Written by: Glendon, Techub News

When the cryptocurrency market is stuck in a stalemate, some institutions continue to expand their positions. Last night, Michael Saylor, founder of Strategy, tweeted that Strategy had once again increased its holdings by approximately $1.25 billion, acquiring 13,627 bitcoins last week, marking the largest investment scale since August of last year. As of January 11, Strategy holds approximately 687,400 bitcoins, with a total investment of about $51.8 billion.

Meanwhile, as the world's largest "new funds" buyer of Ethereum, BitMine also disclosed yesterday that it spent approximately $75.37 million last week to purchase 24,266 ethers, bringing its total holdings to about 4.1678 million ethers, with a total value of approximately $12.9 billion, accounting for 3.45% of the total ETH token supply.

However, despite both being leaders in the Bitcoin and Ethereum DAT markets, the two have experienced markedly different situations during their accumulation processes. According to on-chain analyst Yu Jin, as of January 12, the average cost of Strategy's (MSTR) Bitcoin holdings is $75,353. Thanks to its first-mover advantage, despite market impacts, its unrealized gains still amount to approximately $10.55 billion; in contrast, BitMine's (BMNR) average cost for Ethereum holdings is $3,862, resulting in an unrealized loss of $3.225 billion. This raises a series of questions. Why does BitMine have such a large unrealized loss, yet its pace of accumulating Ethereum has not slowed? During this period, BitMine has also continued to stake a large amount of Ethereum; what considerations lie behind this?

The Leap from DAT Company to Infrastructure Provider

BitMine's high-frequency accumulation and seemingly aggressive staking behavior are the result of multiple factors. First is the performance of BitMine's stock price relative to its net asset value ratio (mNAV). After the cryptocurrency market experienced the "10.11" flash crash and several months of sluggish performance, BitMine was also severely affected, with BMNR's overall stock price trend resembling that of Strategy (MSTR), both suffering significant declines. As of the time of writing, BMNR has fallen from a high of $65.6 in October last year to $31.13, a drop of about 53%; MSTR's current stock price is $162.23, down more than 55% from its October high of about $365.

However, there are notable differences between the two. After hitting a low of $24.33 at the end of November, BMNR has shown a trend of fluctuating upward since December, briefly returning to $40, with a current market value of $132.61 million; in contrast, MSTR's stock price has continued to decline, reaching a low of $149.75 on January 2, with its current market value falling below $50 billion, approximately $46.617 billion.

The key differences in the aforementioned stock price data directly lead to different net asset value ratios (mNAV) for both. As an important observation indicator, Strategy's mNAV (the ratio of market capitalization to the value of held BTC) has now significantly dropped below 1, to about 0.75, indicating that Strategy's financing ability may be somewhat limited; in contrast, BitMine's mNAV is currently at 1.02, although it is far from the peak of 5.7 times in July last year, it still maintains above 1, indicating that its stock price still has some value support.

Secondly, from the perspective of investment cost and strategic considerations, BitMine's average purchase price for Ethereum is $3,862, while the current Ethereum price is about $3,125. Its unrealized loss mainly stems from the market's cyclical pullback, rather than a deterioration of the asset itself. In BitMine's view, the $3.225 billion unrealized loss is essentially not a failure of investment, but a strategic cost. Previously, BitMine's board chairman Tom Lee proposed the company's long-term goal—"5% ETH alchemy," which aims to acquire 5% of the total supply of Ethereum. In yesterday's announcement, BitMine emphasized that the company has completed nearly 70% of this goal in just 6 months, which fully demonstrates that BitMine and its board still highly recognize Ethereum's long-term value.

During the process of accumulating Ethereum, BitMine's important means of increasing stock price and mNAV is through "staking ETH." On December 27, BitMine began attempting to stake its held Ethereum to earn interest, with an initial staking amount of approximately 74,900 ETH, which sparked considerable discussion in the industry. Since then, BitMine has been staking a large amount of its Ethereum reserves daily. After staking approximately 154,200 ETH today, in just 18 days, BitMine has cumulatively staked over 1.3442 million ETH, with a total value of up to $4.2 billion, becoming the world's largest Ethereum staking entity.

At the same time, BitMine is collaborating with three staking service providers to develop a custom infrastructure designed specifically for native Ethereum staking, called the "MAVAN" (American Native Ethereum Validator Network), which is planned to be fully launched in the first quarter of 2026. Its purpose is clear: to eliminate dependence on third-party staking service providers like Lido and Coinbase by deploying facilities that meet institutional and regulatory custody security requirements in the U.S., thereby creating "independent infrastructure" to enhance security, compliance, and yield certainty. This means that BitMine's ultimate goal may not be limited to becoming the largest ETH holder, but rather to become one of the underlying operating systems of the Ethereum staking ecosystem.

Tom Lee has stated, "When all of BitMine's ETH is staked by MAVAN and its staking partners (at a certain scale), the ETH staking fees will reach $374 million annually (calculated at a CESR of 2.81%), or over $1 million daily."

Based on the current APY of approximately 2.86%, if BitMine stakes all of its Ethereum holdings, it could earn about 120,000 ETH in interest over a year, valued at nearly $375 million.

Through this approach, the market has begun to reassess the support of "staking yields" for BitMine's valuation. An important manifestation of this is that BitMine's mNAV has rebounded to 1.02, having previously dropped to 0.85. Moreover, through staking activities, BitMine has formed a revenue closed loop, using staking income to cover unrealized losses, creating positive cash flow to support stock price recovery. Notably, at this stage, BitMine's stock price has begun to show a positive correlation with the staking yield curve.

Additionally, these initiatives by BitMine have also driven a shift in Wall Street institutions' perceptions, as their attention is shifting from a "pure ETH leverage tool" model to a "staking yield flow asset" model. For example, SharpLink, another leading Ethereum treasury company, announced on January 8 that it has deployed $170 million worth of Ethereum on Linea, adopting an enhanced yield strategy.

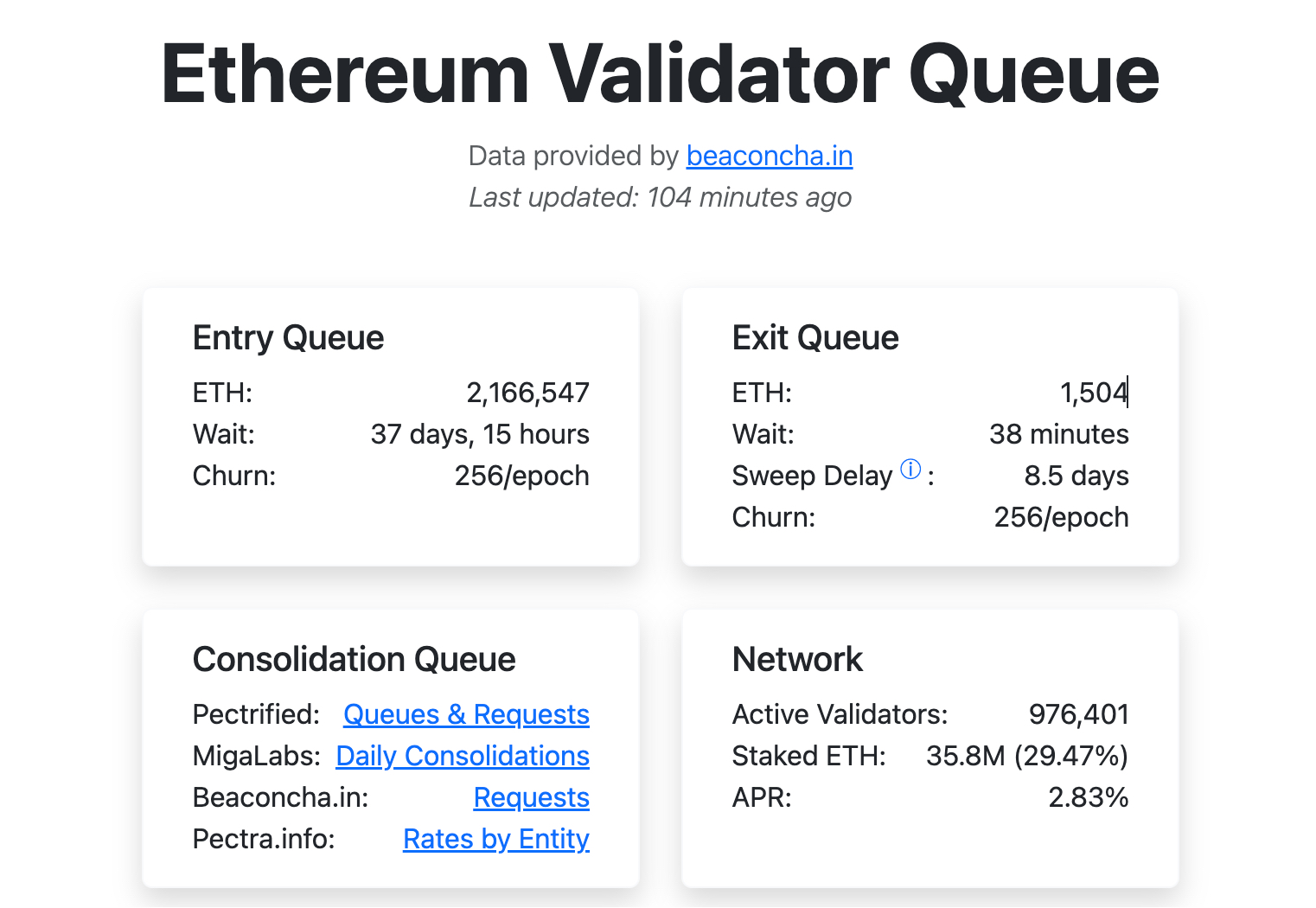

More intuitively, the significant rebound in Ethereum staking demand is reflected in the latest data from the Ethereum Validator Queue, which shows that approximately 2.1665 million ETH are currently queued to enter the Ethereum validator network, with an expected waiting time of 37 days and 15 hours, while only about 1,504 ETH are exiting the queue (previously, the exit queue was completely cleared). At the same time, the total amount of staked Ethereum has also reached 35.8 million ETH, accounting for 29.47% of the total supply, with the number of active validators approaching 980,000.

In stark contrast, last September, the network's "exit queue" exceeded 2.67 million ETH, reaching a historical high. The reversal of this indicator indicates a return of market confidence in the Ethereum ecosystem and suggests that Ethereum is entering a phase of capital accumulation.

It is worth noting that BitMine is currently at a critical period for executing its Ethereum strategy. At the beginning of January, Tom Lee stated in his New Year address that the BitMine board has proposed a significant increase in the number of authorized shares, suggesting raising the number of company shares from 500 million to 50 billion, and urging shareholders to vote on the proposal by January 14.

Tom Lee emphasized that this increase in shares is not intended to dilute shares but has multiple considerations: first, to facilitate fundraising through public market issuance, convertible securities, and secured financing; second, to enable equity payment capabilities for potential mergers or strategic transactions; and most importantly, to create conditions for a stock split if necessary in the future, lowering the investment threshold to attract retail participation.

However, BitMine's bylaws contain a special provision that requires 50.1% of circulating shares to support the issuance of new shares, which is a very high threshold, making it very difficult to obtain authorization for new shares. Currently, BitMine's 500 million authorized shares are about to be exhausted, and if the proposal is not approved, the company will be unable to issue new shares, limiting its financing channels and halting its ETH accumulation.

Nevertheless, from the current situation, BitMine has not yet achieved its goal of "5% ETH alchemy," and the company's development prospects are relatively clear. Additionally, Tom Lee explained, "BitMine aims to create shareholder value by increasing the value of ETH per share. The company will only issue shares at prices above mNAV, optimizing the yield from ETH holdings, and strategically investing its balance sheet in 'moonshot projects.'" Therefore, considering all factors, the likelihood of this proposal passing is quite high.

Conclusion

From BitMine's initiatives, it is essentially applying institutional-level financial engineering to transform cryptocurrency assets from volatile speculative products into predictable, auditable, and financeable infrastructure assets. As an important participant in the Ethereum ecosystem, BitMine's continuous accumulation of Ethereum and large-scale staking behavior conveys a strong institutional confidence in Ethereum's long-term value, indicating that despite short-term price fluctuations, institutions are more focused on long-term returns and network stability.

On the other hand, although the cryptocurrency market has not yet fully recovered, multiple data points suggest that the sell-off may be nearing its end, and market liquidity is relatively good. JPMorgan analyst Nikolaos Panigirtzoglou pointed out that the outflow of funds from Bitcoin and Ethereum ETFs has begun to stabilize this month, and futures market positioning indicators also show that investor de-leveraging behavior for the end of 2025 has basically been completed.

Tom Lee also noted in the announcement that 2026 heralds many positives for cryptocurrencies, as the proliferation of stablecoins and tokenization will drive blockchain to become the settlement layer for Wall Street, particularly benefiting Ethereum's development. "We still believe that the leverage reset after October 10 last year is akin to a 'mini crypto winter,' and 2026 will be the year of recovery for the crypto market, with the market expected to see stronger gains in 2027-2028."

Thus, it can be seen that BitMine's seemingly "crazy" accumulation and staking behavior is not the obsession of a "gambler," but rather a calm layout by a company intending to become a foundational infrastructure of the Ethereum staking ecosystem. The over $3.225 billion unrealized loss is the price of the market cycle, staking yields are the "anchor" of cash flow, and the upcoming MAVAN will become the cornerstone of BitMine's long-term value "moat." While the market is still debating "when Ethereum can rise to $5,000," BitMine is already calculating "how many years can $1 million in daily earnings support."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。