1. Definition of TradFi and the Evolution Logic of the Crypto World

TradFi, or Traditional Finance, specifically refers to the introduction of traditional financial assets— including stocks, bonds, commodities, foreign exchange, ETFs, etc.— into the crypto market for trading through tokenization or synthetic assets.

This concept did not emerge only in 2026 but has gone through three distinctly different stages in its development.

The first stage was the "Synthetic Asset Experimentation Period" from 2020 to 2022. During this time, Mirror Protocol and Synthetix were the first to launch on-chain synthetic U.S. stocks, and FTX and Binance provided tokenized stock trading services through partnerships with licensed brokers. However, the collapse of FTX in 2022 combined with tightening global crypto regulations forced most tokenized stock businesses to go offline, ending this stage with industry restructuring.

The second stage is the "Government Bond Pioneering Period" from 2023 to 2024. In the context of aggressive interest rate hikes by the Federal Reserve, DeFi protocols like MakerDAO began to use U.S. Treasury bonds as underlying RWA assets. BlackRock launched the BUIDL Fund in March 2024 with an initial seed capital of $100 million, which surpassed $1 billion within months, marking the formal entry of Wall Street giants.

The third stage is the "Full Asset Acceleration Period" from the second half of 2025 to the present. Tokenized stocks re-entered the growth curve, MyStonks completed U.S. STO compliance filing, and Backed Finance issued real asset-backed xStocks across nine chains. Traditional custodians like Fidelity and UBS began participating. More importantly, crypto exchanges are no longer satisfied with simply listing tokenized assets but have launched TradFi perpetual contract products, bringing traditional assets like U.S. stocks, gold, and treasury bonds into a 7×24-hour on-chain trading ecosystem.

As a veteran platform in the crypto industry, HTX has taken the lead in this stage by establishing a TradFi perpetual contract product line, focusing on core U.S. stock targets like NVDA, AAPL, MSFT, META, and SPY, providing crypto users with a new path to trade global core assets without leaving the on-chain ecosystem.

The internal logic of this evolution is that the crypto market needs new incremental capital and user groups, and traditional financial assets serve as the most effective bridge connecting the global $75 trillion stock market and the $130 trillion bond market. For HTX, the introduction of TradFi assets signifies a strategic upgrade from a crypto-native platform to a full-asset trading platform.

2. Market Structure and Competitive Landscape

The current TradFi crypto market presents a competitive landscape with three parallel development tracks.

The first track is "Tokenized Real Assets," represented by BlackRock BUIDL, Ondo Finance, Backed Finance, and MyStonks. The characteristic is that assets exist on-chain in the form of ERC-20 tokens, corresponding 1:1 with the underlying real assets and are managed by licensed custodians. Among them, BlackRock BUIDL holds an absolute leading position in the tokenized treasury bond sector with $2.3 billion AUM, capturing about 25% to 30% of the tokenized treasury bond sub-market; Ondo Finance's OUSG has developed to the level of several billion dollars; Backed Finance's xStocks are running on nine chains, requiring whitelist access but no KYC.

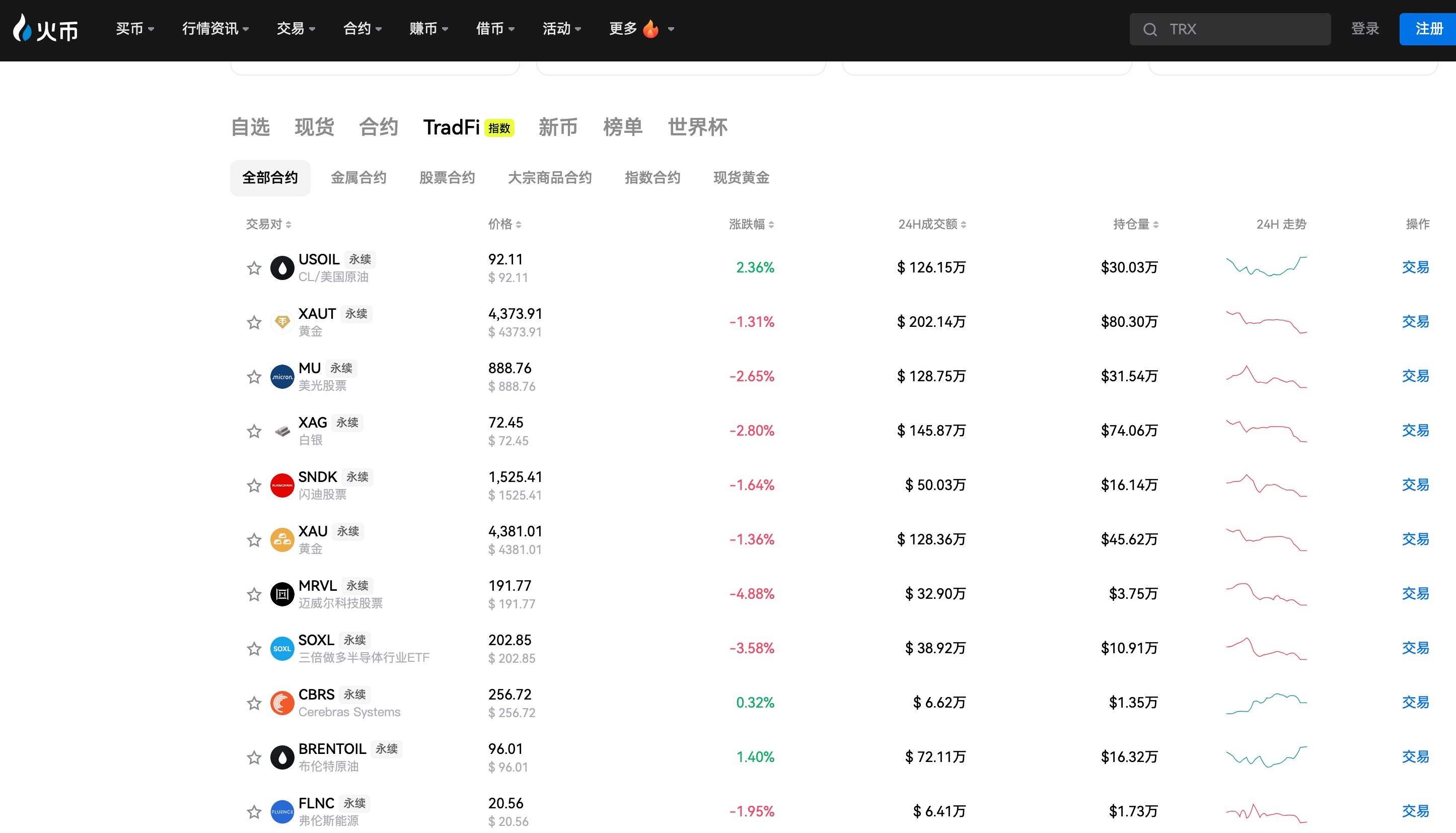

The second track is "TradFi Derivative Perpetual Contracts," which is the fastest-growing segment in 2026. Coinbase launched U.S. stock perpetual contracts in March 2026 for non-U.S. users, supporting individual stocks like Apple, Microsoft, Nvidia, Tesla, and ETFs like SPY and QQQ, with up to 10x leverage for individual stocks and 20x for ETFs, settled in USDC, and trading 7×24 hours. HTX has also launched TradFi perpetual contracts for NVDA, AAPL, MSFT, META, SPY, providing users with global U.S. stock derivative trading services settled in USDT. Hyperliquid holds a 28.6% market share in the RWA perpetual contract field through the HIP-3 protocol. The trading volume of RWA perpetual contracts reached $524.8 billion in Q1 2026, surpassing the $313 billion of the entire year of 2025.

The third track is "TradFi Comprehensive Trading Infrastructure," aiming to provide a unified trading interface for traditional and crypto assets. Some leading platforms connect to contracts for difference through third-party systems like MT5, while others independently develop index perpetual contract products that bundle multiple traditional assets into indices for trading.

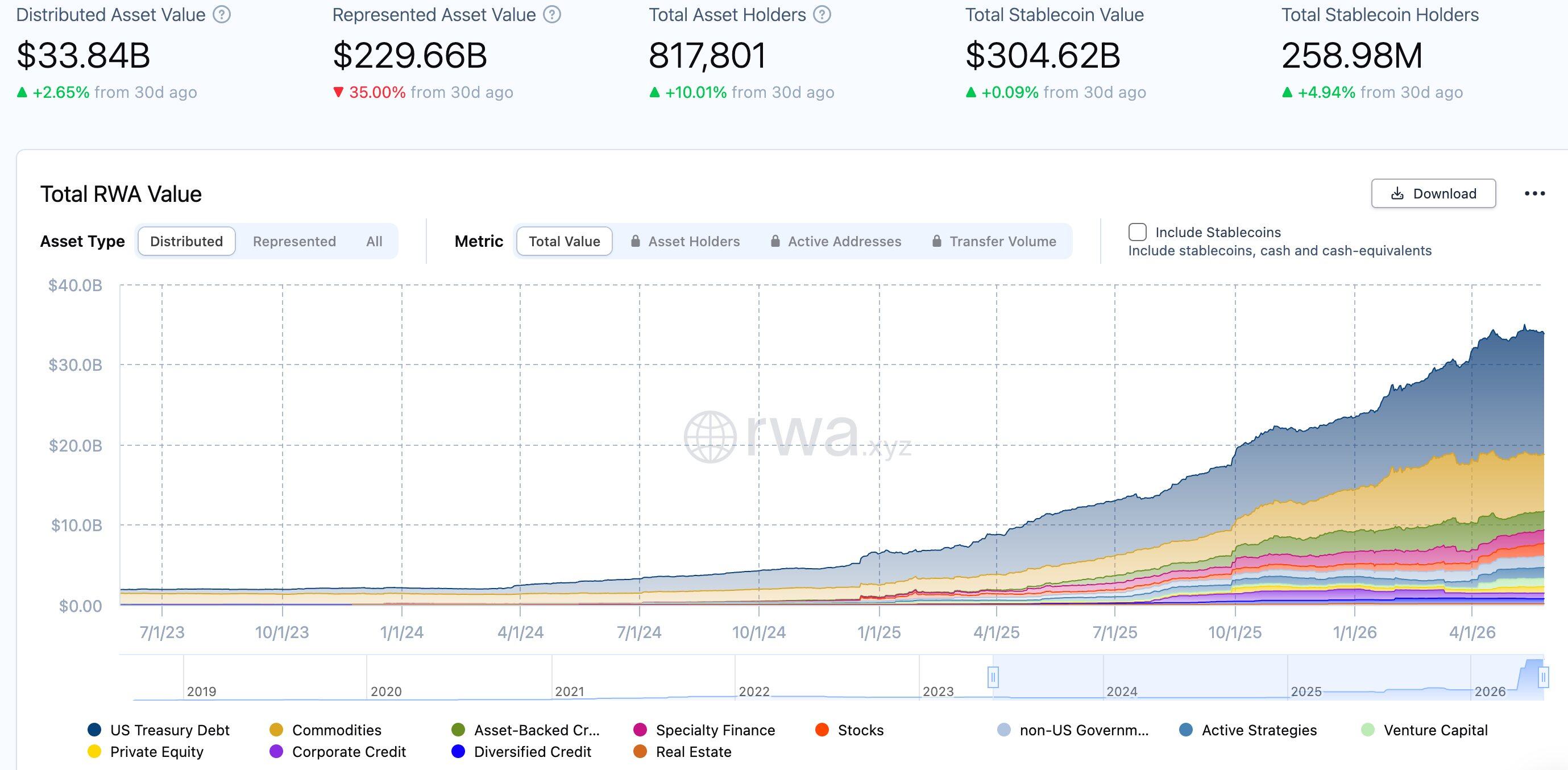

From market data, the tokenized RWA market had reached a TVL of $31 billion to $34 billion by May 2026, nearly tripling from about $11 billion a year ago. Tokenized gold grew from $1.43 billion to $5.55 billion, an increase of 289%; tokenized stocks grew from $200,000 to $486 million, an increase of more than 200 times. BCG predicts that by 2030, the global tokenized asset market could reach $16 trillion, accounting for about 10% of global GDP; McKinsey's conservative estimate is about $2 trillion. Whether optimistic or conservative, there remains a growth potential of dozens to hundreds of times between the current market size and the long-term space.

3. Core Risk Analysis

Although the prospects for TradFi crypto are broad, the risks it faces are equally significant. These risks are both potential traps for investors and core challenges that platform operators need to manage prudently.

The first is compliance and regulatory risk, which is currently the largest source of uncertainty. Tokenized securities essentially fall under the category of securities issuance and must comply with the securities laws of various countries. The SEC's regulatory stance on on-chain securities remains ambiguous; for instance, Coinbase's U.S. stock perpetual contracts are only for non-U.S. users, reflecting the complexity of the regulatory environment. Fragmented cross-border regulations mean that the same tokenized asset may face completely different compliance requirements in different jurisdictions, creating a continuous compliance challenge for globally operating crypto exchanges. HTX also needs to confront the operational complexities arising from regulatory differences when laying out TradFi perpetual contracts.

The second is liquidity risk. Although the trading volume of RWA perpetual contracts has reached $524.8 billion in Q1, the total market capitalization of tokenized spot stocks is only $486 million, indicating a significant imbalance in liquidity depth between spot and derivatives. This structural liquidity mismatch could lead to extreme price deviations during volatile weather, increasing traders' liquidation risks. Additionally, the misalignment between U.S. stock trading hours and the crypto market's 7×24-hour trading model may lead to insufficient price discovery during off-trading hours, increasing the risks of slippage and abnormal volatility.

The third is smart contract and technology risk. Tokenized assets rely on the accurate execution of smart contracts, and any contractual loophole could lead to asset losses. Although institutional products like BlackRock BUIDL are supported by compliance platforms like Securitize, tokenized assets at the DeFi protocol level still face risks such as inadequate contract audits and oracle manipulation.

The fourth is custodial and settlement risk. Tokenization of real assets requires a reliable custodian as support, and if a custodian faces credit risk (similar to the FTX incident), token holders may encounter situations where the underlying assets cannot be redeemed. Although the current mainstream solutions use traditional custodians such as Fidelity and UBS, the legal correspondence between on-chain tokens and off-chain assets has not yet received clear case support in many jurisdictions.

The fifth is exchange rate and interest rate risk. TradFi perpetual contracts are usually settled in USDT or USDC, but the underlying assets are priced in U.S. dollars, and fluctuations in the exchange rate may affect the actual returns of non-U.S. dollar users. At the same time, changes in the Federal Reserve's interest rate policy may directly influence the U.S. stock market trends, thereby transmitting to the price fluctuations of TradFi perpetual contracts.

4. Innovation Trends and Track Opportunities

The TradFi crypto track is showing four major innovation trends, which present strategic growth opportunities for crypto exchanges like HTX.

The first trend is the rapid expansion of perpetual contract product matrices. Following Coinbase's pioneering launch of U.S. stock perpetual contracts, more and more crypto exchanges are connecting to U.S. stock perpetual contract product lines, expanding the targets from the initial 5 to 10 blue-chip stocks to semiconductor ETFs, crypto concept stocks, industry-themed ETFs, and more. HTX has launched contracts for NVDA, AAPL, MSFT, META, SPY, and is expected to cover more TradFi targets in the future, building a complete trading matrix for core U.S. assets. From a competitive landscape perspective, exchanges that can be the first to establish a complete TradFi product matrix will gain a first-mover advantage in user acquisition and trading fee income.

The second trend is the maturation of institutional-grade infrastructure. BlackRock BUIDL has quickly expanded from $100 million in seed capital to $2.3 billion AUM, with newly filed two tokenized funds transitioning to a product line, conveying a long-term commitment of Wall Street's top institutions to tokenization. The participation of traditional custodians like Fidelity and UBS, as well as compliance platforms like Securitize offering KYC, whitelisting, on-chain issuance, and redemption one-stop services, is lowering the entry barriers for institutions. Franklin Templeton's Benji fund has continuously operated since its launch in 2021, and Ondo Finance's OUSG has developed to several billion dollars, with institutional tokenized product lines initially taking shape. This institutional trend means that TradFi crypto is moving from "fringe experimentation" to "mainstream allocation," and crypto exchanges as gateways connecting institutional funds and on-chain assets will see their value increase accordingly.

The third trend is the rise of Permissioned DeFi Pools. This is the most noteworthy structural innovation in the RWA field for 2026. Institutions are creating KYC/AML whitelist-based DeFi liquidity pools on public chains, allowing qualified participants to trade tokenized treasury bonds 7×24 hours, while implementing automated compliance checks through smart contracts. This model retains DeFi's composability and efficiency advantages while meeting regulators' requirements for investor suitability and is seen as a key bridge for institutional large-scale entry. The fourth trend is the gradual clarification of regulatory frameworks. The EU MiCA regulation will be fully implemented in July 2026, the U.S. GENIUS Act was issued in March 2025, and globally, 72 jurisdictions have established regulatory frameworks for crypto assets, with 58 countries adopting FATF travel rules. The certainty of regulation is shifting from "gray areas" to "clear rules," providing institutional guarantees for the long-term development of TradFi crypto. For HTX, regulatory clarity means more confidence in investing resources in building TradFi product lines without worrying about the business interruption risks that sudden policy shifts might bring.

5. Participation Strategies and Investment Logic

For investors, the TradFi crypto track offers multiple levels of investment participation paths.

The first layer is direct participation in TradFi perpetual contract trading. Platforms like HTX have launched U.S. stock perpetual contracts, allowing investors to trade NVDA, AAPL, SPY, etc., using USDT as margin, and leverage trading 7×24 hours. The advantage of this path lies in the low trading threshold; one does not need to open a traditional brokerage account to trade global core assets. However, it is crucial to note the volatility of funding rates for perpetual contracts and the risk of forced liquidation. Particularly, the misalignment between U.S. stock trading hours and the crypto market's 7×24 hour model could result in insufficient price discovery during non-U.S. stock trading periods, increasing trading risks.

The second layer is investing in protocol tokens of the RWA track. Ondo Finance (ONDO) as the leading protocol in the tokenized treasury bond sector has its token value positively correlated with the growth of the on-chain treasury bond scale. Infrastructure protocols like Centrifuge in the RWA space are also worthy of attention. The third layer is to strategically position in crypto exchanges that provide TradFi trading infrastructure.

As the trading volume for TradFi perpetual contracts experiences explosive growth—reaching $524.8 billion in Q1 2026—exchanges that launch TradFi products will directly benefit from the increase in transaction fees. HTX is tapping into the $75 trillion incremental space of the U.S. stock market by launching U.S. stock perpetual contracts, which holds structural significance for its platform revenue and user growth.

Investors should pay particular attention to the compliance qualifications and risk control capabilities of exchanges. Coinbase, as a publicly listed company on NASDAQ, has an inherent advantage in compliance; other exchanges might avoid direct regulatory conflicts by targeting non-U.S. users. Regarding risk warnings, TradFi crypto is still in its early stage, with the liquidity depth of tokenized assets far less than that of traditional markets and the price discovery mechanism still immature. Investors should strictly control their positions, prioritize selecting tokenized products backed by real assets, and avoid participating in high-leverage synthetic asset trading with a lack of compliance foundation. Attention should also be paid to the impact of exchange rate fluctuations on non-U.S. dollar users, as well as the transmission effects of changes in Federal Reserve interest rate policies on U.S. stock trends.

6. Conclusion and Outlook

TradFi crypto is reshaping the boundaries of the crypto industry. From the synthetic asset experimentation in 2020, to the institutional-grade entry of BlackRock BUIDL in 2024, and then to the comprehensive layout of U.S. stock perpetual contracts by exchanges like Coinbase and HTX in 2026, this track has completed a leap from "proof of concept" to "product matrix" in six years.

Current key data is already shocking: the RWA market's TVL surpassed $31 billion, quarterly trading volume for RWA perpetual contracts exceeded $500 billion, and the market capitalization of tokenized stocks increased over 200 times within a year; Wall Street giants like BlackRock have incorporated tokenization into their core product strategies.

As of mid-2026, we judge that TradFi crypto is still in the "early acceleration phase of the growth curve." While there is a significant gap between the $16 trillion forward space predicted by BCG and McKinsey's conservative estimate of $2 trillion, even the conservative estimate implies that the current market size has tens of times the growth potential. In the short term, the expansion of the product matrix for U.S. stock perpetual contracts, the institutional landing of permissioned DeFi pools, and the comprehensive implementation of regulatory frameworks like MiCA will act as three major catalysts driving market growth.

HTX, as an important participant in the crypto industry, has already gained a favorable position in this track by launching TradFi perpetual contracts for NVDA, AAPL, MSFT, META, SPY. In the medium to long term, once trading depth and user experience for TradFi assets on-chain reach the same level as traditional brokerages, crypto exchanges will genuinely transform from "crypto asset platforms" to "full asset trading infrastructures." This represents not only a technological upgrade but a fundamental transformation of the financial infrastructure paradigm. For HTX users, this means that the era of trading crypto assets and global core traditional assets with a single account is approaching.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。