Original Title: "In-Depth Analysis by Web3 Lawyers: How Can Mainland Enterprises Successfully Issue RWA Products in Hong Kong?"

Original Authors: Gui Ruofei, Sha Jun, Crypto Law

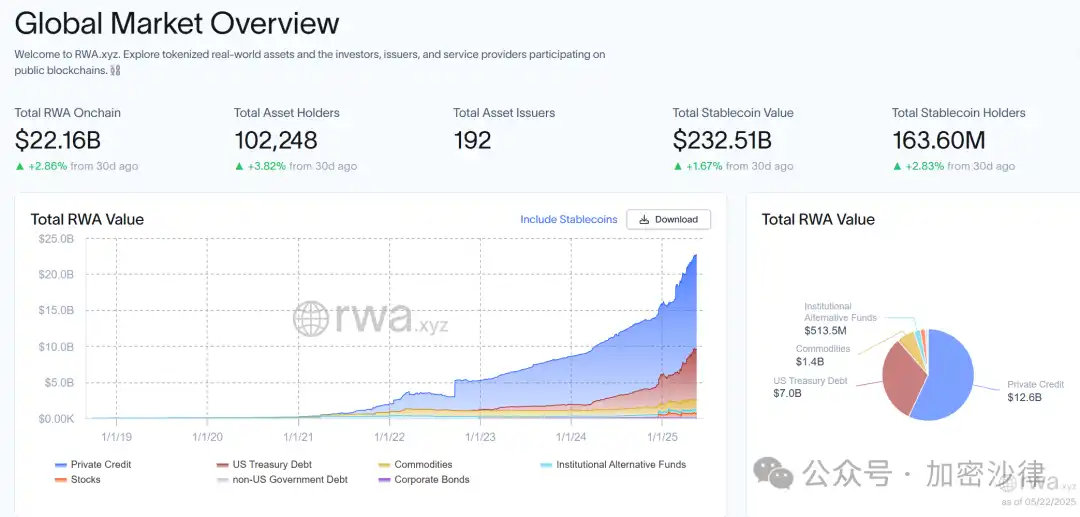

The global asset tokenization process is accelerating, with data from the RWA.xyz platform indicating that by April 2025, the total value of on-chain RWA assets worldwide has surpassed $22 billion. Meanwhile, Deloitte's research report predicts that the tokenized real estate market will reach $4 trillion by 2035.

In this wave of financial innovation, Hong Kong has rapidly developed into a pioneer of compliant development in the RWA field, leveraging its unique institutional advantages—from the asset tokenization project of charging pile assets launched by Longxin Group to the launch of Asia's first compliant tokenized fund by Huaxia Fund. The successful implementation of several benchmark cases confirms the application potential of this innovative financing method in the field of physical assets.

· What exactly is RWA?

· Why choose RWA, and what are its advantages?

· How does Hong Kong regulate RWA?

· What compliance points should mainland enterprises pay attention to when conducting RWA in Hong Kong?

The Crypto Law team has been deeply involved in the cryptocurrency industry for many years, possessing rich experience in handling RWA project structure design and related complex cross-border compliance issues. In this article, we will combine the team's latest RWA project experience and industry research results to clarify and answer the above questions from a professional lawyer's perspective.

(The above image is a dashboard of global on-chain RWA assets organized by the website RWA.xyz)

I. What Exactly is RWA?

RWA, which stands for "Real World Assets," refers to the tokenization of real-world assets, an innovative financial model based on blockchain technology. It maps physical or financial assets onto the blockchain, transforming them into highly liquid and divisible digital tokens. This transformation process not only achieves a digital representation of assets but also endows these real assets with unprecedented transparency and traceability through blockchain technology.

While we can theoretically elaborate on the connotation and extension of the RWA concept, it is challenging for all parties to reach a complete consensus on specific project practices.

"What exactly is true RWA? Which projects should be recognized as RWA projects?" — Professionals, regulatory agencies, and project parties all have their own perspectives and viewpoints on these questions. The Crypto Law team, combining project experience and research results, provides its viewpoint from a legal compliance perspective: "RWA is actually a broad concept without a so-called standard answer. All processes that achieve asset tokenization through blockchain technology can be referred to as RWA." For an in-depth analysis of the RWA concept, see: "Web3 Lawyers Decode: What Kind of RWA Do We Understand?"

II. Why Choose RWA, and What Are Its Advantages?

(1) Activating Heavy Asset Financing Scenarios Difficult for Traditional Finance

Firstly, taking real estate, infrastructure revenue rights, and bulk commodities as examples, these assets are difficult to finance through traditional financial tools due to their heavy asset nature, liquidity constraints, and complex compliance and regulatory issues. The RWA model, combined with blockchain technology, allows for the segmentation of ownership of these physical or rights-based assets, transforming them into highly liquid digital tokens and raising funds from investors through the issuance of digital tokens. RWA opens up a new financing method for these assets, allowing previously "dormant" assets to be revitalized. This means that in a context of limited financing channels, high financing difficulty, and high financing costs, RWA provides enterprises with a new "blood generation method."

For investors, the divisibility of tokens lowers the investment threshold for specific assets. For instance, in traditional finance, an investor wishing to invest in real estate often needs to spend hundreds of thousands of dollars to acquire the entire property rights. The high financial threshold excludes many small and medium investors. However, relying on the RWA model, an investor may only need to spend $50 to purchase a token representing a portion of the property rights. By holding this token, the investor can enjoy investment returns from property appreciation and rental income.

(2) Reducing Financing Costs and Improving Financing Efficiency

In traditional securities issuance processes, enterprises and projects must undergo strict and lengthy review processes, with the qualifications, scale, and operational methods of the issuing entity needing to meet high requirements. Taking asset-backed securities (ABS) issuance as an example, the regulatory and approval standards are extremely strict, which significantly limits the financing needs of some enterprises.

In the RWA model, financing parties only need to comply with local regulatory requirements, while other entry requirements and restrictions are relatively few, although they still need to ensure compliance of the underlying assets. Therefore, this financing method avoids the lengthy review processes and cumbersome issuance procedures of traditional financing to some extent, effectively reducing financing costs.

(3) Customized Transaction Structures

RWA financing provides enterprises with unprecedented flexibility, allowing them to tailor financing structures according to market demands and their own development goals. Enterprises can independently design key terms such as revenue distribution models, redemption mechanisms, and token unlocking mechanisms, and adjust issuance conditions in real-time based on market dynamics. This high degree of flexibility enables enterprises to precisely match investors' expectations and risk preferences, thereby improving the targeting and success rate of financing.

Fundamentally, in addition to introducing blockchain technology to improve financing efficiency and transparency, RWA also changes the financing logic under the traditional financial framework. Traditional financing models, whether debt or equity financing, largely rely on company credit as a basis. In contrast, RWA, through blockchain technology, achieves an effective separation of "company credit" and "asset credit." As a result, even if the issuing entity's credit status is average, as long as the underlying assets are of sufficient quality, financing can be achieved based on the credit of the assets themselves.

This characteristic is similar to the ABS model mentioned above. However, while both have similarities in financing logic, the core difference lies in the investor groups covered and the ecological effects they create. The ABS market is primarily dominated by traditional financial institutions, with a relatively limited participant group, and the trading entities are mostly institutional investors. This characteristic results in insufficient overall trading depth for ABS and a relatively narrow market coverage, lacking widespread influence.

In contrast, the RWA market has a more diverse range of participants. In addition to traditional financial institutions, the RWA financial market also attracts numerous crypto investors and industry ecosystem partners. Therefore, in the RWA market, from professional institutions to ordinary retail investors to partners, everyone can freely buy, sell, and use the tokens, becoming an important part of the token ecosystem.

A large and active ecosystem and community have formed around RWA tokens. The strong community cohesion and ecological stickiness generated will provide robust support for the long-term value growth of RWA tokens, thereby promoting the healthy development of the market. The prosperity of the on-chain ecosystem can also feed back into the off-chain business development of project parties and significantly enhance the brand voice of the project parties.

This on-chain-off-chain collaborative positive feedback development model is the true brilliance of the RWA model compared to traditional financing methods and is something the ABS model finds difficult to achieve. Currently, the market is still continuously cultivating and expanding the RWA investor group. In the current RWA track, various financial asset tokenization products are leading the way. Due to the high compliance, high standardization, and low data capture difficulty of financial assets themselves, the tokenization of financial assets has unique advantages and demonstration effects in the RWA track.

The wave of financial asset tokenization began with low-risk underlying assets such as U.S. Treasury bonds and money market funds, with a typical case being the BUIDL tokenized investment fund launched by the global top asset management group BlackRock. As of now, BUIDL's total market value has reached $2.89 billion. In addition to low-risk financial assets, high-risk stocks, ETFs, and other financial assets have also recently entered the fast lane of tokenization. On May 22 and 23, the Kraken trading platform and Ondo Finance announced their plans to promote the tokenization and on-chain trading of stocks, ETFs, and other financial assets.

With the rapid landing and development of various tokenized financial assets and stablecoins, the scale and liquidity of investors in the RWA market will reach new heights. In the future, more and more different types of RWA products will enter the sight of investors, attracting more Web2 users and traditional financial investors into the RWA ecosystem. The entire RWA ecosystem's flywheel will quickly cycle and develop, bringing new wealth effects and industry opportunities.

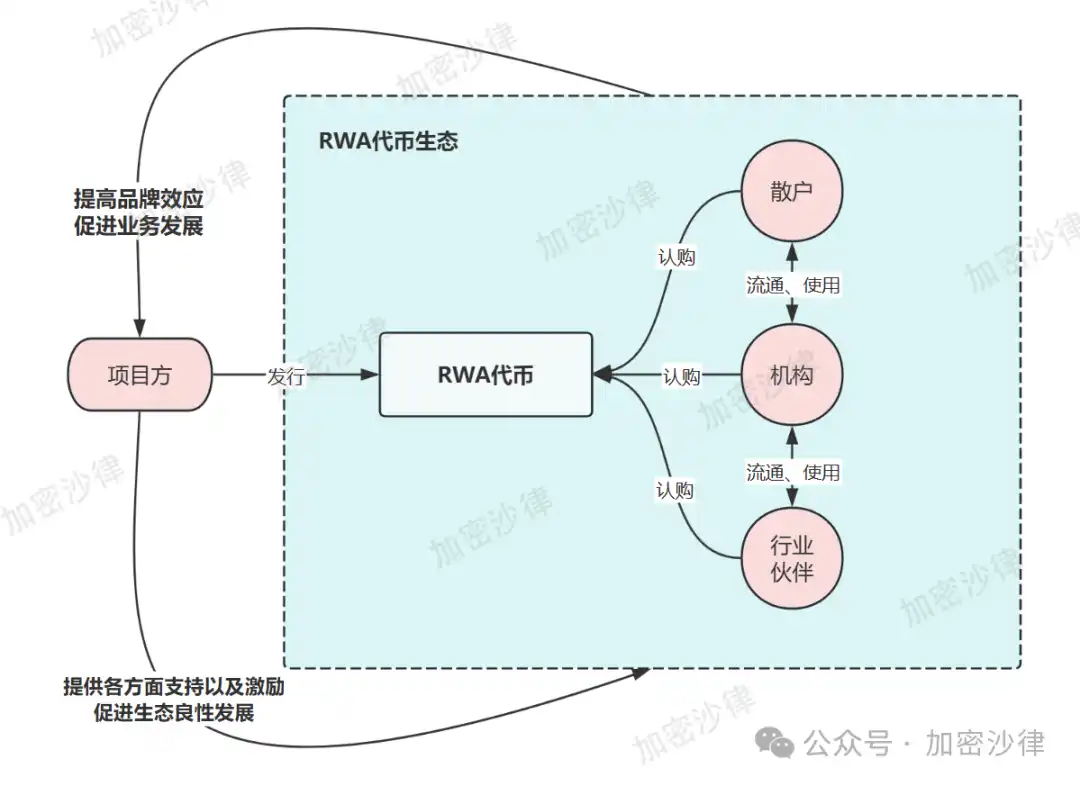

(The above image is a schematic diagram of the RWA ecosystem development model for reference only)

III. How Does Hong Kong Regulate RWA?

(1) Regulatory Principles

The Hong Kong Securities and Futures Commission (SFC), as the backbone of market regulation in Hong Kong, adopts a "See-Through Approach" in regulating RWA products. The core of this principle is that the focus of regulation is not on whether the product takes the form of a "token," but rather on the financial attributes of the real assets corresponding to the tokens. In short, Hong Kong's regulation of RWA aims to return to the essence of the underlying assets, rather than being confined to the form of the tokens. This regulatory principle is also a concrete embodiment of the idea of "same business, same risk, same rules."

(2) Specific Regulatory Documents

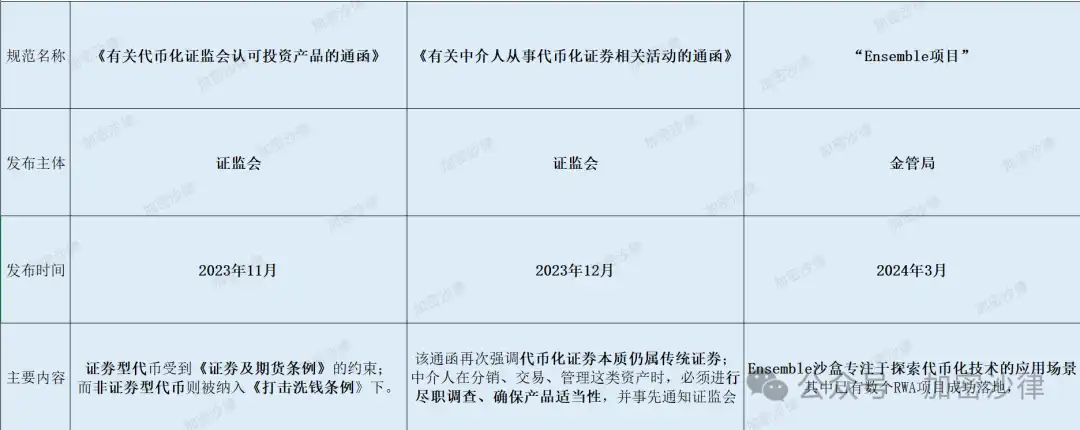

In November 2023, the Hong Kong Securities and Futures Commission (SFC) released a circular titled "On Tokenized Securities Recognized Investment Products," which clarifies the layered regulatory concept for the issuance of securities tokens. According to the relevant regulations, securities tokens are subject to the Securities and Futures Ordinance and must meet the relevant requirements proposed by the SFC in the aforementioned circular, including token issuance qualifications, information disclosure, and investor suitability. Non-securities tokens are included under the regulation of the Anti-Money Laundering Ordinance.

In November 2023, the Hong Kong Securities and Futures Commission issued a circular titled "On Intermediaries Engaging in Tokenized Securities-Related Activities." This circular reiterates that although tokenized securities are issued using blockchain technology, their essence still belongs to traditional securities and must comply with existing securities regulations. Additionally, intermediaries must conduct due diligence, ensure product suitability, and notify the SFC in advance when distributing, trading, or managing such assets.

In March 2024, the Hong Kong Monetary Authority launched the "Ensemble Project." The Ensemble sandbox focuses on exploring application scenarios for tokenization technology, with several RWA projects already successfully implemented, covering various industries such as green bonds, carbon credits, real estate, and supply chain finance.

Overall, from 2023 to 2024, the Hong Kong Securities and Futures Commission has successively released multiple circulars and guidance documents related to tokenized investment products, further clarifying the specific regulatory standards for RWA products (especially tokenized securities), thereby providing clear regulatory guidance for the robust development of the RWA market.

(The above image is a summary of the regulatory framework related to RWA)

The above text specifically analyzes Hong Kong's regulatory framework for RWA, while a complete systematic overview of Hong Kong's virtual asset regulatory policies can be found in the following article: "Mastering in One Article: A Systematic Overview of Hong Kong's Virtual Asset Regulatory Policy Framework"

IV. What Compliance Points Should Mainland Enterprises Pay Attention to When Conducting RWA in Hong Kong?

The reason for issuing RWA must involve a cross-border structure is that within mainland China, the issuance of tokens cannot cross the regulatory red line. On September 4, 2017, the People's Bank of China and seven other departments issued the "Announcement on Preventing the Risks of Token Issuance Financing," clearly stating that no organization or individual may illegally engage in token issuance financing activities, and all types of token issuance financing activities must be stopped immediately.

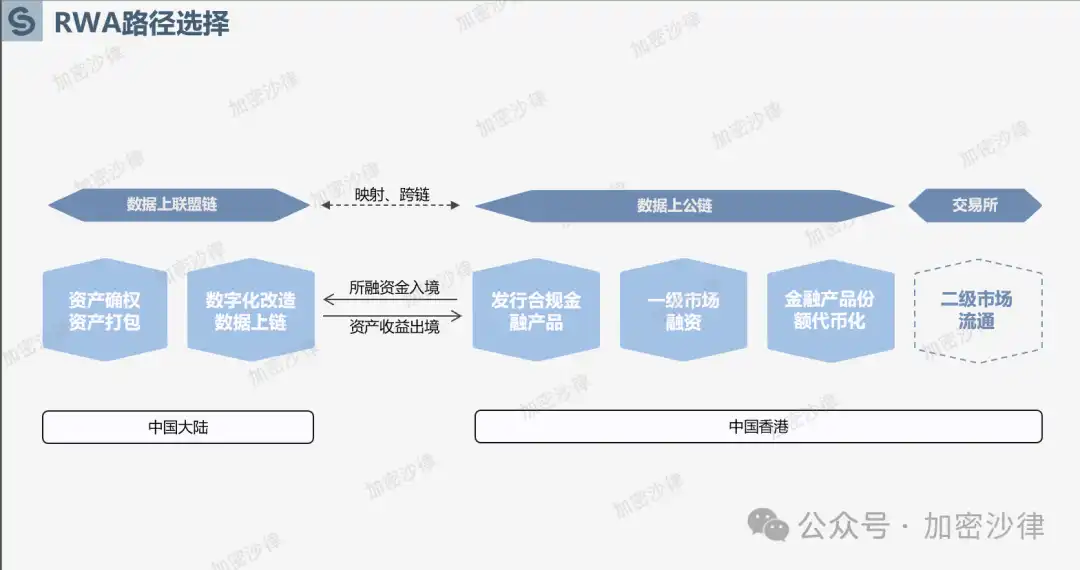

Therefore, the issuance of tokens for RWA projects in mainland China must occur overseas. Among them, Hong Kong has become one of the optimal choices for Chinese enterprises to implement RWA projects due to its sound regulatory framework, friendly policy attitude, and rich industry ecosystem. The following will analyze the key compliance points and framework design ideas for conducting RWA projects in Hong Kong from three aspects: underlying assets, data on-chain, and fund circulation.

(The above image is a schematic diagram of the overall framework for issuing RWA in Hong Kong)

(1) Compliance of Underlying Assets

1. Asset Confirmation

Since the essence of RWA is the tokenization of real-world assets, the holders of the tokens will directly or indirectly possess specific rights to the real-world assets. Therefore, to ensure that the subsequent RWA tokens can be legally issued, circulated, and redeemed, the owners of the underlying assets, i.e., the RWA project parties, must ensure that they have clear and legal ownership of the assets. The compliance team of the RWA project needs to conduct detailed due diligence on the underlying assets during the project process to ensure the legality of ownership. Specifically, the compliance team will conduct ownership dispute checks, collect and verify ownership proof documents, public registration information, litigation status, pledge, mortgage, or judicial freeze situations, and other relevant information during the due diligence process.

2. Asset Audit

After confirming the assets, the project party also needs to hire a professional auditing firm to audit the underlying assets. The audit report will provide reference data for subsequent asset pricing and issuance, including but not limited to the following elements:

· Market Value of the Asset — Fair market value assessment conducted by professional appraisers or valuation experts, referencing historical transaction data, market conditions, and prices of similar assets.

· Asset Depreciation and Impairment — For fixed assets, consider depreciation methods, asset lifespan, and possible impairment situations to ensure that the assessed value reasonably reflects the actual value.

· Asset Risk Identification — Identify risks associated with the asset, such as market risk, legal risk, liquidity risk, operational risk, etc.

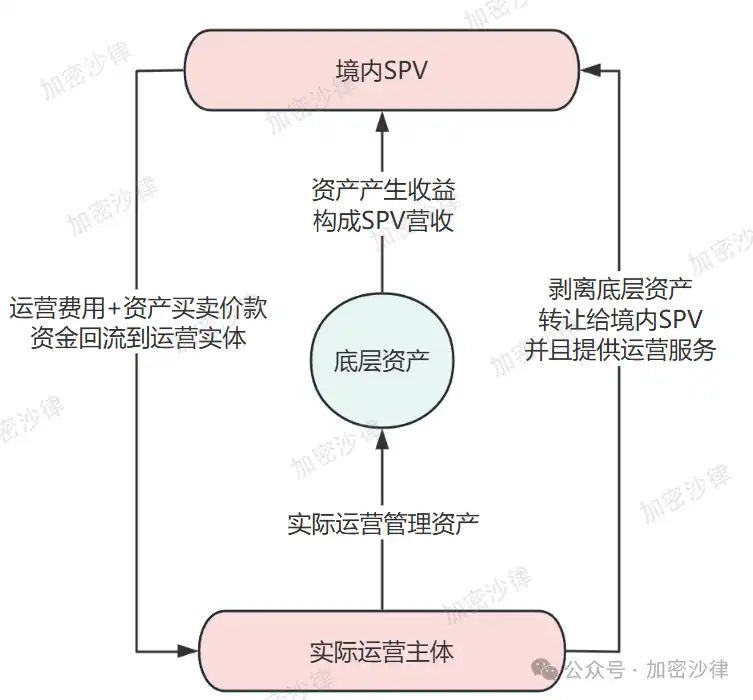

3. Asset Separation

As mentioned earlier, the core value of RWA lies in financing directly based on the credit of quality assets, thereby breaking away from the traditional financing model based on corporate credit. Therefore, when conducting RWA projects, it is necessary to separate the underlying assets from the actual operating entity of the project party to achieve risk isolation between the operating entity and the underlying assets. The following will illustrate one example of asset separation structure design based on a practical case that the Crypto Law team is currently promoting:

First, the project compliance team will assist the project party in establishing an SPV (Special Purpose Vehicle) domestically.

Second, the actual operating entity will transfer the underlying assets to the SPV through a sale transaction.

Finally, the SPV will sign an operational service agreement with the project party, with the project party responsible for managing the underlying assets, and the SPV paying the project party corresponding service fees regularly.

(The above image is a schematic diagram of the asset separation framework design for reference only)

In summary, through this asset separation structure, the project party can transfer asset ownership to the SPV, achieving risk isolation while facilitating subsequent asset packaging and issuance. Meanwhile, although the actual operating entity no longer owns the asset's rights, it can continue to manage and operate the underlying assets through the service agreement.

(2) Compliance of Data On-Chain

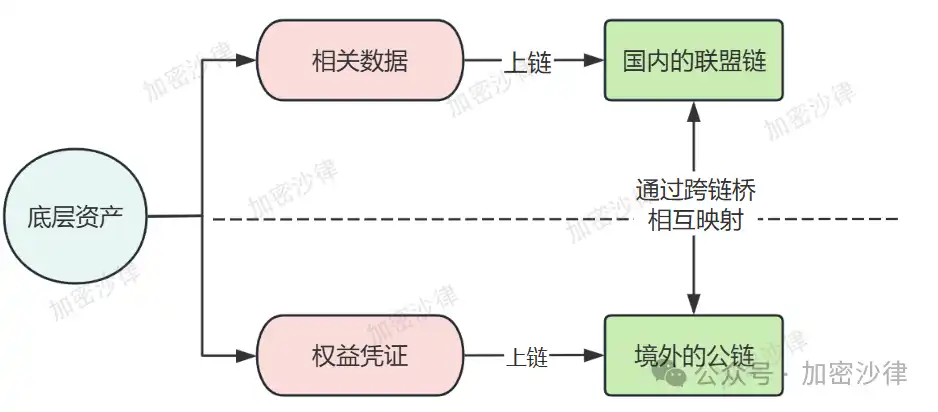

Due to the strict regulations in China regarding cross-border data transmission and data exchange, most RWA projects do not choose to transmit relevant data overseas and circulate and disclose it on public chains. The Crypto Law team found during research that, under the premise of meeting the compliance requirements of China's "Data Security Law" and "Personal Information Protection Law," project parties prefer to choose a "Two Chains and One Bridge" model to achieve data on-chain.

Specifically, RWA asset data is chosen to be on-chained in a domestic consortium chain and completed for proof of storage, while the corresponding RWA tokens are deployed on a high-performance public chain overseas. The RWA tokens circulating overseas and the data on-chain domestically are mapped and bound through a cross-chain bridge. This architectural design not only solves the problem of on-chain proof of data related to the underlying assets of RWA, ensuring the transparency and traceability of asset data but also avoids crossing the compliance red line of cross-border data transmission.

(The above image is a schematic diagram of the "Two Chains and One Bridge" model for reference only)

In addition to the "Two Chains and One Bridge" model, RWA projects can also rely on the Hainan Free Trade Port's cross-border data flow pilot zone (hereinafter referred to as "Hainan Free Trade Data Port") to complete cross-border data on-chain and circulation. According to the disclosed information, the Crypto Law team summarizes that the core framework of the data exit plan for Hainan Free Trade Port is as follows:

Data is actively classified and graded by regulatory agencies;

Establish a data whitelist; if data is included in the whitelist, it can be directly exported without approval;

If the data is not included in the whitelist, regulatory agencies will apply corresponding regulatory procedures based on different data types: personal information protection certification, data exit security assessment, personal information exit standard contract filing, etc.

The Crypto Law team has found that, in addition to the compliance requirements in the data circulation link, there are also some key compliance points and administrative regulatory requirements in the data collection, storage, desensitization, and packaging stages of the underlying assets of RWA. Due to the length of this article, these will not be discussed here.

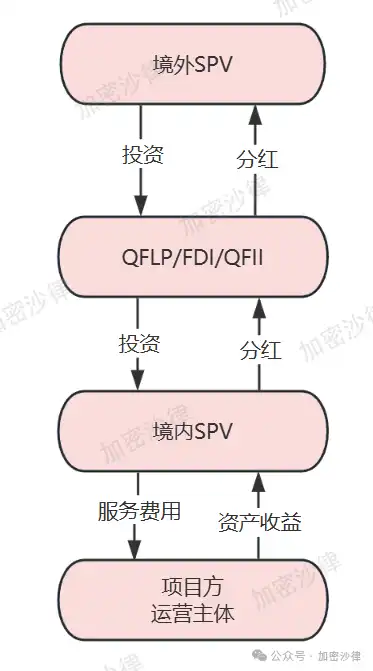

(3) Compliance of Fund Circulation

Due to the strict foreign exchange controls implemented in China, the funds raised from issuing RWA overseas cannot be directly transferred to the actual operating entity in China. The compliance team needs to specifically design a framework and path for the collection and circulation of overseas funds. Based on the project experience of the Crypto Law team, after financing through token issuance overseas, RWA projects generally collect the funds to the overseas SPV through a funding channel, which are then ultimately transferred to the actual operating entity. The funding channels in this structure have the following three options:

1. QFLP (Qualified Foreign Limited Partner)

2. FDI (Foreign Direct Investment)

3. QFII (Qualified Foreign Institutional Investor)

When designing the fund circulation structure, the compliance team generally needs to comprehensively consider the following factors: tax burden, entry threshold, procedural requirements, compliance costs, etc. Moreover, during the actual implementation of the project, the project team must pay attention to compliance first. The preparation of declaration materials for different funding channel entities, responses to window opinions, and adjustments and improvements to the corresponding framework all require the full support of a professional legal team.

(The above image is a schematic diagram of the funding channel for RWA projects for reference only)

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。