Canggu (NYSE:CANG), this is an undervalued "Eastern MicroStrategy."

This round of "MicroStrategy-ization" has swept through the capital markets: putting Bitcoin on the balance sheet, combined with the narrative of "long-termism + capital tools," can indeed bring about a pricing premium. However, the script is too easy to copy, leading to a large number of "talk but no action" imitators in the market—slogans come first in announcements, while actual holdings remain vague, let alone systematic disclosures and closed funding loops: there are neither clear refinancing and risk control arrangements nor verifiable data rhythms.

The result is that "more and more companies are telling stories, but very few can solidify and stabilize their balance sheets."

In the author's view, to identify whether a company is "telling a story" or "truly has substance," a worthy "MicroStrategy-style" company must meet the following conditions: incorporate long-term holding into corporate governance, utilize capital market tools (such as equity offerings/convertible bonds, etc.) for disciplined balance sheet expansion, provide high-frequency, verifiable financial disclosures, and maintain a solid cash flow. Only when these three resonate in harmony can the story premium solidify into a cyclical balance sheet, rather than collapsing into a bubble when the market retreats.

And Canggu perfectly hits these points.

Looking back at Canggu's "transformation" path

If you straighten out the timeline, you will find that this is not a performance of "buying coins on the rise," but a meticulously planned corporate transformation. First, spin off, then consolidate; first stabilize production capacity, then fix the holding rhythm with monthly disclosures, and finally consolidate synergy through governance.

On November 6, 2024, Canggu first announced and then completed the cash acquisition of 32 EH/s of operational mining machines (the seller being an entity related to Bitmain), while simultaneously disclosing plans to acquire an additional 18 EH/s of operational mining machines through stock issuance (which was later completed on June 27, 2025). This marked the beginning of its entry into the cryptocurrency mining business. That month, Canggu produced 363.9 BTC, and in December, it produced 569.9 BTC, all of which were not sold, marking the earliest form of Canggu's "MicroStrategy-style hoarding of BTC."

By 2025, governance became another main line for Canggu.

One of the most important actions was on May 27, when the company disposed of its entire mainland business, selling it to Ursalpha Digital Limited for a cash consideration of approximately $351.94 million, actively isolating the revenue of the old model from the risks of the new strategy, leaving historical burdens behind. From then on, all capital and disclosure standards aligned with the main axis of "Bitcoin mining + BTC asset management."

Expanding the balance sheet was not about "buying spot and telling stories," but directly incorporating "operational mining machines." Thus, on June 27, Canggu completed the asset delivery of cryptocurrency mining machines through equity settlement, consolidating 18 EH/s of computing power in one go, with the consideration being the issuance of 146,670,925 Class A common shares to the seller; among them, Golden TechGen Limited (GT) became a significant shareholder, holding approximately 19.85%, while the seller collectively held about 41.38%. This "exchange of shares for production capacity" transaction has two key signals: first, most of the machines are located in data centers in the U.S. and other countries, allowing for immediate production upon delivery, reducing the time loss of "buying equipment—powering up—ramping up"; second, the production capacity immediately became a solid foundation for the balance sheet, providing a sustainable source of "inherent BTC" for subsequent monthly disclosures and inventory strategies.

Once the production capacity was in place, the operational rhythm quickly became evident. The July disclosure showed that Canggu's deployed computing power had reached 50 EH/s, with an average operational computing power of 40.91 EH/s for the month, resulting in a monthly output of 650.5 BTC, a 45% increase month-on-month; the ending inventory then rose to 4,529.7 BTC. The significance of this data lies not only in "running fast" but also in the clarity and frequency of disclosures: the company synchronously updates "output/deployment/monthly average/inventory" along four lines, laying the closed loop of "production capacity—output—inventory" in the sunlight, providing investors with an operational dashboard that can be "matched monthly." The management also clearly stated that they "do not intend to sell" the Bitcoin held, and the HODL attitude and rhythm were included in external communications.

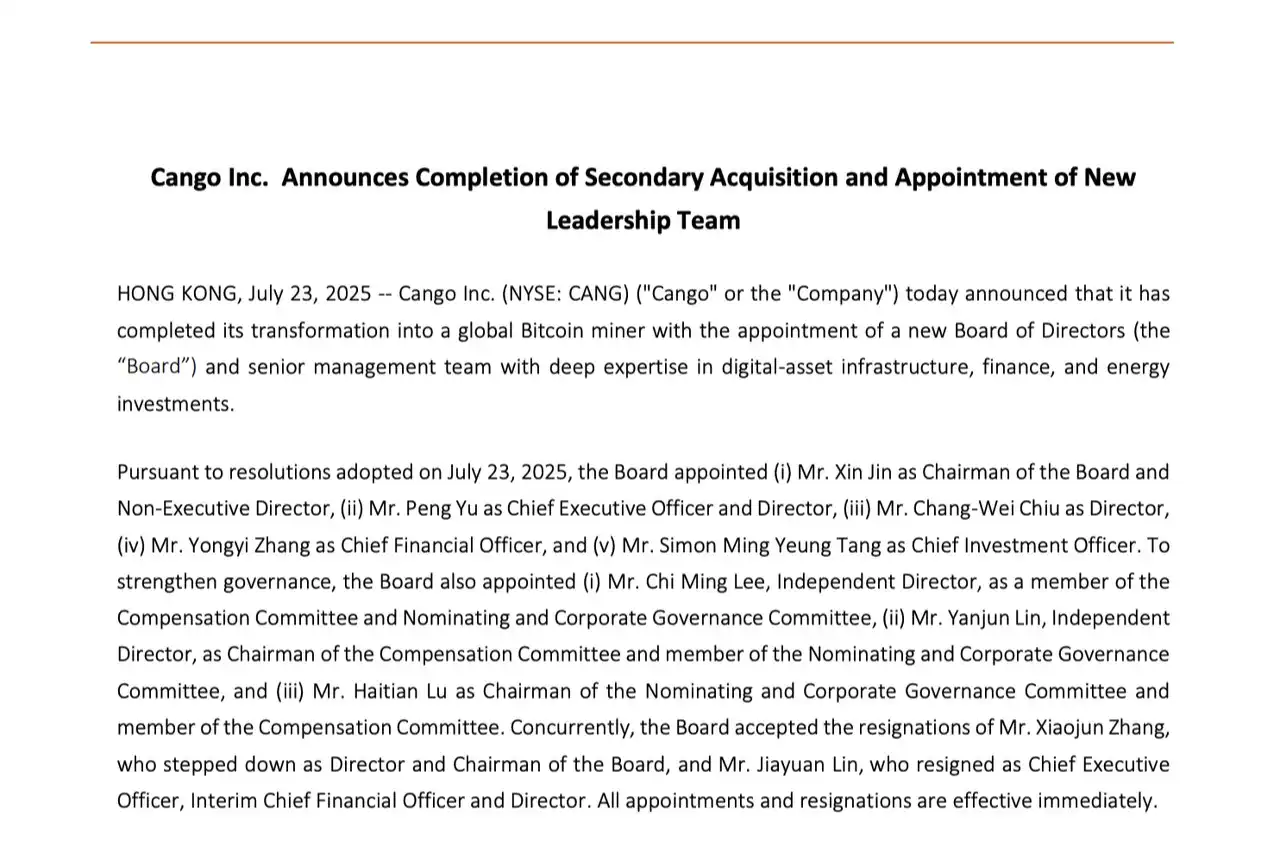

The governance-level shift progressed in tandem with production capacity and disclosures. On July 23, the company announced the completion of a secondary equity transaction and board restructuring: Antalpha founder Moore Xin Jin was appointed chairman, Paul Yu as CEO, Michael Zhang as CFO, and Simon Tang as CIO, among others. On one hand, the control structure and management team were aligned in one go, leaving ample organizational depth for the synergy of "production capacity—capital—power"; on the other hand, strategic cooperation was established with important industry participants, including Bitmain and Antalpha, which means Canggu has greater industrial synergy space and bargaining power in mining machine supply, asset management, and even energy investment. For a company following an "asset-driven" route, such an industrial capital alliance equates to turning external uncertainties into deployable internal resources.

Canggu announces the completion of a secondary acquisition and the appointment of a new management team

Pricing Misalignment: Why is Canggu Undervalued?

Let's first look at the pioneer of "holding coins in U.S. stocks," MicroStrategy itself: in fact, MicroStrategy's greatest competitive advantage lies in its strong capital means, which can raise money in the market, but its own production capacity is almost nonexistent. If you ask people around you who know MicroStrategy, the vast majority are unaware of its main business. In contrast, Canggu's advantage is its own production capacity and endogenous engine, which means continuous mining with mining machines, reducing sensitivity to purely relying on financing for balance sheet expansion.

Using more intuitive premium data, Canggu currently holds 628,791 BTC, corresponding to mNAV≈1.68x; in other words, the market is willing to give it an additional 68% premium above the net value of Bitcoin to price its financing capability and the sustainability of "long-term coin holding."

Applying the same set of metrics to Canggu, by July 2025, Canggu's monthly disclosure showed: inventory of 4,529.7 BTC, monthly output of 650.5 BTC, deployed computing power of 50 EH/s, average operational computing power of 40.91 EH/s, with the company clearly stating "currently does not intend to sell." Based on the approximate price of Bitcoin at $114,165 on August 6, Canggu's market value of held coins is about $517 million; while its disclosed market value is about $833 million, with a stock price of approximately $4.70–$4.73. This means Canggu's "BTC coverage premium" is only ~1.61x ($8.33B/$5.17B), close to MSTR's ~1.68x, not to mention that most current "MicroStrategy-style" companies have premium rates between 3-10 times.

However, unlike MSTR—Canggu also comes with a 50 EH/s computing power engine. The same "coin-holding premium" is layered with "production capacity in hand" as endogenous cash flow, which is the first piece of evidence for being "undervalued."

Comparing with Japan's Metaplanet, it enjoys the benefits of Japan's tax system and investor structure, but lacks the deeper liquidity of the U.S. stock market, which may pose a greater risk of institutional shorting; while Canggu follows the U.S. stock path, with higher disclosure frequency and deeper liquidity, combined with the consolidation of computing power, the threshold for capital participation and expectation management is more transparent.

As for comparing with traditional "pure mining companies," Canggu has even more advantages. We all know that mining companies are inherently profitable, which is why the last wave of crypto enterprise IPOs was led by mining companies.

However, after several cycles, the traditional mining company's model still largely remains in "mine—sell—expand," exposing them more passively to price fluctuations; while Canggu, with its public HODL policy, combined with "equity settlement expansion" capital actions, has pushed itself from the paradigm of "selling mining cash flow" to "strengthening the balance sheet with BTC" as an asset operator, creating a positive spiral that will be healthier.

Looking again at the intuitive data, if we align Canggu's market value with its computing power, we get a rough estimate of the "market value / EH/s" indicator: with $833 million against 50 EH/s, it is about $16.65 million/EH/s; if we use the average operational computing power of 40.91 EH/s, it is only $20.35 million/EH/s. Comparing these two sets of numbers with two leading companies in North America: Riot had deployed 35.5 EH/s by the end of July, with a market value of about $4.1–4.2 billion, corresponding to $106–116 million/EH/s; Marathon's market value is about $5.7–5.9 billion, with "energized hashrate" often around ~54 EH/s in recent quarters, corresponding to $106–109 million/EH/s. In the same field and with the same metrics, Canggu's unit computing power pricing is only about 1/5–1/7 of the leaders, which falls within the undervalued range.

Additionally, looking at the mining machine fleet and efficiency, Canggu has provided efficiency metrics in its annual report and information releases: the average fleet efficiency is about 21.6 J/TH, and in Q4/2024, the unit computing power output reached 17.81 BTC/EH/s, with about 90% of the fleet being Bitmain's water-cooled models; this means that under the same electricity price, its "electricity-to-coin" efficiency is not at a disadvantage. By combining "energy efficiency" with "geographic dispersion" (sites in the U.S., East Africa, Oman, Paraguay, etc.), Canggu has enough room to further reduce the unit BTC all-in cost on the electricity cost curve, which will widen the gap with peers during a bear market.

Canggu's Next Steps

What truly supports valuation is not just swapping for a trendy term, but making the balance sheet "thick" and "stable."

Reflecting on Canggu from this "first principle," it treats Bitcoin as a quasi-strategic reserve at the corporate level: the management has clearly stated in public communications that they "do not intend to sell," and combined with the monthly disclosures of production capacity, output, and inventory rhythms, they have institutionalized HODL from an attitude into a verifiable system for the market.

The key to long-termism is not how long you shout, but how the market can match monthly—investors, each time they open disclosures, see not just price fluctuations, but the increase in inventory, steady operation of production capacity, and governance structure backing all of this. This approach of "handing uncertainty to processes and writing certainty into reports" is the essence of transcending cycles.

Mining has a simple iron rule: electricity price is the number one variable. Whoever can lock in low electricity prices and renewable energy in a broader region and in a long-term stable manner can drive down the "all-in cost" of each BTC to a lower percentile during a bear market. Canggu's new board and management team, with their composite backgrounds in mining machines, finance, and energy investment, means they have the capability to create a closed loop of "electricity price—production capacity—holdings—financing."

Canggu's next step may be to continue making adjustments in the "power side," which determines the upper limit. This includes connecting long-term power agreements and demand response in North America, taking on surplus energy and green power indicators in the Middle East, and seeking cost advantages and flexible power structures in South America and East Africa. At the same time, leveraging expertise in computing power and energy operations, Canggu can gradually move towards providing HPC infrastructure services for AI companies, opening up a second growth curve for the enterprise; the front end is computing power deployment, the back end is the stable thickening of the balance sheet, and the middle relies on the synergy of power contracts, operational efficiency, and capital tools.

However, integrated mining does not seek to achieve everything at once but rather gradually sinks in through project clusters, turning "low electricity prices + high operating rates + replicable operations" into an expandable organizational capability. In a bear market, this determines the pressure resistance radius; in a bull market, this determines the speed of balance sheet expansion and financing bargaining power.

At this point, we may all realize that what Canggu truly wants to convey is not the story of "buying coins on the rise," but rather the story of "utilizing its own production capacity to turn BTC into the foundation of the balance sheet": mining machines bring in endogenous BTC cash flow, the disclosure system provides verifiable trust, and HODL transforms long-termism into company-level rules.

And this is precisely the path through which Canggu fulfills its narrative as the "Eastern MicroStrategy."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。