Original Title: The State of Crypto VC

Original Author: Mason Nystrom

Original Translation: Deep Tide TechFlow

Providing founders with insights into the current state of cryptocurrency financing, as well as my personal predictions for the future of cryptocurrency VC.

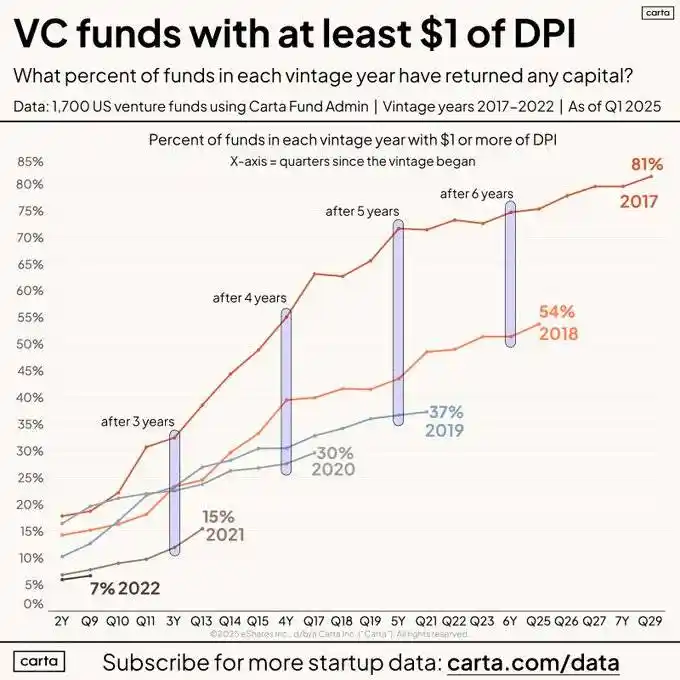

To begin with: The financing environment is challenging due to upstream DPI (Deep Tide Note: a market-cap-weighted index used to track the performance of decentralized finance (DeFi) assets in the cryptocurrency market) and LP funding challenges. Across the entire VC landscape, the amount of capital returned to LPs by funds during the same period has decreased compared to previous years.

This, in turn, leads to a reduction in net capital available to existing and new VCs, ultimately making the financing environment more difficult for founders.

What does this mean for crypto companies?

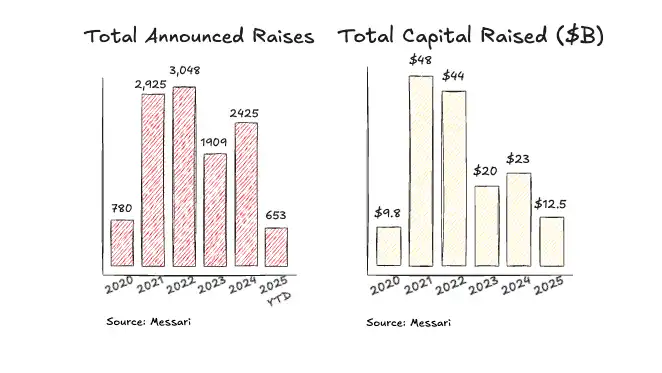

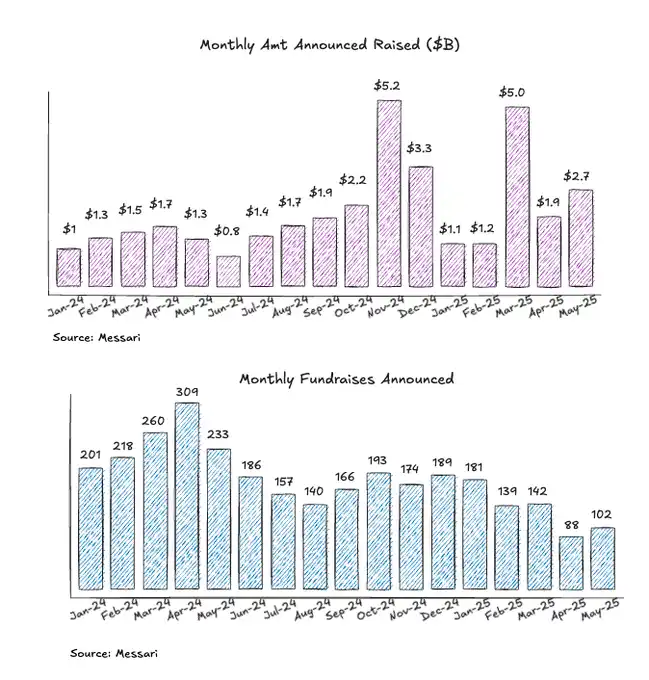

Transaction volume is slowing in 2025, but matches the pace of capital deployment in 2024.

The slowdown in transaction volume may be related to many VCs nearing the end of their funds, resulting in less capital available for deployment.

Some large transactions are still completed by large funds, so the pace of capital deployment remains on par with the previous two years.

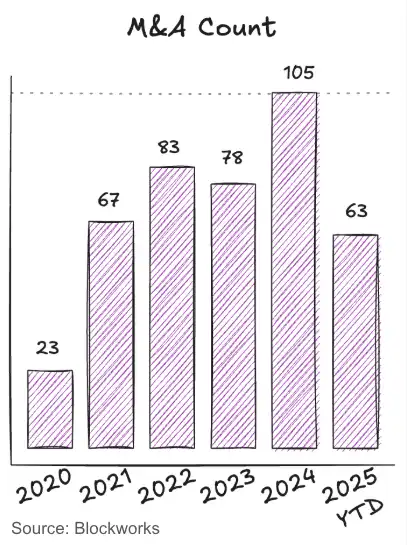

Over the past two years, cryptocurrency M&A transactions have continued to improve, indicating good developments in liquidity and exit opportunities. Recent large M&A transactions, including NinjaTrader, Privy, Bridge, Deribit, and HiddenRoad, signal a positive trend towards consolidation and underwriting more crypto equity risk investments.

In the past year, transaction volume has remained relatively stable, with some larger, later-stage transactions completed (or announced) in Q4 2024 and Q1 2025. This is mainly because more transactions belong to the early Pre-seed, Seed, and Accelerator stages, which typically have ample funding.

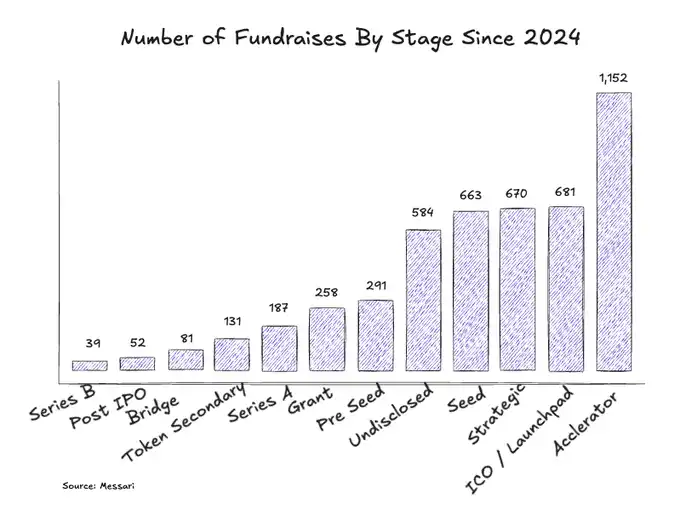

Accelerators and Launchpads lead in transaction volume across stages

Since 2024, a large number of accelerator and Launchpad platforms have emerged in the market, which may reflect a more challenging capital environment and founders opting to launch tokens earlier.

Median deal size in early-stage transactions rebounds

Pre-seed financing amounts have continued to grow year-on-year, indicating that the market still has ample funds in the early stages. The median amounts for Seed, Series A, and Series B financing have approached or rebounded to 2022 levels.

Predictions for the future of crypto VC

1: Tokens will become the primary investment mechanism

Shifting from a dual structure of tokens and equity to a unified structure of single asset appreciation. One asset, one value appreciation story.

Original tweet link: https://x.com/MorphoLabs/status/1930973177691189423

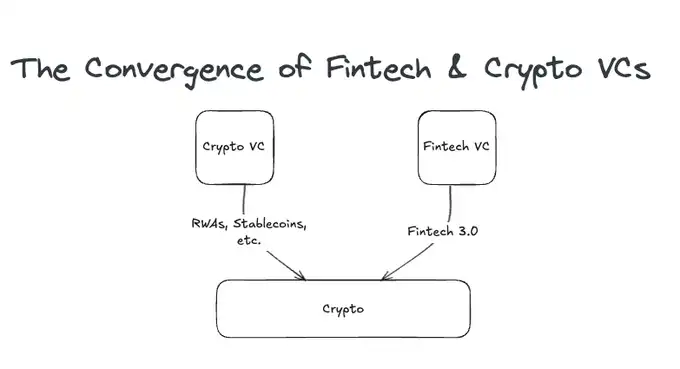

2: The integration of fintech and crypto VC

Every fintech investor is transforming into a cryptocurrency investor as they seek to invest in the next generation of payment networks, new banking models, and tokenized platforms, all built on cryptocurrency rails. Competition in crypto VC is about to intensify, and many crypto VCs that have yet to invest in stablecoins/payment sectors will find it difficult to compete with experienced fintech VCs.

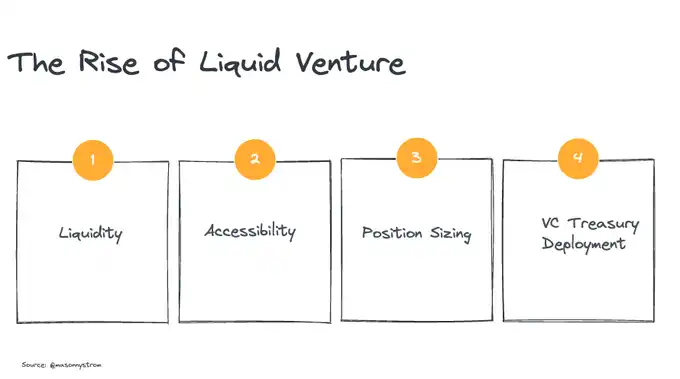

3: The rise of liquidity venture capital

"Liquidity venture capital" — venture capital opportunities in the liquid token market.

· Liquidity — The liquidity of public assets/tokens means faster liquidity.

· Accessibility — Gaining access in private venture capital is not easy, while liquidity venture capital means investors do not always need to win deals; they can directly purchase assets. OTC options are also available.

· Position adjustment — As companies issue tokens earlier, this means smaller funds can still build meaningful positions, and larger funds can similarly deploy into larger liquid assets.

· Capital allocation — Many historically top-performing VCs have held their risk capital in tokens like BTC and ETH, which have generated excess returns. I personally believe that during bear market cycles, it will become more common for VCs to call upon more funds in advance.

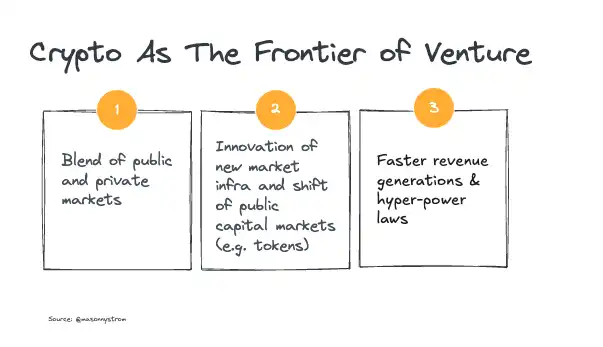

Cryptocurrency will continue to lead the forefront of VC

The integration of public and private capital markets is the direction of venture capital development. As companies delay going public, more traditional VCs are choosing to invest in liquidity markets (holding tools post-IPO) or secondary markets. Cryptocurrency is at the forefront of venture capital. Cryptocurrency continues to innovate in the formation of new capital markets. Moreover, as more assets move on-chain, more companies will look towards on-chain priority capital formation.

Finally, the returns from cryptocurrency are often more power-law driven (Deep Tide Note: In a power-law distribution, the probability of most events occurring is low, while the probability of a very few events occurring is high.), with top crypto assets vying to become the underlying sovereign digital currencies and new financial economies. This decentralization will be greater, but the super-power-law nature and volatility of cryptocurrency will continue to drive capital into the cryptocurrency venture capital space, seeking asymmetric returns.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。