A couple of days ago, The Wall Street Journal published a report featuring a hedge fund that almost no one has heard of, named Darsana Capital.

This fund was established in 2014 and is relatively small. In 2019, it made a decision: to bet on a rocket company that had yet to go public. That year, SpaceX was valued at about $30 billion.

Seven years later, SpaceX is about to go public, with a valuation of $1.75 trillion. The roughly $600 million that Darsana invested that year is now worth about $15 billion. This bet is one of the most profitable hedge fund trades in Wall Street history. SpaceX constitutes nearly 60% of Darsana's total assets.

SpaceX, the largest IPO in history, also marked the kickoff of this year's wave of tech company listings. Stories like Darsana's have been making headlines recently. Google invested $900 million in 2015, which is now worth over a hundred billion. Founders Fund's $20 million lifeline from 2008 has now ballooned to $19.5 billion.

But turning to other reports, the tone changes completely.

At the end of March, Bloomberg and Reuters reported a strange occurrence: a group of investors bought shares in SpaceX but could not confirm whether they actually owned them. One entrepreneur named Tejpaul Bhatia believes he holds SpaceX shares, but has no way to verify whether these shares, which should belong to him, are genuine.

On one side, there's a wealth creation myth precise to the hundred million; on the other, there are those who can't even confirm whether they bought anything. How can the same company and the same IPO produce such a divide?

The Private Secondary Market under "AI Anxiety"

In the past couple of years, AI has driven the valuations in the primary market to outrageous heights.

OpenAI, Anthropic, xAI, SpaceX—these companies have valuations easily in the hundreds of billions, even trillions, and they continue to soar. Average investors looking at these numbers are left with one thought: "I want a piece of that too."

The number of people wanting to get in has never been higher. The trouble is, all these companies are not publicly listed. For ordinary people wanting to buy in before an IPO, almost no channels are available.

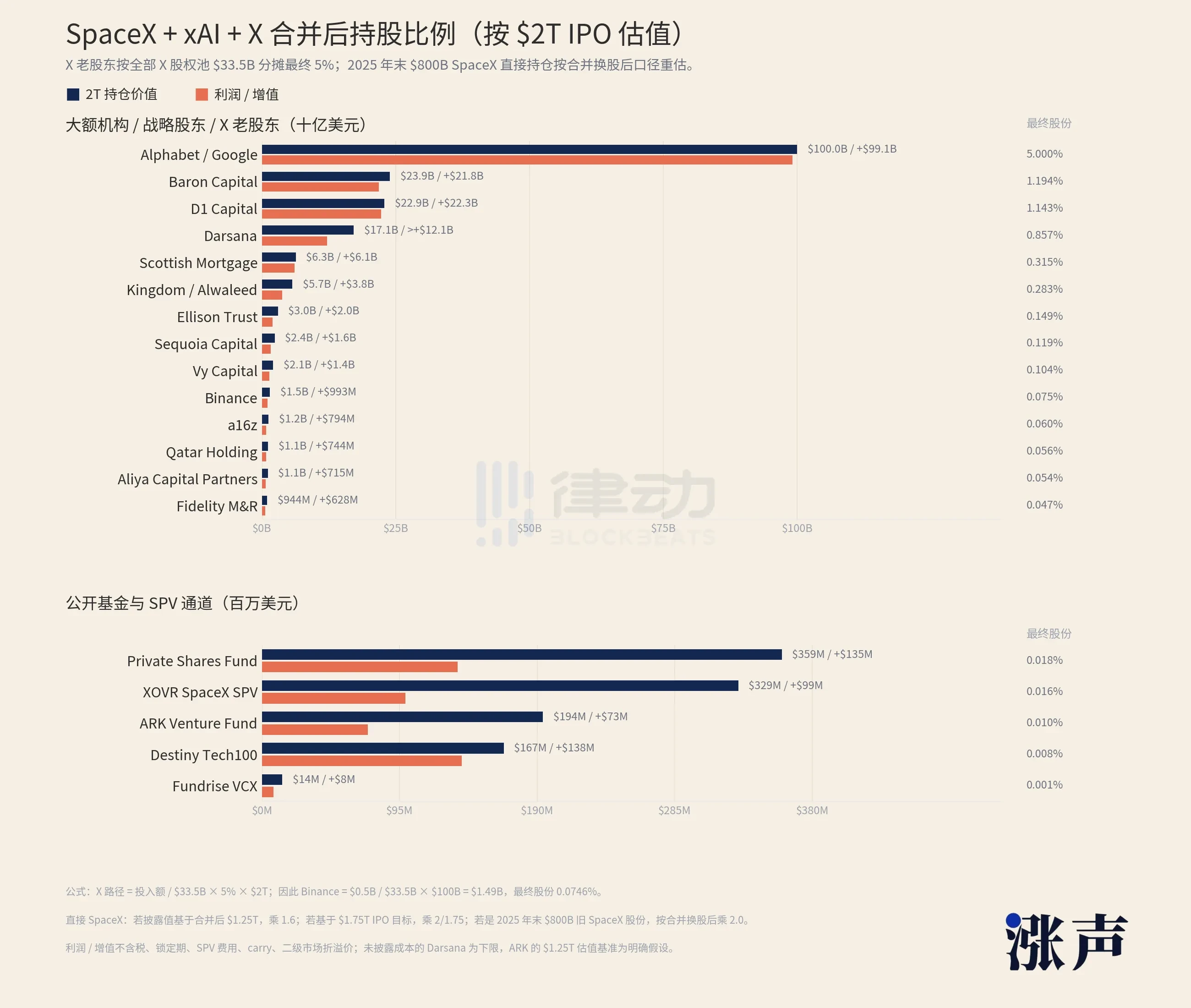

Looking at the list of SpaceX shareholders makes it clear. Large institutions and strategic shareholders hold stakes worth tens of billions or hundreds of billions; Alphabet, Google's parent company, alone holds over a hundred billion. Right now, all the public channels available—such as a few ETFs and funds holding SpaceX—add up to an exposure of about $1 billion.

How much can investment institutions earn from SpaceX, estimated at a valuation of $2 trillion?

Moreover, most channels still keep ordinary people out. The majority of private market avenues are only open to accredited investors. In the United States, this means an annual income of over $200,000 or assets exceeding $1 million excluding primary residences. Those who can't meet this threshold may not even be able to squeeze into that $1 billion small outlet.

In other circumstances, such disparity might deter people. But the logic of FOMO (Fear of Missing Out) works the opposite way. The scarcer the opportunity, and the more they see others making money, the more eager they are to get in.

Money has not exited the market. It's surged into an area known as the private secondary market.

This market specializes in trading shares of private companies. Early investors and employees wanting to cash out, along with those who didn't get early tickets but wish to enter, are matched by platforms, funds, and various intermediaries.

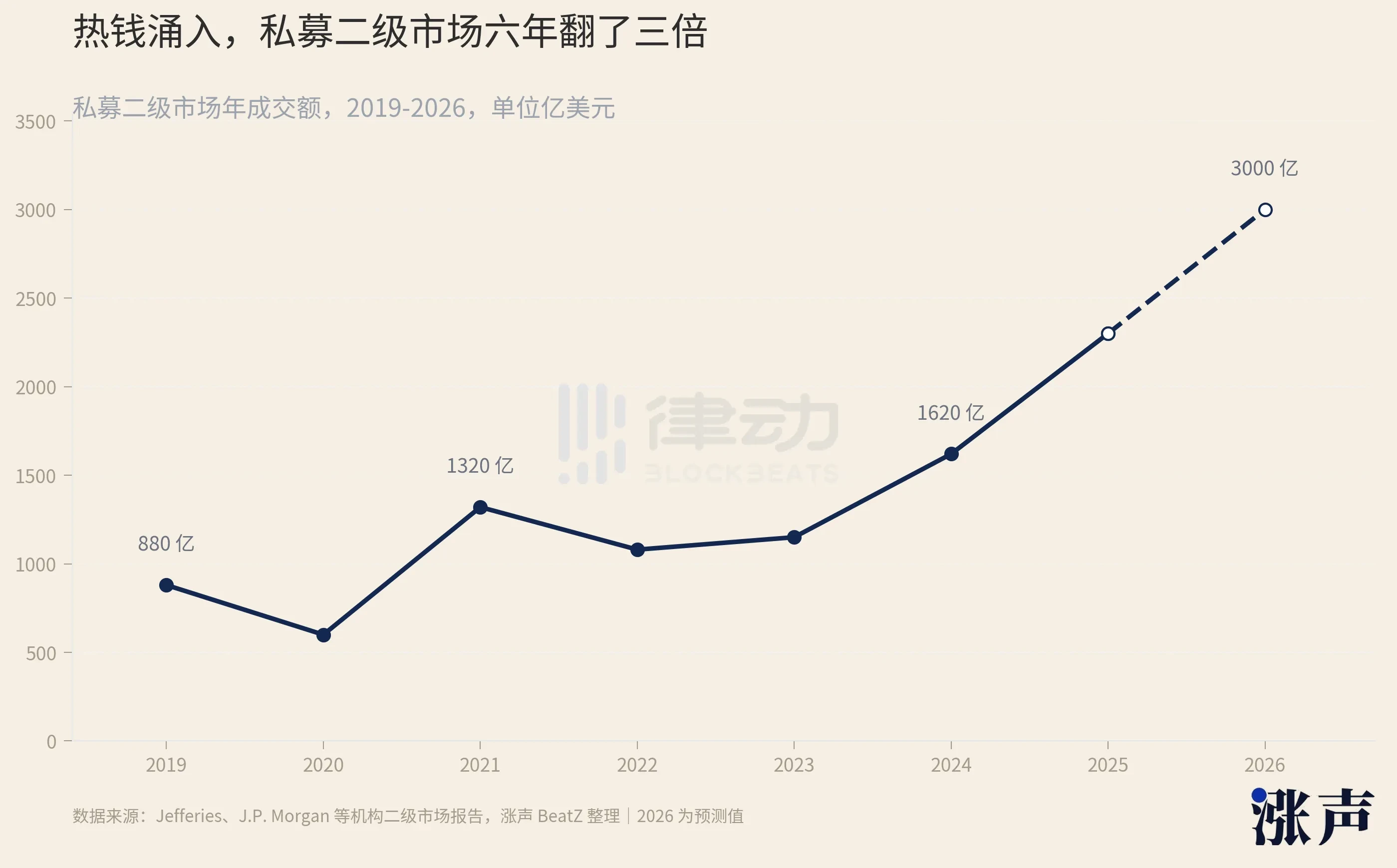

In recent years, this market has inflated tremendously. From 2019 to now, its size has tripled. In 2024, the total transactions are expected to reach approximately $162 billion, rising to around $230 billion in 2025 and anticipated to touch $250 billion in 2026. The number of companies willing to allow shares for secondary transfer has increased from 12 to 31 in just a year.

As money flows in, sellers of SpaceX shares emerge.

How many have come out? According to The New York Times, there are at least 170 special purpose vehicles (SPVs) that have purchased SpaceX shares. An SPV is a shell that can hold shares of SpaceX; whoever manages to obtain any SpaceX shares puts them into this shell and sells shares of the shell to later investors. 170 shells, all revolving around the same company.

These SPVs come from all sorts of backgrounds.

In October 2025, an institution called Witz Ventures launched an SPV on the fundraising platform Republic, named The Cashmere Fund, which bundled together xAI, SpaceX, and Perplexity—three of the hottest targets—to sell to retail investors. About 150 listeners of a financial podcast called Rich Habits collectively bought into SpaceX. Rapper 2 Chainz and SkyBridge founder Anthony Scaramucci have both publicly stated that they hold SpaceX shares.

Retired NBA player Tristan Thompson stated on the show that he invested in SpaceX when it was valued at $300 billion

The issue is that the swarm of intermediaries emerging is of varying quality.

One such institution, Vika Ventures, collected $5.9 million from investors with a promise to buy SpaceX shares. Later investigations uncovered that the founder of this institution used the funds to buy luxury watches and a private jet. In 2023, another financial broker was sentenced to eight years for defrauding over 50 investors of nearly $6 million by selling pre-IPO shares, including shares in SpaceX.

Another once-popular platform, Linqto, focused on celebrity targets like SpaceX; it went bankrupt in 2025, and the SEC is investigating whether it properly verified the accredited investor status of its users, affecting over 13,000 investors.

Even if you encounter someone who is not a scammer, things might still be unclear.

DataPower Capital is an institution dealing in SpaceX shares. Its founder David Yakobovitch told The New York Times that he only accepts transactions that are one layer removed from SpaceX itself. "Once you go down a few layers," he says, "things start to get murky."

Trapped in the Fifth Layer

Returning to the 150 podcast listeners of Rich Habits. What they bought was not SpaceX.

They purchased Witz Ventures, and Witz Ventures bought shares of DataPower Capital. DataPower is the one who directly received shares from SpaceX shareholder registries. This means that a typical person placing an order after listening to the podcast is separated by at least two to three layers from actual SpaceX stock.

With each additional layer, two things happen simultaneously.

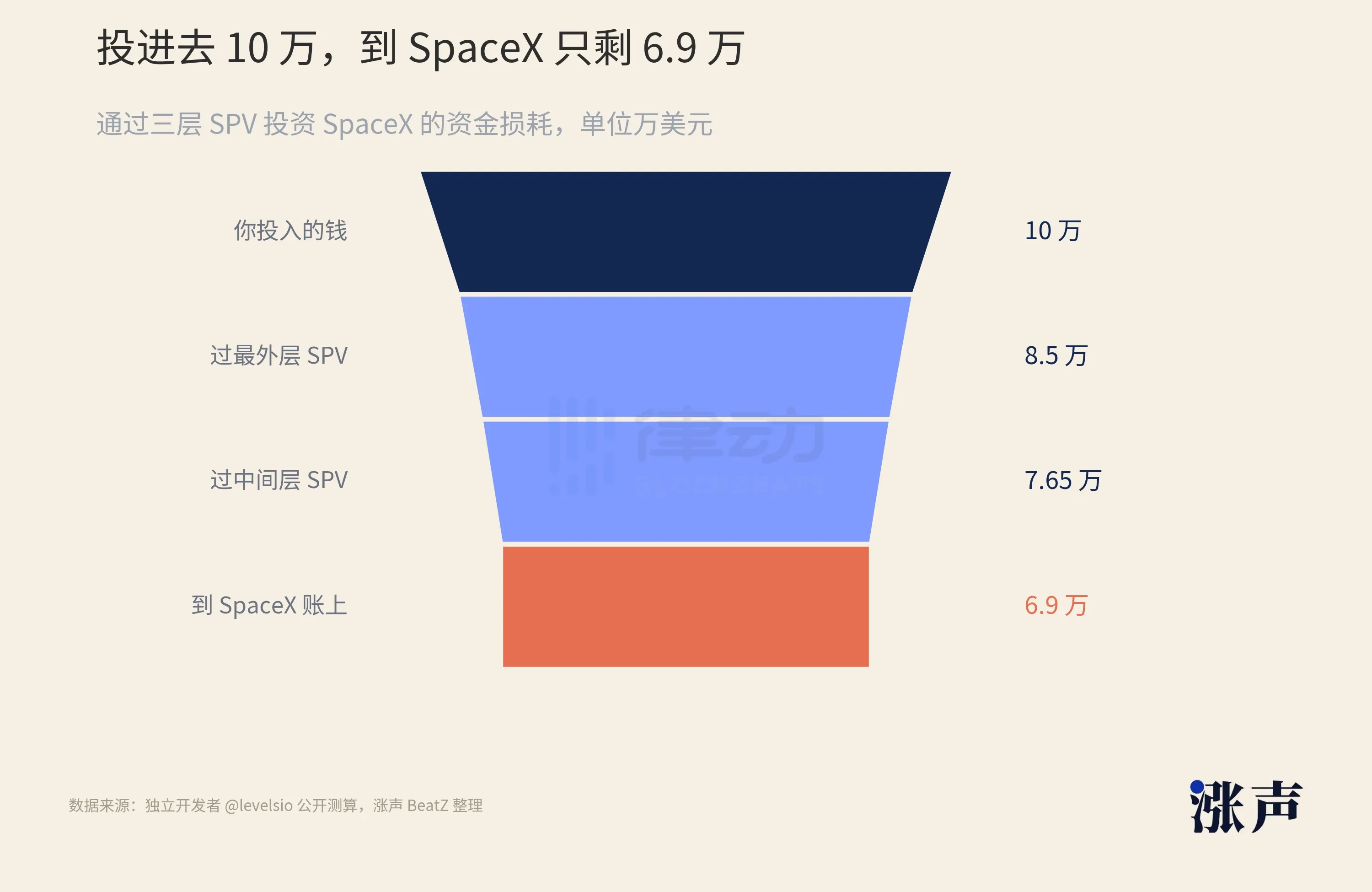

The first is that the money diminishes. Independent developer levelsio calculated on social media: assuming you invest $100,000 into SpaceX through three layers of SPVs, the outermost layer will charge a 6% setup fee, and the two inner layers will each take their own management fees and profit shares, leaving only about $69,000 to reach SpaceX. You haven't even started to earn, and already 30% is gone.

The second is that the truth becomes more distant. This SPV structure has a critical feature: every layer of investors can only see the layer directly above them. If you buy into the outer layer, the layer manager tells you that it holds the next layer. Is that next layer genuine? And is there any SpaceX stock underpinning it? You can't see it, nor are you entitled to investigate.

With 170 shells, you may end up with as many as five layers deep. This is why individuals like Bhatia cannot confirm their holdings. It is not that they aren't attentive; the structure was designed not to allow outsiders to see inside.

Why can SpaceX's nesting doll structure go so deep?

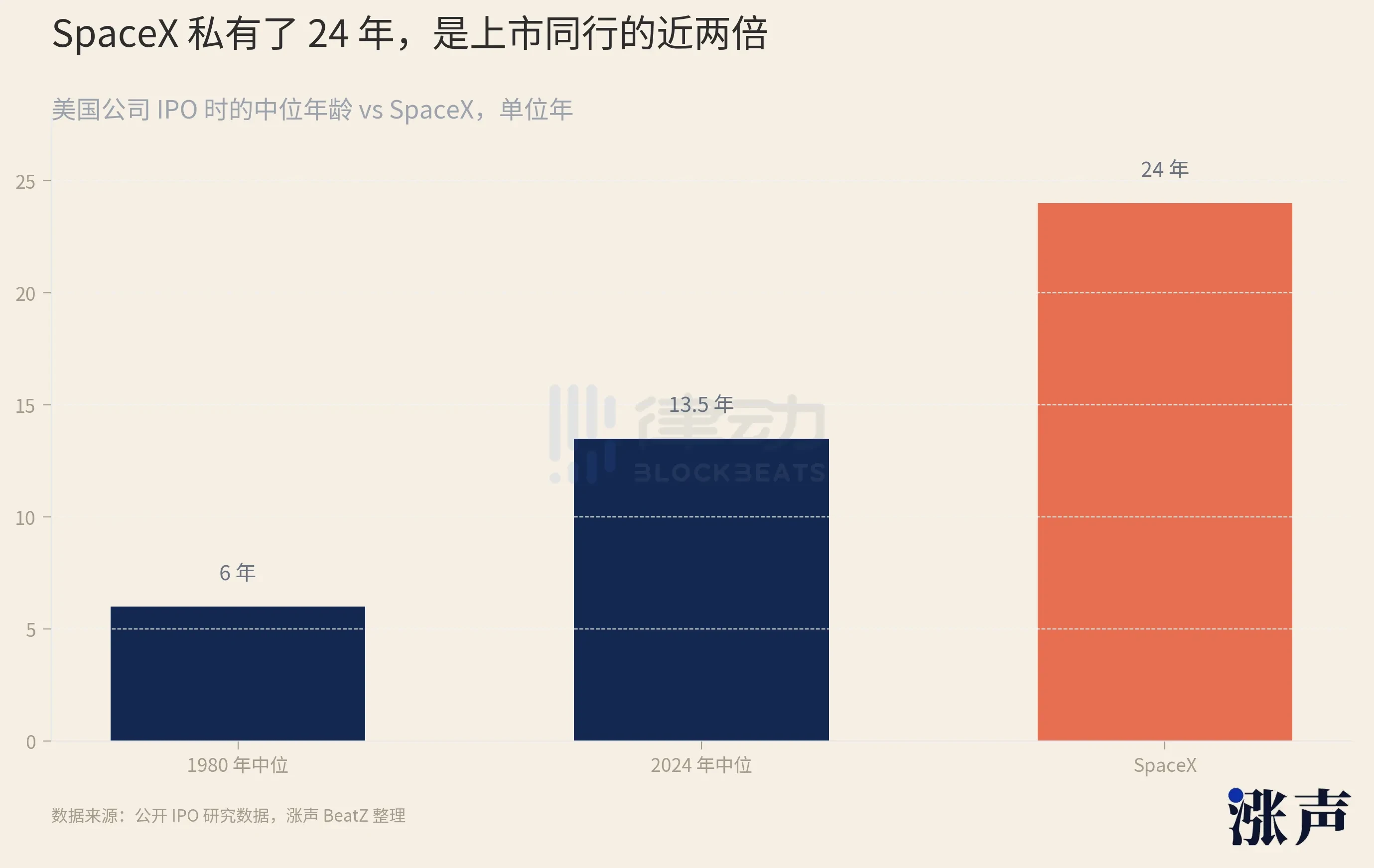

This situation can be attributed to how long it has been in the private market. Founded in 2002, SpaceX still has not gone public as of 2026, thus remaining private for a full 24 years.

What does 24 years mean? The tech companies that went public in 1999 were, on average, only four years old. The ones from 2014 averaged 11 years. In recent years, the median age of companies going public in the U.S. has risen to 14 years. SpaceX's 24 years represents an extreme on this already lengthening curve.

The longer a company spends in the private market, the longer its shares are repeatedly bought, sold, and nested in shells. SpaceX shares have been circulating outside for over 20 years, and layers have accumulated long ago.

The lengthening of the private period is not just unique to SpaceX.

Over the years, the median age of U.S. companies going public has increased from six years in 1980 to about 13.5 years in 2024. The reason is not complicated; there is simply too much money in the private market.

As of 2023, there is still over $650 billion in uninvested money in global venture capital. With companies not lacking for funding, they naturally have no urgency to go public and face the scrutiny and financial reporting pressures of the public market. Consequently, there are more and more unicorns valued at over $1 billion; currently, there are more than 1,500 worldwide, worth a total of $6 trillion, most of which have not raised money through public valuations in over three years.

The longer companies remain in the private market, the longer employees and early investors have their shares locked up. These individuals wanting to cash out have the secondary market as their only exit. As demand piles up, SPVs catering to these needs emerge in large numbers.

In the peak year of 2021 for venture capital, the number of SPVs established in the U.S. grew by 235% year-on-year. By the third quarter of 2024, there were over 2,400 SPVs that were countable and still operational. A tool being used on such a large scale and repetitively for over twenty years, ending up nested to the fifth layer, is almost inevitable.

Furthermore, SpaceX happens to be one of the strictest in managing its stock in the entire private market. Externally, in almost every share transfer, SpaceX exercises its right of first refusal, preventing sales in advance. It also conducts share buybacks every six months, acquiring the shares that employees wish to sell back into its own control.

The tighter the door is welded shut, the pricier the tickets at the entrance become.

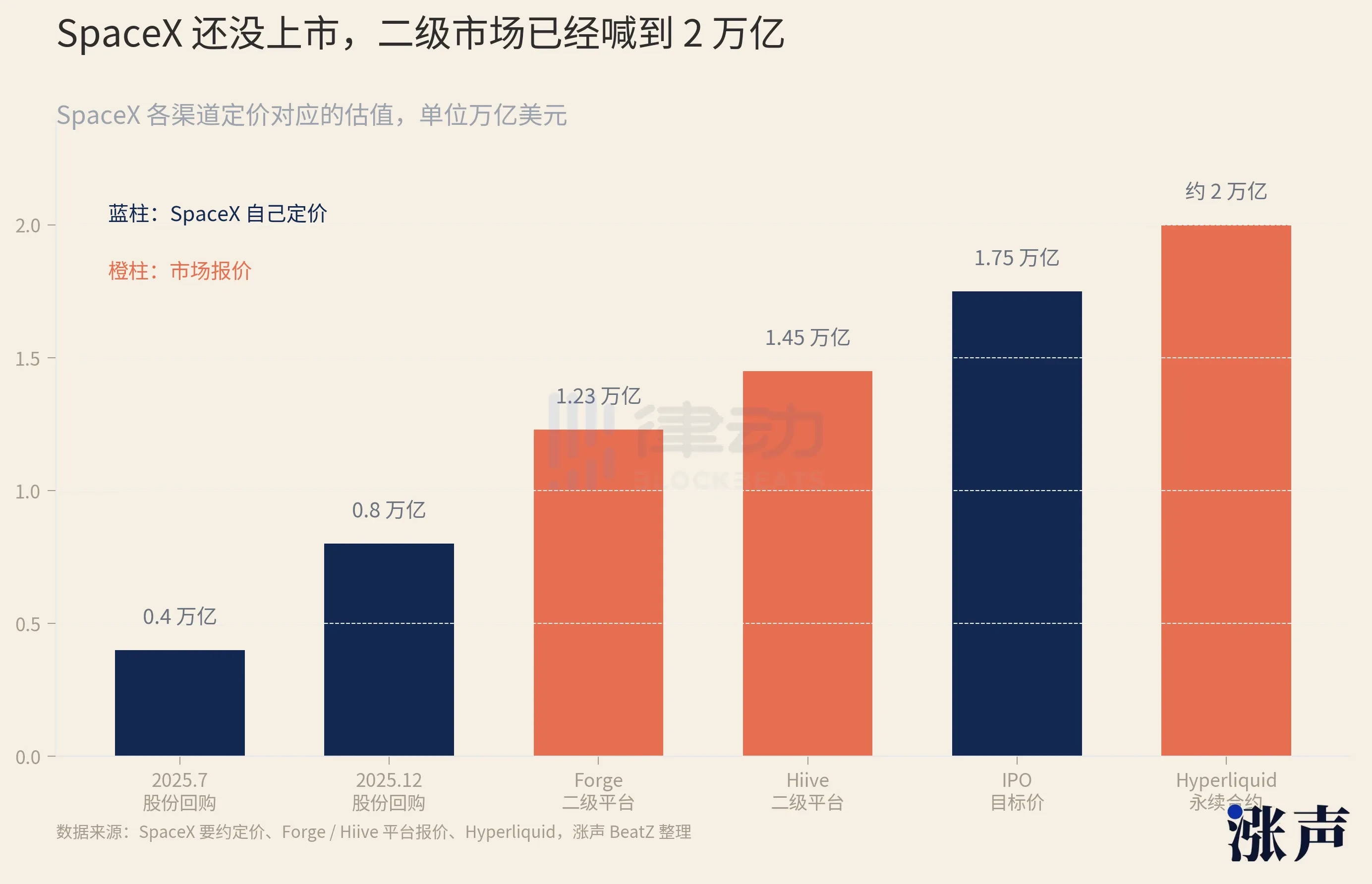

SpaceX has set its own pricing: for a share buyback in July 2025, the valuation was set at $400 billion; six months later, it doubled to $800 billion. But offers in the secondary market have run ahead. The Forge platform valued it at around $1.23 trillion, Hiive at $1.45 trillion, and the crypto trading platform Hyperliquid even listed contracts corresponding to valuations of over $2 trillion, exceeding SpaceX's own target public valuation.

An even more tangled issue arises from mergers. In March 2025, Musk merged X, the former Twitter, into his AI company xAI. In February 2026, SpaceX fully absorbed xAI. People who had previously purchased Twitter or xAI, along with all the shells behind them, ended up on SpaceX's shareholder list after two layers of share exchanges.

Opening Blind Boxes

At this level of nesting, the company itself is also becoming restless.

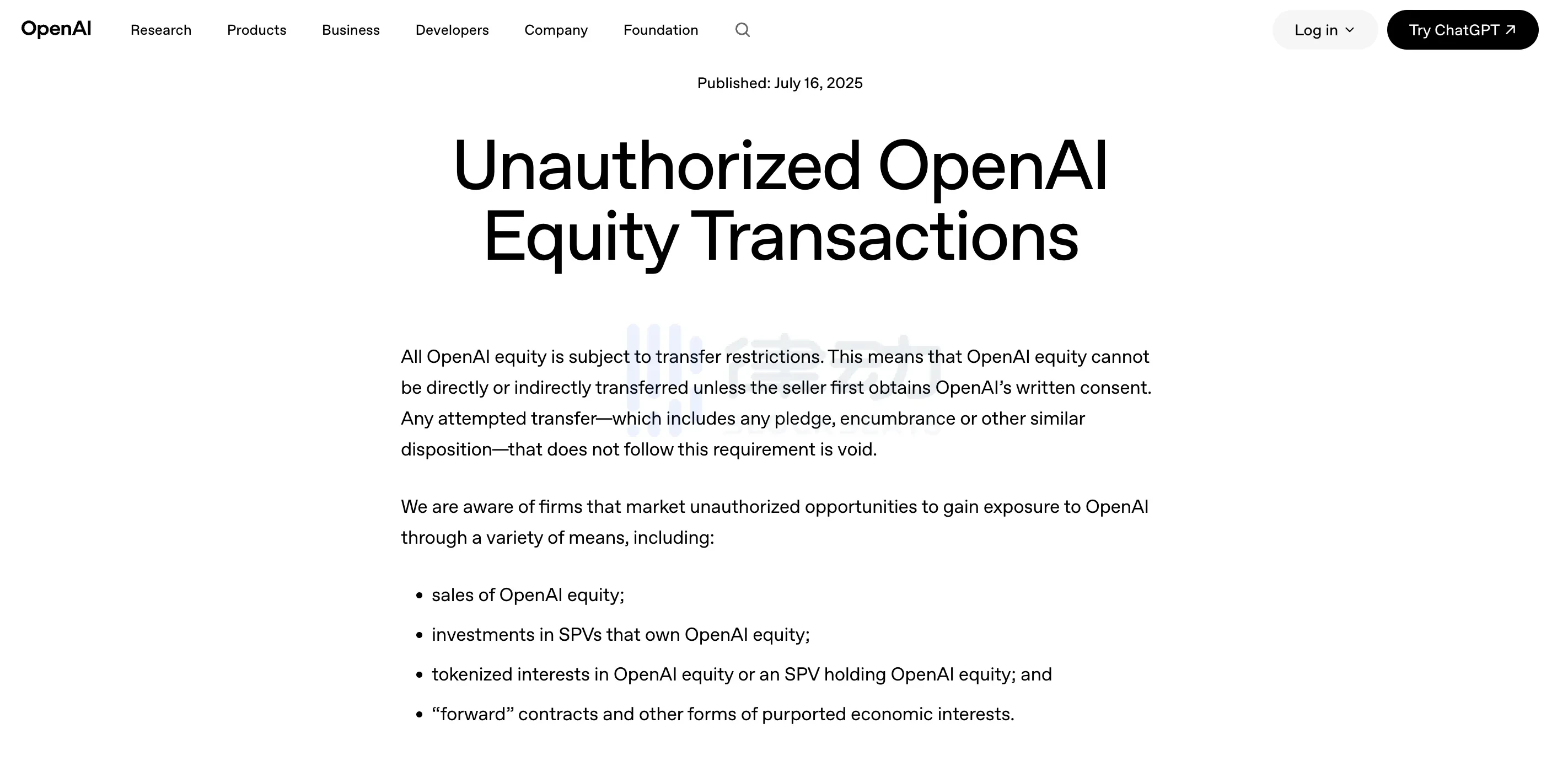

In May 2026, Anthropic and OpenAI both publicly issued statements clearly informing the market that any share transfers not approved by the board would be deemed invalid and would not be recorded in the company's accounts. They specifically named eight platforms, including Forge and Hiive, as unauthorized. Following the announcement, related tokens in the on-chain secondary market that were focused on pre-IPO shares plummeted by 30% to 40% in a single day.

This kind of statement regarding secondary market transactions is not a spontaneous decision from one or two companies.

Recently, when the robotics company Figure AI was rumored to be valued at $39.5 billion, it also moved to halt secondary trading of its own shares. Many of the most sought-after targets in the private market, like Anthropic, SpaceX, Anduril, Stripe, and Databricks, have been taking the same action: reducing the tolerance for secondary trading to zero.

Why did they collectively turn against it?

This involves a little-noticed "red line" for IPOs. According to U.S. regulations, as soon as a company has more than 2,000 shareholders, it must publicly disclose its financials regularly, just like a public company, even if it hasn't gone public yet. The nesting SPV structure makes it difficult for the company to count its actual number of shareholders. An SPV counts as one on the register, but it may contain hundreds of individuals. Once a company unwittingly crosses the line of 2,000, it is forced to open its books.

Another reason relates to the pricing of employee stock options. If a company’s shares are traded freely in the secondary market at inflated prices, then when it sets the exercise price for stock options offered to employees, it must reckon with that number. The crazier the secondary market, the less valuable the options in employees' hands become.

More importantly, there is the issue of information. Shareholders are legally entitled to receive information about the company’s operations. For AI companies, model architecture, training data, and computing resource arrangements are the most sensitive trade secrets. When a company cannot even count its shareholders accurately, it cannot tell where this information is flowing to.

Removing an unclear number of shareholders, maintaining the pricing of options, and closing off information avenues are fairly standard actions. However, when the secondary market ballooned to $230 billion and nesting reached five layers, companies found that private measures could no longer contain the situation. Thus, they stepped into the spotlight and made the statement "Your shares are invalid" public for the first time. SpaceX did not follow with a similar statement, but its right of first refusal serves the same purpose.

The company's "invalid" declaration left those with multiple layers of shells completely suspended. You purchased an SPV and paid for it. Whether the underlying SpaceX shares were issued and valid remains unknown until the company publicly reconciles the accounts.

Thus, buying an SPV for SpaceX has increasingly come to resemble opening a blind box.

The time to open the box is predetermined. On June 12, when SpaceX rings the bell on NASDAQ, its submitted IPO documents will first include a public, verifiable shareholder register. Each and every layer that has been wrapped around its stock over the past twenty years must be reconciled at that moment. If everything matches, the box contains real stock; if it doesn't, it’s just a worthless piece of paper. On that day, Bhatia will know what he actually got.

But after SpaceX, there are still OpenAI, Anthropic, and a long list of names in line. A few scrolls through social media will reveal posts offering "代投" (proxy investment) opportunities in these hottest AI companies.

The hot money generated by AI in recent years is overflowing. There are only a handful of truly worth buying targets, all tightly locked up. With too much money and too narrow a gate, countless shells emerge in between.

As long as this imbalance persists, the private secondary market will remain as it is: a blind box that everyone wants to play with, yet no one can clearly say what they actually drew.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。