 1.5, roll into a PS' with a strike price S' X/4. Do not hold to expiry, because that will expose you to ETH risk when the oracle determines the price.

Let speculators and market makers hold N and provide liquidity for you.

We can compare the nature of liquidation-based synthetic assets with option-based synthetic assets as follows:

In both systems, action must be taken for significant price fluctuations: in one system, the protocol conducts liquidation; in another system, users rebalance. The key distinction of option-based synthetic assets is that users can choose how to execute this action.

Rebalancing can be accomplished through a fully automated on-chain DAO (note: fully automated. All rules are set by the DAO without the need for voting or AI). Such a DAO would act as a "wrapper" for the options system and provide "stablecoins." Alternatively, users can also choose to rebalance locally, using a daemon on their device to complete the task.

By moving the decision point of "when {liquidate/rebalance}" from on-chain tools to the users, we gain two advantages:

- Reduce users' MEV risks, as transactions will not be visible in advance.

- Eliminate reliance on globally normative oracles. Users still need to rely on oracles that respond faster than (for example) two weeks, but they can hide which oracle they are using (for example, a locally run agent queries dozens of financial news websites, and no one knows which ones, then takes the median). This helps protect the system from oracle attacks.

The main choice for users lies in timing and thresholds. If users rebalance frequently, they are more susceptible to counterparty short-term price fluctuations. If users rebalance conservatively, they will bear more quadratic drift.

I believe accepting a moderate level of quadratic drift (for example, an annual standard deviation of about 1-4%) is an underestimated strategy. This cost is indeed significant, and it is counterintuitive, making this design unsuitable as an "accounting stablecoin" (i.e., it cannot allow receivers or senders or capital gains tax agencies to "pretend it is dollars").

However, if you view it not from the "I want to simulate dollars" perspective, but from the "I want price stability" (i.e., the ability to pay known amounts of expenses in the future), it makes much more sense. The annual volatility between fiat currencies far exceeds 1-4%. Each individual or business's expected future expenses priced in their local fiat currency also have an annual volatility far exceeding 1-4%. Furthermore, algorithmic stablecoins (like RAI) also frequently experience roughly comparable magnitude fluctuations in their equilibrium returns.

An important decision to be made is: even if you rebalance conservatively, what is the market mechanism for rebalancing? It is very easy to lose 2% or more annually in multiple rounds of slippage, which is the greatest risk of the entire scheme losing competitiveness.

Fortunately, user time preferences are almost always very low. Users do not care whether to rebalance today, tomorrow, or three days later. We should leverage this to design an ideal market structure where slippage is much lower than that of traditional automated market makers. Rebalancing will be more like one-sided market making rather than instant selling.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。