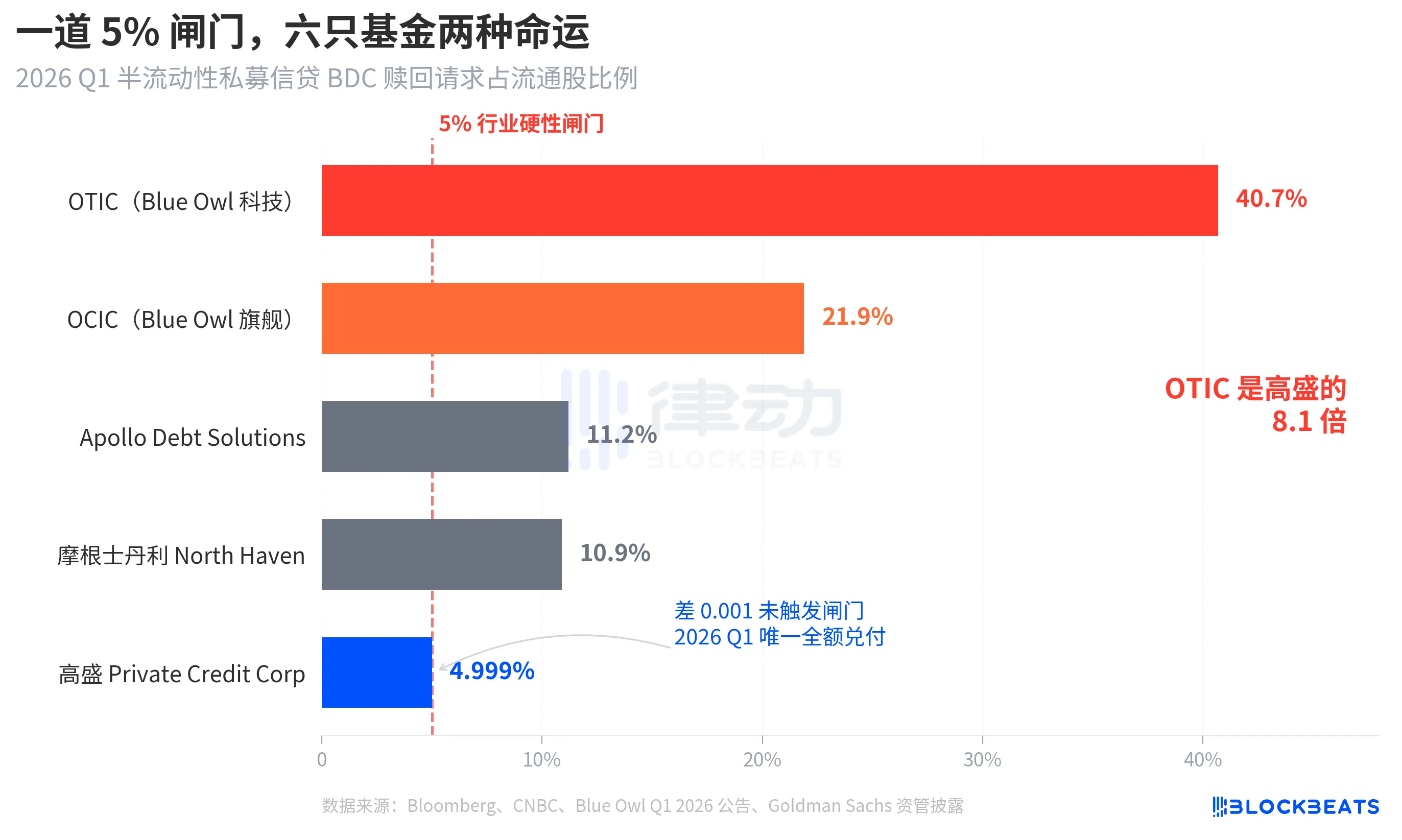

On April 6, 2026, Monday's closing, the stock price of American private credit asset management giant Blue Owl Capital (OWL) fell to $8.45, setting a new weekly low since its listing, and at one point dipped to $7.80 during the day. The trigger for this round of sell-off was the quarterly redemption data of the semi-liquid fund released by Blue Owl the previous Thursday. Its two main non-traded BDC (Business Development Company) funds, OTIC (Blue Owl Technology Income) and OCIC (Blue Owl Credit Income), received approximately $5.4 billion in redemption requests from investors this quarter, with OTIC's redemption rate reaching 40.7% of the outstanding shares and OCIC at 21.9%. Both funds triggered a 5% industry hard gate, releasing less than $1.2 billion proportionally.

Major financial media immediately packaged this incident as "retail investors' private credit narrative collapse" and "AI disrupting software companies spilling over to creditors." But these two labels obscure a more critical issue. The same week, the redemption request ratio for Goldman Sachs Private Credit Corp, under Goldman Sachs Asset Management, was 4.999%, just 0.001 percentage points away from the 5% gate, making it one of the few, possibly the only large semi-liquid perpetual BDC that did not trigger its gate and fully paid out redemption investors. This wave of redemptions is not a "private credit collapse," but a clear K-shaped differentiation.

According to a Bloomberg report on April 6, Goldman Sachs' fund, with a size of $15.7 billion, is an anomaly that "dodged the exodus" this quarter. Meanwhile, Blue Owl's OTIC redemption rate is 8.1 times that of Goldman Sachs, and OCIC is 4.4 times. While the market's attention is entirely focused on Blue Owl's plunge, the real question worth asking is why two institutions with the same structure, in the same week, under the same 5% gate presented completely different outcomes.

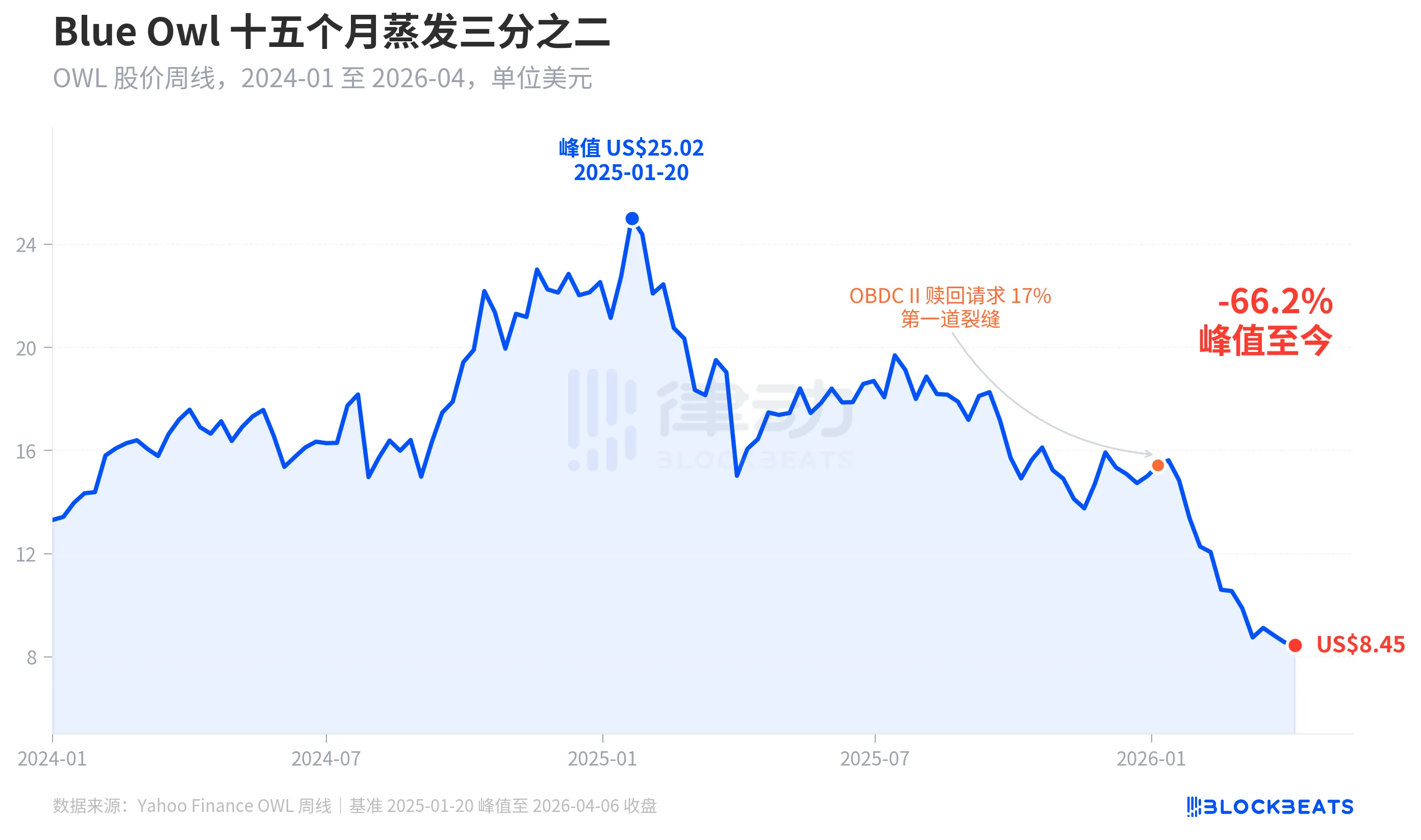

Stock Price Lost Two-thirds in Fifteen Months

First, let's look at how the market priced Blue Owl. According to historical weekly data from Yahoo Finance, Blue Owl Capital (OWL) closed at $25.02 in the week of January 20, 2025, marking an all-time high. By the week of April 6, 2026, it closed at $8.45, a drop of 66.2% in fifteen months, evaporating nearly two-thirds of its market value.

The stock price first showed a significant crack in early January 2026 when another fund under Blue Owl, OBDC II (a smaller non-public BDC), disclosed redemption requests equivalent to 17% of its outstanding shares, which was seen as the "first crack." Subsequently, the stock price declined continuously until the end of the first quarter, when both main funds, OTIC and OCIC, simultaneously triggered their gates, with the stock hitting an absolute low of $7.80 since its listing.

Interestingly, Blue Owl's stock price drop (-66.2%) far exceeds the deterioration of its fundamentals. OCIC still holds $36 billion in AUM, and the net asset value fell by about 6.5% in the first quarter of 2026, with the company's overall management scale still above $290 billion. The market has obviously been repricing this company based on "uncertainty of future payouts" and "collapse of valuation confidence," rather than solely on current performance.

Same Gate, Different Fates

What truly clarifies the "K-shaped differentiation" is the cross-section. When placing together the five large semi-liquid perpetual BDCs that publicly disclosed redemption data in the first quarter of 2026, the structure becomes clear.

According to Bloomberg, CNBC, and company announcements from the funds, the redemption rates for the five funds are Blue Owl OTIC 40.7%, Blue Owl OCIC 21.9%, Apollo Debt Solutions 11.2%, Morgan Stanley North Haven Private Income Fund 10.9%, and Goldman Sachs Goldman Sachs Private Credit Corp 4.999%. These five funds can roughly be categorized into three tiers.

In the upper tier, Blue Owl's two funds far exceeded the gate, with OTIC's almost half its holders wanting to withdraw, and OCIC close to four times the gate. According to regulations, only up to 5% of the outstanding shares were allowed for redemption, OTIC actually paid out about $179 million, while OCIC paid out about $988 million, locking over $4.2 billion in redemption requests outside the gate.

In the middle tier, Apollo and Morgan Stanley had redemption rates between 10% and 11%. According to reports from Bloomberg on March 11 and March 23, Apollo Debt Solutions paid about 45% of requests, and North Haven paid about 46%. Although they also triggered the gate, the pressure was significantly less than for Blue Owl.

In the lower tier, only Goldman Sachs remained. At 4.999%, it was the only large fund during the period that did not trigger the 5% gate, paying out 100% of all redemption requests.

Bloomberg used the term "Dodges Exodus" in its article title; the fact that OTIC is 8.1 times that number has already indicated the severity of the differentiation. In the same week, with the same structure and rule, the two institutions ended up with completely different fates.

Bubble, Retail Investors Elevated It by 4.4 Times

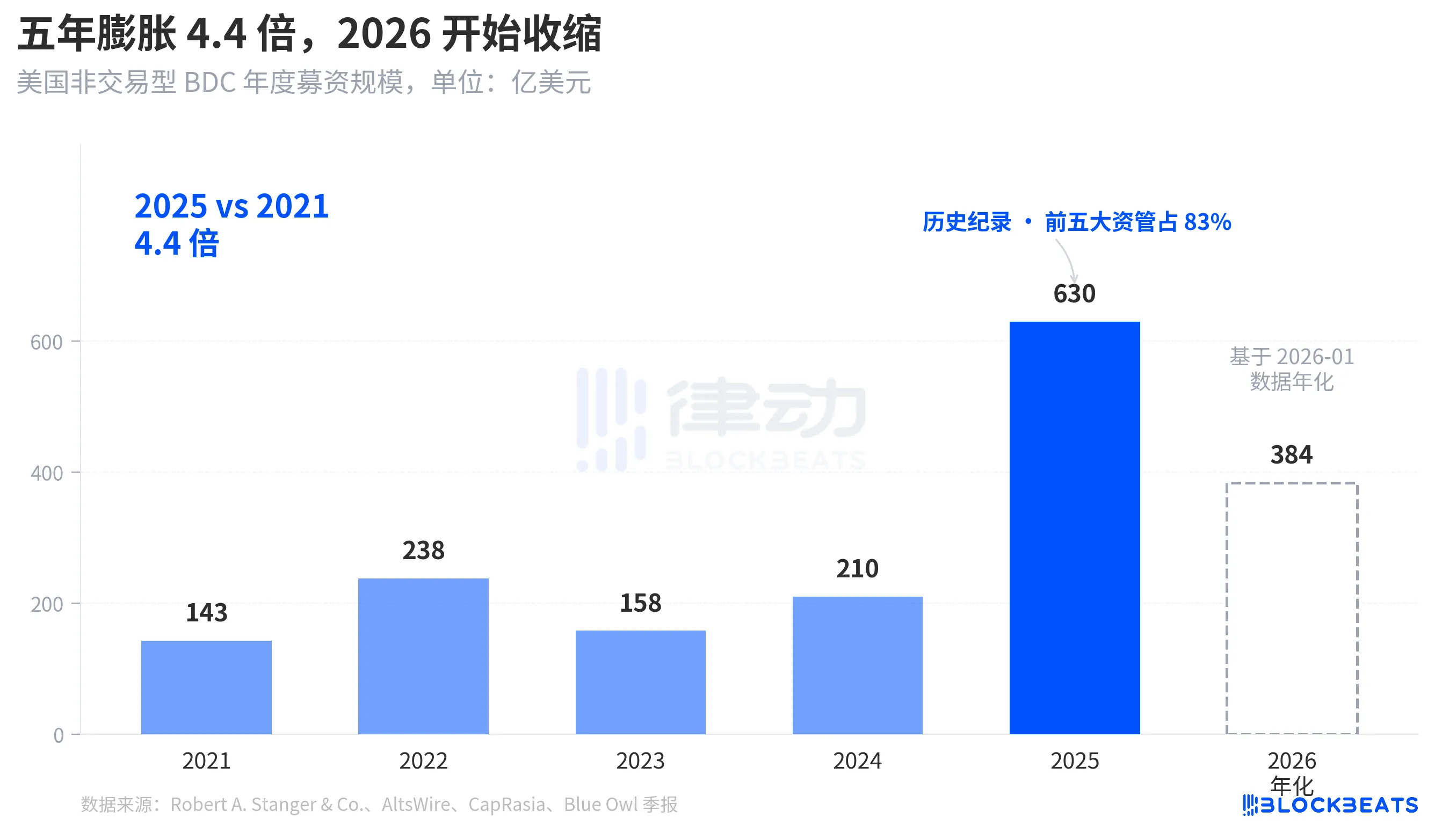

To understand why this wave of redemptions came so strong, one must first look at how deep the incoming money was. According to industry statistics from Robert A. Stanger & Co., the annual fundraising scale of non-traded BDCs in the past five years shows a distinct parabolic trend.

In 2021, it raised $14.3 billion, and by 2025, it reached a historical record of $63 billion, amplifying 4.4 times in five years. The same statistics show that the top five institutions (Blackstone, Blue Owl, Apollo, Ares, and HPS) took about 83% of that, amounting to approximately $52.3 billion concentrated in these top five. The influx of retail capital over the past five years not only is massive in total but also extremely concentrated in distribution.

However, by January 2026, single-month data from Stanger showed that non-traded BDC fundraising was only $3.2 billion, nearly halving compared to the peak of $6.2 billion in March 2025. According to reports from Connect Money and FinancialContent, overall BDC sales fell by about 40% in the first quarter of 2026 compared to the same period last year. In the same quarter that investors began requesting redemptions in concentration, new capital was visibly slowing down, creating simultaneous upward pressure for redemption and downward pressure for new subscriptions, forcing the gate to be stepped on more forcefully than anyone expected.

This is not a cyclical pullback but represents a reassessment of the narrative that semi-liquid perpetual BDCs are sold as a "savings-like product" to retail investors, now being reconsidered at the funding level for the first time.

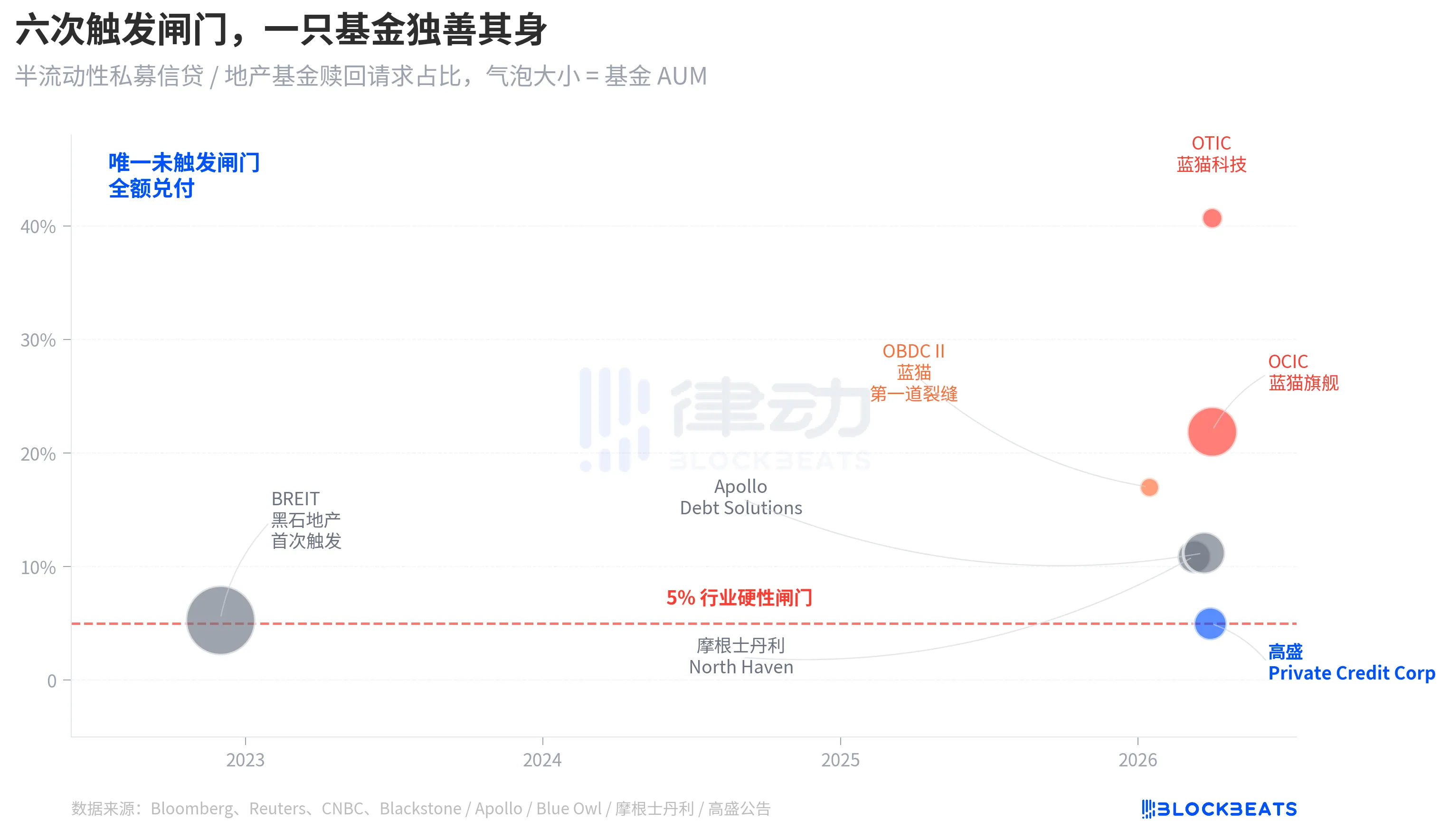

From BREIT to Blue Owl, Vulnerability Gradually Surface Over Four Years

Placing this wave of redemptions on a longer timeline, it becomes evident that it did not erupt suddenly.

The "semi-liquid perpetual" structure has two layers of commitments. It allows funds not to be listed or publicly valued while promising investors that a portion of their shares can be redeemed each quarter at NAV. Essentially, this packages illiquid assets (private credit, private real estate) into a product that appears to be "withdrawable at any time." To prevent bank runs, the industry set a uniform 5% quarterly redemption gate; once quarterly redemption requests exceed 5% of outstanding shares, the fund pays proportional amounts, while the remaining requests are locked for the next quarter.

In November 2022, BREIT, a non-traded real estate trust under Blackstone, first triggered this gate, becoming the first systematic liquidity event for the perpetual semi-liquid structure. According to Caproasia's data, in January 2023, BREIT only released 25% of all requests in a single month, totaling $14.3 billion in redemptions by November 2023. That incident was interpreted as an isolated case for the real estate asset class, with the private credit market not being dragged down.

Four years later, the same cracks spread from real estate to credit. In January 2026, Blue Owl OBDC II disclosed a 17% redemption request, becoming the first signal. On March 11, Morgan Stanley North Haven triggered the gate. On March 23, Apollo Debt Solutions triggered the gate. On April 2, Blue Owl OCIC and OTIC triggered their gates simultaneously. Within seven days, four major asset management BDCs stepped into the same threshold, while Goldman Sachs remained outside the gate with a difference of 4.999% in the same quarter.

The structural vulnerability of semi-liquid perpetual BDCs was not just exposed by Blue Owl’s redemption wave; it has been on the table since BREIT’s trigger in 2022, yet no one truly acknowledged it over the past four years.

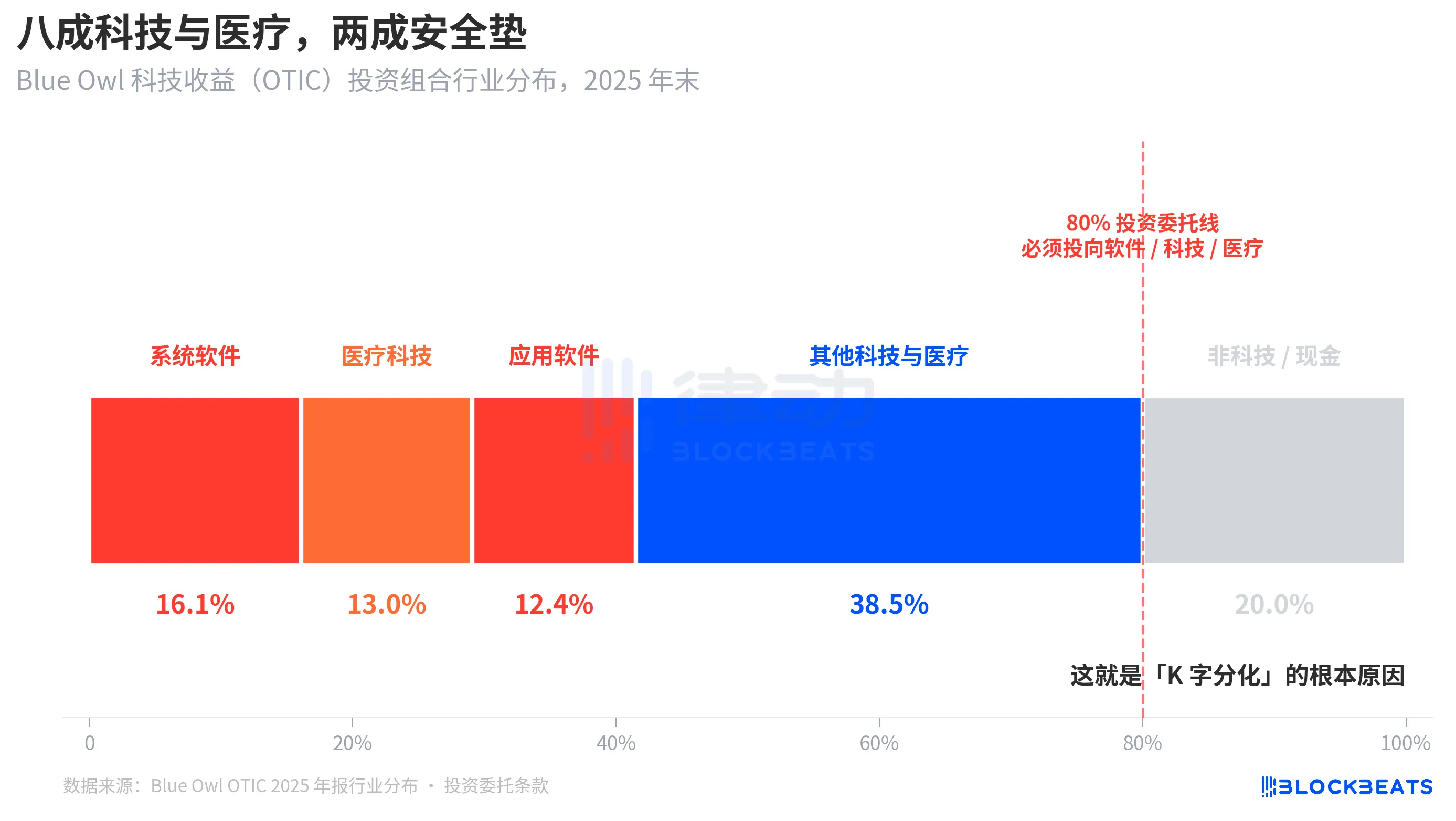

Root Cause, 80% of OTIC Concentrated in Technology and Healthcare

Now returning to the critical question, why did Goldman Sachs and Blue Owl have outcomes differing by 8 times despite having the same structure and same week? Breaking down OTIC's investment portfolio provides clarity on the answer.

According to KBRA rating reports and Blue Owl OTIC’s Q4 2024 financial report, as of the end of 2025, OTIC's portfolio was sized at $6.2 billion, holding 190 companies across 39 end markets, of which 92% have private equity backing, and 93% are first lien senior secured loans. On the surface, it appears to be a fund of decent quality, but its industry concentration is quite special. System software at 16.1%, healthcare technology at 13.0%, and application software at 12.4% make up 41.5% of just these three sub-sectors.

The key issue is that this is not a temporary industry preference of the manager, but a hard rule codified in OTIC’s investment guidelines, with at least 80% of total assets required to be invested in "software and technology-related" companies. Blue Owl describes OTIC in public materials as "mainly investing in large, market-leading software companies providing mission-critical, recurring revenue solutions." From its inception, OTIC has been a SaaS technology credit fund.

Over the past six months, SaaS has been one of the asset classes most severely repriced by AI. When investors began to worry about "AI disrupting software companies’ long-term subscription revenues," a private credit fund with 80% exposure in software and technology would be on the front lines. According to reports from Bloomberg and Reuters, Blue Owl's management acknowledged in their communications with investors that part of the redemption pressure in the first quarter came from "concerns about AI disrupting software companies."

In contrast, Goldman Sachs Private Credit Corp's portfolio (with $15.7 billion AUM) has been described by Bloomberg as "significantly more diversified than its peers," with no single industry sector reaching OTIC's level of technology exposure. With the same private credit, using the same semi-liquid structure, and the same 5% gate, one fund has 80% exposure to current market themes while the other has less than 15%. As a result, one has a redemption rate of 40.7% while the other stands at 4.999%.

This is the fundamental reason for the "K-shaped differentiation." It is not that private credit as an asset class has collapsed, but rather that funds concentrated on the same market themes encountered issues, while diversified funds were hardly affected. The differentiation occurred at the risk exposure layer, not at the structural layer.

Conclusion

JPMorgan CEO Jamie Dimon, in the shareholder letter released on April 6, 2026, coinciding with Blue Owl's new low, wrote: "Private credit, overall, lacks transparency and strict loan valuation markings, which makes people more likely to choose to sell if they believe the environment will worsen, even if actual losses barely change."

Dimon's statement points to structural issues. Private credit is difficult to mark-to-market, and holders are more sensitive to perceived risks than actual losses. From reading this on April 7, 2026, there are two layers of meaning. One is that the 0.001 gap of Goldman Sachs is more a result of diversified structure rather than luck. The other is that the entire $1.8 trillion private credit market has not yet resolved the underlying contradiction of "liquidity and lack of transparency."

A 5% gate did not succeed in splitting Blue Owl and Goldman Sachs into "good funds" and "bad funds"; it simply settled “concentrated bets on current themes” and “diversification” as two different investment decisions in one K-line chart.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。