Original | Odaily Planet Daily (@OdailyChina)

Author|Azuma (@azuma_eth)

In the early morning of May 23, Beijing time, Bloomberg cited sources saying that the U.S. Securities and Exchange Commission (SEC) has postponed the planned "innovation exemption" program. This program was originally intended to greenlight products related to "tokenized U.S. stocks," but due to numerous concerns raised by market participants, the SEC decided to pause its advancement.

As a result of this negative news, the cryptocurrency market experienced a sharp decline, with BTC falling below 76,000 USDT and ETH also dropping below 2,100 USDT; the related concepts of "tokenized U.S. stocks" were even more affected, with ONDO completely retracing the short-term gains stimulated yesterday by the "punishment of Tiger Brokers, Futu, and ChangQiao by the regulatory authority," reporting 0.382 USDT at the time of publication, a 24-hour decline of 6.4%.

Innovation Exemption, A Last-Minute Brake

Since the current chairman Paul Atkins took office, the SEC has changed its previous tough stance of "using enforcement instead of regulation" and is inclined to provide a compliance testing ground for the crypto industry.

Earlier this week, market rumors suggested that the SEC would announce an exemption proposal as early as this week, intending to allow trading platforms to offer on-chain trading services for listed securities (such as NVDA, AAPL, TSLA, etc.) under more relaxed regulatory conditions. This exemption was promoted by SEC Chairman Paul Atkins and Commissioner Hester Peirce, aiming to provide a legitimate testing space for tokenized securities, which the market interpreted as an important signal of U.S. regulators further shifting to support tokenized securities.

However, this innovation exemption, originally scheduled to be officially unveiled to the public this week, has been urgently braked at the last moment. Insiders revealed that the SEC has returned the draft and is starting to consult securities exchanges and other market actors intensively again.

From "completely greenlighting" to "emergency braking," what kind of resistance is the SEC facing? In this epic game regarding "U.S. stocks on-chain," who is vehemently opposed?

Opposition Comes from Wall Street

Similar to the CLARITY bill, which is also facing resistance (see "Why Did the CLARITY Review Suddenly Get Delayed? Why Are There Such Significant Disagreements in the Industry?"), the most vocal opponents of this exemption proposal are the traditional forces of Wall Street, represented by Citadel Securities and the Securities Industry and Financial Markets Association (SIFMA).

As early as several months ago, when the policy was still in the discussion phase, these traditional financial giants had already submitted a strongly worded letter of opposition to the SEC. Overall, the core arguments against from Wall Street focus mostly on three areas.

Firstly, there are concerns about potential liquidity fragmentation in the market. Institutions like Citadel Securities warn that allowing various third parties to disorderly issue "synthetic U.S. stocks" could lead to the fragmentation of U.S. stock assets scattered across numerous DeFi platforms that lack interconnection, depth, and price transparency. This would not bring about efficiency but rather make it impossible for investors to determine the real value of the tokenized stocks they hold at any given moment.

Secondly, there are concerns that U.S. stock tokens may threaten traditional compliance defenses. On anonymous or pseudonymous public blockchains, how can it be ensured that these third-party tokens’ transactions do not become a breeding ground for money laundering? Wall Street giants believe that the current technological means of decentralized platforms cannot adequately enforce core investor protection mechanisms like AML and KYC.

Lastly, there are still gaps technically and legally. Institutional representatives cite legal opinions suggesting that allowing a third-party crypto platform, unauthorized by companies like Apple and Microsoft, to implement "ensuring token holders have voting rights and dividend distributions" remains uncertain within the current legal frameworks and technical pathways.

Within the SEC, There Are Also Reservations

It is noteworthy that this wave of opposition is not only coming from Wall Street's "vested interests"; even within the SEC, there are cautious reservations.

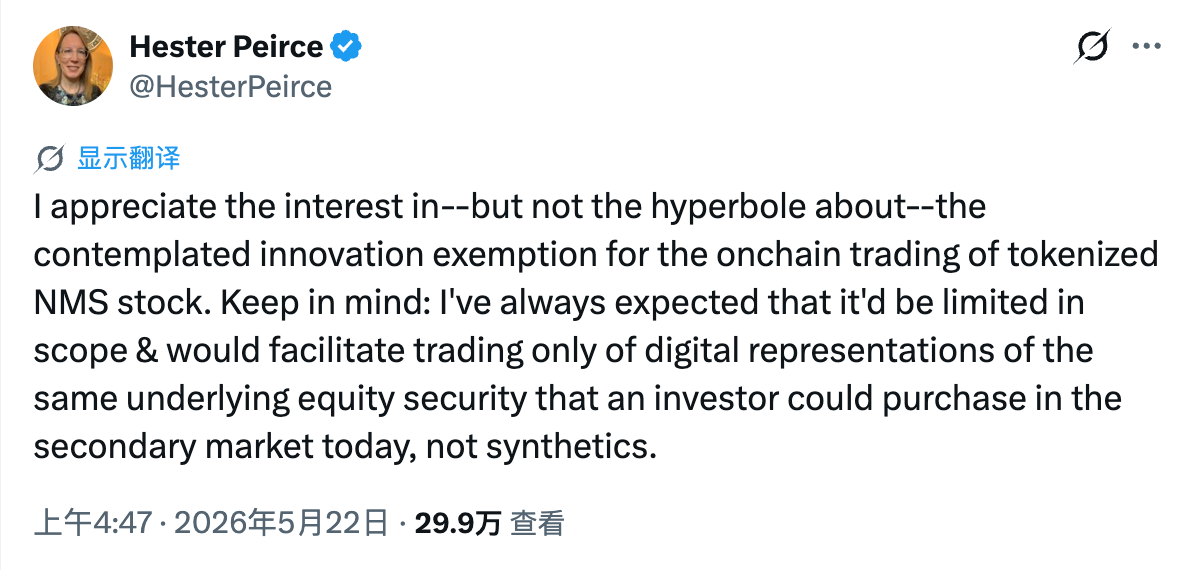

Hester Peirce, a veteran ally of the crypto community affectionately known as "Crypto Mom," publicly spoke out on X yesterday, expressing her change of heart and stating that the scope of this exemption should be strictly limited.

Peirce stated that the SEC should allow attempts to digitize or tokenize a company's own stocks on-chain, led by "the issuer themselves or their affiliates"; rather than allowing a variety of third-party issued, unregulated synthetic assets to flood the market. In other words, the "U.S. stock tokens" Peirce wants to see should be led, authorized, or endorsed by specific listed companies themselves (i.e., the issuers), and must guarantee to investors the same rights as regular shareholders (such as dividends, voting rights, etc.), rather than the more mainstream derivatives or synthetic tokens issued by third parties that track the performance of the underlying stocks.

Even Peirce, who has traditionally been a strong supporter of crypto innovation, has chosen to side with limiting the scope of the exemption, highlighting the significant resistance to the proposal at the legal and compliance levels.

Where Will the Future of Tokenized Stocks Go?

This week's "postponement" undoubtedly serves as a blow to the RWA (Real World Assets) sector, which is on the brink of explosion. The sharp decline of related concept tokens like ONDO also reflects that the market's previous expectations for comprehensive compliance of "U.S. stocks on-chain" may have been overly optimistic. However, it is undeniable that whether the regulatory stance swings or not, the trend of integrating U.S. stock assets with blockchain technology has already become an irreversible tide. In the shadow of this regulatory game, both the crypto-native forces and traditional Wall Street institutions are racing madly in their respective tracks.

- On one hand, crypto-native forces are tearing open gaps from the bottom up. Projects like Ondo, xStocks, and MSX are actively bringing U.S. stock assets on-chain, while Hyperliquid, Trade.xyz, and major CEXs are providing a window for global crypto users to invest in U.S. stocks through perpetual contracts. This bottom-up demand for innovation is continuously pressuring regulators to provide clear responses.

- On the other hand, Wall Street is also accelerating its layout of related businesses. The U.S. Depository Trust & Clearing Corporation (DTCC) plans to officially launch limited production trading of tokenized assets in July this year and expand its promotion in October; Nasdaq is also busy developing a blockchain-based stock issuance framework; Intercontinental Exchange (ICE) has chosen to collaborate with top exchanges in the crypto space like OKX to jointly promote the research and development of tokenized stocks and crypto-related products.

In essence, this postponement of the exemption is actually a fierce collision between the innovative attempts of new forces and the defensive mechanisms of traditional powers. Based on the current developments, the SEC has not yet made a final decision on the revised draft, which also means that the "innovation exemption" has not been completely dead, but it can be anticipated that under the crazy backlash from Wall Street giants and the modifications of opinions within the SEC, even if this exemption can be reintroduced in the future, its radicalness and applicability may experience certain "discounts."

The dream of completely opening up "tokenized stock" trading may need to traverse a long road in the tug-of-war of regulation, but the door to asset tokenization has already been burst open and is destined not to close again.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。