The US Treasury market is a glass house.

The buyer base for Treasuries has become more fragile. Foreign demand is weakening as reliance on leveraged flows has increased.

Stress in Japanese funding markets has emerged as the Bank of Japan shifts away from years of loose monetary policy. Higher domestic yields make foreign Treasuries less attractive for Japanese life insurers and pension funds, which have been major allocators to US assets for decades. Rising FX hedging costs and bond volatility compound this problem.

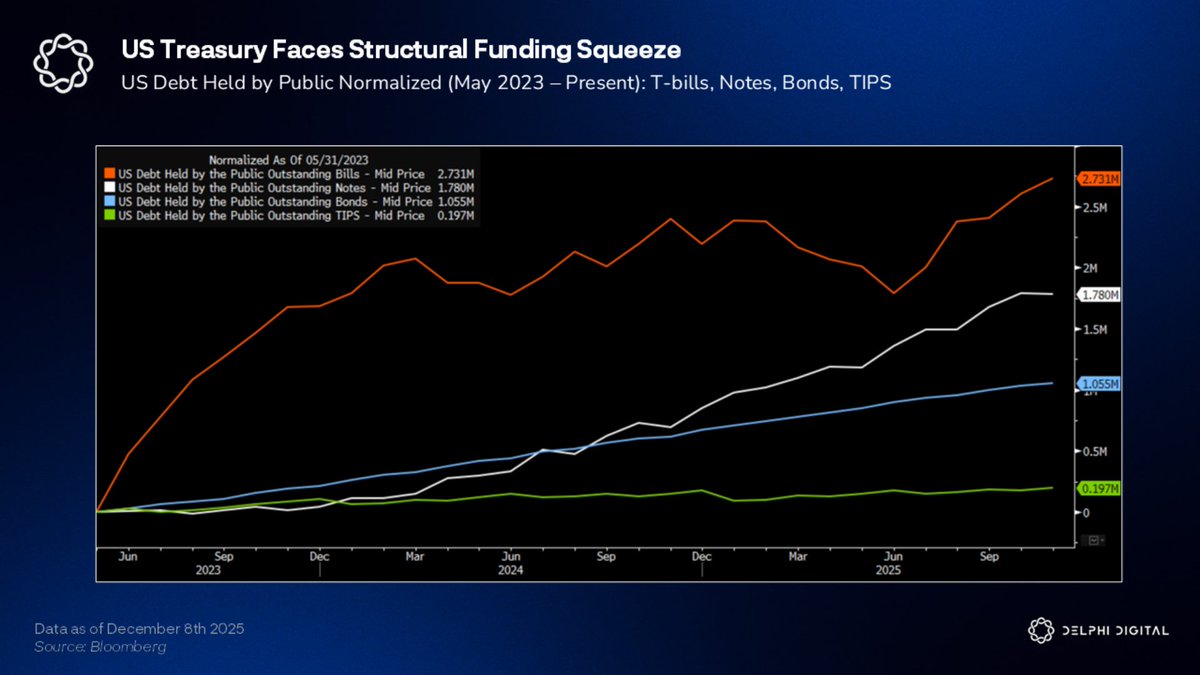

Meanwhile, the Treasury has become increasingly dependent on hedge funds running basis trades to absorb issuance. This ~$2 trillion trade now underpins the long end of the curve. Around $150B in T-bills and $300B in coupon debt matures every month. The US has nearly $10T to refinance over the next 12 months.

To keep the plumbing functional, the Fed's Standing Repo Facility is now viewed as the ultimate safety valve. Officials are actively encouraging banks to arbitrage the funding spread by borrowing from the Fed at lower rates and lending in private repo. Many say this isn't QE, but it functions as an open liquidity valve.

Whether through the SRF becoming permanent or regulatory changes freeing up bank balance sheets, the US Treasury will monetize its debts through the banking system.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。