The week following the interest rate cut has not started well.

Bitcoin has fallen back to around $85,600, and Ethereum has lost the $3,000 mark; cryptocurrency-related stocks are also under pressure, with Strategy and Circle both down nearly 7% during the day, Coinbase dropping over 5%, and mining companies CLSK, HUT, and WULF seeing declines of more than 10%.

From the Bank of Japan's interest rate hike expectations to the uncertainty surrounding the Federal Reserve's subsequent rate cut path, and the systemic de-risking by long-term holders, miners, and market makers, the reasons for this round of decline lean more towards macroeconomic factors.

The Yen Rate Hike: The Underestimated First "Domino"

The Bank of Japan's interest rate hike is the biggest factor in this decline, which may be the last major event in the financial industry this year.

Historical data shows that when Japan raises interest rates, Bitcoin holders do not fare well.

In the past three instances of the Bank of Japan raising rates, Bitcoin fell by 20%–30% within 4–6 weeks. As analyst Quinten has detailed: Bitcoin dropped about 27% after the yen rate hike in March 2024, fell 30% after the July hike, and again dropped 30% after the January 2025 hike.

This time marks the first interest rate hike by Japan since January 2025, with rates potentially reaching a 30-year high. Current predictions in the market show a 97% probability of a 25 basis point hike, which is almost a certainty; the meeting on that day may just be a formality, as the market has already reacted with a decline.

Analyst Hanzo stated that the cryptocurrency market's neglect of the Bank of Japan's movements is a significant oversight. He pointed out that Japan, as the largest overseas holder of U.S. Treasury bonds (holding over $1.1 trillion), could influence global dollar supply, Treasury yields, and risk assets like Bitcoin.

Several Twitter users focusing on macro analysis have also noted that the yen is the largest player in the foreign exchange market after the dollar, and its impact on capital markets may be greater than that of the euro. The nearly thirty-year bull market in U.S. stocks has a lot to do with yen arbitrage. For years, investors have borrowed yen at low interest rates to invest in U.S. stocks, U.S. Treasuries, or purchase high-yield assets like cryptocurrencies. When Japanese interest rates rise, these positions may be quickly liquidated, leading to forced liquidations and deleveraging across all markets.

Moreover, the current market backdrop is that while most major central banks are cutting rates, the Bank of Japan is raising them. This contrast will trigger the unwinding of arbitrage trades, meaning that such rate hikes could lead to renewed turmoil in the cryptocurrency market.

More importantly, the rate hike itself may not be the key risk; rather, the critical factor is the signal released by the Bank of Japan regarding its policy guidance for 2026. The Bank of Japan has confirmed that starting in January 2026, it will sell approximately $550 billion worth of ETF holdings. If the Bank of Japan raises rates again or multiple times in 2026, it will lead to more rate hikes and accelerated bond selling, further unwinding yen arbitrage trades, triggering a sell-off in risk assets and yen repatriation, which could have a lasting impact on the stock market and cryptocurrencies.

However, if fortunate, after this rate hike, if the Bank of Japan pauses further hikes in the upcoming meetings, the market's flash crash may end and a rebound could follow.

Uncertainty Surrounding Future Rate Cuts in the U.S.

Of course, any decline is not due to a single factor or variable. The timing of the Bank of Japan's rate hike and Bitcoin's crash coincides with several other factors: leverage reaching peak levels; tightening dollar liquidity; extreme positions; and the impact of global liquidity and leverage, among others.

Let’s turn our attention back to the U.S.

In the first week following the rate cut, Bitcoin began to weaken. The market's focus has shifted to "how many more cuts can we expect in 2026, and will the pace be forced to slow down?" The two key data points to be released this week—the U.S. macro non-farm payroll report and CPI data—are core variables in this re-pricing of expectations.

With the U.S. government ending a long shutdown, the Bureau of Labor Statistics (BLS) will release employment data for October and November this week, with the most anticipated being the non-farm payroll report to be published tonight at 21:30. The current market expectation is for an increase of only +55k non-farm jobs, significantly lower than the previous value of +110k.

On the surface, this appears to be a typical "bullish for rate cuts" data structure, but the issue lies in whether the Federal Reserve will be concerned about a rapid cooling of the job market and choose to adjust its policy pace more cautiously. If employment data shows a "cliff-like cooling" or structural deterioration, the Federal Reserve may opt to wait and see rather than accelerate easing.

Next, consider the CPI data. Compared to employment data, the CPI data to be released on December 18 has been repeatedly discussed in the market regarding whether it will give the Federal Reserve a reason to "also speed up balance sheet reduction" to counter the Bank of Japan's tightening.

If inflation data rebounds or becomes stickier, even if the Federal Reserve maintains a rate cut stance, it may still choose to accelerate balance sheet reduction to reclaim liquidity, thus achieving a balance between "nominal easing" and "actual liquidity tightening."

The next truly certain rate cut is not expected until the January 2026 meeting, and that timeframe remains distant. Currently, Polymarket predicts a 78% probability that rates will remain unchanged on January 28, with only a 22% probability for a rate cut, indicating significant uncertainty surrounding rate cut expectations.

Additionally, this week, the Bank of England and the European Central Bank will also hold monetary policy meetings to discuss their respective stances. With Japan having already shifted, the U.S. hesitating, and Europe and the U.K. remaining cautious, global monetary policy is in a highly fragmented stage, making it difficult to form a unified approach.

For Bitcoin, this "non-unified liquidity environment" is often more damaging than clear tightening.

Mining Operations Closing, Old Money Continues to Exit

Another common analytical viewpoint is that long-term holders are still continuously selling, and the pace of selling has accelerated this week.

First, there is the selling by ETF institutions, with Bitcoin spot ETFs seeing a net outflow of about $350 million (approximately 4,000 BTC) in a single day, primarily from Fidelity's FBTC and Grayscale's GBTC/ETHE; Ethereum ETFs have seen a cumulative net outflow of about $65 million (approximately 21,000 ETH).

Interestingly, Bitcoin's performance during U.S. trading hours has been relatively weak. Data from Bespoke Investment indicates: "Since the launch of BlackRock's IBIT Bitcoin ETF, holding after market close has yielded a return of 222%, while holding only during market hours has resulted in a loss of 40.5%."

Following this, more direct selling signals have appeared on-chain.

On December 15, net inflows to Bitcoin exchanges reached 3,764 BTC (approximately $340 million), marking a peak for the period. Of this, Binance alone accounted for a net inflow of 2,285 BTC, an increase of about 8 times compared to the previous period, clearly indicating that large holders are concentrating their deposits in preparation for selling.

Additionally, changes in market maker positions also constitute an important background factor. For example, Wintermute transferred over $1.5 billion in assets to trading platforms from late November to early December. Although from December 10 to 16, its BTC holdings saw a net increase of 271 BTC, the market still reacted with some panic to its large transfers.

On the other hand, the selling behavior of long-term holders and miners has also drawn significant attention.

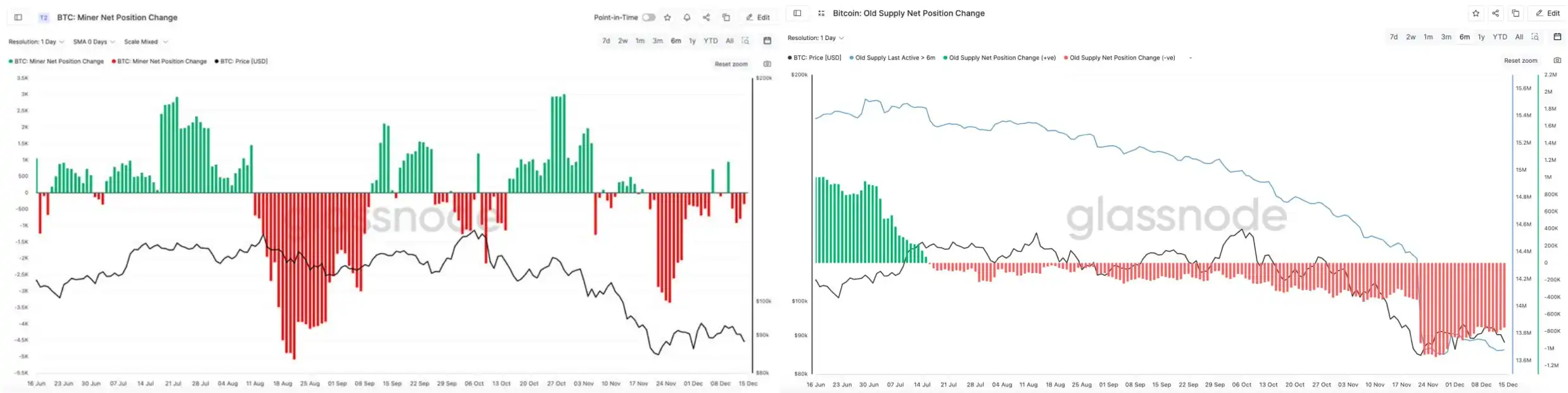

The on-chain monitoring platform CheckOnChain has detected a rotation in Bitcoin's hash rate, a phenomenon that typically occurs during periods of pressure on miners and liquidity tightening. On-chain analyst CryptoCondom noted: "A friend asked me if miners and OGs are really selling their BTC. The objective answer is yes; you can check Glassnode's data on miner net positions and OG long-term BTC holdings."

Glassnode data shows that the selling behavior of OGs who have not moved their holdings for the past six months has been ongoing for several months, with a noticeable acceleration from late November to mid-February.

Adding to this is the decline in Bitcoin's overall network hash rate. As of December 15, according to F2pool data, the Bitcoin network hash rate was reported at 988.49 EH/s, down 17.25% from the same time last week.

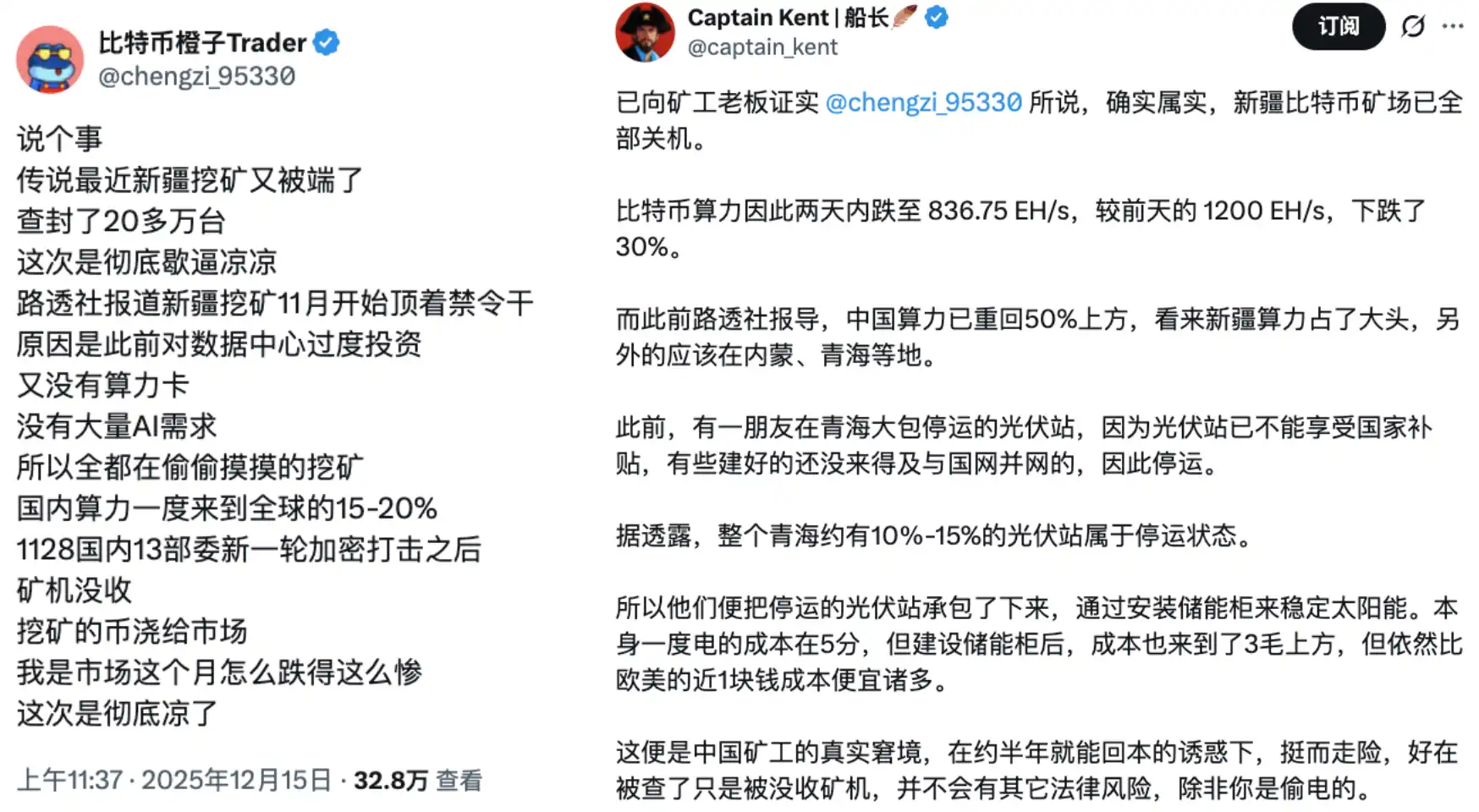

These data points align with the current rumors of "Bitcoin mining operations in Xinjiang shutting down." Nano Labs founder and chairman Kong Jianping also mentioned the recent decline in Bitcoin's hash rate, estimating that at least 400,000 Bitcoin mining machines have shut down, based on an average of 250T (hash rate calculation) per machine.

In summary, the factors contributing to this round of decline include: the Bank of Japan's proactive shift to tightening, which has loosened yen arbitrage trades; the Federal Reserve's inability to provide a clear subsequent path after completing its first rate cut, leading the market to actively lower expectations for liquidity in 2026; and on-chain behaviors of long-term holders, miners, and market makers, which have further amplified the price's sensitivity to changes in liquidity.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。