撰文:Nom

编译:Luffy,Foresight News

TL;DR

- 与以太坊或比特币的 DAT(加密货币财库)相比,SOL DAT 在吸纳当前交易供应量(与流通供应量不同)方面效率更高。

- 近期宣布的 25 亿美元 SOL DAT 计划,相当于以太坊 300 亿美元或比特币 910 亿美元的融资规模。

- 我们终于快要摆脱 FTX 破产清算持有的 SOL 对市场的影响(不过 FTX 在叙事层面的影响仍需消除)。

- SOL 的通胀问题仍会阻碍其价格上涨,亟待解决,SOL 通胀规模约为解锁量的 3 倍。

哦?你真的想读这个吗?首先,简单说几点:

- 我不会争论通胀是好是坏,这事儿我已经聊了够多,就等着后续变化了。

- 我本人持有 SOL 现货、质押 SOL 和锁定 SOL,所以我可能带有偏见。我当然希望自己持有的代币涨价,所以在我看来,代币价格横盘就是坏事。

坏消息:FTX 的破产清算与你的钱

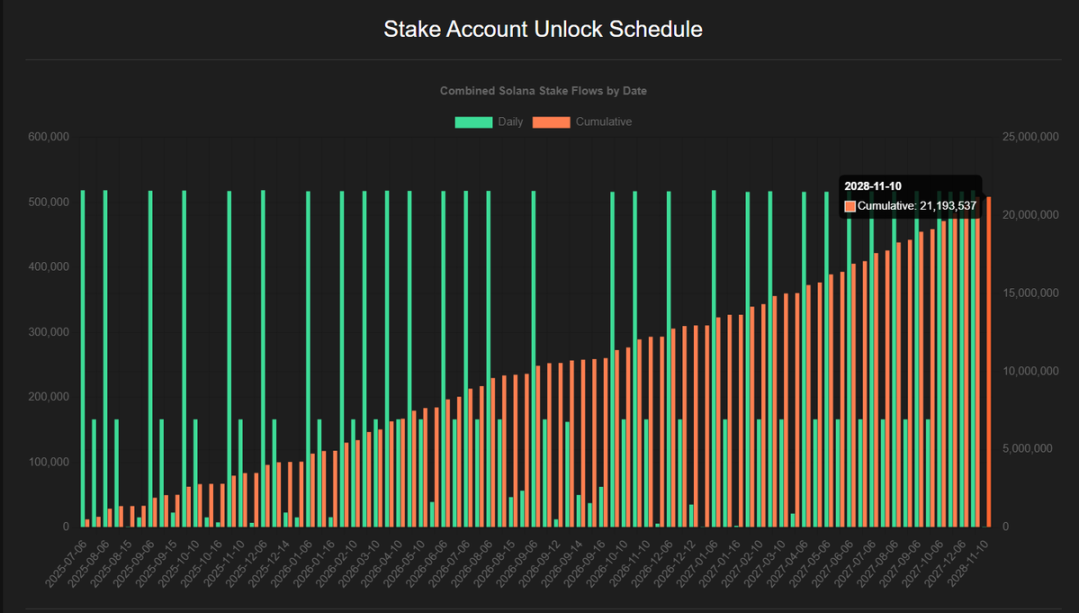

和许多你熟知且喜爱的区块链项目一样,Solana 也曾通过多轮融资向投资者出售代币,其中大量代币流入了 FTX。FTX 破产时,清算资产中持有 4100 万枚 SOL,其中大部分通过几轮交易出售,主要由 Galaxy 和 Pantera 等机构接手,行权价约为 64 美元和 102 美元(还得加上手续费)。以 Solana 当前约 190 美元的价格来看,这些交易现在利润丰厚。通过深入分析质押账户,目前 「清算 SOL」 剩余待解锁量约为 500 万枚,按当前价格计算名义价值约 10 亿美元。

为什么要提这个?

最近,Galaxy 和 Pantera 分别宣布了 12.5 亿美元和 10 亿美元的 SOL DAT 计划,Sol Markets 也加入其中,计划规模 4 亿美元。算上手续费后,这些 DAT 总规模约 25 亿美元。有人担心这不会对 Solana 的价格产生实质影响,因为目前有大量锁定 SOL 可能被这些机构购买。根据 @4shpool 的数据,截至 2028 年,仍有约 2100 万枚 SOL 待解锁,按当前价格计算名义价值约 40 亿美元。粗略估算,「清算 SOL」 约占所有剩余待解锁 SOL 的 1/4。

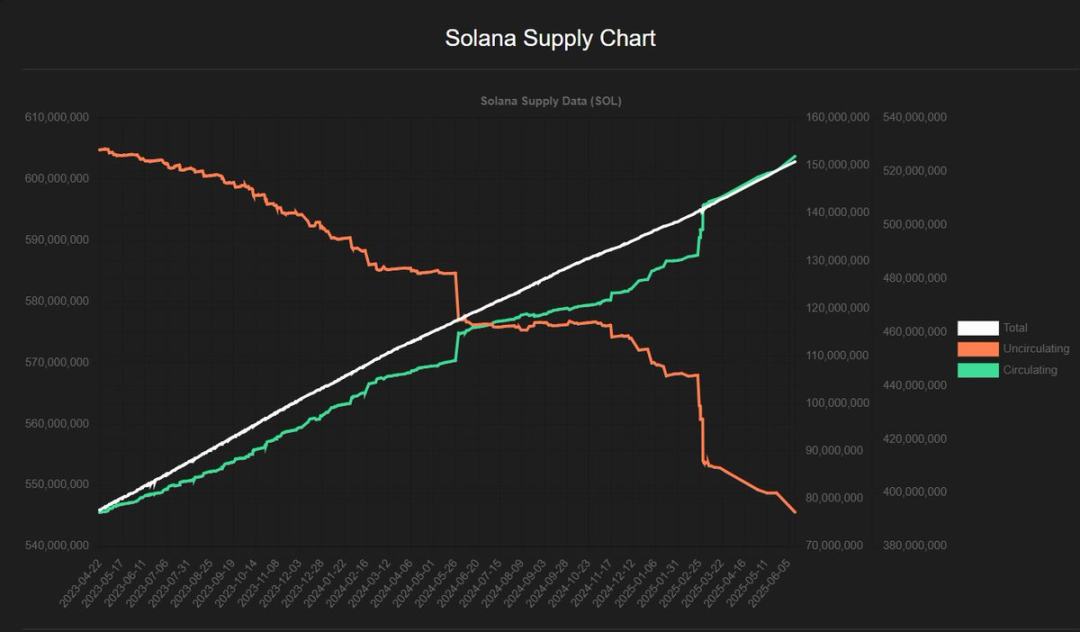

Solana 通胀的另一重问题在于本身的通胀率。通常提到 Solana 的通胀率时,算上解锁量会说是 7%-8%,但实际通胀率约为流通供应量的 4.5%。这意味着,若第 839 个周期的流通供应量约为 6.08 亿枚,一年后通胀带来的新增供应量约为 2750 万枚,加上 1000 万枚的解锁量,流通供应量将增至约 6.455 亿枚,通胀率为 6.2%。再次说明,这只是粗略计算,具体还得让更有经验的分析师来出更精准的图表。

从流通供应量的激增可以看出,「固定」 通胀率的说法并不准确:它在两个时间节点会大幅上升,其他时候则较低。

「行了,书呆子,你的数学算得也不准。我为啥要读这些?」

重点在于一个数字:每天流入市场的 SOL 数量。如果有人免费拿到代币(质押通胀 / 解锁),或是以折扣价获得(FTX 的 SOL)。可以预见,总会有一定比例的人会卖出。我假设未来一年 3750 万枚 SOL 的通胀量会被全部卖出。若是要让价格上涨,这可不是好事。所以我们需要资金流入,可能来自 DAT,也可能来自像 SSK(REXShares 推出)这样的 ETF。理想情况下,每一笔用来买 SOL 的钱都该流入市场,助推价格一路飘绿。但如果有机会买到锁定或折扣 SOL,就没必要非得去市场上买了。所以不妨假设,那些 DAT 机构会在解锁 SOL 流入市场前就出手买下。

这是坏事吗?

简而言之,不是。若要抵消未来一年 3750 万枚 SOL 的抛压(假设 SOL 价格为 200 美元,纯属乐观猜测),每年需要约 75 亿美元的资金流入,也就是每天约 2050 万美元。如果 DAT 能以折扣价从清算 SOL 或其他锁定 SOL 渠道买入,就能提高资金流入的效率。

筹集 4 亿美元以 5% 的折扣买入 SOL,相当于带来 4.2 亿美元的资金流入效果,比直接投入 4 亿美元更划算。唯一的问题是,如何权衡当下从市场买 SOL 和未来减少抛压的时间价值。

未来 3 年,Solana 的通胀规模将超过解锁量(锁定计划截至 2028 年底),而 FTX 的 SOL 仅占剩余解锁量的 1/4—— 所以 DAT 去买清算 SOL 而非从市场买,其实没必要担心。只要有足够的清算 SOL 出售,Galaxy 或 Pantera 中的任何一家都能消化剩余量,这还没算上 DeFi Dev Corp、SOL Strategies 或 Upexi 等现有的 DAT,以及现有的 ETP。

好消息:交易供应量 vs 流通供应量

投入 SOL 的资金比投入 ETH 或 BTC 的资金效率更高,有两个主要原因。

交易供应量

第一,流通供应量不等于市场可交易量,对于质押资产尤其如此。你买不到质押的 SOL,但能买到 LSTs(流动性质押代币)。根据 @solscanofficial 团队的数据,Solana 当前 6.08 亿枚 SOL 中,有 3.84 亿枚处于质押状态,占比 63.1%,无法在市场流通。LSTs 对应的 SOL 数量为 3350 万枚,把这部分算作可购买供应量的话,大致算下来,约 3.5 亿枚 / 5.08 亿枚 SOL 处于锁定状态,占比 57.5%,无法购买(至少得等两天解锁)。相比之下,ETH 的质押率为 29.6%,LSTs 占比 11.9%。市场可交易量越高,价格越难推动,不过 ETH 的解锁计划和各链 DeFi 平台的差异显然也有影响。

相对资金影响

Solana 的估值远低于 ETH 和 BTC。Solana 当前流通市值约 1040 亿美元,而 ETH 和 BTC 分别为 5400 亿美元和 2.19 万亿美元。从相对估值来看,投入 SOL DAT 的 1 美元,相当于投入 ETH DAT 的 5 美元,或投入 BTC DAT 的 22 美元。若再结合质押带来的流通供应量差异,效率差距会扩大到 ETH 的 11 倍、BTC 的 36 倍。好消息是,这些 DAT 会减少市场供应量,还能通过质押获得代币收益(我们已假设这部分会被卖出),且能让 ETF 等后续买入行为对市场价格的影响更显著。SSK 自推出以来,每天约有 200 万美元的资金流入,但抵消通胀需要 10 倍的资金流入,这可能得等更多 ETF 获批后才能实现。

总结

- 与 ETH 或 BTC 的 DAT 相比,SOL DAT 在吸纳当前交易供应量(与流通供应量不同)方面效率更高。目前,SOL DAT 管理的供应量不足 1%,随着 3 个新宣布的计划落地,这一比例可能会升至 3%,若有更多后续计划,可能会达到 5%。

- 近期宣布的 25 亿美元 SOL DAT 计划,相当于 ETH 300 亿美元或 BTC 910 亿美元的融资规模。SOL DAT 需要一个像 Michael Saylor 或 Tom Lee 这样的推动者,叙事才是关键。

- 我们终于快要摆脱 FTX 清算 SOL 对市场的影响(不过 FTX 在叙事层面的影响仍需消除)。

- SOL 的通胀问题仍会阻碍其价格上涨,亟待解决,通胀规模约为解锁量的 3 倍。

- 当前 ETF 的资金流入不足,但预计到第四季度初会有更大规模的产品获批,而 SOL 仍是机构投资者的潜在选择。

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。