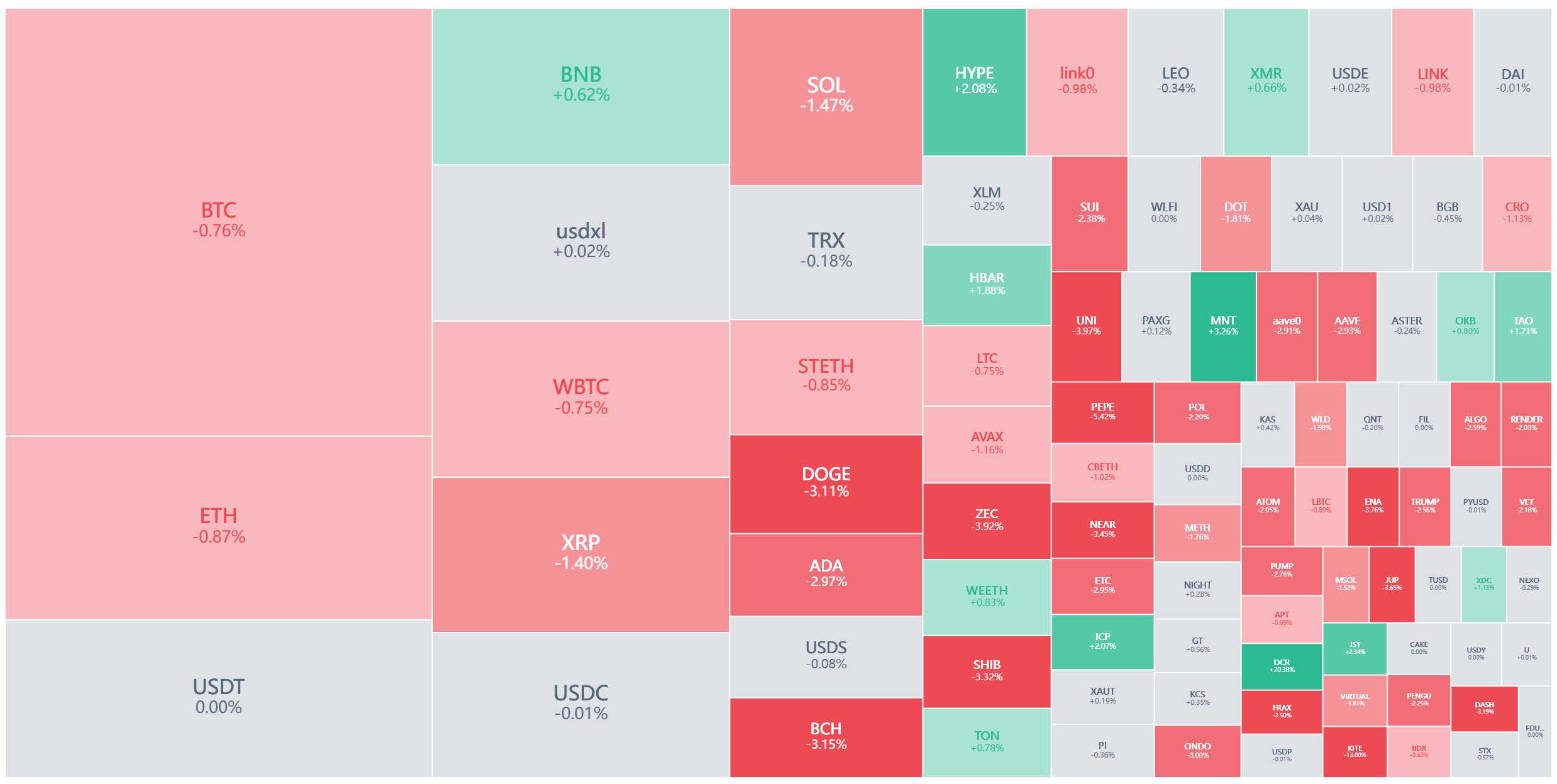

Despite Bitcoin's price rising back above the $70,000 mark this week, the cold signals from the derivatives market have doused the bulls' euphoria with a bucket of cold water. After experiencing a roughly 32% drop over the previous seven weeks, is this rebound the starting point of a trend reversal, or yet another trap to lure in buyers?

An in-depth analysis of the latest futures premium, options skew, and macro fund flows suggests that the market leans towards the latter—under the shadow of cautious sentiment, Bitcoin still faces a thorny path to stabilize above $70,000 and challenge higher levels.

1. The “cold” of the Derivatives Market vs. the “hot” of the Spot Market

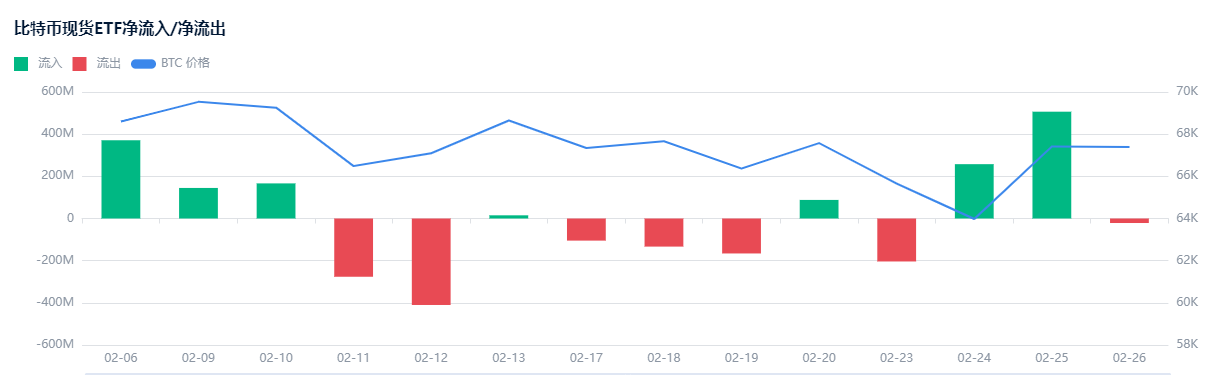

● Bitcoin strongly rebounded from a low of $62,000 on Tuesday and briefly tested the $70,000 mark again. The direct driving force behind this surge came from traditional financial markets: the Bitcoin spot ETF listed in the United States recorded a net inflow of $764 million over the past two days, partially offsetting the $1.2 billion outflow over the previous eight trading days.

○ This "buy-the-dip" behavior by institutions seems to have built a strong defense below $65,000.

● However, beneath the surface, there are undercurrents stirring. In stark contrast to the positive buying in the spot market, the attitude of leveraged funds appears alarmingly cautious. Data shows that the annualized premium rate of Bitcoin futures contracts relative to the spot market is currently only around 2%, well below the neutral threshold of 5%.

○ This metric is typically seen as a thermometer for measuring the sentiment of leveraged bulls; its long-term stay on the floor indicates that professional traders are not only unwilling to add bullish positions but are even reducing leverage amid the rebound.

● The options market conveys an even clearer signal of hedging. The "skewness indicator" measuring the relative cost of put versus call options shows that the price of protective put options is still about 14% higher than call options. In a neutral market sentiment environment, this value typically fluctuates between -6% and +6%.

● Although the level of extreme fear at 28% in the past few days has eased somewhat, options traders are clearly still paying high premiums for potential declines, which is not a characteristic of a bull market.

2. $10.5 Billion “Massive” Options Expiration: Shorts Have Long Set Their Traps

● If the derivatives indicators are merely an indirect reflection of market sentiment, then the monthly options settlement arriving on February 27 is the most realistic test facing the bulls. According to data from major exchanges like Deribit, there will be a massive $10.5 billion in nominal Bitcoin options contracts expiring this time.

● On the surface, the open interest in call options exceeds that of put options, but this is a genuine "bull trap." The intense volatility of Bitcoin prices in early February and the drop below $75,000 caused many previously purchased call options to become deep out-of-the-money contracts.

● Data shows that if the price cannot stabilize above $70,000 by the Friday settlement, nearly 88% of the call options on Deribit will expire worthless. This means that the funds that initially bought these options would lose everything, while the institutions that sold the options (often market makers) would likely reap the benefits.

● From a speculative perspective, the shorts hold an absolute technical advantage in this billion-dollar showdown. The current price range is concentrated between $65,000 and $69,000, which just happens to be the settlement area where the shorts profit the most. Unless the bulls can execute a miraculous 9% surge at the last moment to push the price past the $75,000 "maximum pain point," this options settlement is likely to end with a harvest for the shorts.

3. Macroeconomic Chill: Risk Appetite Unwilling to be Lifted by Nvidia

● Shifting focus away from the crypto market, a larger macro shadow looms over all risk assets. Bitcoin has historically maintained a positive correlation of up to 90% with the Nasdaq 100 index, where the performance of tech stocks serves as a barometer for crypto market sentiment.

● However, a dangerous signal has recently emerged: even after Nvidia, hailed as a leader in AI, released strong earnings reports, its stock price fell 5% on Thursday. This abnormal phenomenon profoundly reflects the current market's extreme risk aversion sentiment—good news is already priced in, and capital is fleeing, with investors no longer willing to pay for any positive news. This is certainly not a good sign for Bitcoin.

● On a macroeconomic level, the Federal Reserve's interest rate policy remains a sword of Damocles. The Economic Daily recently pointed out that Bitcoin's recent plunge is closely related to the weakening of the tech sector in U.S. stocks and the decline in risk appetite in the international financial market.

● Under expectations of liquidity tightening, highly volatile crypto assets often become the first targets to be sold off by institutions. Even if ETFs see inflows, they are more interpreted as tests of left-side trading rather than trend-positive signals.

4. Market Rumors Abound: Quantum Computing and Institutional “Conspiracies”

● In addition to caution on the data front, various unverified market narratives are also disturbing public sentiment. Recently, discussions about the “threat of quantum computing to Bitcoin's security” have resurfaced. Jefferies strategist Christopher Wood has even removed Bitcoin from his portfolio because of this.

● Although developers have proposed upgrades such as BIP-360 for post-quantum cryptography, this long-standing technical concern will undoubtedly shake the confidence of some long-term holders.

● Another rumor points to the quantitative trading giant Jane Street. Market speculation suggests it has suppressed Bitcoin prices through specific strategies. Although the research director at CryptoQuant pointed out that the related trading behavior resembles the delta-neutral strategies commonly employed by hedge funds, rather than active short selling, these rumors reflect a market sentiment in panic mode—when prices fail to rise, any slight movement can serve as a reason for explanation.

5. Confidence is More Important than Gold

● In summary, the current Bitcoin market presents a typical “K-shaped divergence”: Spot ETF funds are flowing in, while derivative leverage is retreating; retail investors are looking for rebounds, while professional traders are buying insurance.

● The "death cross" on the technical front resonates with the cautious signals in the derivatives market. For Bitcoin, while a return to $70,000 is certainly commendable, sustaining the upward momentum to challenge $75,000 requires not only support from the spot market but also a comprehensive return of macro risk appetite and the re-entry of leveraged funds.

● Tonight's options settlement will be a litmus test. If the bulls can withstand the $10 billion expiration pressure and hold $70,000, then the market bottom will be further solidified; conversely, if they crumble amidst the settlement tide, this rebound may merely be a fleeting glimpse amid an ongoing decline. For ordinary investors, it may be optimal to watch more and act less before the alarm in the derivatives market is lifted.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。