Original Author: Kairos Research

Original Translation: Deep Tide TechFlow

Key Summary:

LRT may collaborate with centralized exchanges for integration and introduce the risk/return to market makers as liquidity providers in these centralized venues.

The liquidity of re-mortgaged tokens is not astonishingly good, but overall liquidity is acceptable. However, each individual LRT is associated with greater differences, which will continue to grow with different long-term agency strategies.

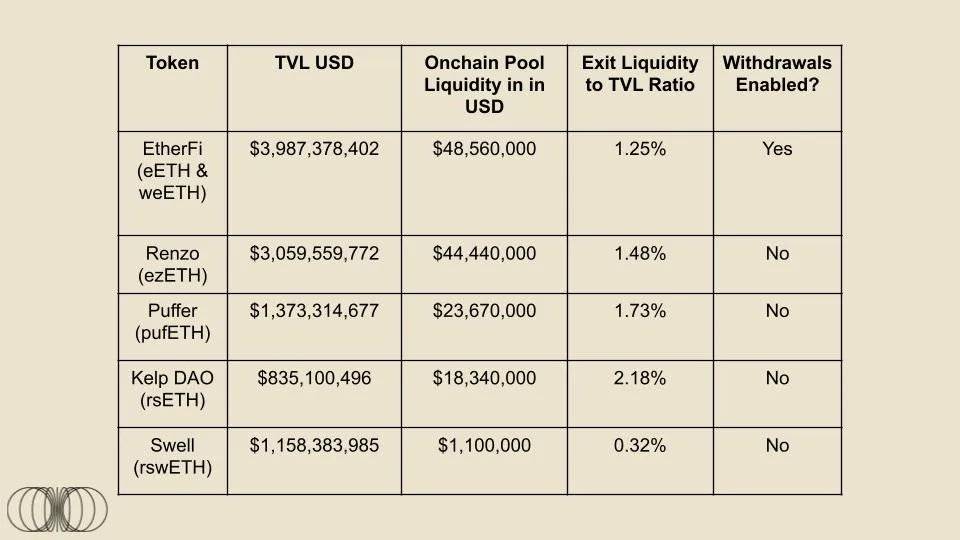

Except for EtherFi, none of these LRT providers have enabled withdrawal functions.

It is expected that liquidity re-mortgaging is a winner-takes-all market structure, and liquidity will bring more liquidity.

Text:

EigenLayer's first AVS officially launched on the mainnet.

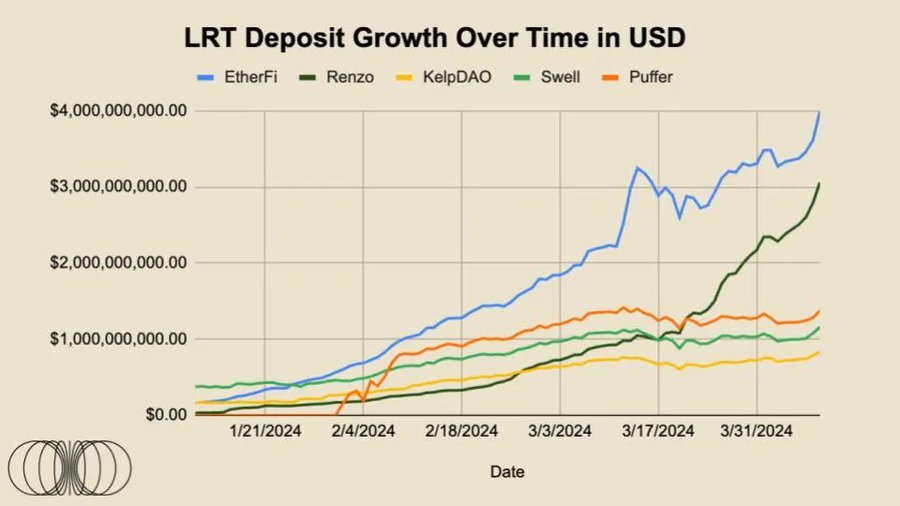

Today, EigenLabs' data availability AVS—EigenDA was released on the mainnet, officially marking the beginning of the re-mortgaging era. Although the EigenLayer market still has a long way to go, one trend is very clear: Liquidity Re-Mortgaging Tokens (LRT) will become the main way for re-mortgagers. Over 73% of all EigenLayer deposits are made through LRT, but how high is the liquidity of these assets? This report will delve into this issue and explain the subtle differences surrounding EigenLayer.

EigenLayer and Introduction of Liquidity Re-Mortgaging Tokens

EigenLayer achieves the reuse of ETH on the consensus layer through a new cryptographic economic tool called "re-mortgaging." ETH can be re-mortgaged on EigenLayer in two main ways: through native ETH re-mortgaging or using Liquidity Re-Mortgaging Tokens (LST). The re-mortgaged ETH is then used to secure other applications, known as Active Verification Services (AVS), allowing re-mortgagers to receive additional mortgage rewards.

The main complaint from users about mortgaging and re-mortgaging is the opportunity cost of mortgaging ETH. This issue is addressed by using Liquidity Re-Mortgaging Tokens (LST) for native ETH mortgaging, which can be seen as a flow receipt token representing the amount of ETH mortgaged by the user. The LST market on Ethereum is currently about $486.5 billion, the largest in the DeFi field. Today, LST accounts for about 44% of all Ethereum mortgages, and with the popularization of re-mortgaging, we expect the field of Liquidity Re-Mortgaging Tokens (LRT) to follow a similar, or even more aggressive, growth pattern.

While LRT shares some similarities with LST, they have distinct differences in their mission. The ultimate goal of each LST is essentially the same: to mortgage users' ETH and provide them with flow receipt tokens. However, for LRT, the ultimate goal is to delegate the user's mortgaged representation to one or more operators and then support a basket of AVS. Each individual operator can choose how to allocate their delegated mortgage among these various AVS. Therefore, the operator to whom LRT delegates their mortgage has a significant impact on the overall activity, operational performance, and security of re-mortgaged ETH. Finally, they must also ensure proper risk assessment of the unique AVS supported by each operator, as the risk reduction may vary depending on the services provided. Note that the risk reduction is essentially zero in the initial listing of most AVS, but over time, we will gradually see the "training wheels" being removed, making the mortgage market increasingly permissionless.

However, despite the differences in structural risk, one similarity remains unchanged: LRT reduces the opportunity cost of re-mortgaged capital by providing flow receipt tokens that can be used as productive collateral or exchanged for DeFi to reduce withdrawal periods. This is particularly important because one of the main advantages of LRT is to avoid traditional withdrawal periods, with EigenLayer having a withdrawal period of 7 days. Considering this core principle of LRT, we naturally expect to see net selling pressure on them, as the entry barrier for re-mortgaging is so low, but the exit barrier is so high, making the liquidity of these LRT their lifeline.

Therefore, as the total mortgage value of EigenLayer continues to rise, it is important to understand the driving factors behind the protocol's growth and how these factors will affect the inflows/outflows in the coming months. At the time of writing this article, 73% of EigenLayer deposits were made through Liquidity Re-Mortgaging Tokens. To put this into context, on December 1, 2023, LRT deposits were about $71.74 million. Today, on April 9, 2024, they have grown to about $10 billion, achieving an astonishing increase of over 13,800% in less than 4 months. However, as LRT continues to dominate the growth of EigenLayer's re-mortgaged deposits, there are some important factors to consider.

Not all LRTs are composed of the same underlying assets

There will be differences in the delegation of mortgages to AVS in the long term, but not much difference in the short term

Most importantly, there are significant differences in the liquidity characteristics of various LRTs

Given that liquidity is the most critical advantage of LRT, most of this report will focus on the last point.

The speculative nature of Eigen Points has greatly stimulated the bull market of current EigenLayer deposits, and we can assume that this will translate into some form of airdrop distribution for potential EIGEN tokens. Currently, no AVS rewards are ongoing, which means that there are no incremental returns on these LRTs other than natural mortgage rewards. In order to drive and maintain a total mortgage value of over $133.5 billion, the AVS market must naturally find a balance between the incremental returns required by re-mortgagers and the natural price that AVS are willing to pay for security.

For LRT depositors, we have already seen the huge success of EtherFi in launching the ETHFI governance token airdrop, currently valued at about $6 billion. Taking all these factors into account, it can be expected that after the launch of EIGEN and other expected LRT airdrops, some capital flows may gradually increase.

However, in terms of reasonable returns, users may find it difficult to find higher returns in the Ethereum ecosystem without involving EigenLayer. There are several interesting revenue opportunities in the Ethereum ecosystem. For example, Ethena is a synthetic stablecoin supported by mortgaged ETH, while also having hedged ETH futures short positions. The protocol currently offers an annualized yield of about 30% on its sUSDe product. In addition, as users become more familiar with interoperability and cross-chain bridging, seekers of returns may look elsewhere, potentially driving capital outflows from Ethereum's production.

Although somewhat complex, overall, we believe it is reasonable to assume that there will be no larger incremental mortgage return event than the potential EIGEN token airdrop to re-mortgagers, and large, blue-chip AVS that have already raised billions of dollars in high valuations in the private market may also issue their tokens to re-mortgagers. Therefore, it can be assumed that after these events, a certain proportion of ETH will flow out of the EigenLayer deposit contract through withdrawals.

Given that EigenLayer has a seven-day cooling-off period for withdrawals, and the vast majority of funds are re-mortgaged through LRT, the fastest way to exit will be to convert your LRT to ETH. However, there are significant differences in the liquidity characteristics of various LRTs, and many LRTs may not be able to be sold on the market price at a large scale. In addition, at the time of writing this article, EtherFi is the only LRT project that has enabled withdrawal functions.

We believe that if the trading price of LRT is lower than the price of its underlying assets, it may bring about painful arbitrage cycles for the re-mortgaging protocol. For example, if an LRT is traded at 90% of its underlying ETH value, market makers/arbitrageurs may buy the LRT and continue the redemption process. Assuming the price of ETH is hedged, they could potentially achieve a net profit of about 11.1%. The general rule of supply and demand is that LRT is more likely to face net selling pressure, as sellers may avoid the 7-day withdrawal queue. On the other hand, users seeking re-mortgaging may immediately deposit their ETH, so there is no benefit to buying LRT on the open market for the ETH they already own.

By the way, we expect that once multiple AVSs go live with protocol rewards and full implementation of reductions, the further choice between exiting or continuing re-mortgaging will ultimately depend on the incremental returns provided through re-mortgaging. We personally believe that many people underestimate the incremental returns provided through re-mortgaging. However, that's a topic for another time.

Data Tracking

The data section of this month's report will track the growth, adoption, and liquidity of the top five LRTs, as well as any notable news that we believe should be monitored.

LRT Liquidity and Trading Volume

Although mortgaging through LST and LRT has more critical advantages than traditional mortgaging, if LRT itself does not have sufficient liquidity, this utility will be almost completely undermined. Liquidity refers to the "efficiency or convenience of converting assets into cash without affecting their market price." LRT issuers must ensure that there is sufficient on-chain liquidity so that large holders can exchange receipt tokens in a liquidity pool with an asset value almost 1:1.

Each existing LRT has very unique liquidity characteristics. For various reasons, we expect these situations to continue:

Some protocols will provide liquidity for their LRT in the early stages to investors and users

Liquidity will be incentivized through subsidies, token issuance, bribery systems on-chain, or expected events such as "points"

Some protocols will have more complex, more concentrated liquidity providers who will maintain their LRT close to the pegged level with less USD liquidity

It is important to note that concentrated liquidity only works within a small price range, and any price movements beyond the selected range will have a significant impact on the price.

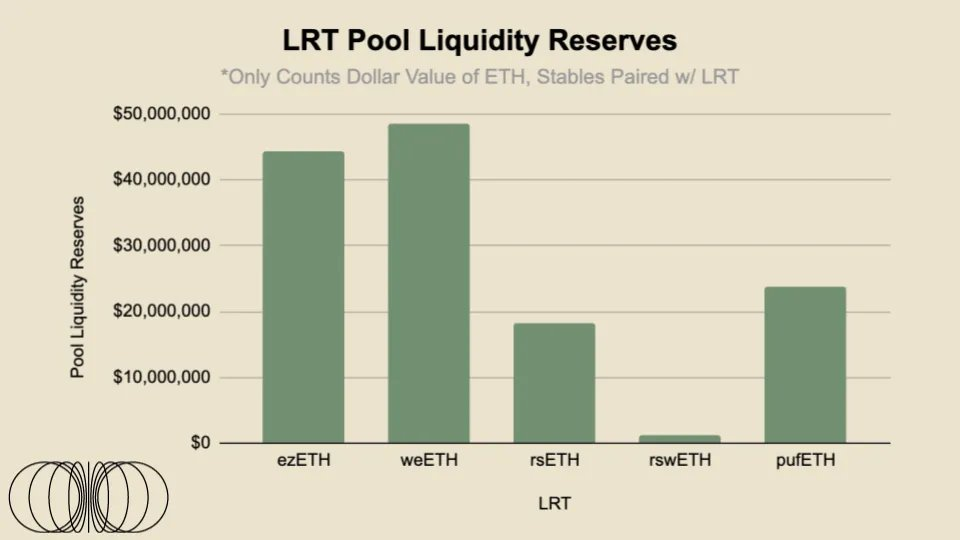

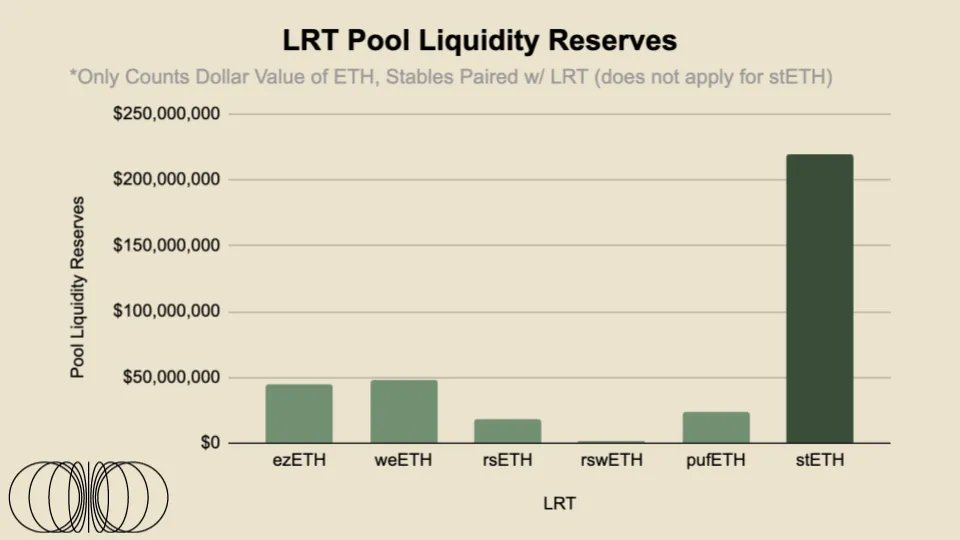

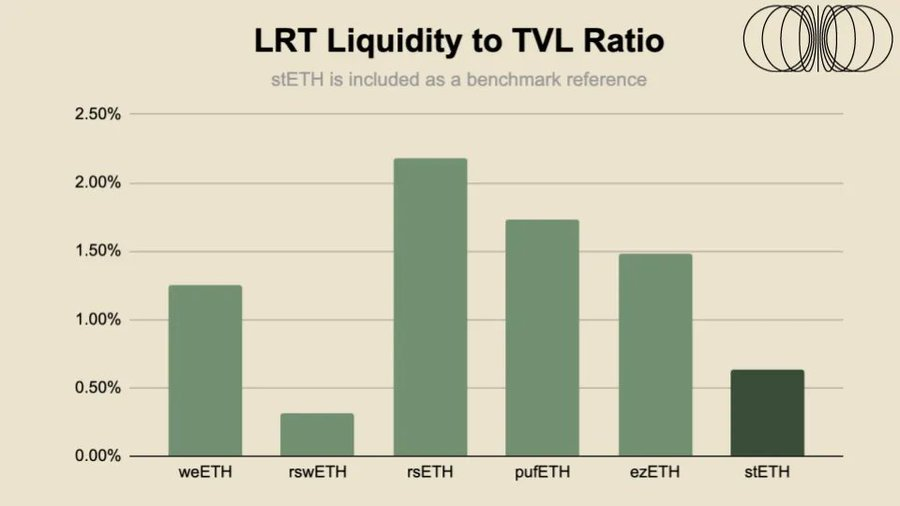

Below is a very simple analysis of the on-chain pool liquidity of the top five largest LRTs on the Ethereum mainnet (+ Arbitrum). Exit liquidity refers to the USD value of cash-like liquidity in the LRT liquidity pool.

For the top five largest LRTs, there is a total of over $136 million in liquidity available across Curve, Balancer, and Uniswap. However, to better understand how high the liquidity is for each LRT, we will apply a liquidity/market value ratio to each asset.

The liquidity ratio of LRT is not overly concerning compared to the top LST—stETH. However, given the increased re-mortgaging risk and the addition of a 7-day withdrawal period for Eigenlayer on Ethereum, the liquidity of LRT may be more important than the liquidity of LST. Additionally, stETH trades on several major centralized exchanges, with professional HFT firms managing the order book, meaning that the liquidity of stETH is far greater than what is seen on-chain. For example, there is approximately over $2 million of +-2% order book liquidity on OKX and Bybit. Therefore, we believe that LRT may also explore this path, collaborating with centralized exchanges for integration and introducing the risk/return to market makers as liquidity providers in these centralized venues. In next month's article, we will delve deeper into the allocation of stable pool liquidity, x*y=k liquidity, and concentrated liquidity among top LRT trading pairs.

LRT Anchoring Data

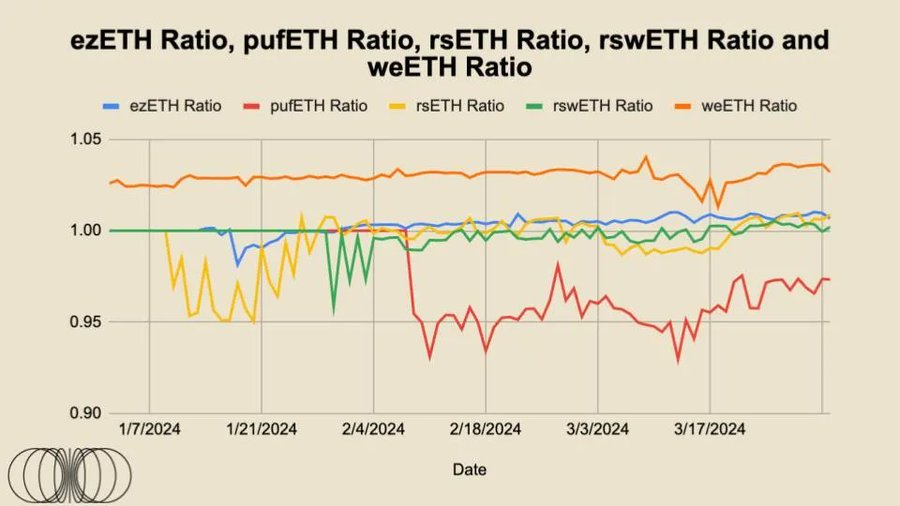

From the above chart, it can be seen that the trading prices of rsETH, rswETH, and ezETH are relatively close to a 1:1 ratio with ETH, with a slight premium. Given that these tokens are non-interest-bearing tokens, unlike stETH, they automatically compound interest rewards, which are then reflected in the token prices. This is why the current price of 1 wstETH is approximately 1.16 ETH. In theory, over time, the "fair value" should continue to increase, as it is determined by time*mortgage rewards, and this will then be reflected in the increasing fair value of these tokens.

Anchoring these LRTs is crucial, as they essentially represent the level of trust market participants have in the project as a whole, directly determined by the capital invested or arbitrageurs willing to trade these premiums and discounts to maintain the token's trading "fair value." Please note that all of these tokens are non-base tokens, meaning they automatically compound and are traded based on the redemption curve.

It can be seen that for ezETH and weETH, the two LRTs with the strongest liquidity, their trading has been relatively stable for a period, mostly in line with fair value. The slight deviation of EtherFi's ezETH from fair value is mainly due to the launch of its governance token, opportunistic airdrop hunters exchanging out of this token, and naturally, other market participants joining in the trading to exchange for discounted arbitrage. We may see similar events occur after Renzo launches its governance token.

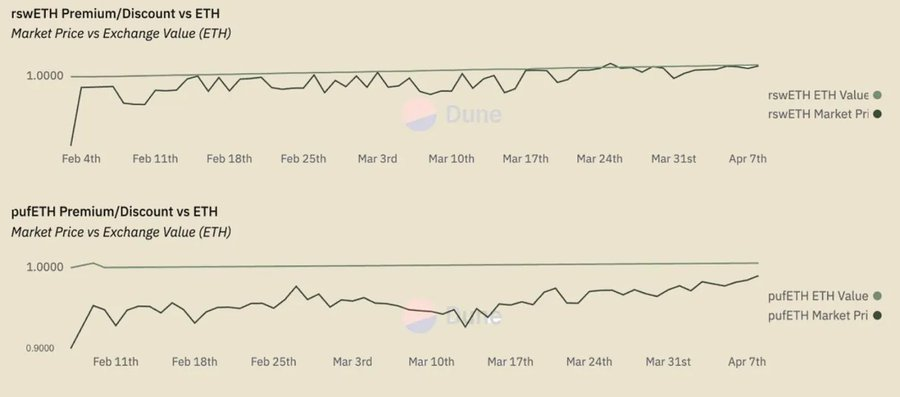

KelpDAO's rsETH initially traded at a discount relative to fair value upon launch but gradually steadied back to a level in line with fair value.

As for rswETH, it has traded at a price lower than its fair value for most of the time, but recently seems to have reached a level in line with its fair value. Among all these LRTs, pufETH is the main outlier, as it has only traded at a discount. However, this trend seems to be coming to an end, as it is moving towards a level in line with its fair value based on the underlying asset.

It should be noted that, except for EtherFi, none of these LRT providers have enabled withdrawal functionality. We believe that ample liquidity combined with the ability for users to withdraw at any time will provide a strong attraction for market participants, meaning a significant portion of liquidity needs to be sourced from the broader DeFi ecosystem.

LRT in the Wider DeFi Ecosystem

As LRT becomes further integrated into the broader DeFi ecosystem, especially in the lending markets, the importance of its pegging will significantly increase. For example, in the current money markets, LST (especially wstETH/stETH) is the largest collateral asset on Aave and Compound, with supplies of approximately $4.8 billion and $2.1 billion, respectively. As LRT becomes more integrated into the wider DeFi ecosystem, we expect these numbers to eventually surpass the supply of LST, especially as the broader market deepens its understanding of risk and product structures, and as they become more long-term trusted over time. Additionally, both Compound and Aave have governance measures for joining Renzo's ezETH.

However, as mentioned earlier, liquidity will still be the lifeline of these products to ensure the breadth and depth of their DeFi integration and long-term viability. We have seen that decoupling events for LST can trigger a series of chaos, click here to read more.

Closing Thoughts

Although stETH has gained early advantages and dominated due to its first-mover advantage, the range of LRTs mentioned in this report were all launched roughly at the same time and have strong market momentum. We expect this to be a winner-takes-all market structure, as the power law applies to most liquidity assets; simply put, liquidity begets liquidity. This is why Binance continues to dominate CEX market share, despite various doubts and turmoil.

In conclusion, the liquidity of re-mortgaged tokens is not astonishing. The liquidity is decent, but each individual LRT has greater differences associated with it, which will continue to grow with different long-term agency strategies. From a psychological model perspective, it may be easier for first-time users to view LRT as collateral ETFs. Many will vie for the same market share, but in the long run, allocation strategies and fee structures may be the determining factors. Additionally, as products become more differentiated, liquidity will become more important, especially due to the length of withdrawal periods. In the cryptocurrency space, seven days sometimes feels like a month in normal time, as global markets operate 24/7. Finally, as these LRTs begin to integrate into the lending markets, pool liquidity will become more important, as liquidators are only willing to take on an acceptable level of risk due to the differing liquidity conditions of the underlying collateral. We believe token incentive mechanisms may play a crucial role in this, and we look forward to delving into different token models after potential airdrops by other LRT providers.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。