Text | Kaori

Editor | Sleepy.txt

Typing "create a card" in Claude, seconds later you will receive a Visa card. But this card is not for you, it is for AI.

Yesterday, there was a frenzy of discussions on X about a product demonstration video for generating virtual cards for large models. For ordinary people, applying for a virtual card for online transactions is not something new, but applying for a virtual credit card for AI has become a hot topic again after the rise of Agent, marking another development in the payment sector.

If you pay attention to this field, you will notice that similar excitement comes around every few months. In September 2025, there was the x402 protocol, where Coinbase and Cloudflare teamed up to turn HTTP status code 402 into a native payment channel for Agents. In October 2025, Visa and Mastercard simultaneously released Agent payment protocols. Now it's virtual cards.

The Agent payment sector is still highly fragmented; they each solve part of the problem, but no one has provided a complete solution. This article aims to answer several questions: What exactly is the Agent virtual card? How does it differ from x402? What problems can the virtual card solve, and what can it not solve? And where are the opportunities in this sector?

This article is sponsored by Kite AI

Kite is the first Layer 1 blockchain designed for AI agent payments. This underlying infrastructure enables autonomous AI agents to operate in an environment with verifiable identities, programmable governance, and native stablecoin settlement.

Kite was founded by senior experts in AI and data infrastructure from Databricks, Uber, and UC Berkeley, and has completed a $35 million funding round with investors including PayPal, General Catalyst, Coinbase Ventures, 8VC, and several top investment foundations.

What is the Agent virtual credit card?

You definitely don't want to hand over your credit card directly to an Agent, just as many people wouldn't install OpenClaw on their main computer.

The reason is simple: the risk exposure is uncontrollable. Regular credit cards have no single transaction limit, no merchant restrictions, and cannot be canceled immediately. Once an Agent makes a mistake or is attacked, your entire account is exposed to risk.

The Agent virtual card is not just giving AI a regular credit card; it is a programmable, limited payment credential. Each card can have a spending limit set, and if the Agent's spending exceeds the pre-set amount, the transaction will be automatically declined. You can also pause or close any card at any time without affecting your underlying bank account.

Overall, the core value of the virtual card lies in its controllability.

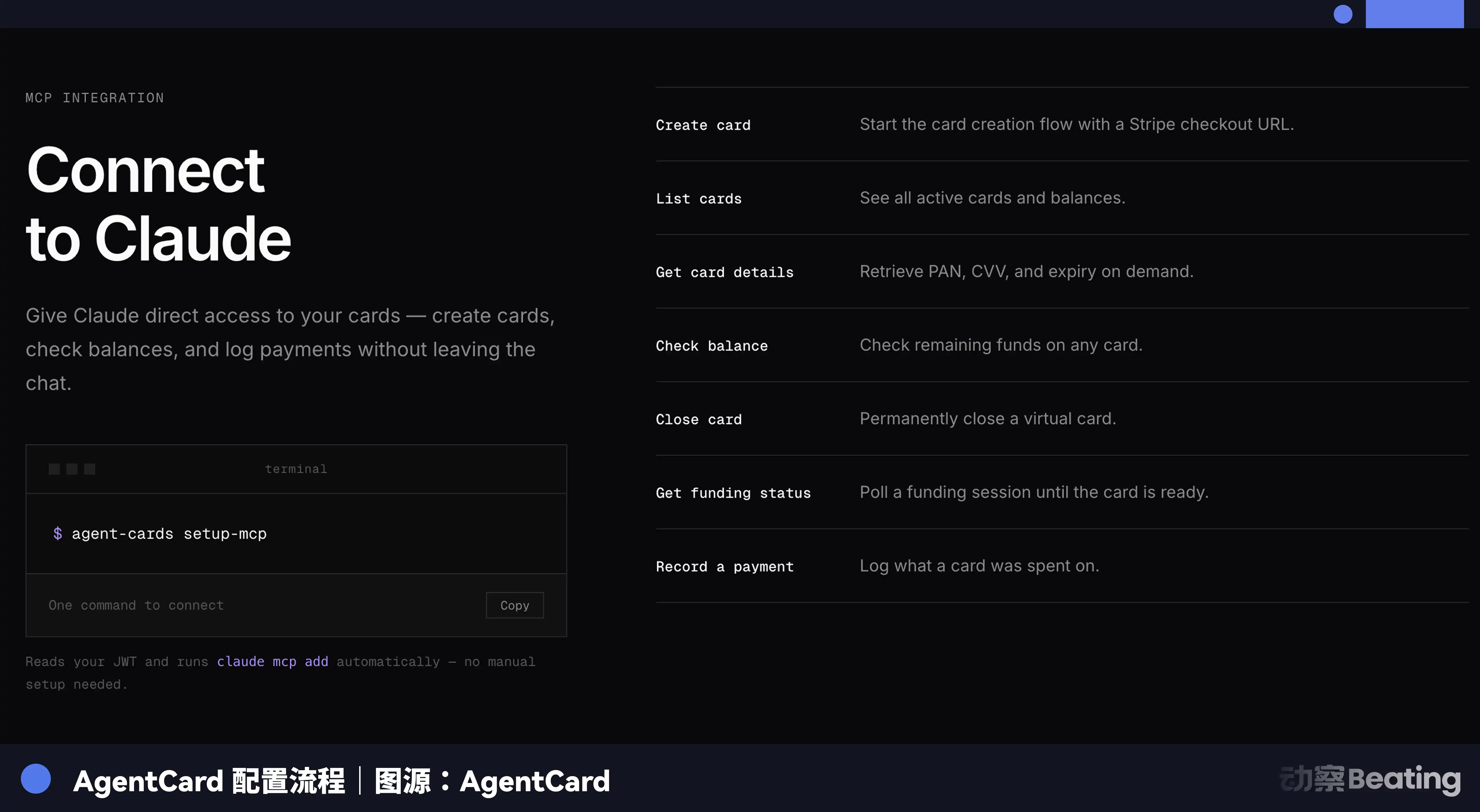

Take the virtual card project AgentCard, which garnered attention yesterday, as an example. It operates through a model context protocol (MCP) server, and the process is as follows: you first top up with the virtual card provider, the Agent calls the MCP tool, such as "create_card(amount=$50)," and the provider's API immediately issues a one-time prepaid Visa card, locking the amount at $50.

The backend has several layers, with the MCP server handling authentication and API calls with fintech companies, and the Agent cannot see your actual source of funds. The card is issued by the issuing bank on the Visa network, and funds are deducted from your pre-linked bank account or credit card. The Agent obtains a temporary card number, used for online checkout or API payments, which is automatically deactivated after use.

Setting it up takes about 5 minutes and can be done through CLI or configuration files. The entire process is highly isolated, and your real card information is never exposed to the Agent.

What problem does the virtual card aim to solve?

The "agent-based commerce" that people talk about is often just one extra step in the human shopping process.

You use ChatGPT to research a pair of headphones, then place the order yourself; that's the first layer. Or you have ChatGPT find the headphones and click purchase, and you confirm the payment; that's the second layer. Or you set a condition for the Agent to automatically buy when the price drops below a certain number; that's the third layer.

In these three scenarios, the Agent uses your payment credentials, and major card organizations and AI labs are already building underlying protocols for these scenarios.

The truly interesting scenarios begin at the fourth layer.

Your Agent needs to call another large model's API, such as switching from Anthropic to a cheaper inference model, purchasing an expensive dataset to complete a research task, or hiring another Agent to handle a subtask.

In these scenarios, the Agent is not charging on your card; it needs its own payment credentials.

The current approach is for developers to buy these things on behalf of the Agent and then grant it access. This is not called agency; it's called proxy purchasing.

To fully liberate humans (but without completely relinquishing trust), a limited Agent payment method is needed, and the programmable features of virtual cards align perfectly with this demand.

Why is this issue only emerging now? Because three conditions have matured simultaneously.

The first condition is the demand side. The thriving lobster installation activities in major cities around the world provide a glimpse.

The second condition is the supply side. Stripe Issuing can now create and manage virtual cards through APIs, with the necessary technology and protocols in place.

The third condition is that card organizations are getting involved. Visa and Mastercard have simultaneously released Agent payment protocols; Cloudflare is participating in establishing technical standards, and Fiserv has become one of the first major payment processors to support these protocols. The platformization has been completed.

From grassroots entrepreneurs to card organization giants, everyone sees the same thing at the same time: Agents need their own financial infrastructure.

Structural limitations of virtual cards

The virtual card solves today's issues, but it inherits an old problem of bankcard networks: slow settlement.

Most people outside the payment industry are unaware that when you swipe a card in a store, the merchant does not receive the money immediately. It can take a day or several days, and cross-border payments may take 30 days to receive funds. Visa does not move funds; banks do, and bank settlements are slow and expensive.

For the Agent, this issue is magnified. If your Agent is buying a lot of tokens from Anthropic and the business suddenly takes off, you might run out of funds before the income arrives.

The virtual card has a second limitation: cross-border costs. Traditional bank cards involve currency conversion, intermediary fees, and compliance checks for cross-border payments. For Agents needing to call APIs and services globally, these friction costs accumulate quickly.

The third limitation is insufficient programmability. As your Agent's transaction scale increases and the number of sub-Agents requiring management grows, the flexibility of virtual cards becomes inadequate. If using virtual cards, the main Agent must apply for each sub-Agent individually or create a new card every time, costing a few dollars.

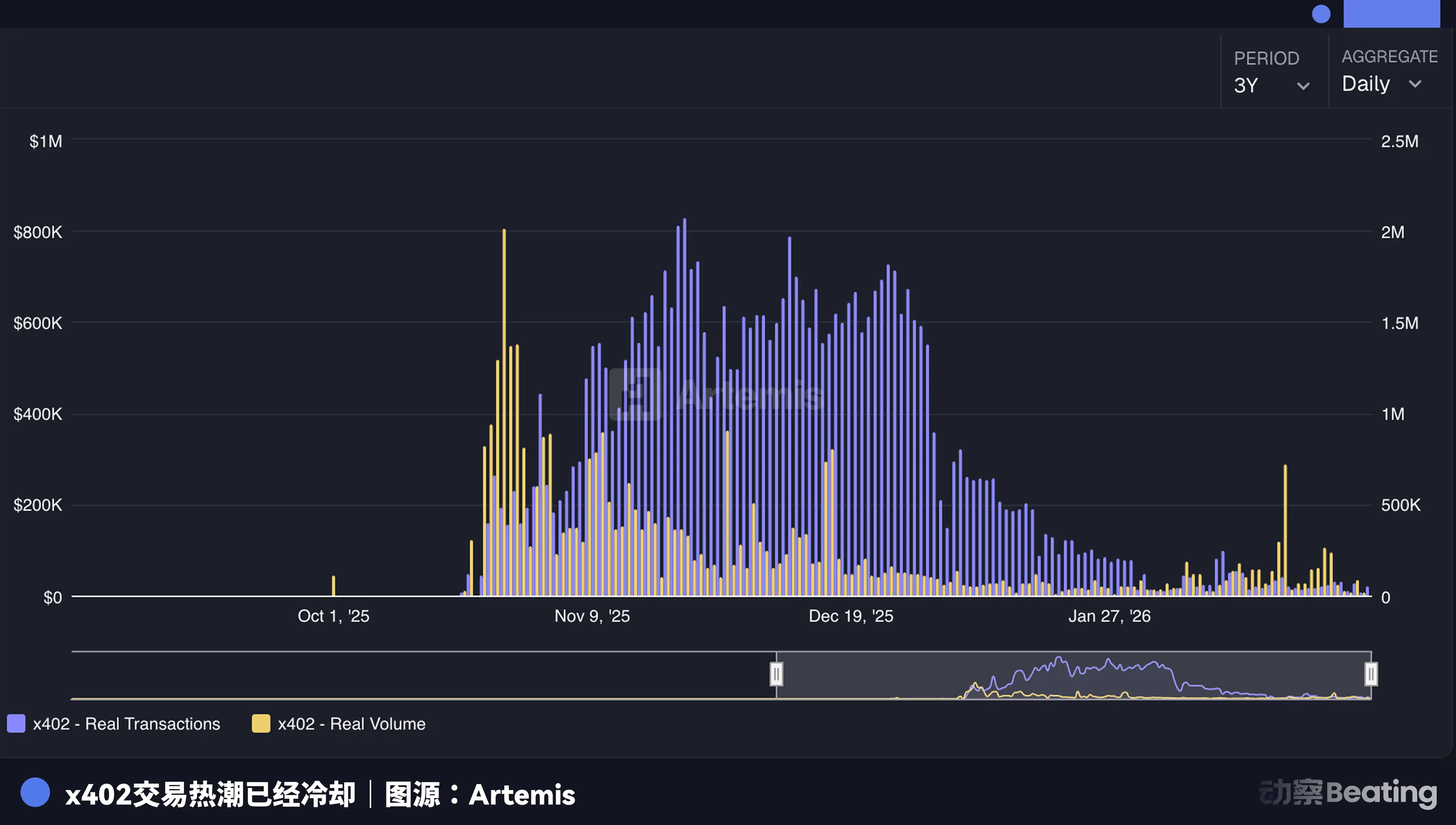

Understanding these limitations reveals why the x402 protocol drew interest a few months ago.

The essence of x402 is to bypass the bankcard network and complete on-chain payments directly at the HTTP layer using stablecoins. For instance, suppose your Agent needs to call a paid API for real-time data. With a virtual card, you must first create a card, register an account on the service provider's website, link the card, subscribe to a monthly plan, obtain the API key, and then configure it for the Agent.

With x402, the Agent sends an HTTP request directly, the server returns a 402 status code and price, the Agent automatically signs a USDC transfer, the server confirms receipt, and the data is returned. No registration is needed, no subscription, pay as you go.

The two are not mutually exclusive. Virtual cards are suitable for Agents making purchases at Visa merchants, online shopping, subscribing to SaaS, or paying cloud service bills. x402 is suitable for direct payments between Agents, calling APIs, purchasing data, or hiring other Agents to complete subtasks.

Currently, most merchants still only accept Visa/Mastercard, so virtual cards are the usable solution today. However, for scenarios like Agent calling APIs or collaborating between Agents, native payment protocols like x402 are more appropriate.

There is also an intermediate solution that accelerates bankcard backend settlements using stablecoins. The front end remains card swiping, while the backend becomes instant on-chain payments. Some say stablecoins will disrupt the bankcard network, which misinterprets the direction. Stablecoins cannot achieve uncollateralized credit, chargeback rights, or Visa-level anti-fraud capabilities; they are to accelerate bankcards, not replace them.

The three-layer solutions build on each other: virtual cards address compatibility, stablecoins solve settlement speed, and native wallets address programmability. Which layer you are on today depends on the type of trading counterpart your Agent needs to deal with.

Three Parallel Entrepreneurial Tracks

The entrepreneurial ventures aimed at Agent payments will ultimately lead to a place that surprises many: machine organization.

Consider how today’s companies manage employee spending: corporate cards, reimbursement rules, budget centers, approval processes, and audit trails. This system is the foundational infrastructure of corporate governance. Now, companies need to provide the same for AI agents.

This means at least three entrepreneurial tracks are simultaneously opening up.

The first is a card issuing platform focused on Agents. Currently, several platforms have entered the market, but most are still limited to the superficial level of virtual card issuance.

The real moat lies in the risk control model, billing logic, and developer experience. For example, onboarding processes do not require filling out forms, registering with APIs, risk control models based on Agent behavior patterns rather than human credit history, and billing logic based on token consumption rather than monthly bills.

The second track is KYA infrastructure. KYA stands for Know Your Agent, corresponding to traditional finance's KYC. When Agents become merchants and buyers, understanding your customer turns into knowing your Agent. Who developed it? What model does it run on? What is the historical transaction record and behavioral pattern? This represents a new layer of trust.

A startup called Skyfire is already working on this. It launched the KYAPay protocol, which allows merchants to verify the identity and authorization status of Agents. In December 2025, Skyfire collaborated with Visa to complete an end-to-end Agent shopping demonstration: the Agent independently researched products, compared prices, and completed purchases, with identity verified throughout by the KYA protocol and payments processed by Visa's Trusted Agent Protocol.

However, entering 2026, Skyfire's official updates have ceased, with no latest products or protocol progress. It can be said that the entire industry still lacks a unified standard, representing a hill to seize.

The third track is a clearing and auditing network for transactions between Agents.

When the main Agent manages dozens of sub-Agents, each with wallets and transaction records, who will reconcile? Who will audit? This presents an opportunity for a "Big Four" accounting firm within the Agent economy.

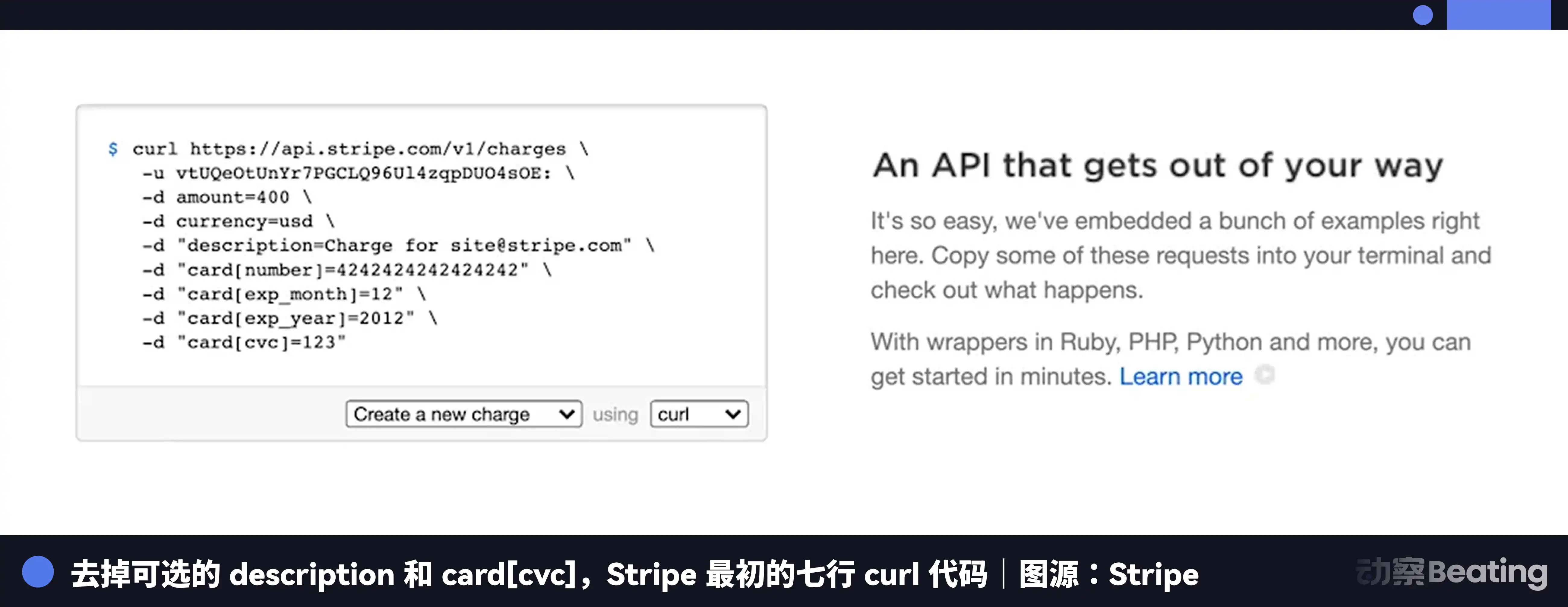

History rhymes. Around 2000, eBay created a marketplace that allowed ordinary people to buy and sell to each other. Those individual sellers could not obtain merchant accounts, and PayPal enabled them to receive payments. By the end of that year, PayPal processed 40% of payments for eBay auctions. Around 2010, independent developers wanted to receive payments online; both PayPal and Cybersource could do it, but the process was lengthy and painful. Stripe solved it with seven lines of code.

The pattern is always the same: every time there is a shift in platform paradigms, a new batch of merchants emerge that current payment systems cannot serve. The winners serve merchants that traditional giants find not worthwhile to conduct risk assessments.

Who are today’s new merchants?

In 2025, GitHub added approximately 36 million developers. In Y Combinator's Winter 2025 cohort, a quarter of the companies had codebases with over 95% generated by AI. On Bolt.new, 67% of the 5 million users are not professional developers.

Millions of ordinary people who could not write production-level code two years ago are now releasing software.

Returning to the initial tweet: giving AI a Visa card to let it spend money on its own may seem like a product feature, but it is actually the starting point of a paradigm shift.

From grassroots entrepreneurs to card organization giants, everyone has realized that Agents need their own financial infrastructure. But virtual cards, stablecoins, and wallets are merely scaffolding.

The real change lies deeper. When natural language becomes the native interface for transactions, payments are no longer a separate industry; they become a fundamental capability embedded in every conversation.

Years ago, eBay's individual sellers were unconcerned with the technical differences between ACH and credit card networks. They just needed something to receive payments with a simple registration, and PayPal provided that. Today, tens of millions of Vibe Coders and their Agents do not care about the underlying disputes between bankcards and stablecoins. They just need to say a word, and the money is there.

Whoever is the first to make it happen will be the next PayPal.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。